Download presentation

Presentation is loading. Please wait.

3

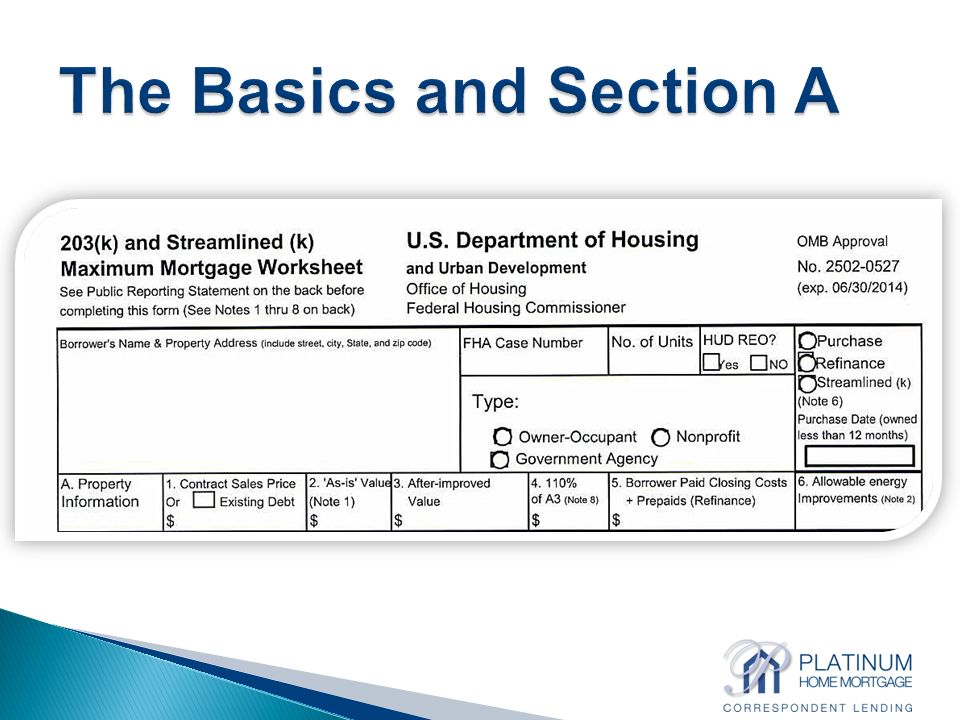

A1 - Contract Sales Price or Existing Debt Purchase: Contract sales price of the property Refinance: The amount of the existing debt HUD REO: FHA Sales Contract A2 - ‘As-Is’ Value Sales price of the home Sales price of the home HUD REO – Original listing price by HUD Refinance - if the property has been owned less than one full year, use the lesser of the ‘as-is’ value or the original acquisition cost, plus any debts incurred for renovation, since the acquisition. Refinance - if the property has been owned less than one full year, use the lesser of the ‘as-is’ value or the original acquisition cost, plus any debts incurred for renovation, since the acquisition.

4

A3. After-Improved Value This value will come from the new 203(k) appraisal. The appraisal should represent the appraiser's estimate of the property's value after completing the proposed project presented in the Consultant’s Work Write-Up or Contractors bids (Streamlined 203(k) only ) A4. 110% After-Improved Value The After-Improved Value multiplied by 110% Condominiums can not go over 100%. Condominiums can not go over 100%.

only ) A4. 110% After-Improved Value The After-Improved Value multiplied by 110% Condominiums can not go over 100%. Condominiums can not go over 100%..")

5

A5. Borrower Paid Closing Costs & Prepaids (Refinances Only) These figures should come from the Good Faith Estimate. It should include FHA Allowable Closing Costs and Prepaids. A6. Allowable Energy Improvements The Allowable Energy Improvements, will be determined by the Home Energy Rating Systems (HERS) report and will consist of those items that will return a measurable savings in energy costs, over the life of the improvement.

These figures should come from the Good Faith Estimate. It should include FHA Allowable Closing Costs and Prepaids. A6. Allowable Energy Improvements The Allowable Energy Improvements, will be determined by the Home Energy Rating Systems (HERS) report and will consist of those items that will return a measurable savings in energy costs, over the life of the improvement..")

6

Scenarios where Energy Efficiency Improvements can be used… If borrower is having difficulty qualifying, approved energy efficient improvements are not included in the borrower’s debt to income ratio. If the loan amount exceeds the maximum mortgage for the area, the borrower can exceed the loan limits by the exact dollar amount of approved energy efficient improvements. If borrower is doing a Streamlined 203(k), the approved energy efficient improvements are not included in the $35,000 maximum (line B14).

, the approved energy efficient improvements are not included in the $35,000 maximum (line B14)..")

8

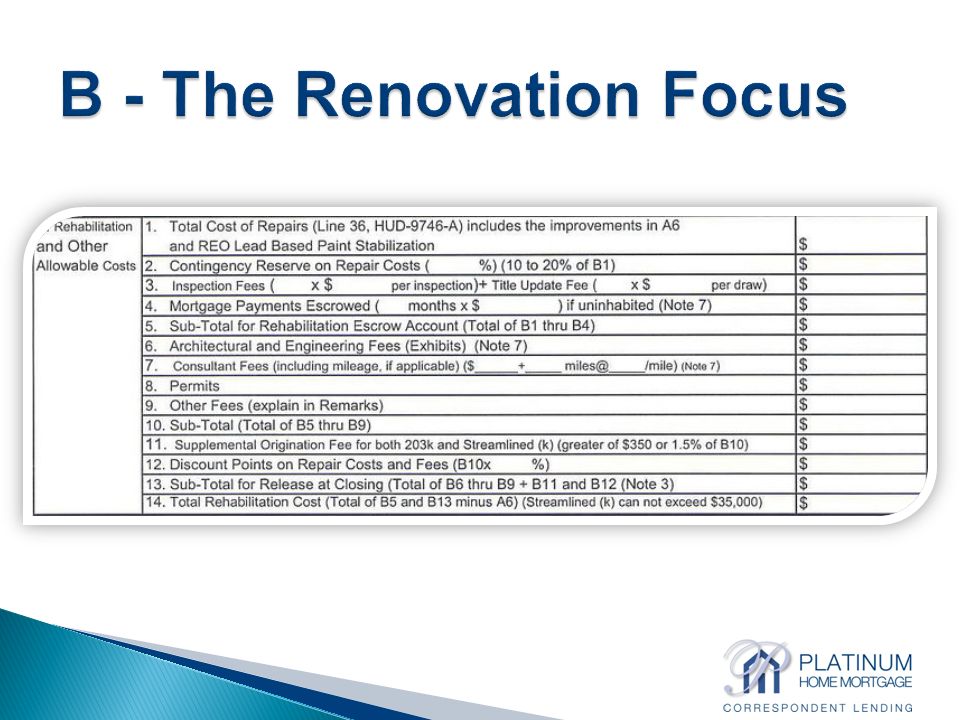

B1 Total Cost of Repairs (includes repairs in A6 and REO lead based paint stabilization) Once the signed Specifications of Repairs, has been reviewed or completed by the HUD Consultant, they sign a template Draw Request form (HUD-9746-A) stating that they have personally inspected the property. This needs to be an original signature and not reproduced or “e-signed”. On a Standard 203(k) the total costs estimated amount on the Draw Request form (Line 36), is entered on B1. The contractor’s estimates would be used on a 203(k) streamline since the draw request form isn’t required. If this is a HUD REO property, the estimated costs for lead based paint stabilization are included which may be different from the HUD credit.

the total costs estimated amount on the Draw Request form (Line 36), is entered on B1. The contractor’s estimates would be used on a 203(k) streamline since the draw request form isn’t required. If this is a HUD REO property, the estimated costs for lead based paint stabilization are included which may be different from the HUD credit..")

9

Protects the borrower from any unforeseen problems or those items that could not have been anticipated or revealed before commencement of the renovation process. Can be used for health, safety, and necessity items or for additional improvements with Standard 203(k). This amount should be between 10% and 20% of the renovation amount as determined by the DE Underwriter after considering the recommendation of the FHA Consultant. If the utilities are off when the property is inspected, the contingency reserve must be 15%.

. This amount should be between 10% and 20% of the renovation amount as determined by the DE Underwriter after considering the recommendation of the FHA Consultant. If the utilities are off when the property is inspected, the contingency reserve must be 15%..")

10

The contingency reserve amount, can be paid in cash. In this case, if the contingency reserve is paid in cash, enter a "0" on this line. In the remarks sections, make a note that the contingency has been paid in cash and list the dollar amount paid, as it must be placed in the repair escrow account at closing. If the contingency reserve comes from someone other than the borrower, document the file with the donor’s name. Funds put up in cash, can be returned to the contributor, if they are not used.

11

Inspection Fees The number of inspections allowed on a project will depend on the scope of the work. Title Update Fees Lien waivers are acceptable for interim draws where the lien law does not require a title endorsement. A final title update/endorsement is required for the final disbursement.

12

The borrower is permitted to finance up to 6 months of mortgage payments on a Standard 203(k). This is allowed ONLY when the property is vacant and the work is not completed If the property is occupied or the work is complete before using all of these funds any unused mortgage payments will be paid down on the principal. Principal, interest, taxes and insurance for the hazard and monthly MIP payments can be included in the mortgage payment.

13

B5. Subtotal (B1-B4) B6. Architectural and Engineering Fees Blueprints and drawings for additions and structural changes that are needed can be prepared by outside professionals. The costs can be financed by the borrower

14

The consultant, will complete an inspection of the property to determine what work needs to be completed. The borrower will work with the consultant to incorporate what they want to do to the property. The consultant will complete the work write-up, in an acceptable format, and prepare the cost estimate so the after-improved appraisal can be completed and the borrower can shop for a contractor. Mileage can be charged when over 30 miles round trip at the IRS rate of 56 cents/mile.

15

Cost of RepairsFee < $7,500.00$400.00 < $15,000.00$500.00 <$30,000.00$600.00 < $50,000.00$700.00 < $75,000.00$800.00 <$100,000.00$900.00 > $100,000.00$1,000.00 NOTE: An additional $100.00 can be charged by the Consultant, if the Borrower wishes to have them complete, a feasibility study, prior to submitting a sales contract, to a seller. Also, an additional fee of $25 can be charged for each additional unit.

16

B8. Permits Building permits can be financed and should be shown on this line. All permits must be in place prior to the first release. B9. Other Fees (explain in Remarks) Any fees that are necessary, in order to complete the reconstruction (i.e. Construction fees and structural certifications), can be financed and should be shown on this line. Explain what the fees are in the remark section.

Any fees that are necessary, in order to complete the reconstruction (i.e. Construction fees and structural certifications), can be financed and should be shown on this line. Explain what the fees are in the remark section..")

17

B10.Subtotal (B5-B9) B11.Supplemental Origination Fee The supplemental origination fee, is calculated as 1½ % of the amount in B10, or $350 whichever is greater and should be shown on this line.

B11.Supplemental Origination Fee The supplemental origination fee, is calculated as 1½ % of the amount in B10, or $350 whichever is greater and should be shown on this line.")

18

Discount points on the portion of the mortgage amount allocated to rehabilitation can be financed on a 203(k). The number of discount points, being financed on the rehabilitation costs cannot exceed those being charged on the total mortgage amount and is a portion of the total discount charged. The borrower may choose to finance the discount attributable to that rehab portion of the loan or pay it in cash.

19

Only those items in this subtotal and below can be released at the closing if there is a paid receipt or invoice to be paid (Total B6 thru B9 + B11 and B12)

")

20

Total Rehabilitation Funds (B5 + B13- A6) Streamlined (k) can not exceed $35,000.

Streamlined (k) can not exceed $35,000.")

22

C1Lesser of Sales Price (A1) or As-Is Value (A2) $______________ C2Total Rehabilitation Cost (B14) $______________ C3Lesser of sum of C1+C2 or 110% of after improved value (A4) __________________ C1 __________________ C1 +__________________ C2 =__________________ Total OR __________________ A4 (whichever is less) $______________

or As-Is Value (A2) $______________ C2Total Rehabilitation Cost (B14) $______________ C3Lesser of sum of C1+C2 or 110% of after improved value (A4) __________________ C1 __________________ C1 +__________________ C2 =__________________ Total OR __________________ A4 (whichever is less) $______________")

23

C4Maximum Mortgage Amount ____________________ C3 ____________________ C3 Required Adjustments +/-____________________ Required Adjustments +/-____________________ =___________________ Total X LTV factor 96.5% OR less ____________-______ allowable down payment (like HUD $100 down)$___________________

$___________________")

25

$________________________ A1 (Existing Debt) +$________________________ B14 (Rehabilitation Cost) +$________________________ A5 (Borr Paid CC & PPds) $________________________ Discount on total loan amt minus B12 financed discount on the rehabilitation -$________________________ FHA MIP refund The discount on the refinance, is calculated by multiplying the number of discount percentage points, by the whole loan amount. The discount on the repairs, has already been calculated and added to the loan, on Line B12. By subtracting the discount on repairs, from the total discount to be collected, an accurate cash discount amount is determined.

26

D2. Lesser of sum of "As-Is" Value (A2) + Rehabilitation Costs (B14) OR 110% After-Improved Value (A4) Note : Reminder that if the property is owned less than 1 year, you must use the lesser of the current "As Is Value" or the original cost of the property, plus documented renovation since acquisition. $_______________________ A2 (As-Is Value) $_______________________ A2 (As-Is Value) + $_______________________ B14 (Rehabilitation Costs) = $_______________________ OR OR $_______________________ A4 $_______________________ A4

+ Rehabilitation Costs (B14) OR 110% After-Improved Value (A4) Note : Reminder that if the property is owned less than 1 year, you must use the lesser of the current As Is Value or the original cost of the property, plus documented renovation since acquisition. $_______________________ A2 (As-Is Value) $_______________________ A2 (As-Is Value) + $_______________________ B14 (Rehabilitation Costs) = $_______________________ OR OR $_______________________ A4 $_______________________ A4.")

27

D3. $____________________D2 x LTV Factor (97.75%) D4. Maximum base mortgage amount lesser of D1 or D3

29

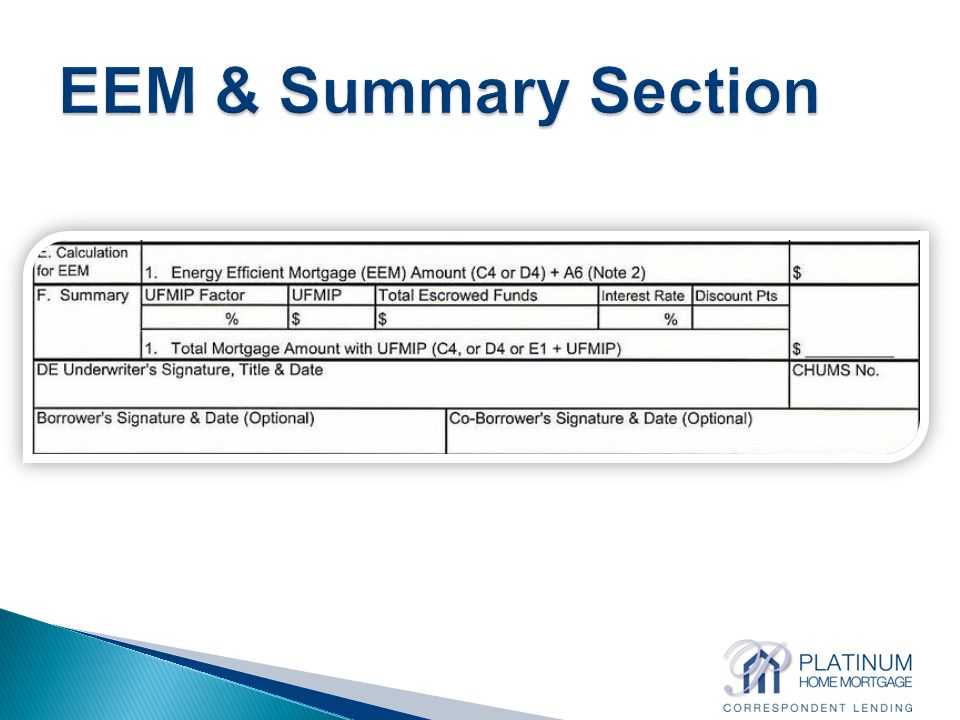

Section E: Energy Efficiency Mortgage (EEM) Amount (C4 or D4) + A6 This is the final step, in the calculation of the mortgage amount, used ONLY when an energy efficiency mortgage, is being done in conjunction with the 203(k) rehabilitation loan. The calculation of mortgage amount completed in C4 or D4, is the mortgage amount, for which the Borrower must credit qualify. The amount calculated in E1, MAY exceed the statutory loan limit, but it cannot exceed 110% of the After Improved Value from A4.

30

Section: Remarks This area, is to be used to communicate additional information, on the details of the loan. This is the place, to convey the information about the specific items that have been paid in cash and by whom, so that if they remain unused, they can be given back to the donor. Only cash put up by the borrower, will be returned to the borrower! This is also the spot for the Underwriter to comment about reducing the mortgage amount or other changes to the calculated numbers.

31

The ‘Total Escrowed Funds’ box, in section F, should include the following: $_____________________________ B14 - Total Rehab Costs plus$_____________________________A6 - Energy Improvement Escrow Funds Plus$_____________________________ Cash Escrowed Items =$_____________________________ Total Repair Escrow Funds ML 95-40 added two boxes to the remarks section, to state the interest rate, on the loan and the number of discount points, being charged, excluding the origination fee.

32

Problem #1 – Purchase transaction Purchase is $100,000 After Improved Value is $200,000 Estimate of repairs $60,000 15% Contingency reserve will be required Four inspections at $125 One title update $75 Architectural fee $1,000 The consultant fee $800 Building Permit will cost $250

33

Problem #2 – Refinance transaction Borrowers have lived in property for 5 years and currently have a conventional loan. Existing debt is $150,000 “As-Is” appraised Value is $180,000 The estimated “As-Completed” value of the property is $300,000 Closing costs are $6,750 and prepaids are $3,250 Estimates cost of repairs is $70,000 15% contingency reserve Five inspections at $125 a piece and one title update at $75 The consultant fee $700 Building permit fees are $350

Similar presentations

249-1800,>")

& 203(k) Training Presents July 20, 2011.>")

LOANS With Tim Pascarella.>")

. FHA Streamlined 203(k) Review What is the FHA Streamlined 203(k) Loan Program? What are the program guidelines? What types of.>")

Loan Program 8/7/14.>")

Simple Process For Simple Repairs.>")

Applicant Workshop January 30, 2010.>")