Download presentation

Presentation is loading. Please wait.

1

Andrew F. Brathwaite Cyril Soeri June 2014

2

IFRS for SMEs Exposure Draft ◦ Questions ◦ Proposed amendments ◦ Other IASB Guide for Micro-sized Entities applying the IFRS for SMEs

3

Standard issued by IASB July 2009 Request for Information issued June 2012 as part of comprehensive review ED published October 2013 Only limited amendments proposed, to clarify existing requirements or add guidance Comment period ended March 3, 2014 (58 responses) Few significant new issues identified Final amendments expected in second half of 2014

Few significant new issues identified Final amendments expected in second half of 2014")

4

Changes (5) New and revised IFRSs (13) New guidance (7) Minor clarification (21) New exemptions (5) Disclosure (3) SMEIG Q&A (3)

New and revised IFRSs (13) New guidance (7) Minor clarification (21) New exemptions (5) Disclosure (3) SMEIG Q&A (3)")

5

An entity has public accountability if: its debt or equity instruments are traded in a public market…, or it holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses. This is typically the case for banks, credit unions, insurance companies, securities brokers/dealers, mutual funds and investment banks.

6

Section 29 Income Tax based on March 2009 Exposure Draft which was never finalized Proposal to align main principles of Section 29 Income Tax with IAS 12 Income Taxes Retain some presentation and disclosure simplifications Taxes payable approach will not be permitted but IASB open to simplifications

7

Proposed that: ◦ effective date be one year after final amendments are issued ◦ Early adoption be permitted Tentative plan for revisions every three years unless earlier amendment warranted ◦ Feedback received in favour of five year cycle with urgent issues being addressed earlier where warranted

8

Reword: “ Most this is typically the case for banks, credit unions, insurance companies, securities brokers/dealers, mutual funds and investment banks will meet this second criterion” Use of IFRS for SMEs in separate financial statements of parent company

9

… if obtaining or determining the information necessary to comply with the requirement would result in excessive incremental cost or an excessive additional effort for an SME.. Undue cost or effort depends on the entity’s specific circumstances and on management’s judgment when assessing the costs and benefits. 9

10

Existing exemptions: ◦ Measurement of investment property at fair value ◦ Disclosing estimate of financial effect of contingent assets ◦ Use of projected unit credit method to measure defined benefit obligation ◦ Measuring biological assets under fair value model

11

Additional proposed exemptions: ◦ Measurement of investments in equity instruments at fair value ◦ Recognition of intangible assets separately in a business combination ◦ Requirement to offset income tax assets and liabilities

12

Clarification that the single amount presented for discontinued operations includes any impairment of the discontinued operation measured; Incorporation of the main change under IAS 1 (2011 amendment) Presentation of Items of Other Comprehensive Income, which requires entities to group items presented in other comprehensive income (OCI) on the basis of whether they are potentially reclassifiable to profit or loss.

Presentation of Items of Other Comprehensive Income, which requires entities to group items presented in other comprehensive income (OCI) on the basis of whether they are potentially reclassifiable to profit or loss.")

13

The financial statements of the parent and its subsidiaries used in the preparation of the consolidated financial statements shall be prepared as of the same reporting date unless it is impracticable to do so. If it is impracticable to prepare the financial statements of a subsidiary as of the same reporting date as the parent, the parent shall consolidate the financial information of the subsidiary using the most recent financial statements of the subsidiary, adjusted for the effects of significant transactions or events that occur between the date of those financial statements and the date of the consolidated financial statements.

14

Modification to require that if an entity is unable to make a reliable estimate of the useful life of an intangible asset, the useful life should not exceed 10 years, rather than be fixed at 10 years.

15

Active market: ◦ A market in which transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis. Transaction costs (financial instruments): ◦ Incremental costs that are directly attributable to the acquisition, issue or disposal of a financial instrument. ◦ An incremental cost is one that would not have been incurred if the entity had not acquired, issued or disposed of the financial instrument.

: ◦ Incremental costs that are directly attributable to the acquisition, issue or disposal of a financial instrument. ◦ An incremental cost is one that would not have been incurred if the entity had not acquired, issued or disposed of the financial instrument..")

17

Many requirements of IFRS for SMEs will not be relevant to micro-sized entities (‘micro entities’) as they generally only encounter a narrow range of simple transactions. This Guide is intended to help micro entities that are within the scope of the IFRS for SMEs, ie who do not have public accountability, and are either required to prepare general purpose financial statements in accordance with the IFRS for SMEs as issued in July 2009 (for example, under the law in their jurisdictions) or choose to do so, to identify more easily the requirements of the IFRS for SMEs that are relevant to them. It is not a separate Standard for micro entities. This Guide is not intended for micro entities preparing financial statements solely for taks reasons or to comply with local laws (unless local laws require micro entities to use the IFRS for SMEs). However, those micro entities may still find this Guide helpful in preparing such financial statements.

or choose to do so, to identify more easily the requirements of the IFRS for SMEs that are relevant to them. It is not a separate Standard for micro entities. This Guide is not intended for micro entities preparing financial statements solely for taks reasons or to comply with local laws (unless local laws require micro entities to use the IFRS for SMEs). However, those micro entities may still find this Guide helpful in preparing such financial statements..")

25

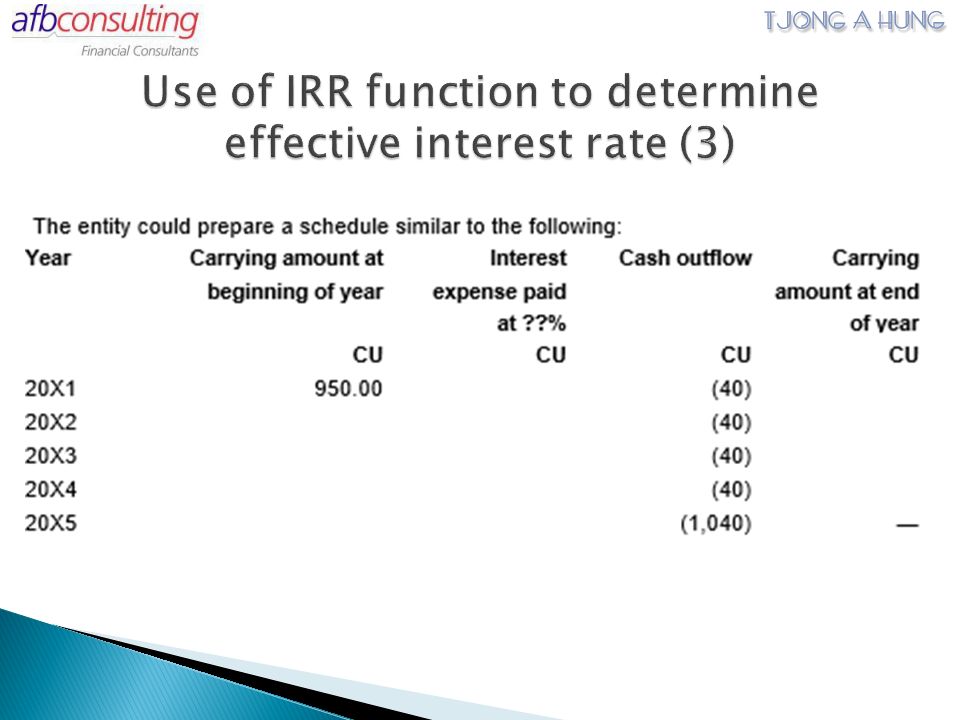

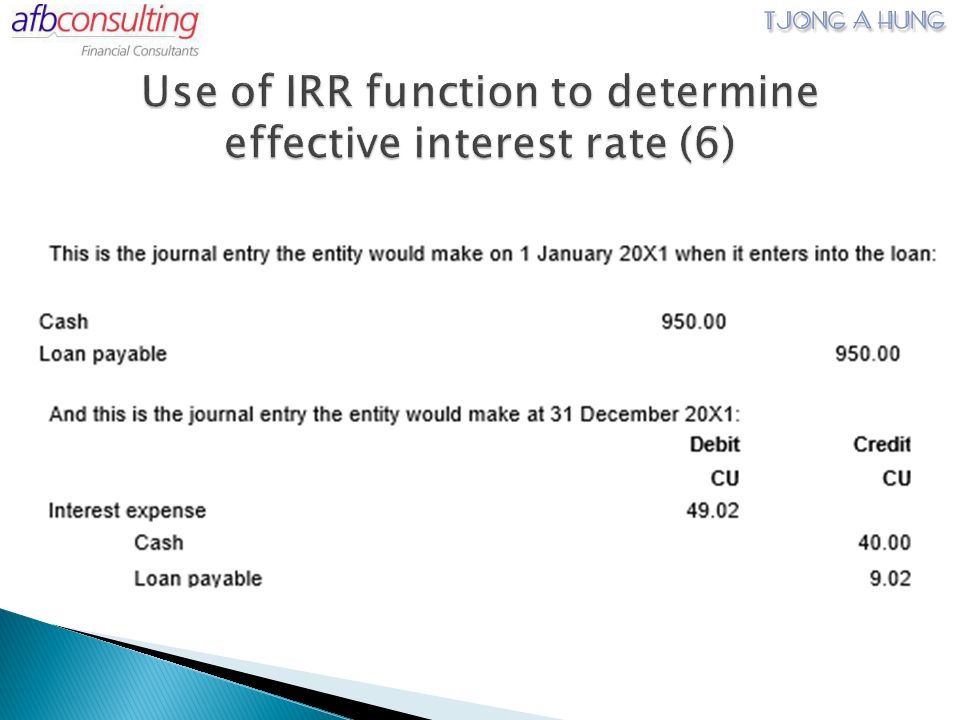

The effective interest rate (see paragraph G105) can be determined using the ‘Internal Rate of Return’ function in an Excel spreadsheet. This is illustrated below using the example of a five-year bank loan. Additional help can be found using the help function in Excel. On 1 January 20X1, an entity obtains a five-year CU1,000 loan from a bank, paying bank administration fees of CU50, so that the net cash received is CU950. The entity is required to pay cash interest of 4 per cent annually in arrears (= 4% × CU1,000 = CU40). The entity is required to repay the loan of CU1,000 to the bank on 31 December 20X5.

. The entity is required to repay the loan of CU1,000 to the bank on 31 December 20X5..")

26

The effective interest rate (see paragraph G105) can be determined using the ‘Internal Rate of Return’ function in an Excel spreadsheet. This is illustrated below using the example of a five-year bank loan. Additional help can be found using the help function in Excel. On 1 January 20X1, an entity obtains a five-year CU1,000 loan from a bank, paying bank administration fees of CU50, so that the net cash received is CU950. The entity is required to pay cash interest of 4 per cent annually in arrears (= 4% × CU1,000 = CU40). The entity is required to repay the loan of CU1,000 to the bank on 31 December 20X5.

. The entity is required to repay the loan of CU1,000 to the bank on 31 December 20X5..")

31

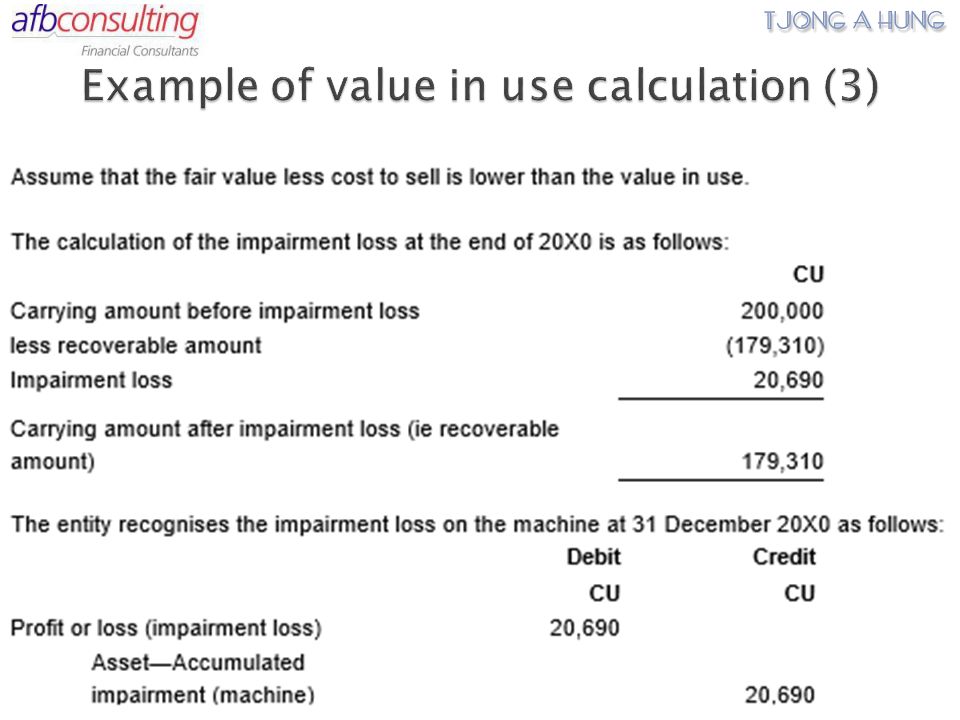

At the end of 20X0 an entity tests a machine for impairment. The machine was bought five years earlier for CU300,000, when its useful life was estimated to be 15 years and the estimated residual value was nil. At 31 December 20X0, after recognising the depreciation charge for 20X0, the machine’s carrying amount was CU200,000 and its remaining useful life was estimated at 10 years. The machine’s value in use is calculated using a pre-tax discount rate of 14 per cent per year. Budgets approved by management reflect expected cash inflows net of the estimated costs that are necessary to maintain the level of economic benefit that is expected to arise from the machine in its current condition. Assume, for simplicity, that the expected future cash flows occur at the end of each reporting period.

34

IFRS FOR SMEs Update

Similar presentations

,>")

>")

1 International Financial Reporting Standards IFRS for SMEs Joint DUBAI SME-ASCA-IFRS Foundation Workshop.>")