Download presentation

Presentation is loading. Please wait.

1

Review Ch. 4, Ch. 12, Ch. 13

2

Chapter 4 Outline 1.What is financial planning 2.Financial planning models 3.The percentage of sales approach 4.External financing and growth 5.Caveats in financial planning 2

3

Percentage of sales approach: COMPUTERFIELD CORPORATION Financial Statements Income statementBalance sheet Sales$8,000C AC A $5000Debt$8250 Costs5,800FA $7000Equity$3750 Net Income$2,200Total$12000Total$12000 3

4

EFN and Capacity Usage Suppose COMPUTERFIELD is operating at 80% capacity: 1. What would be sales at full capacity? (1p) 2. What is the capital intensity ratio at full capacity? (1p) 3. What is EFN at full capacity and Dividend payout ratio is 15%? (1p) What is EFN to increase sales to 12000 and Dividend payout ratio is 35%? 4

2. What is the capital intensity ratio at full capacity. (1p) 3. What is EFN at full capacity and Dividend payout ratio is 15%. (1p) What is EFN to increase sales to and Dividend payout ratio is 35%. 4.")

5

Q 1:8,000/.8=10,000; Full capacity as increase 10,000/8,000 = 1.25 (25%) Income statement Sales $8,000 Costs $5,800 N I $2,200 Ret earnings 2,200*.85=1,870 New Ret earnings 1,870*1.25=2,337.5 There is no indication that any changes took place in % cost for the proforma income statement, we can get the same result by increasing RE or by creating proforma IS 13-5

Income statement Sales $8,000 Costs $5,800 N I $2,200 Ret earnings 2,200*.85=1,870 New Ret earnings 1,870*1.25=2,337.5 There is no indication that any changes took place in % cost for the proforma income statement, we can get the same result by increasing RE or by creating proforma IS 13-5")

6

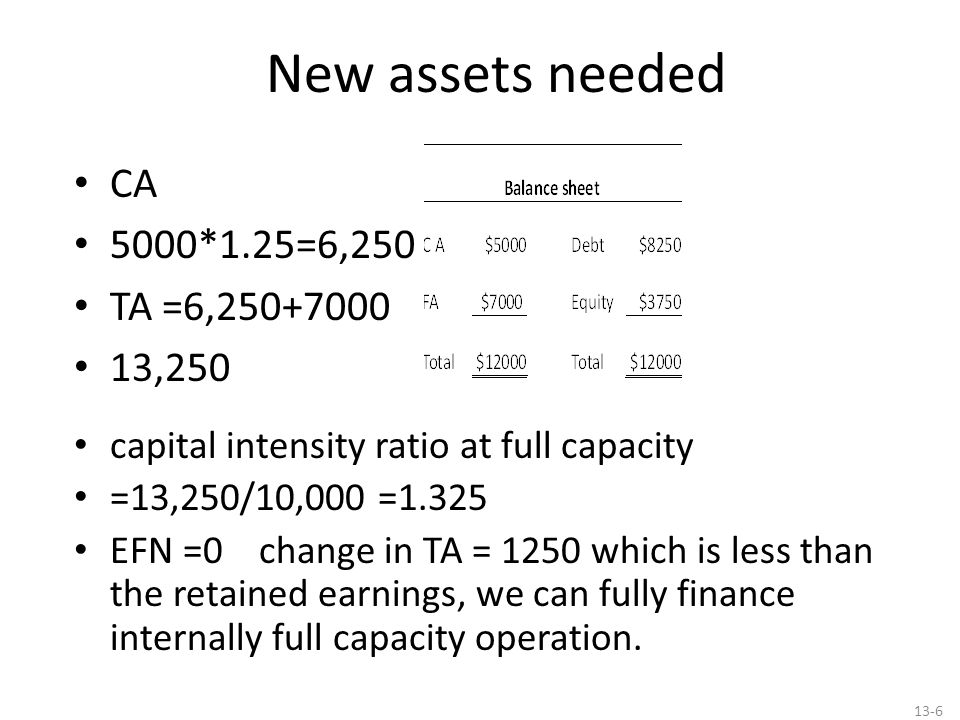

New assets needed CA 5000*1.25=6,250 TA =6,250+7000 13,250 capital intensity ratio at full capacity =13,250/10,000 =1.325 EFN =0 change in TA = 1250 which is less than the retained earnings, we can fully finance internally full capacity operation. 13-6

7

What is EFN to increase sales to 12,000 (50%) and Dividend payout ratio is 35%? Income statement Sales $8,000 Costs $5,800 N I $2,200 Ret earnings 2,200*.65=1,430 New Ret earnings 1,430*1.5=2,145 There is no indication that any changes took place in % cost for the proforma income statement, we can get the same result by increasing RE or by creating proforma IS 13-7

8

Recent Sales 8,000; Proj. Sales 12,000 Increase 50% CA 5,000*1. 5=7,500 FA=7,000+1,400 TA =15,900 FA=7000/10000 per unit of sales=.7 Inv. Need for 2000 more units of sales =.7*2000=1,400 EFN=1,755 change in TA = 3,900 from RE=2,145 13-8

9

EFN=1,755 D/E ratio =3/2 EFN=1,755 How much debt should be issued? How much equity? If they issue only debt (all 1,755 in bonds) what will be the D/E ratio on the proforma BS? D=8,250+1,755=10,005 E=3,750+2,145=5,895 D/E=1.69 13-9

what will be the D/E ratio on the proforma BS. D=8,250+1,755=10,005 E=3,750+2,145=5,895 D/E=")

10

Please, Review also Internal Growth Rate Sustainable Growth Rate

11

Chapter 12 Overview Return of an investment: arithmetic and geometric The variability of returns Efficiency of capital markets 11

12

Arithmetic vs. Geometric Averages (1) Geometric return = the average compound return earned per year over multiyear period Arithmetic average return = the return earned in an average (typical) year over a multiyear period 12 Geometric average return =

Geometric return = the average compound return earned per year over multiyear period Arithmetic average return = the return earned in an average (typical) year over a multiyear period 12 Geometric average return =.")

13

The Variability of Returns Variance = the average squared deviation between the actual return and the average return Standard deviation = the positive square root of the variance 13

14

The Normal Distribution (2) 14

14")

15

Z-score For any normal random variable: Z – z-score X – normal random variable - mean 15

16

Chapter 13 Outline Expected Returns and Variances of a portfolio Announcements, Surprises, and Expected Returns Risk: Systematic and Unsystematic Diversification and Portfolio Risk Systematic Risk and Beta The Security Market Line (SML)

")

17

Portfolios The risk-return trade-off for a portfolio is measured by the portfolio expected return and standard deviation, just as with individual assets 17 Portfolio = a group of assets held by an investor Portfolio weights = Percentage of a portfolio’s total value in a particular asset

18

Portfolio Expected Returns (1) The expected return of a portfolio is the weighted average of the expected returns for each asset in the portfolio You can also find the expected return by finding the portfolio return in each possible state and computing the expected value 18

The expected return of a portfolio is the weighted average of the expected returns for each asset in the portfolio You can also find the expected return by finding the portfolio return in each possible state and computing the expected value 18")

19

Calculate Portfolio Variance Portfolio variance can be calculated using the following formula: Correlation is a statistical measure of how 2 assets move in relation to each other If the correlation between stocks A and B = -1, what is the standard deviation of the portfolio? 19

20

Portfolio Diversification 20

21

Measuring Systematic Risk Beta (β) is a measure of systematic risk Interpreting beta: – β = 1 implies the asset has the same systematic risk as the overall market – β < 1 implies the asset has less systematic risk than the overall market – β > 1 implies the asset has more systematic risk than the overall market 21

is a measure of systematic risk Interpreting beta: – β = 1 implies the asset has the same systematic risk as the overall market – β < 1 implies the asset has less systematic risk than the overall market – β > 1 implies the asset has more systematic risk than the overall market 21")

22

Portfolio Expected Returns and Betas 22 RfRf

23

Reward-to-Risk Ratio: The reward-to-risk ratio is the slope of the line illustrated in the previous slide – Slope = (E(R A ) – R f ) / ( A – 0) – Reward-to-risk ratio = If an asset has a reward-to-risk ratio = 8? If an asset has a reward-to-risk ratio = 7? 23

24

The Fundamental Result The reward-to-risk ratio must be the same for all assets in the market If one asset has twice as much systematic risk as another asset, its risk premium is twice as large 24

25

Security Market Line (2) 25

25")

Similar presentations

ROSENGARTEN CORPORATION Pro forma balance sheet after 25% sales increase ($)(Δ,$)($)(Δ,$) AssetsLiabilities and Owner's Equity Current assetsCurrent.>")

>")