Download presentation

Presentation is loading. Please wait.

1

Financialisation of the South African economy: impact on the economic growth path and employment Sam Ashman, Seeraj Mohamed, Susan Newman Corporate Strategy and Industrial Development Research Programme School of Economic and Business Sciences University of the Witwatersrand

2

Background 4 Periods of global financial systems –1873 - 1914 (gold standard and global trade stability); –1918 - 1939 (interwar period, including Great Depression) –1945 - late-1970s (Bretton-Woods and Golden Age – embedded liberalism, capital controls and tight financial regulation, global trade stability); –Late-1970s to present (liberalisation, neo- liberalism and global financialization – instability in trade and financial markets, global financial crises)

; – (interwar period, including Great Depression) – late-1970s (Bretton-Woods and Golden Age – embedded liberalism, capital controls and tight financial regulation, global trade stability); –Late-1970s to present (liberalisation, neo- liberalism and global financialization – instability in trade and financial markets, global financial crises)")

3

A short history of financial markets There have been different forms of global financial architecture and regulation over time The history of financial markets is not an evolution towards free markets The globalisation of financial markets did not occur because of improvements in information technology The role of the state in financial markets during the neo- liberal era has not decreased it has changed from regulation to stop crises to bail outs after crises There is a close relationship between financialisation, the increasing power and growth of finance, and the development of neo-liberalism/Washington Consensus Shift from industrial capitalism to finance capitalism

4

Financialisation in South Africa: Implications Financialisation reshaped the South African economic growth path over the past two decades Finance was directed to finance and consumption and the sectors with strong linkages to these activities This economic growth path is not sustainable Limits are the size of bubbles in real estate and financial asset markets and debt for consumption The global financial crisis provided these constraints resulting in huge job losses Large-scale legal and illicit capital outflows created more reliance on short-term volatile inflows

5

SA’s financial sector in global context Financial depth: Liquid liabilities as a ratio of GDP (Based on data from Beck and Demirg üç -Kunt 2009) Deposit money bank assets as a percentage of GDP Ratio of stock market capitalisation to GDP Other financial institution assets as a ratio of GDP

Deposit money bank assets as a percentage of GDP Ratio of stock market capitalisation to GDP Other financial institution assets as a ratio of GDP")

6

Financialisation: Impact on Households Households on average saving for the future through the acquisition of financial assets BUT without forgoing current consumption which is financed by debt. However, the aggregate story on shifting savings and investment behaviour of households with financialisation is a story of a wealthy minority – Increasing incomes from dividends and interest payments to richest has driven worsening income inequality since 1994 – The financialisation leaves the majority of the population facing more precarious lives

7

Credit extended by all monetary institutions to the domestic private sector

8

ABSA House Price Index

9

Household savings to disposable income

10

Distribution of Household Assets

11

Distribution of household assets by wealth percentile (Based on data from Daniels, Finn and Musundwa 2012)

")

12

Implications: NFCs Since 1994 the composition of financial acquisitions shifts from lending to other sectors and money assets to greater diversification across a variety of financial assets, notably the acquisition of ordinary shares, fixed interest securities and other assets The asset side of the non-financial corporate balance sheet has shifted towards increasingly short-term assets This increased acquisition of financial assets has been financed through the expansion of credit The maturity mismatch between assets and liabilities is not conducive to long-term productive investments which drive capital accumulation Consequently, we have seen the financing of the acquisition of (largely short-term) financial assets rather than fixed capital

financial assets rather than fixed capital")

13

Financial assets as a percentage of fixed capital stock for non-financial corporations in South Africa: 1970-2010 Authors’ calculations based on flow-of-funds tables compiled by SARB 2011

14

Amounts receivable as a percentage of internal funds for non-financial corporations in South Africa: 1970-2010 Authors’ calculations based on flow-of-funds tables compiled by SARB 2011

15

Annual financing gap, external financing and the difference between the two for the non-financial corporate businesses Flow-of-funds tables, SARB 2011

16

Acquisition of financial assets by non-financial corporations by asset type Flow-of-funds tables, SARB 2011

17

Sources of external financing by non-financial corporations Flow-of-funds tables, SARB 2011

18

Implications: Saving & Investment Contrary to the view that South Africans do not save enough we show that gross domestic savings has stagnated since 2002 with an increase in gross savings being driven by capital inflows from the rest of the world attracted by high interest rates, healthy returns on South African capital markets Low domestic savings is due to poverty and inequality The financial sector attracts short-term and speculative rather than long-term productive capital These short-term inflows finance a large current account deficit and maintain the overall balance of payments, but this is at the expense of productive investment and employment creation

19

Restructuring of NFCs Most powerful corporations have used their corporate power to maintain their dominance over the South African economy while internationalising their operations. Their global context is one where competition is much harder Harsh competition has driven a process of increased global Concentration across most economic sectors and global value chains Within this new context, the lines of authority within global value chains and between the shareholder value movement and corporate management are stricter As a result, the large South African corporations that have internationalised have used their power in South Africa to maintain high levels of economic rents to support their operations in more cut throat international markets and unfriendly value chains

20

Financialisation of commodities markets Financialisation of commodities markets mean that fundamentals in real economy are increasingly delinked from price formation and market conditions for minerals products SA increased dependence on the mining and minerals industry in the era of financialisation There is strong risk of negative consequences associated with financial crises and contagion and the possibility of even more destabilising bubbles and crashes. The environment leads to increased uncertainty and more difficulty for planning investment and increasing employment in mining

21

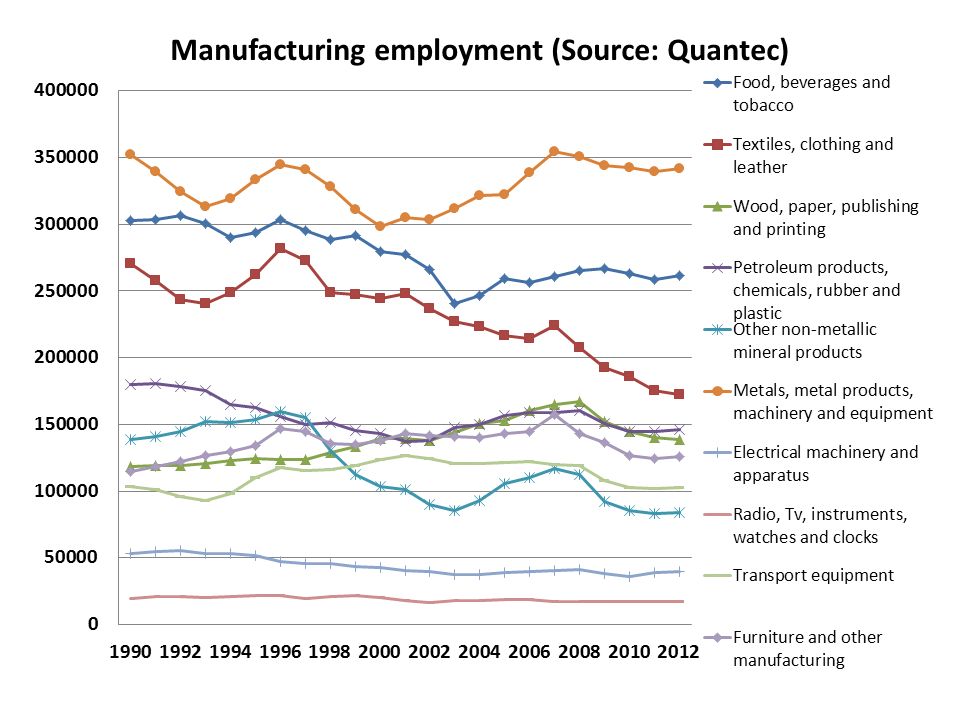

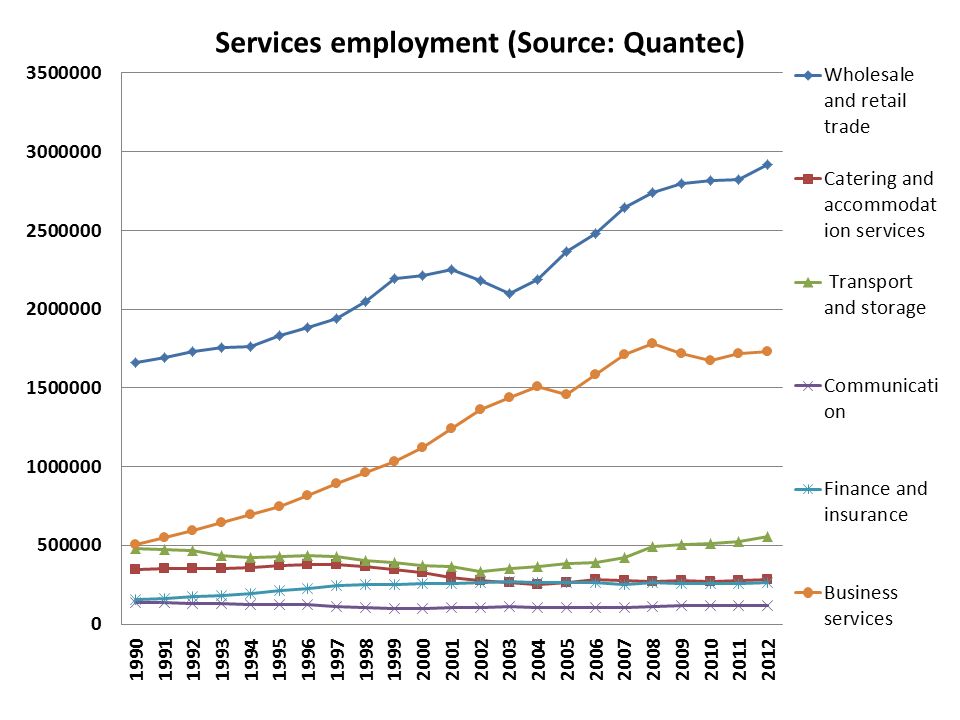

Labour markets and productivity Impact of corporate restructuring and financialisation on employment has been negative The changes have led to increasingly precarious employment in non-productive services We have to challenge mainstream economists wrt the direction of causation of low skills and productivity – De-industrialisation causes lower productivity – There has been lower productivity as a result not of poor training and skills but because of – Poor pay, casualisation and outsourcing, less training and increasing unemployment have a negative impact on productivity

Similar presentations

; Kaminsky,>")