Download presentation

Presentation is loading. Please wait.

1

Mthuli Ncube Chief Economist and Vice President African Development Bank group 2 May 2011 DANIDA DEVLOPMENT DAYS, Copenhagen: 2-4 May 2011 KEYNOTE ADDRESS 1

2

Part A: Africa Now Part B: Africa in 50 years time Part C: Development Challenges 2

3

Africa Now 3

4

African growth is strong. Africa the 3 rd fastest growth region over 10 years Africa did well out of financial crisis due to good economic management, and diversification GDP level at US$1.6 billion at par with Brazil or Russia Growth is being held back by factors such as infrastructure (taking away 2% of GDP growth) Africa is natural resource rich Growth not Inclusive Source: AfDB 4

Africa is natural resource rich Growth not Inclusive Source: AfDB 4.")

5

5 Commodity prices Domestic consumer market Macroeconomic policies and reforms: Reaping the benefits of decade of reforms Agriculture, services and manufacturing: Good harvests, diversification in some countries

6

6 Inclusive growth Strong demand for more accountability and good political governance in Africa The youth bulge deserves urgent attention Africa is growing but there are risks

7

7 Ghana (12%) Ethiopia DRC Zimbabwe (7,8%) Mozambique(7,7%) Angola Tanzania (6,9%) Nigeria Botswana Liberia (7,3%) South Africa Lesotho (2,9%) Comoros (2,5%) Benin (2,5%) Swaziland (1,9%) Egypt Tunisia (1,1%) Madagascar (0,6%) Côte d’Ivoire (-7,3%) Lybia 7,8% 3,6% 6,9% 7,3% 8,4% 6,9% -19% 1,6% 10% 6,9% 7,7%

Ethiopia DRC Zimbabwe (7,8%) Mozambique(7,7%) Angola Tanzania (6,9%) Nigeria Botswana Liberia (7,3%) South Africa Lesotho (2,9%) Comoros (2,5%) Benin (2,5%) Swaziland (1,9%) Egypt Tunisia (1,1%) Madagascar (0,6%) Côte d’Ivoire (-7,3%) Lybia 7,8% 3,6% 6,9% 7,3% 8,4% 6,9% -19% 1,6% 10% 6,9% 7,7%")

8

Intra-Africa trade remains low compared to other regions Investment in regional transport infrastructure and ports, is necessary Source: AfDB 8

9

9

10

Poverty levels are falling Per capita income is rising Inequality is rising Intra-Africa trade has risen slightly and so has Africa’s share of world global trade ICT access and penetration has increased substantially Access to water and sanitation has not improved 10

11

Staple food yields have not improved Fertilizer consumption has fallen Under-5 child mortality has fallen Primary school completion rates are flat Number of fragile states has dropped Combustible renewables and waste to generate energy is not increasing Cost of doing business has fallen Time required for business start-up has fallen 11

12

12

13

13

14

Sub-Saharan Africa lags behind other developing regions on all dimensions Regional connectivity is particularly lacking 14

15

Source: AUC, AfDB, WB presentation at UN Millennium Summit, September 2010 15

16

Lost production due to power outages and high regulatory costs reduce competitiveness of African exports Working hours lost due to power outage, 2009 Total regulatory costs as % of sales

17

Agriculture sector is important as 60% of population in Africa depends on it Staple crop yields remain flat Fertilizer consumption low Source: FAO 17

18

Improvements in 3 areas of governance No improvement in “voice and accountability” Static in “government effectiveness” Source: World Governance Indicators 2010 18

21

Source: Leveraging migration for Africa: remittances, skills and investments 2011 Destination of migrants from SSA

22

Recorded remittances41.1 ODA39.4 FDI55.7 Private debt & portfolio equity-10.9

23

Cost of formal banking is high (in some countries minimum deposit can be as high as 50% of per capita GDP. Internet and broadband subscription extremely low (so internet banking remains out of reach to most) Mobile banking a way to provide financial services to the unbanked Country Deposits Accounts per 100 Adults Subscribers per 100 inhabitants MobileInternetBroadband Algeria 68.393.813.52.3 Botswana 48.196.16.20.8 Congo-DR 0.615.40.5 Gambia 26.9847.60.02 Ghana 27635.40.1 Kenya 29.648.6100.02 Madagascar 33.830.61.630.2 South Africa 78.892.38.21 Tunisia67.29534.13.6

Mobile banking a way to provide financial services to the unbanked Country Deposits Accounts per 100 Adults Subscribers per 100 inhabitants MobileInternetBroadband Algeria Botswana Congo-DR Gambia Ghana Kenya Madagascar South Africa Tunisia")

24

Africa in 50 years time! 24

25

25

26

26

27

27

28

28

29

29

30

30

31

31

32

32

33

33

34

34

35

Africa’s Development Challenges 35

36

Infrastructure Deficit (US$45 billion annually) Improving investment climate Development of Small to Medium Scale enterprises…as a strategy for fostering “Inclusive growth” and “structural transformation” Land Ownership reform (ownership will help development of SMEs in agriculture) Effective and transparent management of natural resource revenues< e.g Sovereign Wealth Funds ODA in the form of “insurance”…state contingent Financial inclusion 36

Improving investment climate Development of Small to Medium Scale enterprises…as a strategy for fostering Inclusive growth and structural transformation Land Ownership reform (ownership will help development of SMEs in agriculture) Effective and transparent management of natural resource revenues< e.g Sovereign Wealth Funds ODA in the form of insurance …state contingent Financial inclusion 36")

37

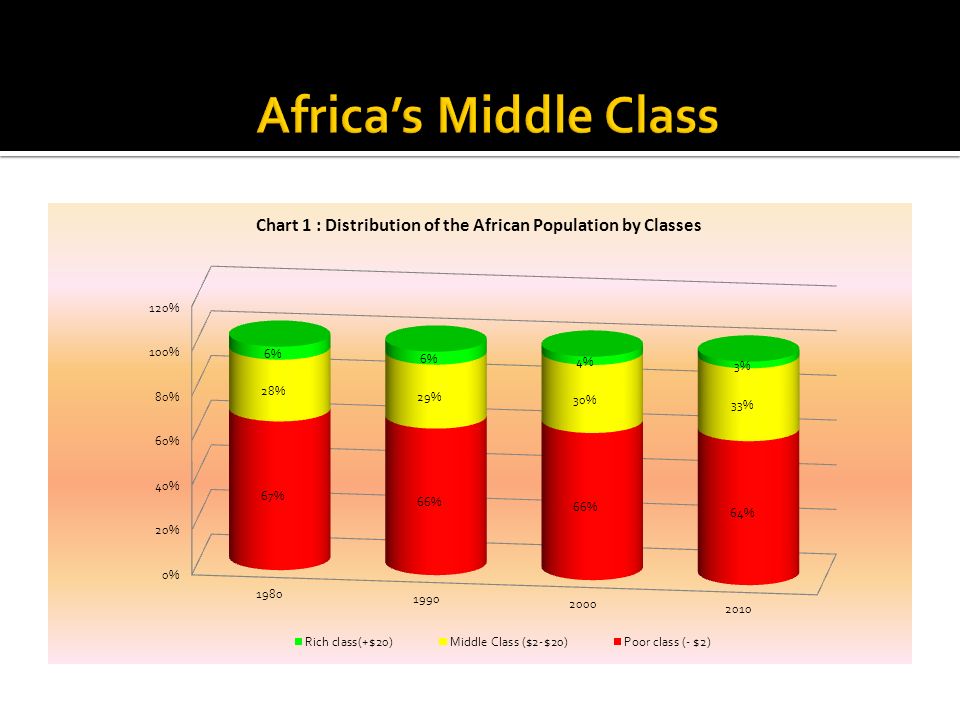

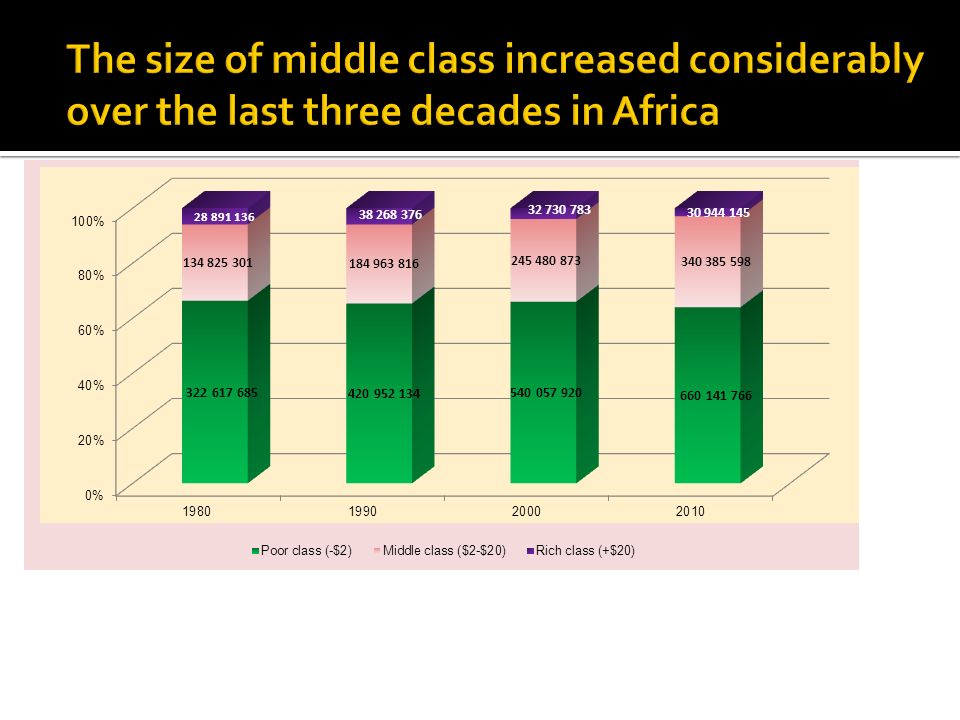

Recognize and Support the growing middleclass in Africa Danida to form partnership with Danish companies to invest in Energy Infrastructure Supporting development of Small to Medium Scale enterprises…as a strategy for fostering “Inclusive growth” and “structural transformation”…entrepreneurship ecosystem Facilitate agricultural land ownership reform (ownership will help development of SMEs in agriculture) Effective and transparent management of natural resource revenues, e.g Sovereign Wealth Funds Convert ODA to some form of “insurance”…state contingent, if certain “events” occur Invest in Financial Inclusion in partnership with private sector, eg M-Pesa growth in Kenya based on mobile telephony FACILITATION rather than RESOURCE OUTLAY 37

Effective and transparent management of natural resource revenues, e.g Sovereign Wealth Funds Convert ODA to some form of insurance …state contingent, if certain events occur Invest in Financial Inclusion in partnership with private sector, eg M-Pesa growth in Kenya based on mobile telephony FACILITATION rather than RESOURCE OUTLAY 37")

38

38

Similar presentations

![Addressing Key Structural Vulnerabilities for [Africas] LDCs UN-OHRLLS Brainstorming Meeting on Substantive Preparation for UNLDC-IV New York, NY 14-16.](/2/722341/big_thumb.jpg "Addressing Key Structural Vulnerabilities for [Africas] LDCs UN-OHRLLS Brainstorming Meeting on Substantive Preparation for UNLDC-IV New York, NY 14-16.>")