Download presentation

Presentation is loading. Please wait.

1

Marshall Public Schools #413 Truth in Taxation Hearing for Taxes Payable in 2013

2

Welcome December 3rd, 2012 6:00 P.M. Board Room-Marshall Middle School Presented by: Bruce Lamprecht Director of Business Services

3

ISD 413, Marshall Truth in Taxation Law State law initially approved in 1998. The 2009 legislature made several changes: Property tax hearing can now be held a regular meeting. Hearing must be at 6:00 PM or later. Levy may be adopted at the same meeting. Requirement to publish meeting notice was deleted. All school districts must now hold a hearing. Previously some districts were exempted from the requirement to hold a hearing. You are here for the school district’s annual required hearing.

4

ISD 413, Marshall Tax Hearing Presentation State law requires that we present information on the current year budget and actual revenue and expenses for the prior year State law also requires that we present information on the proposed property tax levy, including: The percentage increase/decrease over the prior year Specific purposes and reasons if taxes are being increased/decreased District must also allow for public comments

5

Agenda for Hearing A. Background on School Funding, Property Tax Levies, and Budgets B. Information on District Budget C. Information on the District’s Proposed Tax Levy for Taxes Payable in 2013 D. Public Comments and Questions

6

Public Education is Strong in Minnesota…… In Minnesota, the most commonly taken standardized college entrance exam is the ACT. Seventy-eight percent of Minnesota high school graduates in 2012 took the assessment. Minnesota’s average composite score of 22.8 was the highest in the nation among the 27 states in which more than half of the college-bound students took the test in 2012. Minnesota has led the nation in average composite ACT scores for five consecutive years. The national composite score was 21.1. Marshall’s composite score was 22.4.

7

State of MN Constitution “ARTICLE XIII MISCELLANEOUS SUBJECTS Section 1. UNIFORM SYSTEM OF PUBLIC SCHOOLS. The stability of a republican form of government depending mainly upon the intelligence of the people, it is the duty of the legislature to establish a general and uniform system of public schools. The legislature shall make such provisions by taxation or otherwise as will secure a thorough and efficient system of public schools throughout the state.”

8

As a result… School District Funding is Highly Regulated by the State State sets formulas which determine revenue; most revenue is based on specified amounts per pupil State sets tax policy for local schools State sets maximum authorized property tax levy (districts can levy less but not more than amount authorized by state, unless approved by the voters) State authorizes school board to submit referendums for operating and capital needs to voters for approval

State authorizes school board to submit referendums for operating and capital needs to voters for approval")

9

State Funding for Schools Has Not Kept Pace with Inflation Increases in basic general education revenue per pupil have been less than inflation Per-pupil revenue for fiscal year 2013-14 is projected to be $401 below the 2004-05 inflation adjusted amount For Fiscal 2013 and 2014, basic per-pupil funding is projected to increase by less than 1% per year, while most districts’ expenses will likely increase, without budget cuts, by 2-3% annually

10

Trends in General Education Formula Allowance for Minnesota School Districts FY 05 – FY 14

11

Impact is budget cuts and levy referendums… With minimal increases in state funding expected, some districts continue to face projected budget shortfalls for FY 2014 and FY 2015 and anticipate the need for budget cuts To meet local school budget shortfalls, in 2012, 40 Minnesota districts submitted proposals to voters seeking support of increased operating levies 29 districts, or 73%, passed at least 1 operating levy question

12

ISD 413, Marshall School District Levy 2012 Payable 2013 2013-2014 School Year Fiscal Year 2014

13

ISD 413, Marshall School Levy vs. Budget Cycle Unlike cities and counties, a school district does not set its budget when setting the tax levy Property Tax Levy Final levy set in December Property taxes levied on calendar year basis Budget Preliminary budget approved in June, six months later School district fiscal year is July 1 st through June 30th

14

ISD 413, Marshall, Minnesota Contrast of City/Township/County Levy Cycle to School District Levy Cycle J A N F E B M A R A P R M A Y J U N J U L A U G S E P O C T N O V D E C J A N F E B M A R A P R M A Y J U N J U L A U G S E P O C T N O V D E C J A N F E B M A R A P R M A Y J U N J U L A U G S E P O C T N O V D E C Legislation City/Twp/County Tax Levy Decision Collection of Levy Budget Year School District Tax Levy Decision Collection of Levy Budget Year 201420122013

15

Budget and Levy Adoption Calendar J A N F E B M A R A P R M A Y J U N J U L A U G S E P O C T N O V D E C J A N F E B M A R A P R M A Y J U N J U L A U G S E P O C T N O V D E C J A N F E B M A R A P R M A Y J U N J U L A U G S E P O C T N O V D E C Audit 2011-2012 2012/2013 Current Budget 13-14 Budget Preparation Adoption of 13-14 Budget Update Current Budget Year Final Current Budget Year Update Tax Levy Decision Collection of Levy 2013-2014 Budget Year 201420122013

16

Property Tax Share By Governmental Entity

17

Change in Tax Levy Does not Determine Change in Budget Tax levy is based on many state-determined formulas Some increases in tax levies are revenue neutral, offset by reductions in state aid Expenditure budget is limited by state-set revenue formulas, voter-approved levies, and fund balance, not just by tax levies

18

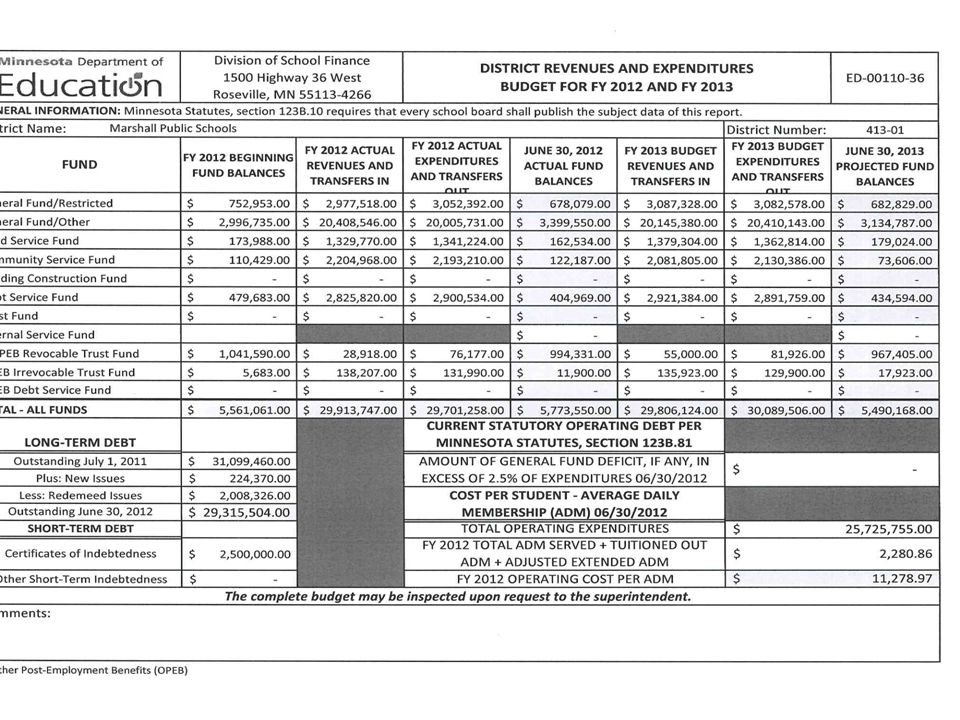

School District Budget Current School and Fiscal Year 2012-2013

19

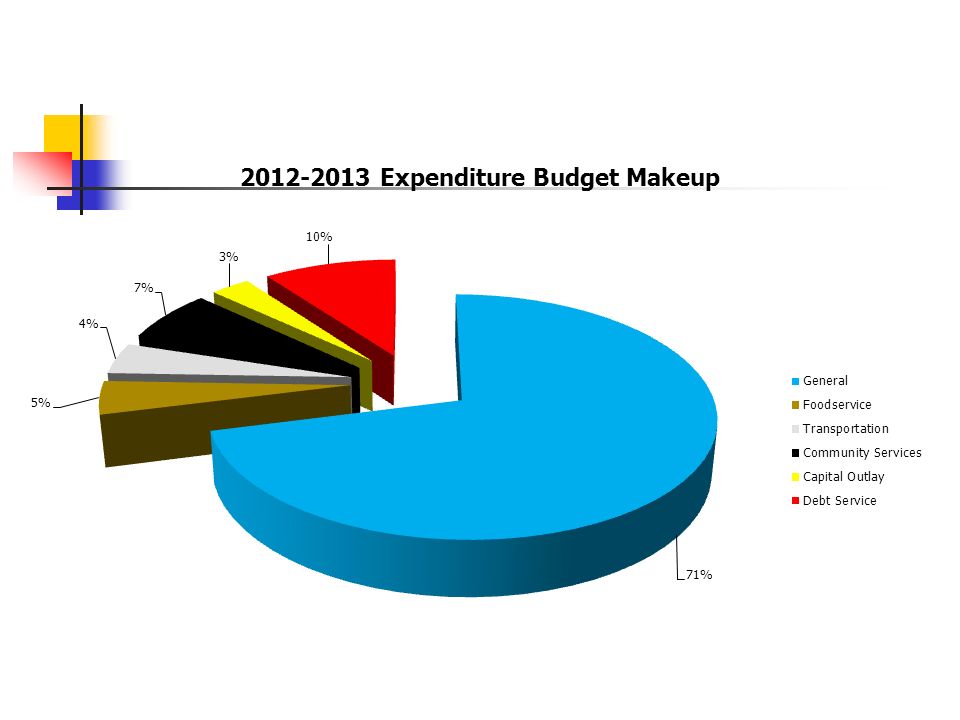

MARSHALL PUBLIC SCHOOLS 2012-2013 BUDGET OVERVIEW REVENUES 11-12 Actual12-13 Budget% Change ---------------------------------------------- General Fund$21,532,256$21,496,586 -.1% Foodservice $1,329,770 $1,379,304 3.7% Transportation $1,276,430 $996,481 -21.9% Community Services $2,204,968 $2,081,805 -5.6% Capital Outlay $891,762 $739,641 -17.0% Debt Service $2,964,027 $3,057,307 3.1% Total $30,199,213$29,751,124 -1.5%

20

MARSHALL PUBLIC SCHOOLS 2012-2013 BUDGET OVERVIEW EXPENDITURES 11-12 Actual12-13 Budget% Change ---------------------------------------------- General Fund$21,243,942$21,317,402.3% Foodservice $1,341,224 $1,362,814.2% Transportation $1,276,430 $1,280,000.03% Community Services $2,193,210 $2,130,386 -2.9% Capital Outlay $852,135 $895,319 5.1% Debt Service $3,032,524 $3,021,659 -.4% Total$29,939,465$30,007,850.2%

22

2012-2013 Revised Budget Analysis

23

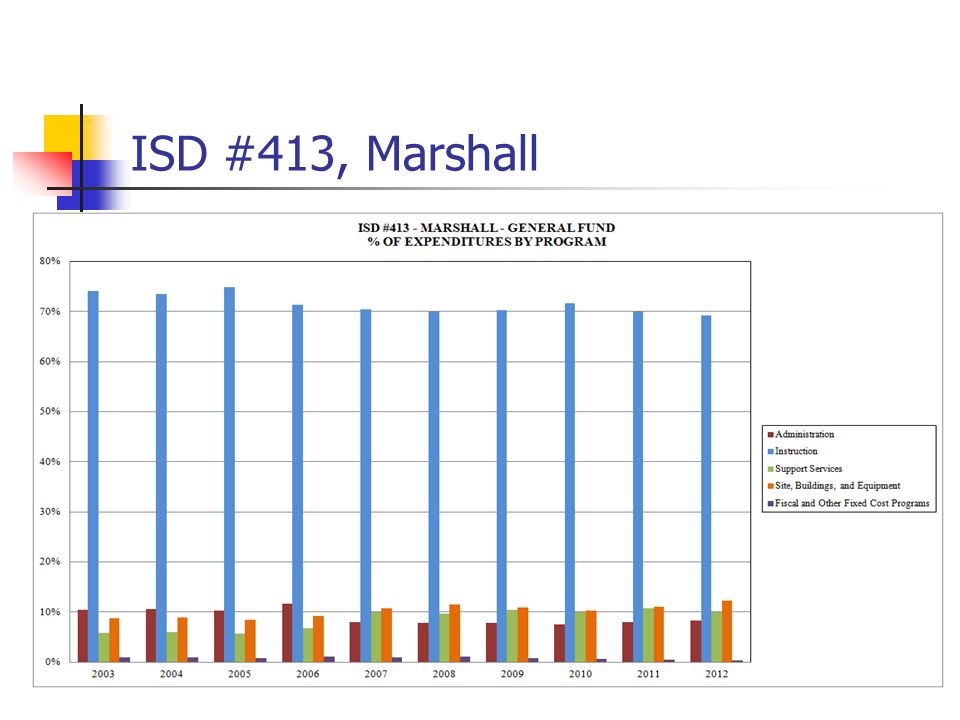

General Fund Expenditures June 30th, 2012

24

ISD #413, Marshall Marshall Public Schools Summary of Staff Employed

25

ISD #413 - MARSHALL GENERAL FUND EXPENDITURES JUNE 30th, 2012

26

ISD #413-Marshall-General Fund Expenditures By Object Code

27

ISD 413, Marshall

28

ISD #413, Marshall

30

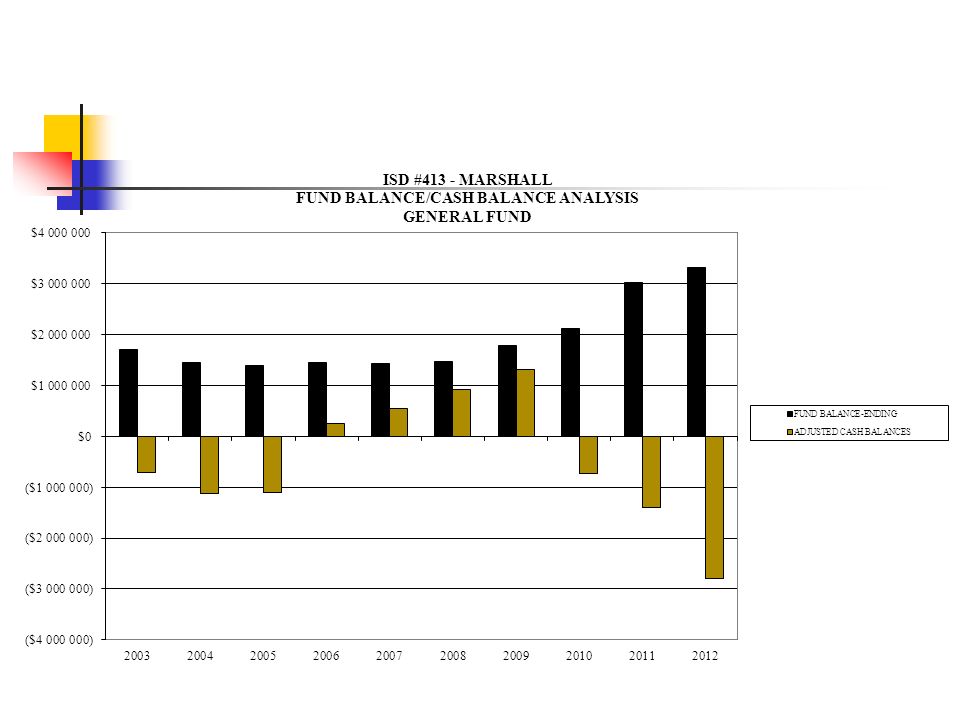

ISD #413 Audit Highlights The audit results for 2011-2012 showed an ending General Fund balance of $3,314,461 or 15.6% of expenditures. The Transportation Fund showed a zero ending fund balance after a revenue transfer from Fund 01. The Capital Outlay Fund ended with a balance of $763,168 exceeding the established goal of $400,000 by a goodly amount. The Foodservice Fund ended with a much better ending fund balance than projected considering two major capital purchases. The Debt Service Fund balance provides cash flow for the District and sometimes allows us to under-levy.

32

ISD #413, Marshall The Revised General Fund Budget for 2012- 2013 shows a $104,335 deficit in revenues over expenditures. This includes a transfer of $283,519 to the Transportation Fund to zero out the fund balance. This translates into a $2,765,751 ending fund balance or a 14.97 fund balance percent with a stated, approved goal of 8.0% (fund balance/expenditures) being the minimum.

being the minimum..")

33

How Much Revenue is State Aid vs. Local Sources?

34

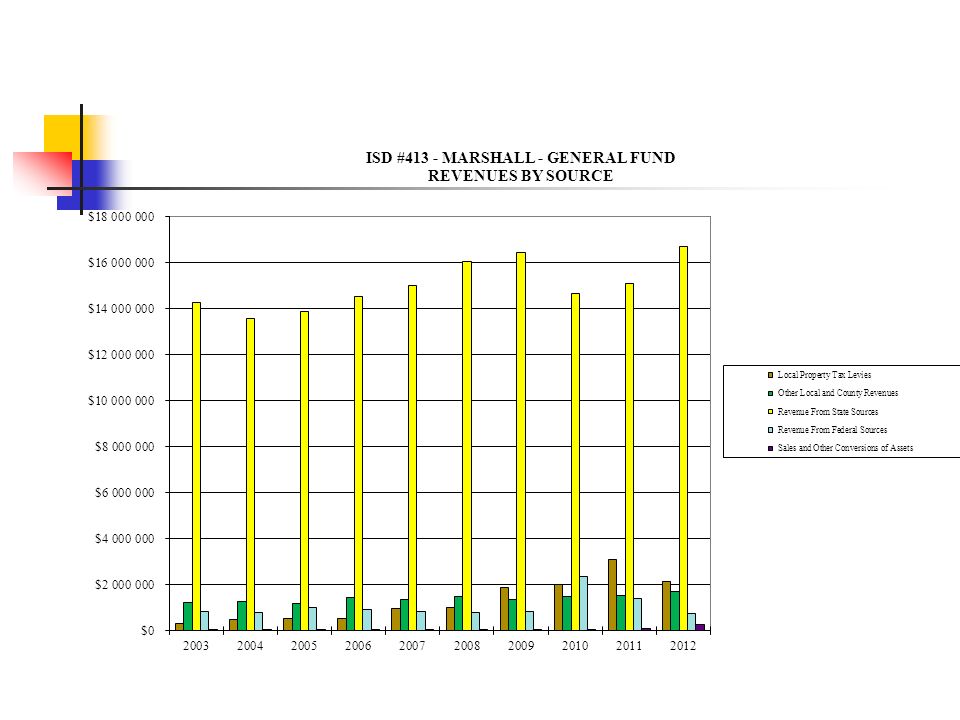

General Fund Revenues By Source

36

General Fund Revenue Sources by Percent

37

ISD 413, Marshall General Fund Changes in Basic per Pupil Allowance

38

Revenue-Adjusted For Inflation

40

Proposed 2013 Property Tax Levy Determination of levy Comparison 2012 to 2013 levies Specific reasons for changes in tax levy Impact on taxpayers

41

ISD 413, Marshall Authority for School Levies A School District Tax Levy must be either: Set by State Formula or Voter Approved

42

Property Tax Background Every owner of taxable property pays property taxes for the various ‘taxing jurisdictions’ (county, city or township, school district, special districts) in which the property is located Each taxing jurisdiction sets its own tax levy, often based on limits in state law County sends out bills, collects taxes from property owners, and distributes funds back to other taxing jurisdictions

in which the property is located Each taxing jurisdiction sets its own tax levy, often based on limits in state law County sends out bills, collects taxes from property owners, and distributes funds back to other taxing jurisdictions")

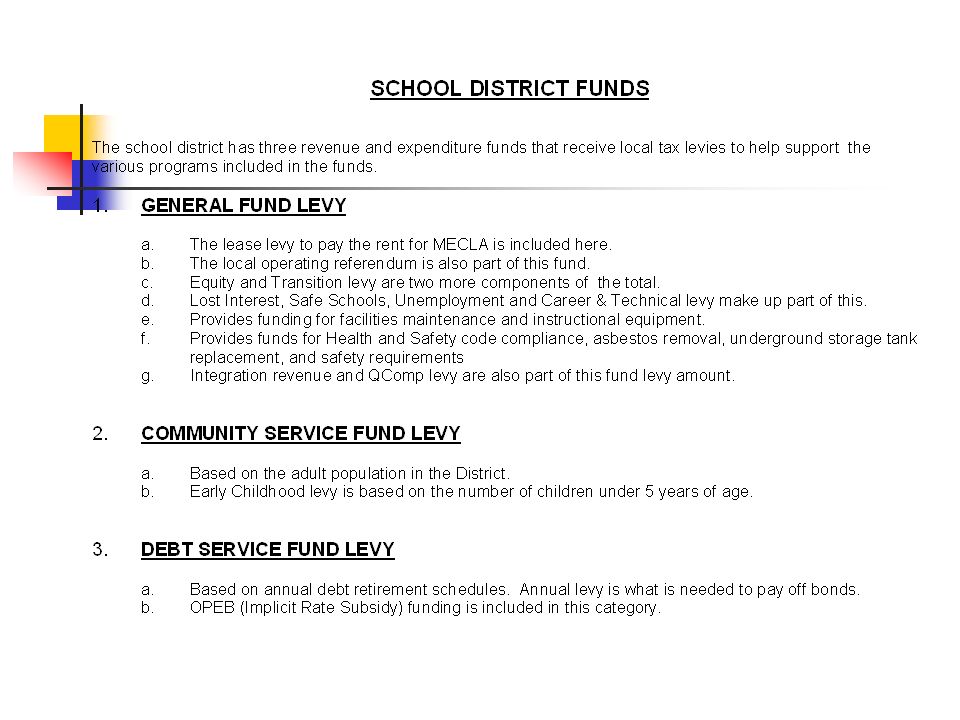

43

School District Property Taxes Each school district may levy taxes in up to 30 different categories ‘Levy Limits’ (maximum levy amounts) for each category are set either by: State law, or Voter approval Minnesota Department of Education (MDE) calculates detailed levy limits for each district

for each category are set either by: State law, or Voter approval Minnesota Department of Education (MDE) calculates detailed levy limits for each district")

44

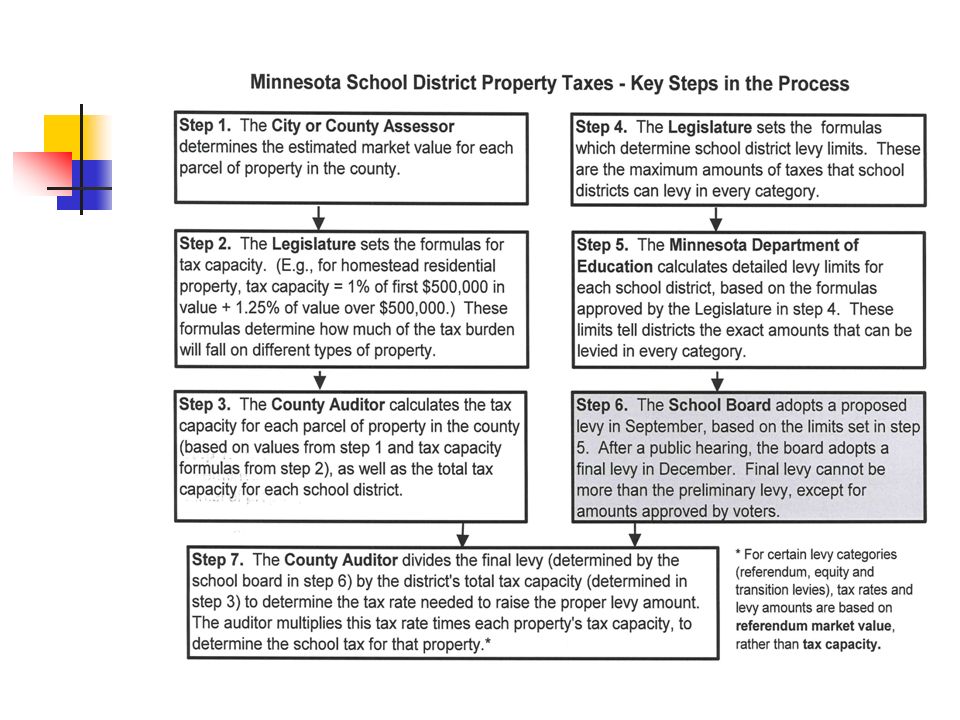

Property Tax Background School District Property Taxes Key steps in the process are summarized on the next slide Any of these steps may affect the taxes on a parcel of property, but the district has control over only 1 of the 7 steps

46

The Homestead Credit Shift The 2011 legislature repealed the Homestead Market Value Credit In its place, the Legislature implemented a Homestead Market Value Exclusion

47

Property Tax History-$150K Parcel PrimaryParcel'sDistrictRate Property Taxes by Year and Property Type PayableSchoolMarketTotalAgainst ResidentialCommercialAgricultural Year ValueLevyRMVNTCHomesteadIndustrialLand & Bldg 20012001-02150,0005,249,3020.0011410.657324$1,157$1,650$542 20022002-03150,0001,780,0590.0000570.233595$359$534$193 20032003-04150,0001,685,7440.0000640.209072$323$480$172 20042004-05150,0003,568,3310.0005370.374747$643$924$309 20052005-06150,0003,556,9220.0005660.340827$596$852$281 20062006-07150,0004,253,8690.0006570.369130$652$929$305 20072007-08150,0004,442,6380.0006520.345149$616$874$285 20082008-09150,0005,427,6760.0015960.344482$756$1,015$284 20092009-10150,0005,560,5780.0015940.327338$730$976$270 20102010-11150,0005,489,7630.0016100.289605$676$893$239 20112011-12150,0005,714,4380.0016620.308009$711$942$254 20122012-13150,0005,880,1860.0016410.300163$696$922$248 2013Excluding Addition150,0006,172,7150.0016680.318779$728$967$263 2013Including Addition150,0006,172,7150.0016680.318779$728$967$263

48

Changing School District Property Taxes

49

Comparable Levies On Residential Homesteads

50

Changing Property Taxes On A $150K Residential Homestead

52

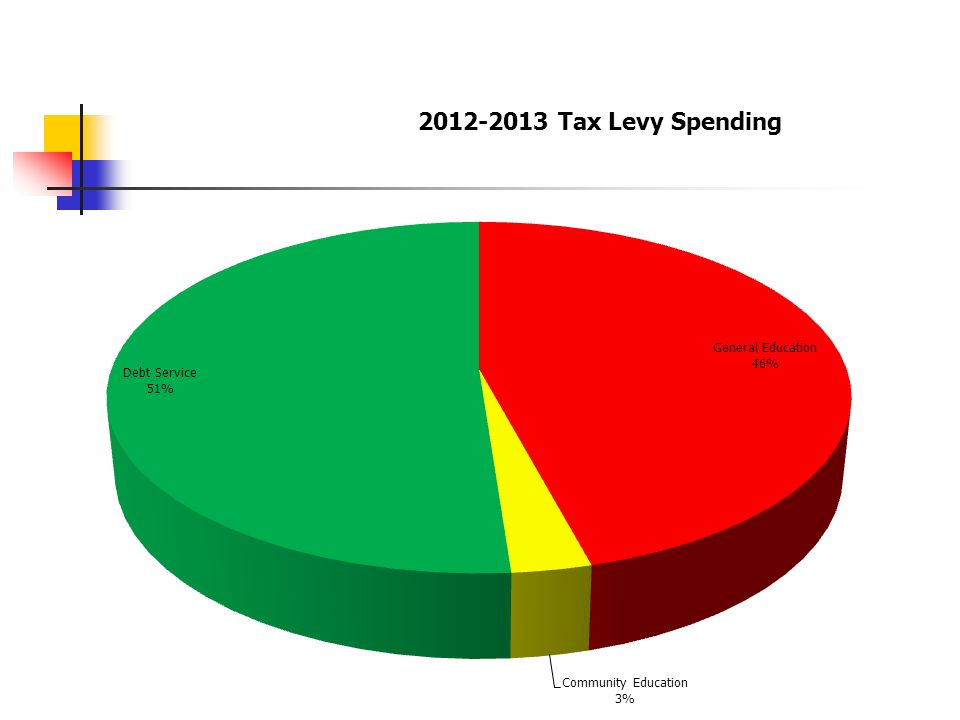

ISD 413, Marshall How are the Proposed 2012 School Taxes Spent?

53

Pay 2012/Pay 2013 Levy Comparison Fund11 Pay 1212 Pay 13Increase% Change General2,666,738.772,533,931.25 167,192.48 6.27% Community Service 172,604.86 184,213.55 11,608.69 6.73% General Debt Service 2,904,919.613,029,555.32 124,635.71 4.29% OPEB Debt Service 135,923.00 133,376.87 -2,546.13 -1.87% Total5,880,186.246,181,076.99300,890.75 5.12%

55

ISD 413, Marshall Basic general education aid and levy formula (1) NTC 2011 14,332,198 (2) Sales Ratio 2011 94.6% (3) ANTC 2011 15,150,315 (4) Standard Levy Limit FY 2014 0.0% (5) Gen Education Basic Levy Limit 2012 0.00 AMCPU2013-2014 2558.32 Formula Allowance Pay 2013 5,224.00 (6) Basic General Education Revenue 13,364,663.68 (7) Basic General Education Aid Revenue FY 2014 13,364,663.68 (8) General Education Aid Percentage FY 2014 100.0%

NTC ,332,198 (2) Sales Ratio % (3) ANTC ,150,315 (4) Standard Levy Limit FY % (5) Gen Education Basic Levy Limit AMCPU Formula Allowance Pay , (6) Basic General Education Revenue 13,364, (7) Basic General Education Aid Revenue FY ,364, (8) General Education Aid Percentage FY %")

56

ISD 413, Marshall District #413 Proposed Property Tax Stmt. for 2013

57

ISD 413, Marshall The School District Levy is increasing by: $300,890.75 or 5.12%

58

Tax Levy History 1999 Pay 2000$5,149,862.382.60% Decrease 2000 Pay 2001$5,063,847.461.67% Decrease 2001 Pay 2002$1,780,058.9764.58% Decrease 2002 Pay 2003$1,685,744.135.30% Decrease 2003 Pay 2004$3,568,330.76111.68% Increase 2004 Pay 2005$3,556,922.390.32% Decrease 2005 Pay 2006$4,253,869.0019.59% Increase 2006 Pay 2007$4,442,638.194.44% Increase 2007 Pay 2008$5,427,675.7022.17% Increase 2008 Pay 2009$5,560,578.162.40% Increase 2009 Pay 2010$5,489,763.141.27% Decrease 2010 Pay 2011$5,714,432.294.09% Increase 2011 Pay 2012$5,880,186.242.90% Increase 2012 Pay 2013$6,181,076.995.12% Increase

59

ISD 413, Marshall What are the main variables that cause property tax increases and decreases? 1. Changes in market values 2. Changes in class rates/history 3. Market Value Homestead Exclusion 4. Voter Approved Referendums 5. Ongoing Legislative Action

60

ISD 413, Marshall Changes in Market Value The market values are final and are not a subject for the upcoming budget hearings. They were discussed at the local board of review and county board of equalization hearings held earlier this year. The final taxable market values may reflect a reduction under the limited value law. If this property is a qualifying homestead, the final taxable market values may exclude improvements which you made to this property.

62

Net Tax Capacity Property Comparison DescriptionResidential Homestead Commercial Industrial Agricultural Homestead (Land & Buildings) Property Value$200,000 Tax Rate Pay 2013 1.00 %2.00%.50% Net Tax Capacity Amount $2,000.00$4,000.00$1,000.00

Property Value$200,000 Tax Rate Pay %2.00%.50% Net Tax Capacity Amount $2,000.00$4,000.00$1,000.00")

63

State Property Tax Refunds State of Minnesota has two tax refund programs and one tax deferral program available for owners of homestead property These programs may reduce the net tax burden for local taxpayers, but only if you take time to complete and send in the forms For help with the forms and instructions: Consult your tax professional, or Visit the Department of Revenue web site at www.taxes.state.mn.us

64

State Property Tax Refunds Minnesota Property Tax Refund (aka “Circuit Breaker” Refund) Has existed since the 1970’s Available to all owners of homestead property Annual income must be approx. $99,240 or less (income limit is higher if you have dependents) Refund is a sliding scale, based on total property taxes and income Maximum refund is $2,370 Especially helpful to those with lower incomes Fill out state tax form M-1PR

Refund is a sliding scale, based on total property taxes and income Maximum refund is $2,370 Especially helpful to those with lower incomes Fill out state tax form M-1PR.")

65

State Property Tax Refunds Special Property Tax Refund Available for all homestead properties with a gross tax increase of at least 12% and $100 over the prior year Refund is 60% of the amount by which the tax increase exceeds the greater of 12% or $100, up to a maximum of $1,000 No income limits Fill out state tax form M-1PR Minnesota Department of Revenue (651) 296-3781

")

66

Senior Citizen Property Tax Deferral Allows people 65 years of age or older with a household income of $60,000 or less to defer a portion of the property taxes on their home Taxes paid in any year limited to 3% of household income for year before entering deferral program; this amount does not change in future years Additional taxes are deferred, but not forgiven State charges interest up to 5% per year on deferred taxes and attaches a lien to the property The deferred property taxes plus accrued interest must be paid when the home is sold or the homeowner(s) dies

dies")

67

ISD 413, Marshall Whereas, Pursuant to Minnesota Statutes the School Board of Independent School District No. 413, Marshall, Minnesota, is authorized to make the following proposed tax levies for general purposes: Now Therefore, Be it resolved by the School Board of Independent School District No. 413, Marshall, Minnesota, that the amount to be levied in 2012 to be collected in 2013is set at $6,181,076.99. The clerk of the Marshall School Board is authorized to certify the proposed levy to the County Auditor of Lyon County, Minnesota. General Fund$2,833,931.25 Community Service $184,213.55 Debt$3,162,932.19 Total Proposed School Tax Levy$6,181,076.99

68

Next Steps Tonight-Board will accept public comments and questions on proposed levy December 17th-Board will conduct subsequent hearing (if necessary) and certify final amount of tax levy payable in 2013

and certify final amount of tax levy payable in 2013")

69

ISD 413, Marshall Public Comments and Questions

70

THE END THANK YOU FOR ATTENDING!

Similar presentations

![Public Hearing on the 2012-13 Budget and Proposed 2013 Property Taxes [Put Your School District Name Here] December 2012 Information on changes to school.](/22/6386311/big_thumb.jpg "Public Hearing on the 2012-13 Budget and Proposed 2013 Property Taxes [Put Your School District Name Here] December 2012 Information on changes to school.>")