Download presentation

Presentation is loading. Please wait.

1

Bab 8. Minggu 14 Model Binomial untuk Opsi

2

Setelah menyelesaikan perkuliahan minggu ini, mahasiswa bisa : Menjelaskan model binomial dalam pergerakan harga saham Menjelaskan model binomial untuk harga opsi call tipe Eropa dan Amerika Menurunkan formula harga opsi call tipe Eropa dan Amerika Tujuan Pembelajaran

3

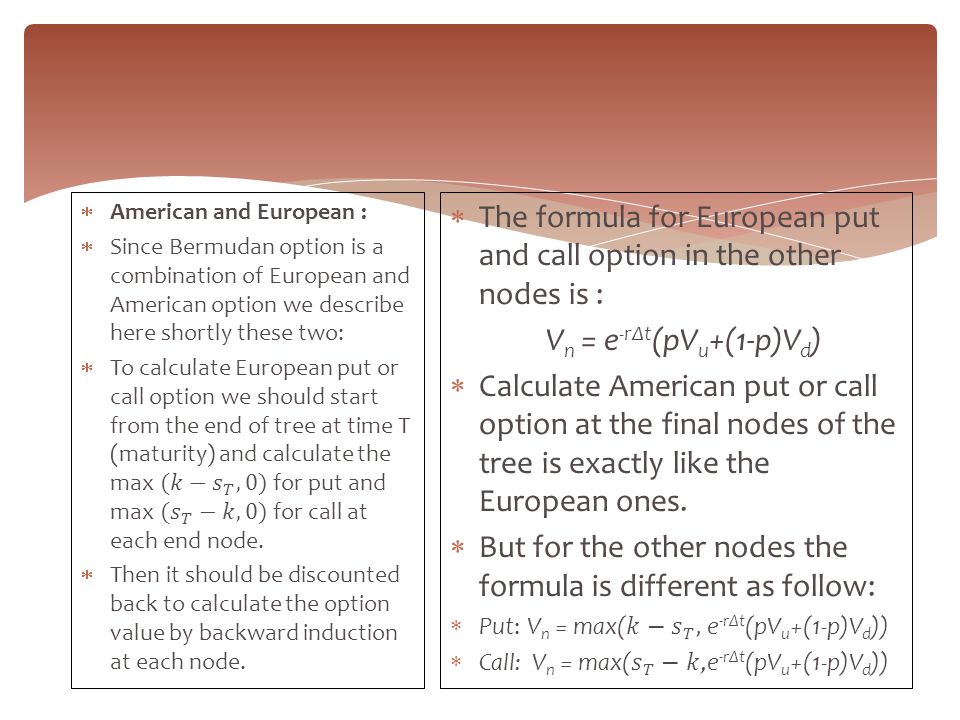

Introduction Like Bermudian islands which are located between Europe and America, Bermudan options are a combination of American and European options. Unlike the European options which can be exercised only at maturity and American option that can be exercised at any time, Bermudan can be exercised at predetermined dates up to maturity. A Bermudan Option is a type of option with early exercise restricted to certain dates during the life of the option. Bermudan Options have an “early exercise” date and expiration date. Bermudan options act like both European options and the American ones. It behaves like European options since it cannot be exercised at any time and it behaves like American options due to the fact that it can be exercised at some specific times. The value of Bermudan Option is always equal or greater than European and equal or less than American ones.

4

Binomial Model: Binomial model is a very popular model for option pricing, Binomial tree shows different ways that stock price can move during option’s life time based on certain probability of moving up or either down. There are different formulas for the probability of up and down but Cox-Ross-Rubenstein formula is the most common model for the binomial tree so in our model we used Cox-Ross- Rubenstein formula:

6

Example: Consider the tree below which is a 6-step binomial tree with T=1.5 year and the Bermudan option can only be exercised once a year. The red nodes are the nodes that Bermudan option can be exercised at that time. For those nodes option value should be calculated like American ones for the rest of the nodes, they should be calculated like European options. European American

7

Parameters Call or Put Number of Nodes6 Time to Maturity1,5 Risk-Free Rate0,06 Volatility0,08 Stock Price50 Strike Price53 1-Probability0,321136 Results Up Rate of Stock1,040811 Down Rate of Stock0,960789 Probability0,678864 Price3,000 0123456 0369121518 63,56246 0 61,07014 0 58,67554 00 56,37484 0,0949830 54,16435 0,4272810,3002410 52,04054 0,9464961,1498520,949064 50 1,603062,08863333 48,03947 3,0664444,171461 46,15582 5,2777966,844183 44,34602 7,864911 42,60719 10,39281 40,93654 11,2744 39,33139 13,66861

8

Stock Price ($)S50 Strike Price ($)K53 Volatilityσ0,08 Time to expiration (year)T1 continuous compounding rater0,06 the number of periodsn6dt = T/n =0,1667 exercisable periods2, 4 upward movementu1,0332exp(σ*dt^0.5) downward movementd0,96791/u risk-neutral probabilityp0,6457(exp(rdt)-d)/(u-d)

S50 Strike Price ($)K53 Volatilityσ0,08 Time to expiration (year)T1 continuous compounding rater0,06 the number of periodsn6dt = T/n =0,1667 exercisable periods2, 4 upward movementu1,0332exp(σ*dt^0.5) downward movementd0,96791/u risk-neutral probabilityp0,6457(exp(rdt)-d)/(u-d)")

9

exercise date 0,0000 0,12950,36921,05243,0000 0,53481,28843,00004,07936,1616 1,39433,00004,07936,16167,13939,1233 Bermuda put option lattice 2,32234,07936,16167,13939,123310,005811,8977 time period0123456

10

References Hull, John C. Options, futures, and other derivatives.6 th ed. Upper Saddle River, N.J. : Pearson Prentice Hall, cop. 2006 Wilmott, Paul, The Mathematics of Financial Derivatives, Cambridge : Cambridge Univ. Press, 1995

11

Terima Kasih

Similar presentations