Download presentation

Presentation is loading. Please wait.

1

Financial Literacy Suppose you have $100 in a savings account earning 2 percent interest a year. After five years, how much would you have? Possible answers: More than $102; exactly $102; or less than $102. Imagine that the interest rate on your savings account is 1 percent a year and inflation is 2 percent a year. After one year, would the money in the account buy … ? Possible answers: More than it does today; exactly the same; less than today.

2

Financial Literacy If interest rates rise, what will happen to bond prices? Possible answers: Bond prices will rise; fall; stay the same; there is no relationship. Bond prices fall Reason- newer bonds pay higher interest rate than older ones- older bonds are worth less so price drops A 15-year mortgage typically requires higher monthly payments than a 30-year mortgage, but the total interest paid over the life of the loan will be less. Possible answers: true or false. True Reason: pay off principal at a faster rate

3

Financial Literacy Buying a single company’s stock usually provides a safer return than a stock mutual fund. Possible answers: true or false. Answer: False Reason: spread out your risks to protect money Does carrying a balance on your credit card help your credit? Should you pay down your largest debts first?

4

What is Financial Literacy Knowledge and skills to manage financial resources effectively Long term vision Planning for future Use skills every day What are your financial goals today, in 10 years, 20 years? Do you feel confident about your ability to make personal financial decisions?

5

Financial Literacy The more you know about economics, the more informed decisions you will make regarding your current and future finances. What comes to mind when you think of economics? What roles do you and your family members play in the country’s economy? How might limited funds affect your financial decisions? What are your economic needs and wants?

6

The Fundamentals of Economics Scarcity & Economics Economics Study of decisions that go into making, distributing, and using goods and services Opportunity Costs What you give up to get something else Costs and benefits to all decisions

7

Opportunity Cost Eat Breakfast Ride the bus Cut your last class Go out to lunch Go in after school for help in physics In pairs- choose two entries from list on left. Identify the next best choice (Ex.-eat breakfast or skip breakfast) List the benefits of each choice and costs of each choice Compare answers with partner Did you make same choice, why or why not?

List the benefits of each choice and costs of each choice Compare answers with partner Did you make same choice, why or why not .")

8

Scarcity Choose which goods and services to use or not use Limited resources Unlimited needs & wants Scarcity of Goods and Services

9

Factors of Production-resources needed to produce goods & services amount of each factor determines wealth

10

New Factors of Production? Time speed and time delivers a primary marketplace advantage (IE- Toyota Prius- 15 months for design, development, & deployment) Information four “V’s” of data: volume, velocity, variety and veracity. Capital

Information four V’s of data: volume, velocity, variety and veracity. Capital.")

11

Basic Economic Questions

12

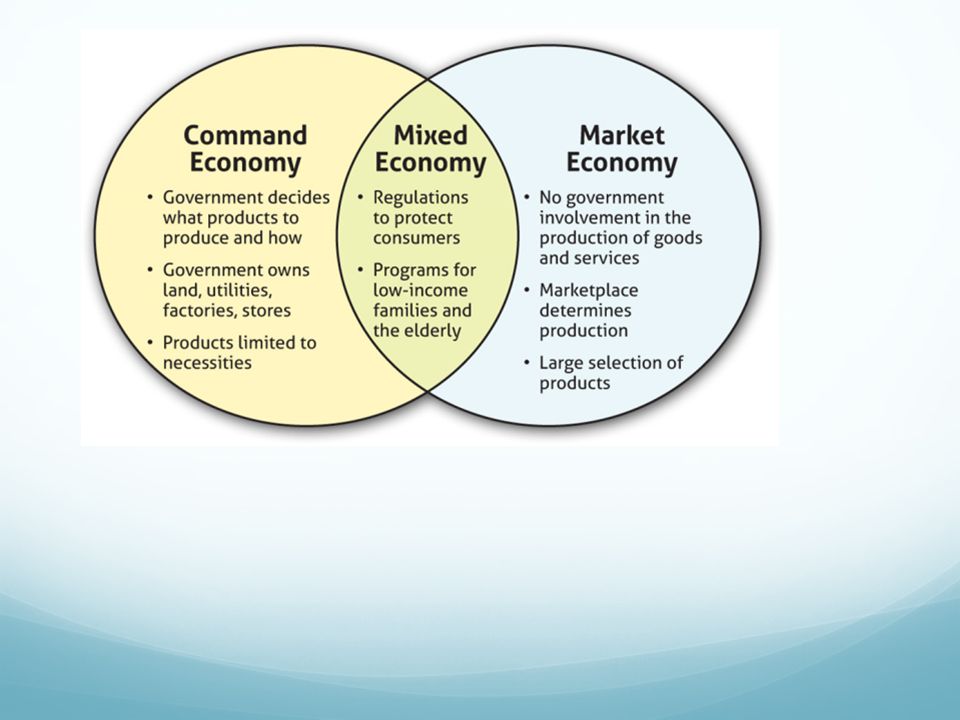

Types of Economic Systems Economic Systems Traditional Economy- economic questions answered by customs and traditions Command Economy- central authority controls all economic decisions Market Economy- supply, demand, pricing allow people to make economic decisions (market, not govt. controls economic decisions)

.")

14

Law of Supply and Demand When Demand exceeds supply Raise the price When Supply exceeds demand Lower the price Supply and Demand Determine prices & wages

15

Supply and Demand Supply How much producers are willing to produce at a certain price Demand How much consumers are willing to buy at a certain price

16

Supply & Demand Equilibrium Point Price @ which producers and consumers agree Result- no shortages or overages Surpluses Supply exceeds demands Result-lower prices encourage consumers to buy When do Surpluses most often occur in clothing stores? Shortages Demand exceeds supply Result-producers increase price to make profits What would be the result of a shortage of employees in an industry?

17

Influences on Supply

18

Demand Elasticity Elastic Demand Demand for products are affected by price & substitutes Inelastic Demand Price has little influence on demand Reason: necessities, brand loyalty

19

Review

20

What type of economy is the United States? Why? Mixed Economy- government has laws and regulations that control some aspects of the economy Describe how supply, demand, and scarcity affect a market economy Market economy- driven by consumer decisions. Consumers decide there is a demand for a specific good or service, then economy adapts to supply the goods or services. Scarcity and demand- drive producers to decide which goods to produce with limited resources List the factors that allow people to make economic decisions in a market economy Supply, demand, and system of pricing.

21

Financial System Financial Markets- Mechanism that provides means for purchasing and selling stocks, bonds, commodities Stocks Ownership shares in a corporation bonds- $$$ loaned to a company or government Commodities Agricultural (wheat, sugar), mining products (coal, irone ore)

, mining products (coal, irone ore)")

22

…financial markets What’s the purpose of the financial markets? Companies find investors and lenders Brings buyers and sellers together How can you make money with stocks? How do lenders make money with stocks? Investors- dividends, sell stock higher than purchased Lenders- paid interest What can influence the U.S. financial market? Economy, political unrest, govt. policies

23

Financial Institutions Depository Institutions Mange $$$$ deposited in institution Commercial banks Credit unions Savings and Loan Associations How do these institutions use YOUR money?

24

Financial Institutions Non-Depository Institutions link between savers and borrowers Sell securities and insurance policies Purpose- generate income and invest or lend funds they collect Types of Non-Depository Institutions Insurance companies Mutual funds Stock brokerage firms SEC regulates this industry

25

Non-Depository institutions Investment Bankers Help companies Issue new securities to investing public Assist investors by purchasing, trading stocks and bonds Mutual Fund Portfolios of stocks Individuals purchase shares in a mutual fund Brokerage Firms Buy and sell securities for individuals Provide advice on managing investments

26

Incentives Think of tasks that you do not enjoy or that you avoid doing. What type of incentive, or reward, would motivate you to do that task?

27

Business Incentives Rewards/bonus wages Workers sales Loyalty programs Consumers

28

Government Incentives Positive-Tax relief, tax incentives Negative- fines Producers 401k, Individual Retirement Accounts (IRAs)- not considered income for tax Specific stocks/bonds- ex.529 for tax deferred Savors & Investors Tax credits-example- energy efficient goods Purpose-increase consumer spending Citizens

- not considered income for tax Specific stocks/bonds- ex.529 for tax deferred Savors & Investors Tax credits-example- energy efficient goods Purpose-increase consumer spending Citizens")

Similar presentations

>")

Households Firms Government Foreigners Financial Markets.>")

>")