Download presentation

Presentation is loading. Please wait.

1

Revision of Accounting Concepts Important Accounting Concepts Accounting Equation

3

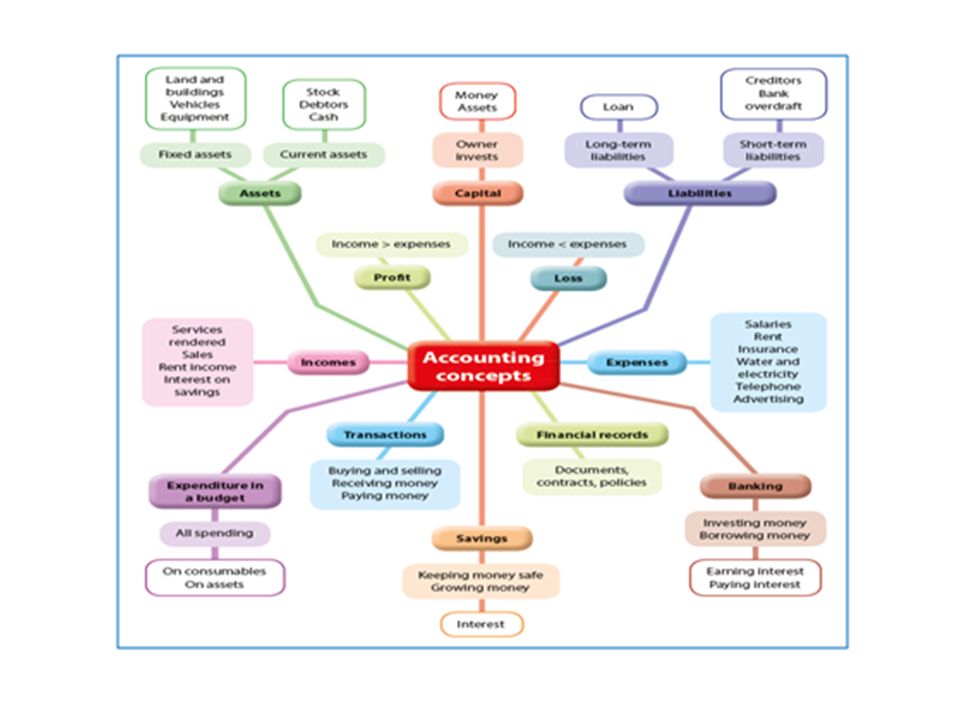

Assets Land and buildings, like shops Vehicles such as cars and trucks Equipment such as computers, furniture and machines Stock – the goods you sell to make money Debtors – people/businesses who owe you money Cash or money in the bank.

4

Different kinds of Assets Fixed Assets: (Non-current Assets) Land and buildings, Vehicles, Equipment, Machinery Current Assets: Trading Stock, Debtors, Cash/Bank

Land and buildings, Vehicles, Equipment, Machinery Current Assets: Trading Stock, Debtors, Cash/Bank")

5

Liabilities Loans – from banks, family or friends Creditors – businesses that you bought from, on account, and that you still owe money to.

6

Different kinds of Liabilities Long term liabilities (non- current liabilities) Loans – such as long term loans from a bank, or mortgage bonds (property loans). Short term liabilities (current liabilities)– creditors (suppliers to whom you owe money) SARS (tax and VAT owing).

– creditors (suppliers to whom you owe money) SARS (tax and VAT owing)..")

7

Owner’s equity Money invested by the owner Assets invested by the owner Profit made by the business.

8

Income Income received from sales Rent received from tenants Interest received from investments Money received from providing a service.

9

Expenses Salaries and wages paid to workers Advertising costs Rent paid Cost of goods sold Electricity and water Telephone or cell phone Transport..

10

What is the accounting equation? This relationship between assets, owner’s equity and liabilities is shown in the form of an equation or sum. ASSETS = OWNER’S EQUITY + LIABILITIES The owner invests money (capital), say R300 000 in the business. This money, together with the money borrowed from outsiders (loan) say R200 000, should equal the value of the assets of the business (land and buildings, equipment, vehicles, stock, cash and debtors) in other words, R500 000. R500 000 = R300 000 + R200 000

, say R in the business. This money, together with the money borrowed from outsiders (loan) say R , should equal the value of the assets of the business (land and buildings, equipment, vehicles, stock, cash and debtors) in other words, R R = R R")

11

The accounting equation

12

Important notes about the Accounting Equation ASSETS = OWNER’S EQUITY + LIABILITIES This then also means: OE = A – L L = A = OE OE + L = A After every transaction the Equation must always balance. A transaction always has a dual effect on the equation. (Two parts of the equation must change, or there must be a plus (+) and a (-) in one part of the equation. Step 1: Identify the two accounts involved Step 2: Decide if the two accounts are assets/liabilities or Owner’s Equity (Remember all incomes and expenses influence the Owner’s Equity) Step 3: Indicate the change by showing a + or a – or a 0 in the appropriate column Step 4: Check the logic – if you plus on the left-hand side of the = you HAVE to plus on the right hand side of the =

and a (-) in one part of the equation. Step 1: Identify the two accounts involved Step 2: Decide if the two accounts are assets/liabilities or Owner’s Equity (Remember all incomes and expenses influence the Owner’s Equity) Step 3: Indicate the change by showing a + or a – or a 0 in the appropriate column Step 4: Check the logic – if you plus on the left-hand side of the = you HAVE to plus on the right hand side of the =.")

13

REMEMBER: The accounting equation has two sides The TWO sides must always balance

14

Activity: Equation P. Pocket invested R20 000,00 in his business by depositing this amount into the business’ bank account. He bought stock for R10 000,00 cash. He borrowed R80 000,00 from a friend and deposited the money into his bank account. He bought a vehicle for R120 000,00 cash.

15

The accounting equation – example When the business receives money, for example from a service rendered, a profit is made which will increase the Owner’s equity, therefore Assets will increase (with the cash received) and Owner’s equity will increase with the income received. When a business pays for an expense such as the telephone or rent, then Assets will decrease as there is now less money and the Owner’s equity will also decrease as the expense will decrease the profit of the owner. Example: Paid R4000 for stationery and received R8000 for services rendered :

16

Apply the Equation practically Use the information below and calculate the total owners’ equity by using the equation A = OE + L

17

Answer Assets = Owner’s Equity + Liabilities R182 700 = R160 700 + R22 000

18

Consolidation Activity: Question 1 Define what income and expenses are. Use examples to explain your answer.

19

Answer Question 1 Income is the money a business earns through selling goods, by offering a service or by investing money – services rendered, rent income. Expenses are the payments which must be made to pay for goods and services which are used in the running of the business – electricity, wages, stationery.

20

Question 2 Identify the correct accounting name for the following transactions: Money received from services delivered by the business Bought envelopes Paid for an advert in the paper Received interest from the bank.

21

Answer Question 2 Services Rendered Stationery/Postage Advertisements Interest received

22

Question 3 3. Streaks-Ahead is a hairdressing business owned by Alex Tutton. Calculate whether her business has made a profit or a loss for October. Below is a list of all her income and expenses:

23

Answer Question 3 Incomes – Expenses = Profit Incomes: 24 500 + 590 +3 500 Expenses: R600 + R2 500 + R6 790 + R4 500 + R2 000 + R860 + R100 + R200 28 590 – 17 550 = R11 040

24

Question 4 Look at your answer to Question 3. a) Do you think Alex will be happy with the profit or loss made by her business?

Do you think Alex will be happy with the profit or loss made by her business .")

25

Answers Question 4 (a) a)Alex should be happy with the profit she has made, but perhaps R11 040 is not enough for her as it might be very hard work to run a hairdressing salon.

a)Alex should be happy with the profit she has made, but perhaps R is not enough for her as it might be very hard work to run a hairdressing salon.")

26

Question 4 (b) b) How much income did she make from selling shampoo?

b) How much income did she make from selling shampoo")

27

Answer Question 4 (b) b)R 3 500 – R2 000 = R1 500

b)R – R2 000 = R1 500")

28

Question 4 (c) c) Give Alex four suggestions on how she can increase her profit.

c) Give Alex four suggestions on how she can increase her profit.")

29

Answer Question 4 (c) Alex can cut down on expenses find cheaper suppliers or she can increase her turnover by taking on more clients run an advertising campaigns.

Alex can cut down on expenses find cheaper suppliers or she can increase her turnover by taking on more clients run an advertising campaigns.")

Similar presentations

1MEDA 144 Acctg Basics.>")

Then use the navigation.>")

, p>")

>")

Waikato Legal Services Mary Low Waikato Management School The University of Waikato.>")