Download presentation

Presentation is loading. Please wait.

1

CHOP February 26, 2010 Getting More Cash Into Your Practice

2

Objectives Learn More Techniques In Financial Counseling Bring More Cash In Through Appealing Denials Install Practice-Wide Cash Management

3

Market Trends More patients are paying out-of-pocket Changes in self-payments including: Increased co-pays Coinsurance payments Deductible payments Out-of-pocket payments for uninsured

4

Mean Health Insurance Costs Per Worker Hour for Employees with Access to Coverage, 1999-2005 Source: Kaiser Family Foundation analysis based on data from the National Compensation Survey, 1999-2005, conducted by the Bureau of Labor Statistics.

5

Out of Pocket Costs Are Too High (2005) NOTE: Insured includes those with public or private insurance coverage. SOURCE: Kaiser Commission on Medicaid and the Uninsured analysis of the Kaiser Low-Income Coverage and Access Survey 2005: National All-Income Sample. Percent of adults (age 19-64) reporting in past 12 months:

reporting in past 12 months:.")

6

Market Trends Deductibles are growing due to HDHP’s. 1.3 million have an HSA (1% of total insured population) 8.5 million have high deductible plans without HSA’s. (Per the Employee Benefit Research Group – 2006 Survey) $1 billion dollars invested in HSAs by Americans (according to data gathered by inside Consumer-Directed Care (ICDC) newsletter Feb. 24 issue ) More patients are paying out-of-pocket

8.5 million have high deductible plans without HSA’s. (Per the Employee Benefit Research Group – 2006 Survey) $1 billion dollars invested in HSAs by Americans (according to data gathered by inside Consumer-Directed Care (ICDC) newsletter Feb. 24 issue ) More patients are paying out-of-pocket.")

7

Decrease in Employer Sponsored Insurance (million) 3.6% National Unemployment Rate Increase since 2007 (from 4.9% in Dec-07 to 8.5% in Mar-09) = 3.6 3.9 Medicaid /CHIP Enrollment Increase (million) Uninsured Increase (million) & 8.9 Note: Totals may not sum due to rounding and other coverage. Source: John Holahan and Bowen Garrett, Rising Unemployment, Medicaid, and the Uninsured, prepared for the Kaiser Commission on Medicaid and the Uninsured, January 2009.Rising Unemployment, Medicaid, and the Uninsured Impact of the Rise in Unemployment on Health Coverage, 2007 to 2009

8

Uninsured Rates Among Nonelderly by State, 2007-2008 <14% Uninsured (18 states & DC) 14 to 18% Uninsured (18 states) National Average = 17% SOURCE: Kaiser Commission on Medicaid and the Uninsured/Urban Institute analysis of 2008 and 2009 ASEC Supplements to the CPS., two-year pooled data. AZ WA WY ID UT OR NV CA MT HI AK AR MS LA MN ND CO IA WI SD MOKS TN NM OK TX AL MI IL OH IN KY NC PA VA WV SC GA FL ME NY NH MA VT NJ DE MD RI DC CT >18% Uninsured (14 states) NE

NE.")

9

Physicians’ Net Income from Practice of Medicine and Percent Change vs. Private Sector Occupations (1995, 1999, 2003) Average Reported Net Income (dollars) Average Net Income, Inflation Adjusted (1995 dollars) Percent Change in Inflation- Adjusted Income 199519992003199519992003199519992003 All Patient Care Physicians 180,930186,768202,982180,930170,850168,122-5.6%*-1.6%-7.1%* Primary Care Physicians 135,036138,018146,405135,036126,255121,262-6.5*-4.0*-10.2* Specialists210,225218,819235,820210,225200,169195,320-4.8*-2.4-7.1* Medical Specialists 178,840193,161211,299178,840176,698175,011-1.2-2.1 Surgical Specialists 245,162255,011271,652245,162233,276224,998-4.9-3.6-8.2* Private Sector Professional, Technical, Specialty Occupations^ N/A 4.32.56.9 *Rate of change is statistically significant at p<.05. N/A: Not available. ^The Bureau of Labor Statistics (BLS) Employment Cost Index of wages and salaries for private sector “professional, technical and specialty” workers was used by the Center for Studying Health System Change (HSC) to calculate estimates for these workers; significance tests were not available for these estimates. HSC calculated inflation-adjusted estimates using the BLS online inflation calculator (http://146.142.4.24/cgi-bin/cpicalc.pl).http://146.142.4.24/cgi-bin/cpicalc.pl Source: Center for Studying Health System Change, Community Tracking Study Physician Survey, Losing Ground: Physician Income, 1995- 2003, Tracking Report No. 15, June 2006, Table 1, at http://www.hschange.com/CONTENT/851/851.pdf.http://www.hschange.com/CONTENT/851/851.pdf

Average Reported Net Income (dollars) Average Net Income, Inflation Adjusted (1995 dollars) Percent Change in Inflation- Adjusted Income All Patient Care Physicians 180,930186,768202,982180,930170,850168, %*-1.6%-7.1%* Primary Care Physicians 135,036138,018146,405135,036126,255121, *-4.0*-10.2* Specialists210,225218,819235,820210,225200,169195, * * Medical Specialists 178,840193,161211,299178,840176,698175, Surgical Specialists 245,162255,011271,652245,162233,276224, * Private Sector Professional, Technical, Specialty Occupations^ N/A *Rate of change is statistically significant at p<.05. N/A: Not available. ^The Bureau of Labor Statistics (BLS) Employment Cost Index of wages and salaries for private sector professional, technical and specialty workers was used by the Center for Studying Health System Change (HSC) to calculate estimates for these workers; significance tests were not available for these estimates. HSC calculated inflation-adjusted estimates using the BLS online inflation calculator ( Source: Center for Studying Health System Change, Community Tracking Study Physician Survey, Losing Ground: Physician Income, , Tracking Report No. 15, June 2006, Table 1, at")

10

Declining Physician Compensation Source: MGMA Median Compensation Survey

11

Market Trends Below are the estimated recovery percentages by control point for inpatients Pre-Admission (100%) Admission (75-80 %) Inpatient (65-75%) At Discharge (60-70%) One Month After Discharge (<40%) The bottom line is: when you are in the patient’s mindset, you can collect!

Admission (75-80 %) Inpatient (65-75%) At Discharge (60-70%) One Month After Discharge (<40%) The bottom line is: when you are in the patient’s mindset, you can collect!")

12

What can you do to gain success in your collections efforts? Think that the Financial Counseling Process does not end until the $$ is in the bank

13

FIRST STEPS Ensure that your physicians are committed to collecting money---that means they cannot give out the double message to patients. It does not help anything if they tell patients not to ever worry about money. There message should be…”our financial counselor will assist you with finding ways to pay for your care…” Nothing will improve without provider support.

14

Pre-Visit Collect demographic information. Collect insurance information. Explain conditions of treatment meaning financial terms. Clarify who is responsible for the bill. Verify insurance and benefits. Obtain authorizations and/or referrals for the services you know about.

15

Insurance Verification Check List Patient has the insurance they say they do and it is primary with effective date Insurance address for bill Plan type: HMO/PPO/other Deductibles impacting care delivered in the office, e.g. IV drugs, radiology, labs, chemotherapy administration Episodic patient cost sharing for care delivered in the office, e.g. flat copays for Rx; coinsurance payments, amount Lifetime, annual or episode out of pocket maximum Catastrophic coverage (yes/no) Benefit caps: lifetime or other If possible, patients’ current status regarding deductibles and out of pocket maximums; current progress toward caps Insurer requirements: Prior authorization; certification; notification; case management, step therapy Specialty pharmacy preference for patient costs, pharmacy billing.

Benefit caps: lifetime or other If possible, patients’ current status regarding deductibles and out of pocket maximums; current progress toward caps Insurer requirements: Prior authorization; certification; notification; case management, step therapy Specialty pharmacy preference for patient costs, pharmacy billing..")

16

Do You Want to Treat? Insured patients---yes! Underinsured/ uninsured Do they have $$$ or assets? Will they pay? Do they qualify for Medicaid? Do they qualify for other assistance in your state? Can they be insured by patient assistance or Foundations? Can they go on a trial? Remember: Foundations will fund premiums only if there is a specific request

17

Process Improvements: Pre-Visit If uninsured, begin the process before the patient arrives… “To best serve you at this practice, we need for you to bring in your tax returns for the last three years or another form of proof of income when you come to the office for your first visit. We can try to get funding for your treatment, if you qualify…”

18

Process Improvements: Pre-Visit Deliver a consistent message to patients about their financial responsibility and continually educate them on their specific benefit plan. Each patient that visits should sign a conditions of treatment that includes: Obligation to pay patient costs Obligation to obtain referrals Obligation to inform you of change in insurance, employment or care status Be party to a collection effort, if they fail to pay their bill.

19

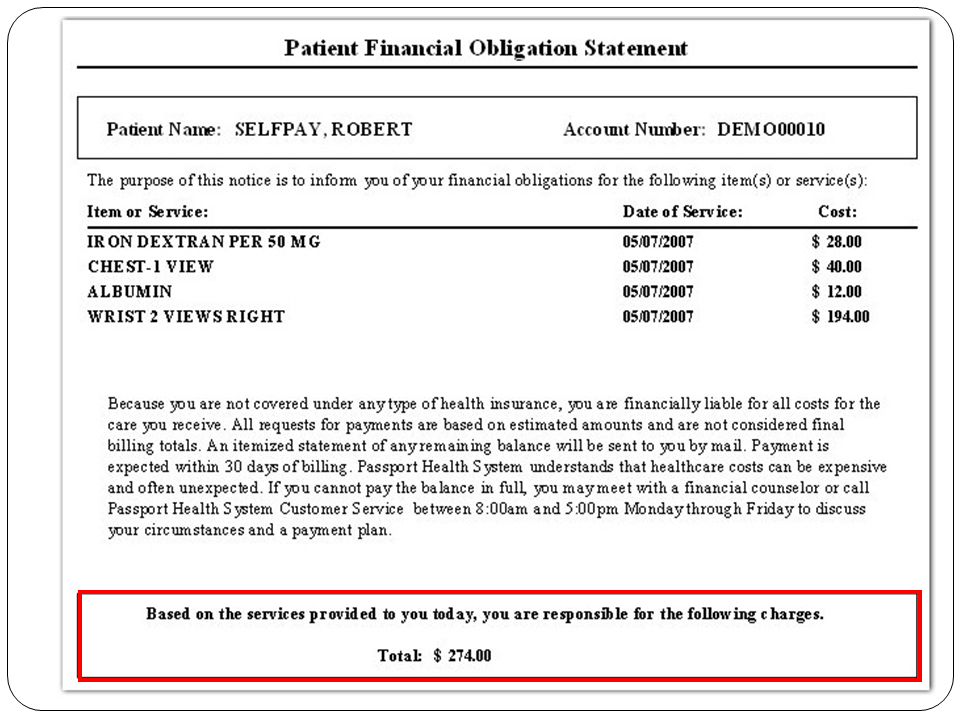

Process Improvements: The First VISIT Provide detailed explanations where appropriate. Train registration staff on how to present the conditions of treatment forms and create scripts to support the process Allow time in the registration process for the registrar to more fully review the forms with the patient or consult with the financial counselor. Have the forms signed and return a copy to the patient. Use a Patient Financial Obligation Statement that they should sign prior to their first TREATMENT Tip: Statement content can vary from illustrating co-pay, deductible and coinsurance information to much more complex calculations, such as those that regimen specific and payer-specific (contractual database or use your ERA data).

..")

21

Process Improvements: FIRST VISIT For insured patients, do the following: Review treatment plan thoroughly (if and when it is available) Explain treatment alternatives, if there are any. Calculate out-of-pocket costs if you know them and provide the patient with approximate time frame for these costs. Inform patient of the obligation to pay patient costs at the time of the visit, if possible. Take a deposit for the first round of chemo if it is occurring that day. Take credit cards in case bills are not paid or if the patient prefers to pay by credit card. Answer any questions the patient or family may have. Perform a credit check, if the patient will owe more than benchmark amount (≥ $5000)

.")

22

Process Improvements: Patient Financial Counseling Collecting money from patients can be both a challenge and a delicate situation if not handled properly. Remember their care is a higher priority than collecting payment, but collecting cannot be ignored.

23

Process Improvements: Financial Counseling Sample script with insurance: “We have verified your benefits. The good news is your insurance company is covering the majority of your bill. Today all you are responsible for is $XX. How would you like to pay today: cash, check, or credit card?” Increase points of collections----ever thought of putting an ATM outside of your office or in the waiting room? REMEMBER: Patients with insurance often think their bills are paid !

24

Uninsured and Underinsured: The Visit These patients can be treated in the hospital---but do not give up too easily…they need a financial interview and they need to bring the following: Three years of tax statements or proof of income Statements of working assets---IRAs, 401K, life insurance, annuities, etc., if you consider them r the programs for the patients do Bank references for patients who have a high self-pay balances Credit cards Proof of Medicaid rejection, if they are going the PAP route

25

High Balance Patients—The VISIT UNINSURED PATIENTS: DO THEY QUALIFY FOR PAP or FOUNDATIONS? The 2009 Poverty Guidelines for the 48 Contiguous States and the District of Columbia Persons in familyPoverty guideline 1$10,830 214,570 = 500% = $72,050 318,310 422,050 525,790 629,530 733,270 837,010 For families with more than 8 persons, add $3,740 for each additional person.

26

High Balance Patients—The VISIT Some PAPs besides having an income requirement have an asset requirement. What is this? Not the patient’s house or car Retirement funds: 401K, IRA, SEP Stocks, marketable securities Other real estate Other investment transactions

27

High Balance Patients—The VISIT Why do all of this? Manage the patient and provider expectations Get patient through the process faster…right now it takes a long time Be prepared with next steps for patients who do not qualify But, bottom line, keep as many folks with you as possible.

28

Financial & Insurance Verification Patient is referred to Oncologist and Dx/Tx determined Locate & Evaluate Assistance Programs Call/ascertain Program Requirements Entire application submitted Notification of approval or denial Patient completes patient portion Practice completes office portion 32 min 62 min 44 min 33 min 2160 min (36 hrs) 11400 min (190 hrs) (7.9 days) 1%16%83% Percent of Processing Time Analyze Value Stream Process Map 99% of the Process Time Involves Two Process Steps Source: E-Expert Reimbursement Partners 2008 PAP Survey

min (190 hrs) (7.9 days) 1%16%83% Percent of Processing Time Analyze Value Stream Process Map 99% of the Process Time Involves Two Process Steps Source: E-Expert Reimbursement Partners 2008 PAP Survey")

29

Alternatives for Patients Other facilities Clinical Trials Treat them anyway Working their assets---what?

30

Working Assets Viatical and Other Insurance Settlements Restructuring Retirement Funds Payment Plans Automatic Credit Card Withdrawals

31

What is a life or viatical settlement? A life or viatical settlement is a proven financial strategy that enables eligible policy holders to sell their life insurance to a funding institution and receive a lump sum of cash. This also means the patient does not need to pay premiums.

32

Please note that the definitions of these terms vary by state. What is the difference between a life and a viatical settlement? Life settlements generally involve individuals over the age of 65. Viatical settlements generally involve individuals of any age who are terminally or chronically ill.

33

Financial Counseling & collections The financial counseling process does not end after the first visit. Any patient with an outstanding balance over 30 days of over $5000 should be counseled. Alternatives involving credit and assets should be offered. Also remember that some patients will spend down to Medicaid levels.

34

Increase your collections Train your staff on how to ask for payment. Introduce scripts if necessary. Prepared answers for the more common objections for non-payment will give your staff the confidence to be more assertive.

35

PUT INCENTIVES IN PLACE For lowering patient balances or DSO For successful PAP applications in less than 5 days For collection of patient balances over $5-10K For lowering the number of patients that are sent to the hospital For overall reduction in DSO or denials

36

Who Makes A Good Financial Counselor Someone who understands practice finance and collections. Someone who is tactful and empathizes well with patients and caregivers Someone who can talk about finances without wincing or being afraid to ask for what they need. Someone who does not give up easily. Someone with astute quantitative skills.

37

Make Everyone A FC Have a Contract Book at your Front Desk Pictures of Insurance Cards Pre-Auth, Referrals Needed With E-mails or Telephone Numbers Employers Who Use, if Applicable Contract Copays and Deductibles In-network, Out-of-Network Contracted Rates (for billing) Contracted Pharmacies Discharge Area with scripts, appointments, and charging. Signs in waiting room.

38

Best Practice: ESA “Gatekeeper” What is that? If you have physicians who give ESAs either because they do not know the lab results OR they choose to ignore them, you need one or more gatekeeper(s). This means that patients may not get ESAs until the “gatekeeper” has approved them after reviewing the latest lab result.

. This means that patients may not get ESAs until the gatekeeper has approved them after reviewing the latest lab result..")

39

Denials Are All Around! Denied claims as a percent of claims 10% -15% or more in many practices Medicare alone denies approximately 6.3% of all line items billed Estimated cost to work a denial is $25 - $30 per claim

40

PART A & PART B PROCESS (Non-Expedited) Beneficiary receives the service Medicare contractor (fiscal intermediary or carrier or MAC) issues initial determination explaining whether Medicare will pay for a service already received. Beneficiary has 120 days to request redetermination by contractor. Provider may also request redetermination Appeals will be consolidated Time frame may be extended for “good cause” Contractor has 60 days to issue redetermination

41

PART B APPEALS (cont.) If redetermination is unfavorable can request a“reconsideration” by Quality Independent Contractor (“QIC”) 120 days to request reconsideration Beneficiary & provider appeals will be consolidated Time may be extended for good cause Must fill out a reconsideration form which is available at http://www.cms.hhs.gov/cmsforms/downloads/cms20033.pdf QIC must issue decision within 60 days. Parties may request escalation to ALJ if time frame not met 60 days to request review by ALJ

42

ALJ HEARINGS Hearings conducted by Medicare ALJs in DHHS Office of Medicare Hearings and Appeals Minimum amount disputed must be $120 in 2008; $124 in 2009. ALJs are in 4 regional offices, not local offices Must fill out the ALJ request form ( http://www.cms.hhs.gov/cmsforms/downloads/cms20034ab.pdf ) For Part A and Part B claims, ALJ must issue decision within 90 days – with exceptions No time limit if request for in-person hearing granted

For Part A and Part B claims, ALJ must issue decision within 90 days – with exceptions No time limit if request for in-person hearing granted.")

43

ALJ HEARINGS (cont.) For ALJ hearings under Parts A, B, C & D Amount of claim must be at least $120 in 2008 (changes annually) Subject to annual increase Can aggregate certain claims Hearings conducted by video teleconferencing (VTC) if available, or by telephone ALJ assigned to case has discretion to grant request for in-person hearing

For ALJ hearings under Parts A, B, C & D Amount of claim must be at least $120 in 2008 (changes annually) Subject to annual increase Can aggregate certain claims Hearings conducted by video teleconferencing (VTC) if available, or by telephone ALJ assigned to case has discretion to grant request for in-person hearing")

44

APPEALS PROCESS – BEYOND THE ALJ HEARING If ALJ decision is unfavorable, have 60 days to request an Appeals Council review (address will be in the rejection letter) Must be in writing within 60 days after the ALJ decision, Appeals Council reviews the record concerning only those issues, unless unrepresented beneficiary requests. If Appeals Council decision is unfavorable, have 60 days to request review in federal court Must meet amount in controversy requirement Amount may increase each year ($1180 in 2008)

.")

45

CALCULATING TIME FRAMES Time frames are generally calculated from date of receipt of notice 5 days added to notice date Time frames sometimes extended for good cause, examples include: Serious illness Death in family Records destroyed by fire/flood, etc Did not receive notice Wrong information from contractor Sent request in good faith but it did not arrive

46

MEDICARE ADVANTAGE APPEALS “Organization determination” is initial determination regarding basic and optional benefits Can be provided before or after services received Issued within 14 days May request expedited organization determination if delay could jeopardize life/health or ability to regain maximum function. Plan must treat as expedited if requested by doctor Issued within 72 hours

47

MEDICARE ADVANTAGE (MA) Request reconsideration w/i 60 days of notice of the organization determination. Reconsideration decision issued within 30 days for standard reconsideration. 72 hours for expedited reconsideration. Unfavorable reconsiderations automatically referred to independent review entity (IRE). Time frame for decision set by contract, not regulation Unfavorable IRE decisions may be appealed to ALJ to MAC to Federal Court

. Time frame for decision set by contract, not regulation Unfavorable IRE decisions may be appealed to ALJ to MAC to Federal Court.")

48

MEDICARE ADVANTAGE (MA) Fast-Track Appeals to Independent Review Entity (IRE) before services end for Terminations of home health, SNF, CORF Two-day advance notice Request review by noon of day after receive notice IRE issues decision by noon of day after day it receives appeal request 60 days to request reconsideration by IRE 14 days for IRE to act

Fast-Track Appeals to Independent Review Entity (IRE) before services end for Terminations of home health, SNF, CORF Two-day advance notice Request review by noon of day after receive notice IRE issues decision by noon of day after day it receives appeal request 60 days to request reconsideration by IRE 14 days for IRE to act")

49

MEDICARE ADVANTAGE GRIEVANCE PROCEDURES Grievance procedures to address complaints that are not organization determinations. 60 after the event or incident to request grievance Decision no later than 30 days of receipt of grievance. 24 hours for grievance concerning denial of request for expedited review.

50

PART D APPEALS PROCESS- OVERVIEW Each drug plan must have an appeals process Including process for expedited requests A coverage determination is first step to get into the appeals process Issued by the drug plan An “exception” is a type of coverage determination Next steps include Redetermination by the drug plan Reconsideration by the independent review entity (IRE) Administrative law judge (ALJ) hearing Medicare Appeals Council (MAC) review Federal court

Administrative law judge (ALJ) hearing Medicare Appeals Council (MAC) review Federal court")

51

PART D APPEALS PROCESS – COVERAGE DETERMINATION A coverage determination may be requested by A beneficiary A beneficiary’s appointed representative Prescribing physician Drug plan must issue coverage determination as expeditiously as enrollee’s health requires, but no later than 72 hours standard request Including when beneficiary already paid for drug 24 hours if expedited- standard time frame jeopardize life/health of beneficiary or ability to regain maximum function.

52

EXCEPTIONS: A SUBSET OF COVERAGE DETERMINATION An exception is a type of coverage determination and gets enrollee into the appeals process Beneficiaries may request an exception To cover non-formulary drugs To waive utilization management requirements To reduce cost sharing for formulary drug No exception for specialty drugs or to reduce costs to tier for generic drugs A doctor must submit a statement in support of the exception

53

PART D APPEALS - COVERAGE DETERMINATIONS ARE NOT AUTOMATIC A statement by the pharmacy (not by the Plan) that the Plan will not cover a requested drug is not a coverage determination Enrollee who wants to appeal must contact drug plan to get a coverage determination Drug plan must arrange with network pharmacies To post generic notice telling enrollees to contact plan if they disagree with information provided by pharmacist or To distribute generic notice

that the Plan will not cover a requested drug is not a coverage determination Enrollee who wants to appeal must contact drug plan to get a coverage determination Drug plan must arrange with network pharmacies To post generic notice telling enrollees to contact plan if they disagree with information provided by pharmacist or To distribute generic notice")

54

PART D APPEALS PROCESS NEXT STEPS If a coverage determination is unfavorable: Redetermination by the drug plan. Beneficiary has 60 days to file written request (plan may accept oral requests). Plan must act within 7 days - standard Plan must act within 72 hrs.- expedited Then, Reconsideration by IRE Beneficiary has 60 days to file written request IRE must act w/i 7 days standard, 72 hrs. expedited ALJ hearing MAC review Federal court

. Plan must act within 7 days - standard Plan must act within 72 hrs.- expedited Then, Reconsideration by IRE Beneficiary has 60 days to file written request IRE must act w/i 7 days standard, 72 hrs. expedited ALJ hearing MAC review Federal court.")

55

PART D GRIEVANCE PROCESS Each drug plan must have a separate grievance process to address issues that are not appeals May be filed orally /in writing w/i 60 days Plans must resolve grievances w/i 30 days generally w/i 24 hrs if arise from decision not to expedite coverage determination or redetermination

56

USEFUL WEBSITES www.medicare.gov www.medicareadvocacy.org www.healthassistancepartnership.org

57

Private Insurance Appeals Appeals process must be outlined in the contract. Sometimes, it is outlined on the payer’s web site. Do not contract with a payer unless you know their appeals process.

58

Appeals Process: Internal Assess the denial and damage Gather data Draft letter Follow up Guerilla tactics

59

Guerrilla Tactics Involve a lawyer---if only a cc Employer/ Union For Medicare or Medicaid Local representation HHS Regional Office State Insurance Commissioner State Medical Society The Press

60

Stop the Bleeding Do you have a denial management strategy? Do you have an ERA (835) Analyzer? What are your top five denials by payer? by dollar amount? by type? How do you prioritize denials? How long does it take to address them? How many claims are improperly paid? What is your plan to improve your denial rate?

Analyzer. What are your top five denials by payer. by dollar amount. by type. How do you prioritize denials. How long does it take to address them. How many claims are improperly paid. What is your plan to improve your denial rate .")

61

Find The Bleeding Front Desk Poor demographics No payer contact information Insurance changes not tracked Change of patient address Wrong guarantor No signature on financial commitment form

62

Find the Bleeding Insurance verification/ Billing Lack of authorization Patient not eligible MA not Medicare Insurance ceiling not identified Deductible fulfillment not tracked Coordination of benefits MSP Catastrophic coverage

63

Find the Bleeding Charge capture/billing Coding Billing for supervising physician Medical necessity Support for unlisted codes Timely filing Duplicate claims Inability to write off small amounts

64

Find the Bleeding Clinicians Change of diagnosis Poor charge capture Off-label use with no ABN Dictation delays No submission of hospital charges

65

Solutions Front Desk/ Financial Counseling Technology Eligibility/verification products On-line eligibility verification Insurance company websites Contract book Establish standardized registration polices, procedures, processes and performance levels Ensure that registration staff is thoroughly trained Insurance plans and requirements prior to treatment Plan requirements, e.g., referrals, authorizations Importance of correct demographics

66

Solutions Charge Posting Computerized coding tools Updated charge capture/Superbills Claims editors Claims “scrubbers” Online access to Medicare policies for all providers

67

Strategies Advanced Financial Counseling is a real key to success… Focus on the problem as an organization-wide opportunity to recover revenue---everyone has to participate! Maintain an electronic folder of winning appeal letters and make it an accessible library. Invest in systems to track, work and report denials, e.g. 835 analyzers Develop standards for reporting types of denials and communicate this information Assign responsibility for denials and reward people for improvements in denial rates Measure improvement on an ongoing basis.

Similar presentations