Download presentation

Presentation is loading. Please wait.

1

Module 6 Reporting and Analyzing Operating Assets

2

Accounts Receivable When companies sell to other companies, they offer credit terms, which are called sales on credit (or credit sales or sales on account). When companies sell to other companies, they offer credit terms, which are called sales on credit (or credit sales or sales on account). Accounts receivable are reported on the balance sheet of the seller at net realizable value, which is the net amount the seller expects to collect. Accounts receivable are reported on the balance sheet of the seller at net realizable value, which is the net amount the seller expects to collect.

. Accounts receivable are reported on the balance sheet of the seller at net realizable value, which is the net amount the seller expects to collect. Accounts receivable are reported on the balance sheet of the seller at net realizable value, which is the net amount the seller expects to collect..")

3

Cisco Systems, Inc. Current Assets Note: Cisco’s Accounts Receivable are reported net of a $177 million allowance for uncollectible accounts.

4

Allowance for Uncollectible Accounts The amount of expected uncollectible accounts is usually computed based on an aging analysis. The amount of expected uncollectible accounts is usually computed based on an aging analysis. Each customer’s account balance is categorized by the number of days or months the underlying invoices have remained outstanding. Each customer’s account balance is categorized by the number of days or months the underlying invoices have remained outstanding. Based on prior experience or on other available statistics, bad debts percentages are applied to each of these categorized amounts, with larger percentages being applied to older accounts. Based on prior experience or on other available statistics, bad debts percentages are applied to each of these categorized amounts, with larger percentages being applied to older accounts.

5

Aging Analysis Example GAAP requires companies to disclose the amount of the allowance for uncollectible accounts, either on the face of the balance sheet or in the notes. Companies are also required to disclose their accounting policies with respect to receivables.

6

Reporting Accounts Receivable Given our gross balance of $100,000 and estimated uncollectible accounts of $2,900, accounts receivable will be reported as follows:

7

3M’s Current Assets

8

Bad Debt Expense Bad Debt Expense is equal to the increase in the allowance for uncollectible accounts. Bad Debt Expense is equal to the increase in the allowance for uncollectible accounts. In our previous example, if a previous balance of $2,200 existed in the allowance for uncollectible accounts, the company would record a bad debt expense of $700. In our previous example, if a previous balance of $2,200 existed in the allowance for uncollectible accounts, the company would record a bad debt expense of $700. If the allowance for uncollectible accounts has a prior balance of $(1,000), bad debt expense would be $1,700. If the allowance for uncollectible accounts has a prior balance of $(1,000), bad debt expense would be $1,700.

, bad debt expense would be $1,700. If the allowance for uncollectible accounts has a prior balance of $(1,000), bad debt expense would be $1,700..")

9

Write-off of Uncollectible Accounts The write-off of an uncollecitble account does not affect income. The amount written-off is reflected as a reduction of the account receivable balance and the allowance for uncollectible accounts: The write-off of an uncollecitble account does not affect income. The amount written-off is reflected as a reduction of the account receivable balance and the allowance for uncollectible accounts:

10

Accounts Receivable Transactions

11

Cisco’s Receivable Footnote

12

Cisco’s Allowance for Doubtful Accounts Footnote

13

Income Shifting By underestimating the provision, expense is reduced in the income statement, thus increasing current period income. By underestimating the provision, expense is reduced in the income statement, thus increasing current period income. In one or more future periods, when write-offs occur for which the company should have provisioned earlier, it must then increase the provision to make up for the underestimated provision for the earlier period. In one or more future periods, when write-offs occur for which the company should have provisioned earlier, it must then increase the provision to make up for the underestimated provision for the earlier period. This reduces income in one or more subsequent periods. Income has, thus, been shifted (borrowed) from a future period into the current period. This reduces income in one or more subsequent periods. Income has, thus, been shifted (borrowed) from a future period into the current period.

from a future period into the current period. This reduces income in one or more subsequent periods. Income has, thus, been shifted (borrowed) from a future period into the current period..")

14

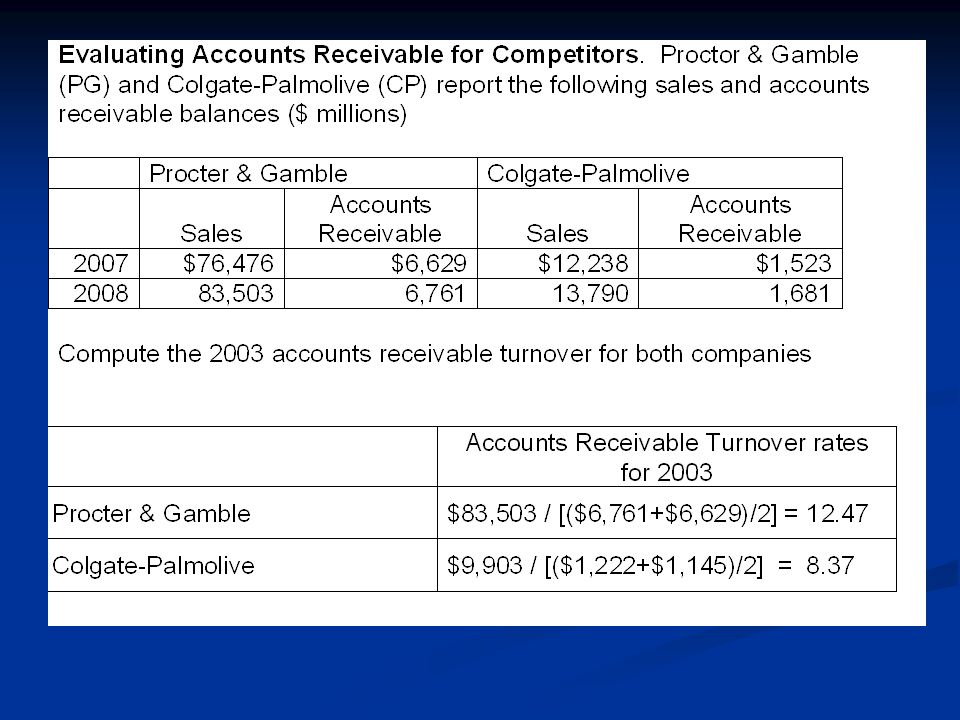

Receivables Turnover Rate The accounts receivable turnover rate reveals how many times receivables have turned (been collected) during the period. The accounts receivable turnover rate reveals how many times receivables have turned (been collected) during the period. More turns indicate that receivables are being collected quickly More turns indicate that receivables are being collected quickly

during the period. More turns indicate that receivables are being collected quickly More turns indicate that receivables are being collected quickly.")

15

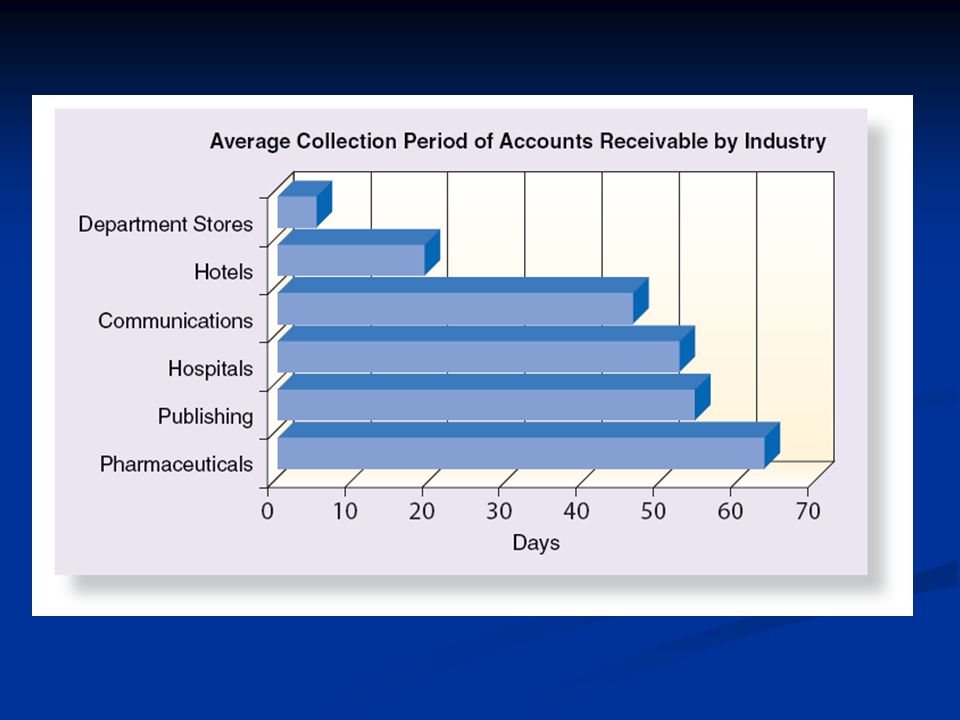

Days Sales in Receivables A companion ratio is the Average Collection Period: A companion ratio is the Average Collection Period:

16

Example Suppose that Suppose that sales are $1,000 sales are $1,000 ending accounts receivable are $230 ending accounts receivable are $230 average accounts receivable are $200. average accounts receivable are $200.

18

Insights from Accounts Receivable Turnover 1. 1. If turnover slows, the reason could be deterioration in collectibility. However, there are at least three alternative explanations: A seller can extend its credit terms. A seller can take on longer-paying customers. The seller can increase the allowance provision. 2. Asset utilization Asset turnover is often viewed as an important dimension of financial performance, both by managers for internal performance goals, as well as by the market in evaluating investment choices.

19

Receivable Turnover Rates for Selected Companies

21

Inventories Inventory costs either are reported on the balance sheet or they are transferred to the income statement as an expense (cost of goods sold) to match against sales revenues. Inventory costs either are reported on the balance sheet or they are transferred to the income statement as an expense (cost of goods sold) to match against sales revenues. The process by which costs are removed from the balance sheet is important. The process by which costs are removed from the balance sheet is important.

to match against sales revenues. The process by which costs are removed from the balance sheet is important. The process by which costs are removed from the balance sheet is important..")

22

Manufacturing Costs Raw materials cost is relatively easy to compute. Design specifications list the components of each product, and their purchase costs are readily determined. Raw materials cost is relatively easy to compute. Design specifications list the components of each product, and their purchase costs are readily determined. Labor cost in a unit of inventory is based on how long each unit takes to build and the rates for each labor class working on that product. Labor cost in a unit of inventory is based on how long each unit takes to build and the rates for each labor class working on that product. Overhead costs include the manufacturing plant depreciation, utilities, plant supervisory personnel, and so forth. Overhead costs include the manufacturing plant depreciation, utilities, plant supervisory personnel, and so forth.

23

Cost of Goods Sold When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as cost of goods sold (COGS). COGS is then matched against sales revenue to yield gross profit: When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as cost of goods sold (COGS). COGS is then matched against sales revenue to yield gross profit: Sales revenue Sales revenue - COGS - COGS Gross profit Gross profit

. COGS is then matched against sales revenue to yield gross profit: Sales revenue Sales revenue - COGS - COGS Gross profit Gross profit.")

24

Inventory Cost Flows to Financial Statements

25

Inventory Costing Methods First-In. First-Out (FIFO). This method assumes that the first units purchased are the first units sold. First-In. First-Out (FIFO). This method assumes that the first units purchased are the first units sold. Last-In, First-Out (LIFO). The LIFO inventory costing method assumes that the last units purchased are the first to be sold. Last-In, First-Out (LIFO). The LIFO inventory costing method assumes that the last units purchased are the first to be sold. Average cost. The average cost method assumes that the units are sold without regard to the order in which they are purchased. Instead, it computes COGS and ending inventories as a simple weighted average. Average cost. The average cost method assumes that the units are sold without regard to the order in which they are purchased. Instead, it computes COGS and ending inventories as a simple weighted average.

. This method assumes that the first units purchased are the first units sold. Last-In, First-Out (LIFO). The LIFO inventory costing method assumes that the last units purchased are the first to be sold. Last-In, First-Out (LIFO). The LIFO inventory costing method assumes that the last units purchased are the first to be sold. Average cost. The average cost method assumes that the units are sold without regard to the order in which they are purchased. Instead, it computes COGS and ending inventories as a simple weighted average. Average cost. The average cost method assumes that the units are sold without regard to the order in which they are purchased. Instead, it computes COGS and ending inventories as a simple weighted average..")

26

FIFO Inventory Costing:

27

LIFO Inventory Costing

28

Weighted Average Inventory Costing Weighted Average = $80,000 / 700 units = $114.286 / unit

29

Cisco’s Inventory Footnote This footnote includes at least two items of interest for our analysis of inventory: Cisco uses the FIFO method of inventory costing. Inventories are reported at the lower of cost or market (LCM), which means that inventory is written down if its replacement cost, referred to as ‘market,’ declines below its balance sheet cost

, which means that inventory is written down if its replacement cost, referred to as ‘market,’ declines below its balance sheet cost.")

30

Cisco’s Inventories

31

Lower of Cost or Market Companies must write down the carrying amount of inventories on the balance sheet if the reported cost exceeds market value. lower of cost or market This process is called reporting inventories at the lower of cost or market and creates the following financial statement effects: Inventory book value is written down to current market value (replacement cost); reducing inventory and total assets. Inventory write-down is reflected as an expense on the income statement.

; reducing inventory and total assets. Inventory write-down is reflected as an expense on the income statement..")

32

LCM Illustration To illustrate, assume that a company has inventory on its balance sheet at a cost of $27,000. Management learns that the inventory’s replacement cost is $23,000 and writes inventories down to a balance of $23,000. The following financial statement effects template shows the adjustment.

33

Inventory Costing Effects on Income Statement

34

FIFO’s “Phantom Profits” Assume a FIFO inventory costing method: Beginning Inventory 1/01/04: 35 units @ $1.20 Purchase of 20 units @ $1.35 Ending Inventory 03/31/04: 10 units 45 units were sold at a price of $2.75/unit Gross profit is computed as follows: Sales (45 x $2.75)$123.75 FIFO COGS (35 @ $1.20 + 10 @ $1.35) 55.50 Gross Profit$ 68.25 Q: What portion of the gross profit is “economic” and what portion is the “holding gain”?

$ FIFO COGS $ $1.35) Gross Profit$ Q: What portion of the gross profit is economic and what portion is the holding gain")

35

Phantom profit consists of both economic profit and holding gain. Economic profit is the number of units sold multiplied by the difference between the sales price and the replacement cost of the inventories. Holding gain is the increase in replacement cost since the inventories were acquired, which equals the number of units sold multiplied by the difference between the current replacement cost and the original acquisition cost. This is typically approximated by the LIFO reserve (the difference between LIFO and FIFO inventories). Solution: Economic Profit: 45 units x ($2.75-$1.35)$63.00 Holding Gain: 35 units x ($1.35-$1.20)5.25 $68.25

. Solution: Economic Profit: 45 units x ($2.75-$1.35)$63.00 Holding Gain: 35 units x ($1.35-$1.20)5.25 $")

36

Inventory Costing Effects on Cash Flows One reason frequently cited for using LIFO is the reduced tax liability in periods of rising prices. One reason frequently cited for using LIFO is the reduced tax liability in periods of rising prices. Companies using LIFO are required to disclose the amount at which inventories would have been reported had it used FIFO. Companies using LIFO are required to disclose the amount at which inventories would have been reported had it used FIFO. The difference between these two amounts is called the LIFO reserve. The difference between these two amounts is called the LIFO reserve.

37

CAT’s LIFO Reserve The use of LIFO has reduced the carrying amount of 2007 inventories by $2,617 million. This difference, referred to as the LIFO reserve, is the amount that must be added to LIFO inventories to adjust them to their FIFO value.

38

LIFO’s Cash Savings for CAT Use of LIFO reduced CAT’s inventories by $2,617 million, resulting in a cumulative increase in cost of goods sold and a cumulative decrease in gross profit and pretax profit of that same amount. Because CAT also uses LIFO for tax purposes, the decrease in pretax profits reduced CAT’s cumulative tax bill by about $916 million ($2,617 million 35% assumed corporate tax rate).

..")

39

Gross profit analysis Gross profit ratio equals gross profit divided by sales. Gross profit ratio equals gross profit divided by sales. A decline in this ratio is usually cause for concern since it indicates that the company has less ability to mark up the cost of its products into selling prices. A decline in this ratio is usually cause for concern since it indicates that the company has less ability to mark up the cost of its products into selling prices.

40

Cisco’s Gross Profit Margin

41

Possible Causes for a Decline in Gross Profit Ratio Some possible reasons for a decline in Gross Profit Ratio follow: Some possible reasons for a decline in Gross Profit Ratio follow: Product line is stale Product line is stale. New competitors enter the market New competitors enter the market. General decline in economic activity General decline in economic activity. Inventory is overstocked Inventory is overstocked. Manufacturing costs have increased Manufacturing costs have increased. Changes in product mix Changes in product mix.

42

Inventory Turnover Rates for Selected Companies

43

Average Inventory Days for Selected Industries

44

3M Avg. Inv. Days Outstanding Inventories Cost of Goods Sold Avg. Inv. Days Outstanding 20072,60111,71381.05 20082,85212,73581.74

45

Newell Rubermaid’s LIFO Liquidation Footnote

46

Long-Term Assets Long-term assets mainly consist of property, plant, and equipment (PPE). Long-term assets mainly consist of property, plant, and equipment (PPE). These assets often makeup the largest asset amounts. These assets often makeup the largest asset amounts. Future expenses arising from these long- term assets often makeup the larger expense amounts—typically reflected in depreciation expense and asset write-downs. Future expenses arising from these long- term assets often makeup the larger expense amounts—typically reflected in depreciation expense and asset write-downs.

. These assets often makeup the largest asset amounts. These assets often makeup the largest asset amounts. Future expenses arising from these long- term assets often makeup the larger expense amounts—typically reflected in depreciation expense and asset write-downs. Future expenses arising from these long- term assets often makeup the larger expense amounts—typically reflected in depreciation expense and asset write-downs..")

47

Depreciation Factors and Process Depreciation requires the following estimates: 1. Useful life – period of time over which the asset is expected to generate cash inflows 2. Salvage value – Expected disposal amount for the asset at the end of its useful life 3. Depreciation rate – an estimate of how the asset will be used up over its useful life.

48

Variance in Depreciation A company can depreciate different assets using different depreciation rates (and different useful lives). A company can depreciate different assets using different depreciation rates (and different useful lives). The using up of an asset generally relates to physical or technological obsolescence. The using up of an asset generally relates to physical or technological obsolescence.

. The using up of an asset generally relates to physical or technological obsolescence. The using up of an asset generally relates to physical or technological obsolescence..")

49

Depreciation Methods All depreciation methods have the following general formula: All depreciation methods have the following general formula: Depreciation Methods: Depreciation Methods: 1. Straight-line method 2. Accelerated Methods (Double-declining- balance method)

.")

50

Straight-line Method Straight-line method: Under the straight-line (SL) method, depreciation expense is recognized evenly over the estimated useful life of the asset. Straight-line method: Under the straight-line (SL) method, depreciation expense is recognized evenly over the estimated useful life of the asset. Consider the following example: Consider the following example: An asset (machine) with the following details: (1) cost of $100,000 (2) salvage value of $10,000 (3) useful life of 5 years

method, depreciation expense is recognized evenly over the estimated useful life of the asset. Consider the following example: Consider the following example: An asset (machine) with the following details: (1) cost of $100,000 (2) salvage value of $10,000 (3) useful life of 5 years.")

51

Straight-line Depreciation Example For the straight-line method, we use our illustrative asset to assign the following amounts to the depreciation formula: For the straight-line method, we use our illustrative asset to assign the following amounts to the depreciation formula:

52

SL Example For the asset’s first year of usage, $18,000 ($90,000 * 20%) of depreciation expense is reported in the income statement. At the end of that first year the asset is reported on the balance sheet as follows: For the asset’s first year of usage, $18,000 ($90,000 * 20%) of depreciation expense is reported in the income statement. At the end of that first year the asset is reported on the balance sheet as follows: Net book value (NBV) is cost less accumulated depreciation. Net book value (NBV) is cost less accumulated depreciation. At the end of year 2, the net book value will be reduced by another $18,000 to $64,000. At the end of year 2, the net book value will be reduced by another $18,000 to $64,000.

of depreciation expense is reported in the income statement. At the end of that first year the asset is reported on the balance sheet as follows: Net book value (NBV) is cost less accumulated depreciation. Net book value (NBV) is cost less accumulated depreciation. At the end of year 2, the net book value will be reduced by another $18,000 to $64,000. At the end of year 2, the net book value will be reduced by another $18,000 to $64,000..")

53

Double-declining-balance method Double-declining-balance method. For the double- declining-balance (DDB) method, we use our illustrative asset to assign the following amounts to the depreciation formula: Double-declining-balance method. For the double- declining-balance (DDB) method, we use our illustrative asset to assign the following amounts to the depreciation formula:

method, we use our illustrative asset to assign the following amounts to the depreciation formula: Double-declining-balance method. For the double- declining-balance (DDB) method, we use our illustrative asset to assign the following amounts to the depreciation formula:.")

54

Double-declining-balance method The asset is reported on the balance sheet as follows: The asset is reported on the balance sheet as follows: In the second year, $24,000 ($60,000 40%) of depreciation expense is recorded in the income statement and the NBV of the asset on the balance sheet follows: In the second year, $24,000 ($60,000 40%) of depreciation expense is recorded in the income statement and the NBV of the asset on the balance sheet follows:

of depreciation expense is recorded in the income statement and the NBV of the asset on the balance sheet follows: In the second year, $24,000 ($60,000 40%) of depreciation expense is recorded in the income statement and the NBV of the asset on the balance sheet follows:")

55

DDB Depreciation Schedule

56

Comparison of Depreciation Methods INSIGHT: All depreciation methods leave the same salvage value. Total depreciation over asset life is identical for all methods.

57

Asset Sales International Paper Co.’s sale of land: International Paper sold land, carried on its balance sheet at $1.7 billion (computed as $6.1 billion sale less $4.4 billion gain), for $6.1 billion, and realized a gain on the sale of $4.4 billion.

, for $6.1 billion, and realized a gain on the sale of $4.4 billion.")

58

Asset Impairments Impairment of plant assets other than goodwill is determined by comparing the sum of the expected future (undiscounted) cash flows generated by the asset with its net book value. Impairment of plant assets other than goodwill is determined by comparing the sum of the expected future (undiscounted) cash flows generated by the asset with its net book value. Companies must recognize a loss if the asset is deemed to be impaired. Companies must recognize a loss if the asset is deemed to be impaired.

cash flows generated by the asset with its net book value. Companies must recognize a loss if the asset is deemed to be impaired. Companies must recognize a loss if the asset is deemed to be impaired..")

59

TJX’s Asset Impairment

60

Potential Problems with Asset Write-downs Asset write-downs present two potential problems: Asset write-downs present two potential problems: 1. Insufficient write-down. 2. Writing down more than is necessary.

61

Footnote Disclosures Cisco reports the following PPE asset amounts in its balance sheet:

62

Cisco’s Depreciation Policy Supplemental information:

63

Analysis Implications PPE Turnover: analysis of the productivity of long-term assets. PPE Turnover: analysis of the productivity of long-term assets.

64

PPE Turnover for Selected Companies

65

PPE Turnover for Selected Industries

66

Analysis of Useful life and Percent Used Up Estimated useful life = Estimated useful life = Percent used up = Percent used up =

Similar presentations

. 7/11/03.>")

. These assets often makeup.>")