Download presentation

Presentation is loading. Please wait.

1

Destination-based Sales Tax Streamlined Sales and Use Tax Agreement Presented April 22, 2008

2

Recording date of this workshop is April 22, 2008. Some of the rules and procedures discussed in this workshop are subject to change. Please check university resources before relying exclusively on this recorded presentation. Recording date of this workshop is April 22, 2008. Some of the rules and procedures discussed in this workshop are subject to change. Please check university resources before relying exclusively on this recorded presentation.

3

Background Catalog and Internet sales Growth in untaxed sales has increased 25% annually Washington relies on sales tax to fund essential public services Many Washington businesses are losing sales: $10 billion per year

4

Background Destination-based sales tax is also an effort to remove the competitive disadvantage Washington businesses face. It is a change in the way sales tax is collected.

5

Background The national Streamlined Sales and Use Tax Agreement

6

Current law: Retail sales tax is collected at the rate for the location (store or warehouse) from which the goods are shipped. New law: Effective July 1, 2008, retailers must collect sales tax using the rate for the location where the customer receives the merchandise. What will change

7

Example 1: Destination-based sales tax

8

Example 2: Destination-based sales tax

9

City business license is not required because of deliveries by common carrier (Substitute House Bill 3126) 2008 legislation

2008 legislation")

10

There is no change: When the customer receives the goods at the seller’s location When a seller delivers goods to the customer at a location outside the state When the sale is a wholesale sale For sales of most services What doesn’t change

11

Motor vehicles Trailers Semi trailers Aircraft Watercraft Manufactured, modular and mobile homes Towing services Florists (more than 51% of sales must be flowers) What doesn’t change

What doesn’t change")

12

Up to $1,000 in tax credits Software, hardware, IT services, or anything needed to implement change Can claim starting July 2008 or Two years of service from a Certified Service Provider Small business assistance

13

To qualify, you must have: Less than $500,000 in Washington sales annually 5% of taxable sales income from deliveries At least 1% of taxable sales income from deliveries outside the jurisdiction where most sales tax is collected Small business assistance

15

Tax rate lookup, including handheld access City and county tax rates Customer database conversion service Excel worksheet Downloadable files Tools

16

dor.wa.gov

17

destinationtax.dor.wa.gov

18

Address lookup with calculator 6500 Linderson Way SW Tumwater 98501 $100.00

19

Address/calculator results

20

ZIP+4 lookup with calculator

21

ZIP+4/calculator results

22

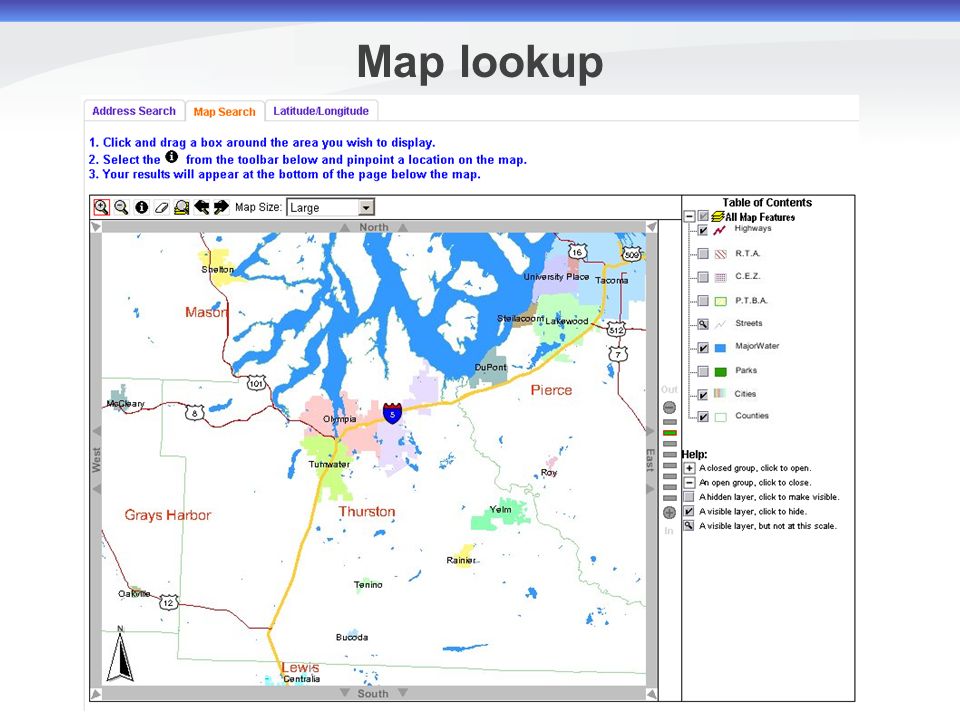

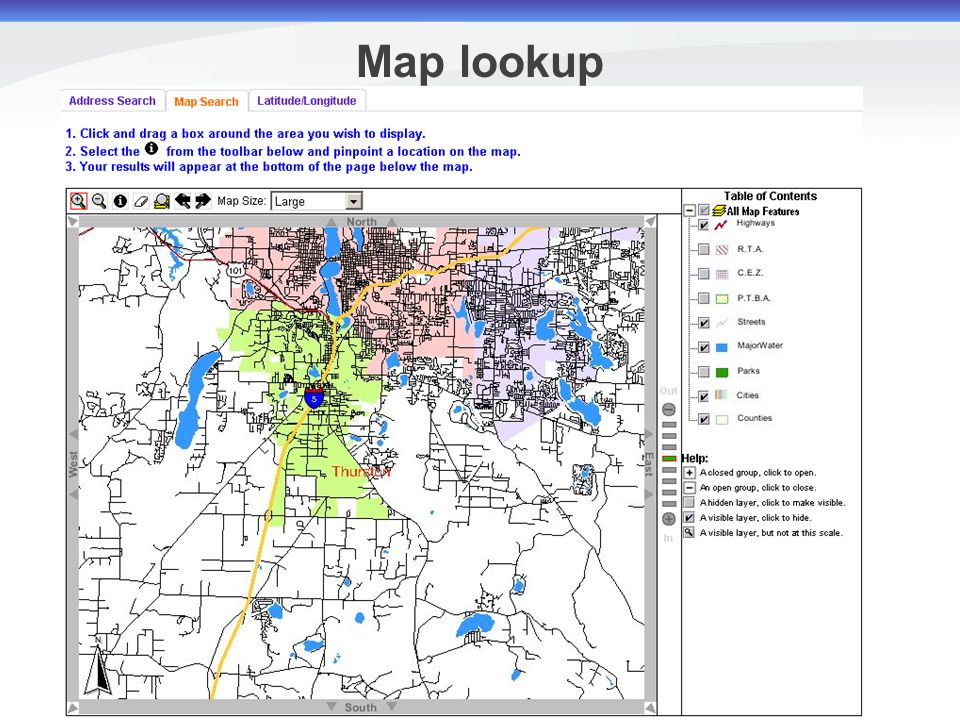

Map lookup

25

Map lookup results

26

Tax lookup by latitude/longitude

27

Latitude/longitude results

28

By address or latitude/longitude taxrates.dor.wa.gov Lookup on handheld devices

29

Lookup results

30

City/county tax rates

31

Tax rates listed alphabetically

32

City/county tax rates

33

Tax rates listed by county

34

City/county tax rates

35

Tax rates in Excel format

36

City/county tax rates

37

Tax rates in QuickBooks format

38

Customer database conversion service

40

Submit customer database

41

Customer database results

42

Customer database error file

43

Excel worksheet

44

Sales ledger tab

45

Summary tab

46

Local tax reporting tab

47

Location codes and rates tab

48

Deductions tab

49

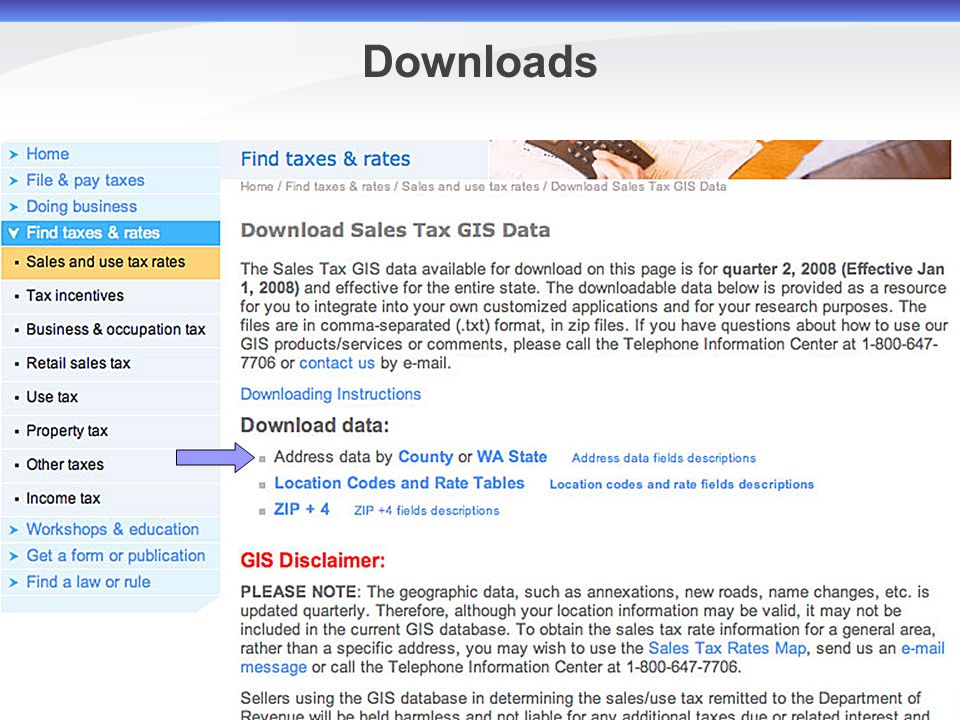

Downloads

51

State address data

52

Downloads

53

Address database download fields

54

Downloads

55

Location code and rate table

56

ZIP+4 downloads

58

Coming soon County maps – Show location code boundaries and tax rates Available upon request Updated quarterly Other tools

59

Being researched Web service – enables point-of-sale or shopping cart software to interact with the department’s online tax rate lookup tool. Other tools

60

Web: destinationtax.dor.wa.gov Phone: 1-800-647-7706 E-mail: dorcommunications@dor.wa.govdorcommunications@dor.wa.gov You may also request a written ruling or contact us at: Department of Revenue Taxpayer Services PO Box 47476 Olympia, WA 98504-7476 More information

61

WSU employees attending this session via videoconferencing and who wish to have it recorded on their training history must notify HRS within three days of the session date: hrstraining@wsu.edu

Similar presentations

Streamlined Sales Tax Project (SSTP) Overview Society for Information Management (SIM)>")

An Enhancement For iSeries 400 DMAS from Copyright I/O International, 2003, 2004, 2005 Skip Intro.>")

>")

The Process for Reviewing State and Local Sales Tax Information at the Department of Revenue.>")