Download presentation

Presentation is loading. Please wait.

1

Crazy Eddie, Inc. Case 1.6

2

Crazy Eddie Facts High school drop out at age sixteen. Began his career by peddlimg TVsets in his Brooklyn neighborhood. Famous for his “crazy” sales tactics and advertisements. Sometimes he would lock the door until the customer bought an item. His TV and radio ads were memorable as well as annoying. Most distinctive trait was his inability to trust anyone outside his large extended family; evidenced by their appointment as officers of his company. In the early 1980s, sales of electronics exploded. Crazy Eddie had seven distinct product lines by 1987. In 1984, Crazy Eddie went public. It took the underwriting firm more than a year to publicly offer the stock as they found the company’s financial records to be in disarray (extensive related party transactions, interest-free loans to employees, highly speculative investments, and numerous family member executives).

.")

3

Crazy Eddie Facts, cont’d

Once public, Antar strived to convince the world that his firm was financially strong and well managed. His efforts worked as analysts from prominent investment firms wrote glowing reports regarding Crazy Eddie’s management team and the company’s bright prospects for the future. In 1986, Antar resigned as company president after realizing more than $50 M on the sale of Crazy Eddie stock. In his absence, the company’s financial condition worsened rapidly. Shortly after a hostile takeover in November 1987, a physical inventory count revealed a $65 M shortage of inventory that equaled the total profits reported by Crazy Eddie since going public in 1984. What were Antar’s tactics for accounting irregularities? He required subordinates to book false entries (sales and inventory that didn’t exist) and prepare inventory count sheets for items that did not exist. Four different accounting firms audited Crazy Eddie’s financial statements over its turbulent history.

and prepare inventory count sheets for items that did not exist. Four different accounting firms audited Crazy Eddie’s financial statements over its turbulent history.")

4

Crazy Eddie Facts, cont’d

Main Hurdman supposedly “lowballed” to obtain the Crazy Eddie audit. The accounting firm’s objectivity was questioned as it audited the inventory system that it developed itself. Their independence was questioned because many of Crazy Eddie’s accountants were former members of that accounting firm. During court cases, it was revealed that Antar and his associates engaged in a large-scale plan to deceive the auditors (collusion). They destroyed incriminating physical documents to conceal inventory shortages; stopped using the sophisticated, computer based inventory system and returned to the old manual system to make it more difficult to find irregularities; and shipped inventory from store to store just before they were to have inventory counts. When finally caught in May 1994, Antar was sentenced to 12 years in prison and ordered to pay restitution of $121 M to former stockholders and creditors.

. They destroyed incriminating physical documents to conceal inventory shortages; stopped using the sophisticated, computer based inventory system and returned to the old manual system to make it more difficult to find irregularities; and shipped inventory from store to store just before they were to have inventory counts. When finally caught in May 1994, Antar was sentenced to 12 years in prison and ordered to pay restitution of $121 M to former stockholders and creditors.")

5

Financial Analysis and Red Flags

Student 1

14

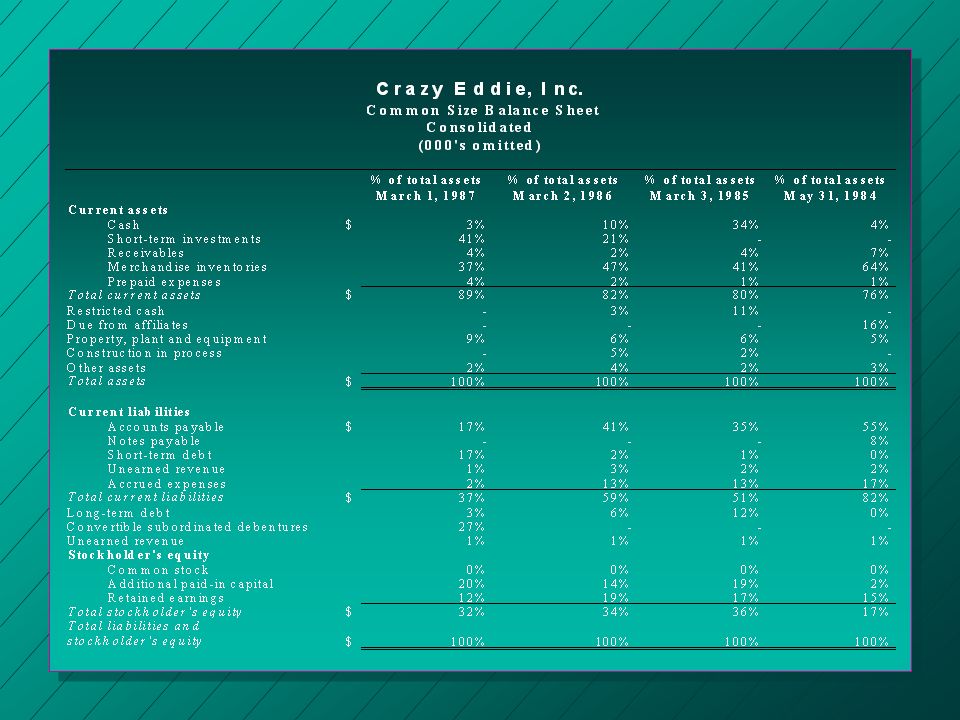

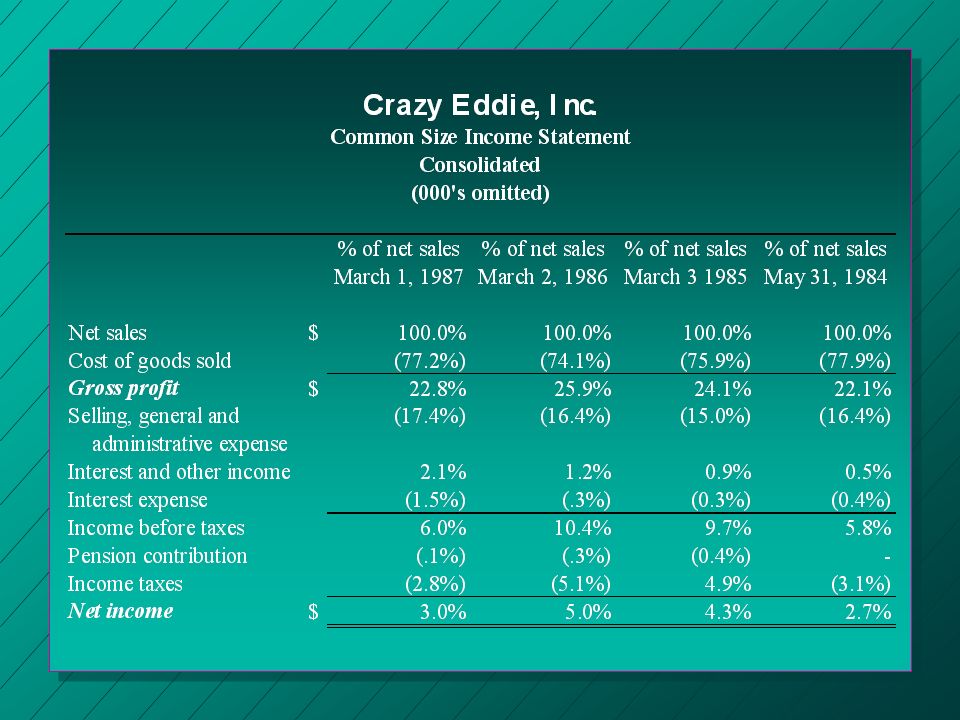

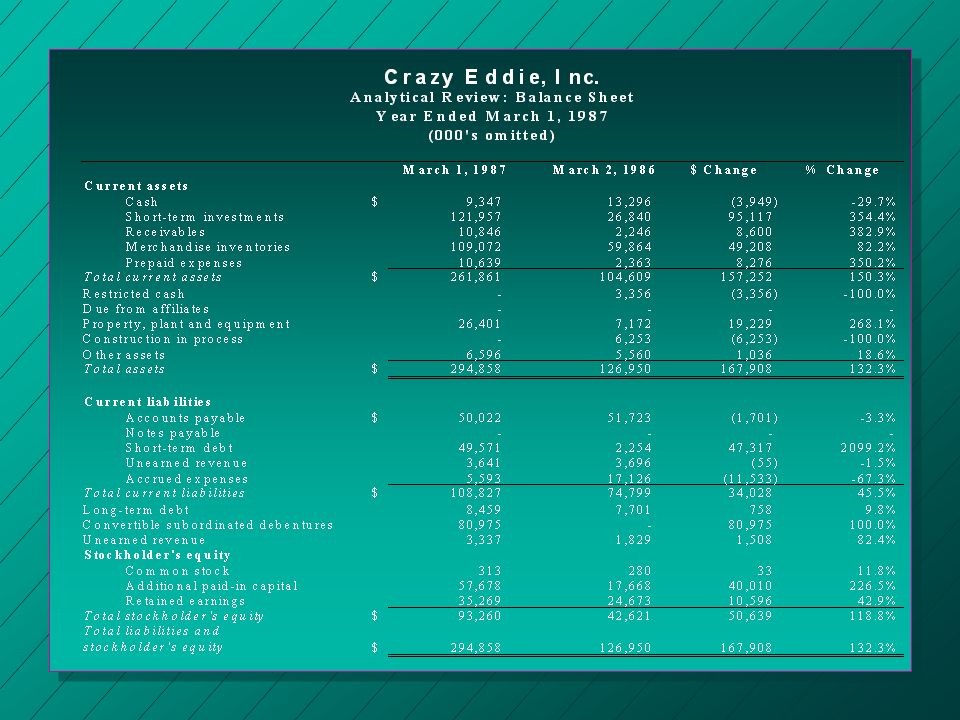

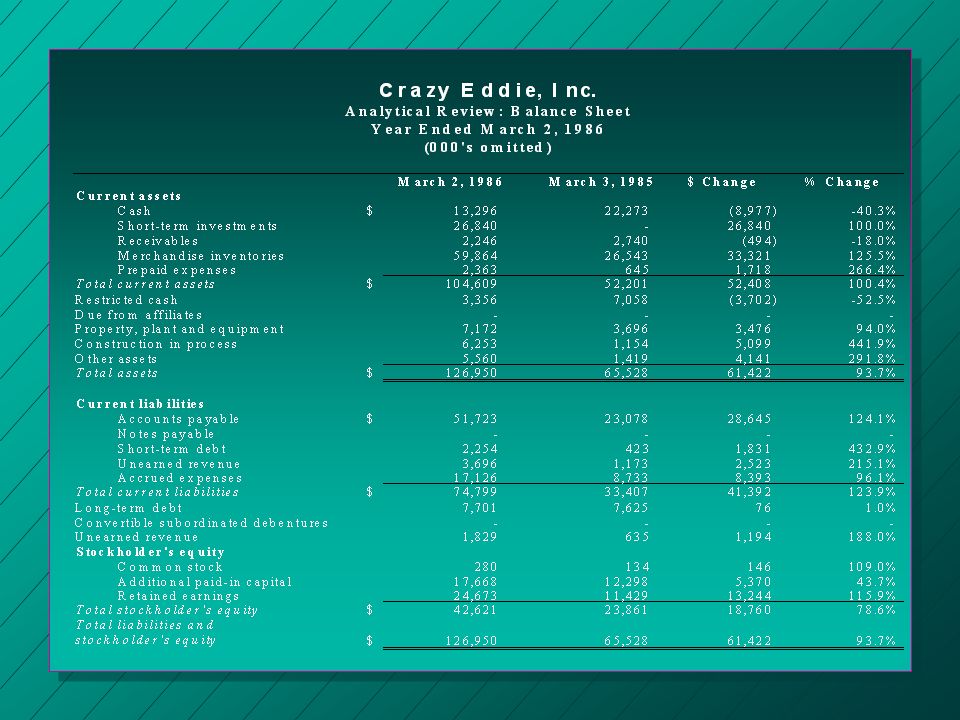

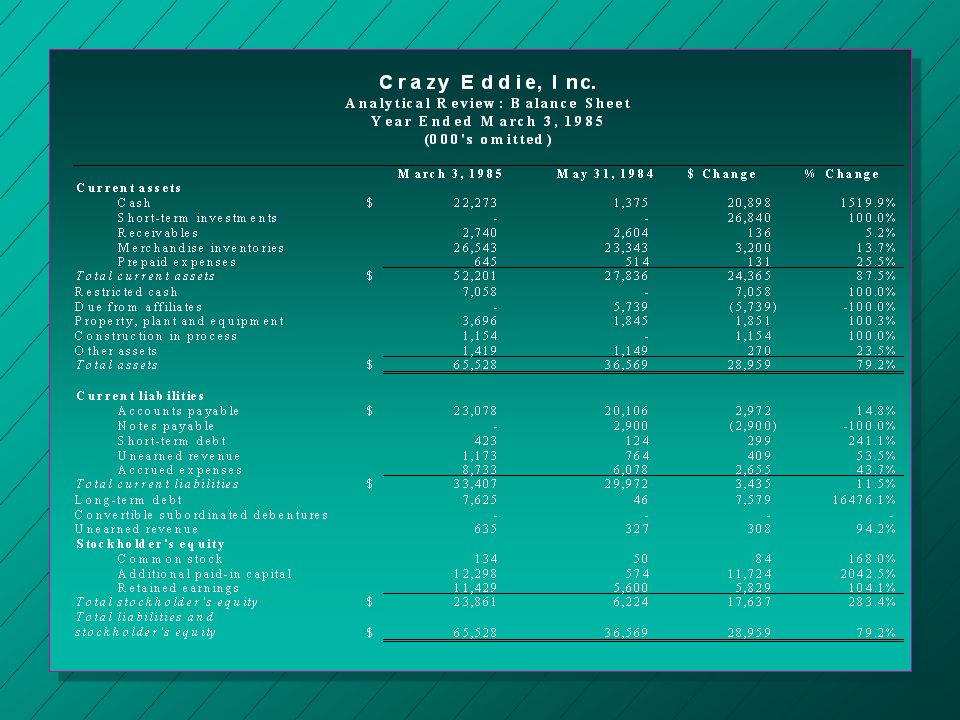

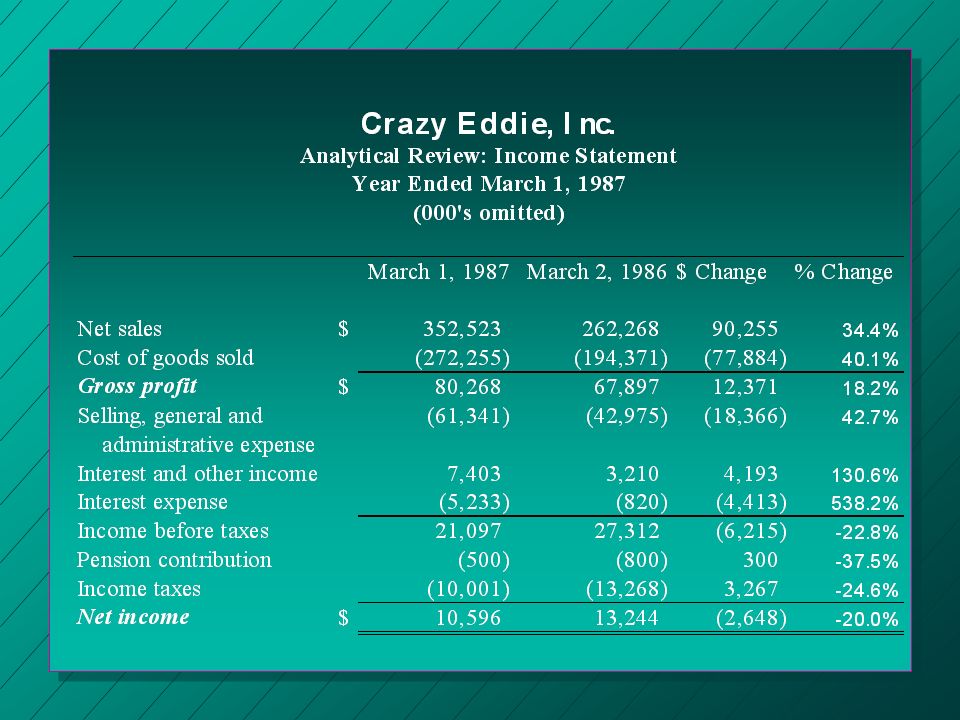

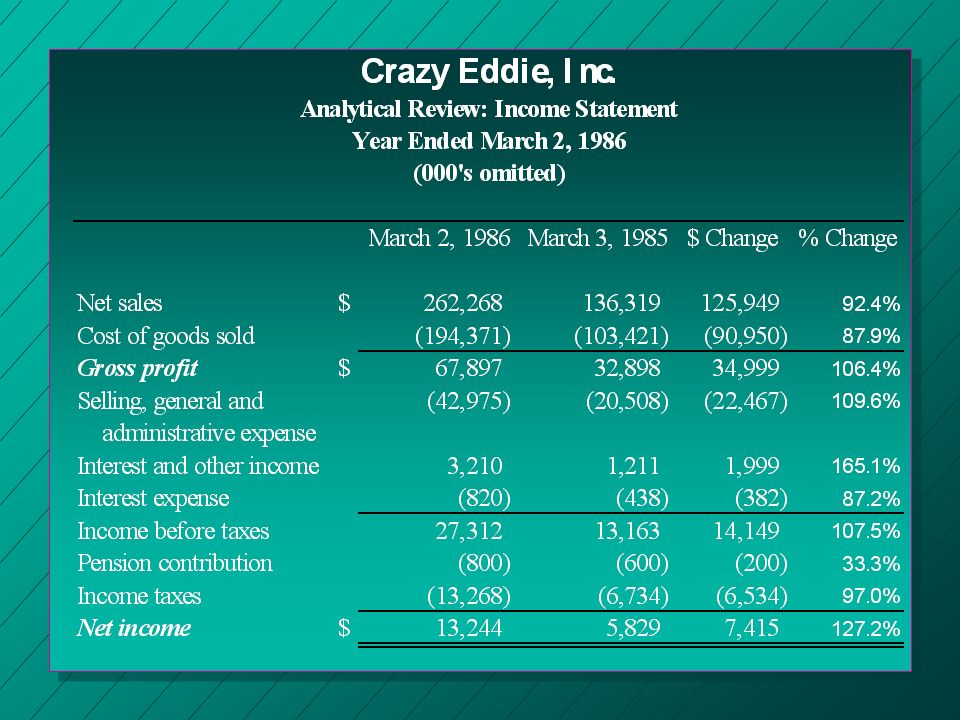

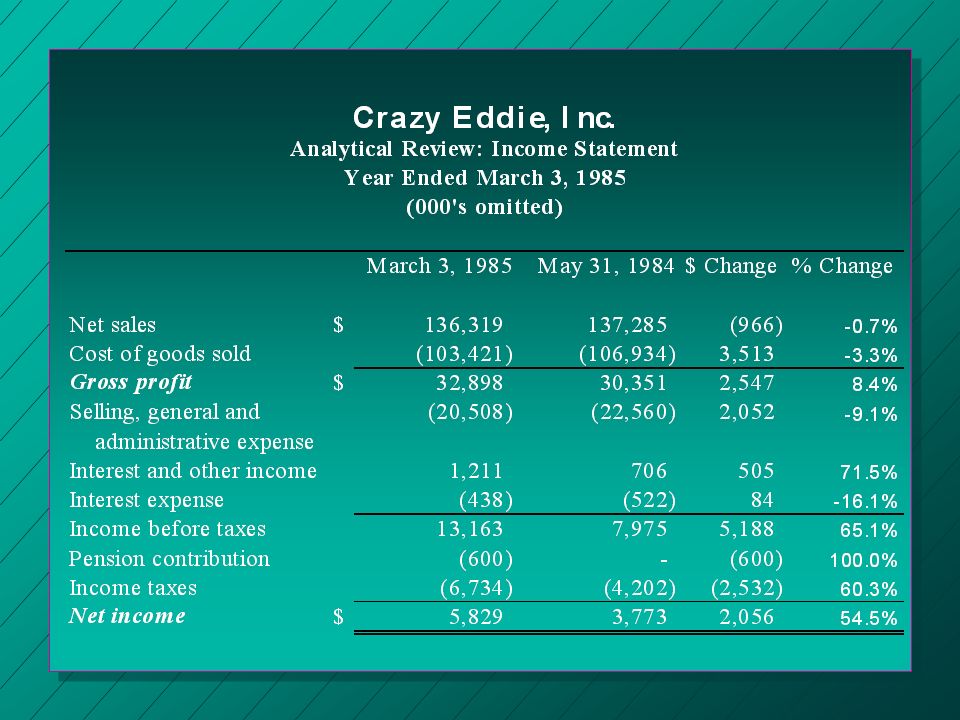

Red Flags: Financial Current Ratio is going up. Inventory represents half of total assets and since inventory is volatile, then that ratio should be questioned further. Inventory Turnover is getting slower. Since sales are going up, you’d assume inventory would be turning over faster. Consider the electronics industry: you would assume that the goods would turnover more often than 4 months (113 days). Accounts Receivable Turnover: every 7 days? Seems odd… Gross margin and Profit margin going down, but sales going up… something is fishy. Sales went from -7% to +92% to +34%. Very volatile.

. Accounts Receivable Turnover: every 7 days Seems odd… Gross margin and Profit margin going down, but sales going up… something is fishy. Sales went from -7% to +92% to +34%. Very volatile.")

15

Red Flags: Nonfinancial

Integrity of Antar: high school dropout; began business by pedalling TVs in his Brooklyn neighborhood Related Parties: large number of the company’s officers were family members Switched auditors four times Crazy Eddie’s accountants were former employees of their auditing firm (Main Hurdman)

")

16

Irregularities Student 2

17

Irregularities Falsification of inventory count sheets

Analytical procedures Inventory turnover ratio [113 days -’87 v. 162 in’86] Age of Inventory [112 days - ‘87 v. 80 in ‘86] Compare actual v. budget Compare client to industry Review nonfinancial and outside information Trace to supporting documentation

18

Irregularities ,cont’d

Physical Inventory (GAAS - AU 331) Appropriate instructions Cut off procedures Trace tags to physical counts Vouch inventory to accounts payable Inquire about consigned goods Note any obsolete inventory Cutoff

Appropriate instructions. Cut off procedures. Trace tags to physical counts. Vouch inventory to accounts payable. Inquire about consigned goods. Note any obsolete inventory. Cutoff.")

19

Irregularities, cont’d

Bogus Debit Memos for Accounts Payable Analytical procedures Scan detail for debit memos Compare with prior years and industry Inquire as to nature Trace to supporting documentation Statistical sampling (SAS 39) Recording of transshipping transactions as retail sales Valuation Compare recorded costs to current vendor costs Review related party transactions Cutoff

Recording of transshipping transactions as retail sales. Valuation. Compare recorded costs to current vendor costs. Review related party transactions. Cutoff.")

20

Irregularities, cont’d

Inclusion of consigned goods in inventory Physical observation Inquire with client personnel Review correspondence Possible confirmation (SAS 67) Evaluate sales and receivable records Vouch purchases to detect unrecognized consigned goods

Evaluate sales and receivable records. Vouch purchases to detect unrecognized consigned goods.")

21

Changing Industry and Lowballing

Student 3

22

Retail Consumer Electronics Industry

During the early 1980s, the electronics industry was undergoing dramatic changes. How do the changes within an industry affect audit planning decisions? The primary concern involves the increased inherent risk of the audit In this particular case, the electronics industry introduces the possibility of inventory obsolescence. The correct response to these demands would be different staffing of the audit team. For instance, the audit team may consist of several seniors and managers rather than the typical team, which includes staff accountants and seniors. In addition, audit planning involves developing an overall strategy for the expected conduct and scope of the audit. (AU 311).

.")

23

Discussion of Audit Planning (cont’d)

Moreover, the audit planning varies with the size and complexity of the entity, experience with the entity, and knowledge of the entity’s business. The auditor should obtain a level of knowledge of the entity’s business that will enable him to plan and perform his audit in accordance with GAAS. That level of knowledge should enable him to obtain an understanding of the events, transactions, and practices that may have a significant effect on the financial statements. The knowledge helps the auditor identify areas that need special consideration; assess conditions under which accounting data are produced, processed, reviewed, and accumulated; evaluate the reasonableness of estimates; and make judgments about the appropriateness of accounting principles.

24

Discussion of Audit Planning (cont’d)

The auditor should also obtain a knowledge of matters that relate to the nature of the entity’s business, its organization, and operating characteristics. These matters include types of business; types of products and services; capital structure; related parties; locations; and production, distribution, and compensation methods Additional consideration should be given to the economic conditions, gov’t regulations and changes in technology. That knowledge is ordinarily obtained through experience with the entity or industry and inquiry of personnel of the entity. Working papers from prior years may provide some additional insight about the entity and its industry. Other sources that the auditor may consult include AICPA accounting and auditing guides, industry publications, F/S of other entities in the industry, textbooks, periodicals, and individuals with knowledge of the industry (specialists).

.")

25

The Importance of Understanding the Clients Industry

In the case of Crazy Eddie, Inc., understanding the clients industry was of utmost importance in detecting errors and misstatements in the financial statements. More specifically, the inventory account should have been examined carefully due to the nature of technology and the potential for obsolete inventory. In addition, a closer look into the transactions of Crazy Eddie, Inc. may have potentially uncovered some of the problems with the inventory account For instance, the practice of buying electronics at wholesale prices and selling them for just below retail to competitors does not seem to be a normal industry practice for a retail electronics dealer. Furthermore, the examination of Crazy Eddie’s distribution methods may have uncovered the stockpiling of inventory scheme that enabled the corporation to overstate the inventory balance by $65 million. Another factor involves the hiring of family members to run the corporation, which was experiencing a period of phenomenal growth.

26

Lowballing and Its Effects on Audits

Lowballing (quasi rents) is a practice utilized by auditors, whereby the auditing firm bids for an audit at a price below its cost. In other words, the firm is charging a fee below the marginal cost of the audit. The primary reason that auditors employ this practice is to ensure that receive and retain a client base. The theory is that the initial loss will be recovered in future years when the audit costs remain constant while audit fees increase.

is a practice utilized by auditors, whereby the auditing firm bids for an audit at a price below its cost. In other words, the firm is charging a fee below the marginal cost of the audit. The primary reason that auditors employ this practice is to ensure that receive and retain a client base. The theory is that the initial loss will be recovered in future years when the audit costs remain constant while audit fees increase.")

27

The Effect of Lowballing on Independent Audit Services

Critics of the auditing profession often allege that the practice of lowballing creates a potential incentive to auditors to reduce the quality of the audit. This contention states that auditors will make concessions (about accounting treatment) to their clients in order to retain the client in future engagements. As a result, many studies have been conducted on this relatively new issue. However, no definitive answer has been reached about this contention.

to their clients in order to retain the client in future engagements. As a result, many studies have been conducted on this relatively new issue. However, no definitive answer has been reached about this contention.")

28

Audit Sampling and Independence

Student 4

29

Audit Sampling Question #5 You test the year-end inventory cutoff procedures, and 10 out of 30 invoices are missing. What course of action would be appropriate? Find this to be material, since 10 missing invoices constitutes one third of the sample Ask questions to the individuals involved with the transactions Trace receiveing report to related purchase voucher Get in touch with the customers involved with the transactions for independent verification Report to the senior manager your findings AU Section 331- “Inventories”

30

Independence Question # 6 What are the pros and cons of hiring individuals who have formerly served as a company’s independent auditor? Cons Independence becomes questionable Ability to objectively audit the company becomes questionable Critics say “A company that hires one of its former auditor can more easily conceal fraudulent activities during the course of audits” AU Section 220 Independence ET Section 102 Integrity and Objectivity

31

Independence, cont’d Pros

Big accounting firms encourage their personnel to work for clients in the apparent belief that it helps cement the accountant-client relationship The former independent auditor would have a greater understanding and greater knowledge of the business and how it functions AU Section 8310 Knowledge of the Business

32

Related Academic Research

33

Additional comments/Information

34

Questions?

Similar presentations