Download presentation

Presentation is loading. Please wait.

1

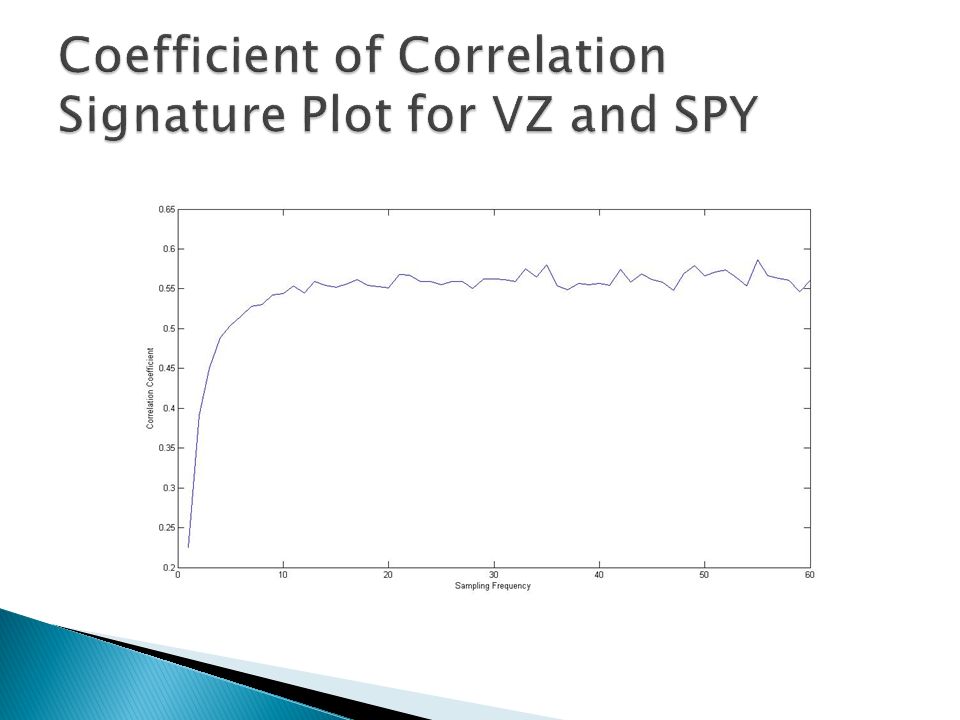

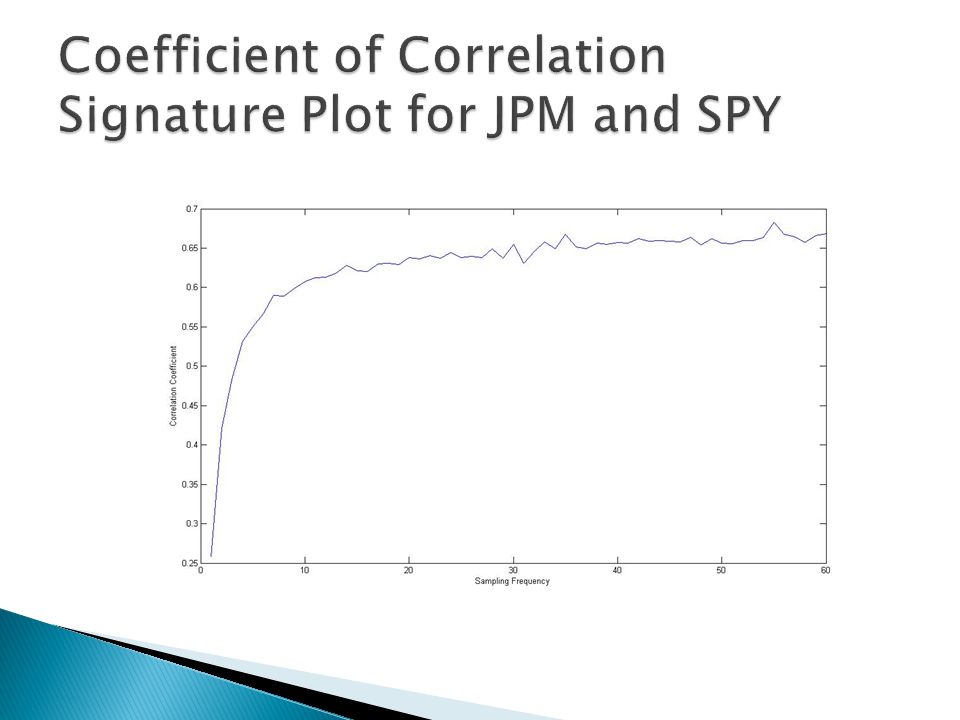

Correlation and Market Returns Mingwei Lei

2

It is often said that correlations between stocks increases when the market is tanking My goal is to empirically find a negative correlation between market returns and coefficient of correlation of various stocks and indices returns This presentation will focus on the relationship between market returns and coefficient of correlation between stocks and market returns

3

Write a program that match up data of stocks and indices Find optimal sampling frequency to calculate returns Partition data into periods to be analyzed Calculate market returns and coefficient of correlation between stock and market returns for each partitioned period Plot coefficient of correlation against market returns to find a relationship

5

11 min return sampling frequency 10 day in each partitioned period

6

11 min return sampling frequency 20 day in each partitioned period

7

11 min return sampling frequency 30 day in each partitioned period

9

11 min return sampling frequency 10 day in each partitioned period

10

11 min return sampling frequency 20 day in each partitioned period

11

11 min return sampling frequency 30 day in each partitioned period

12

11 min return sampling frequency 250 day in each partitioned period

13

11 min return sampling frequency 250 day in each partitioned period

14

11 min return sampling frequency 100 day in each partitioned period

15

Found a small negative relationship between market returns and correlation of various stock returns and market returns Relationship is more apparent when size of partitioned periods increase Due to the large norm of residuals, I cannot conclude that there is a definitive negative empirical relationship

16

Go back through codes and make sure everything is correct Look at a few more stocks Examine the relationship between market returns and coefcorr of various stocks’ returns with each other

Similar presentations

>")

‘Investment Analysis and Portfolio.>")