Download presentation

Presentation is loading. Please wait.

1

BUDGETS AND BALANCE SHEETS Chapter 4

2

OBJECTIVES Explain the steps involved in creating a budget Describe the steps involved in creating a personal balance sheet Understand the importance of budgeting in your financial plan

3

OBJECTIVE 1 - CREATING A BUDGET Budget – forecast of future cash inflows and outflows Give you a detailed road map to your financial future Steps: 1.Create a personal cash flow statement 2.Turn your cash flow statement into a budget

4

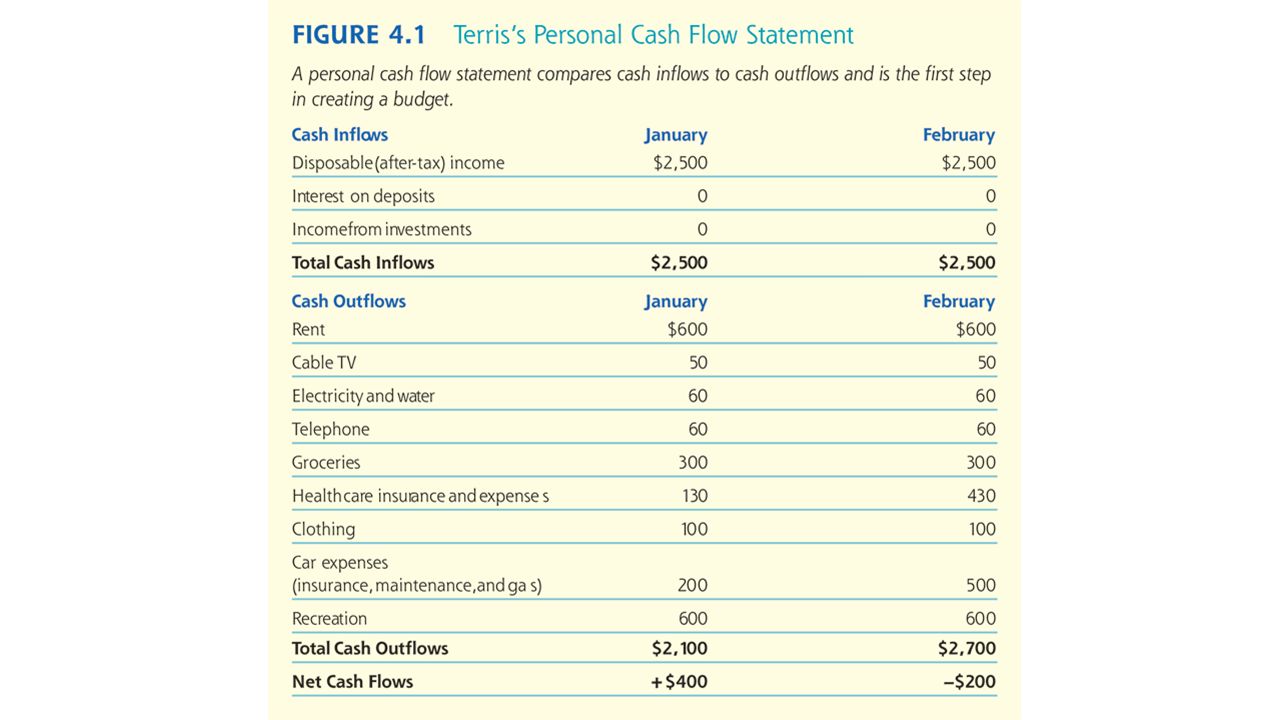

STEP 1 – CREATE A PERSONAL CASH FLOW STATEMENT First step = identify your current cash inflows and outflows Primary cash inflow is their SALARY Cash outflows are anything you spend. Typically impacted by family size, age, and personal spending habits Create a personal cash flow statement record (show inflow and outflow) to show where you money comes from and where it goes

to show where you money comes from and where it goes.")

6

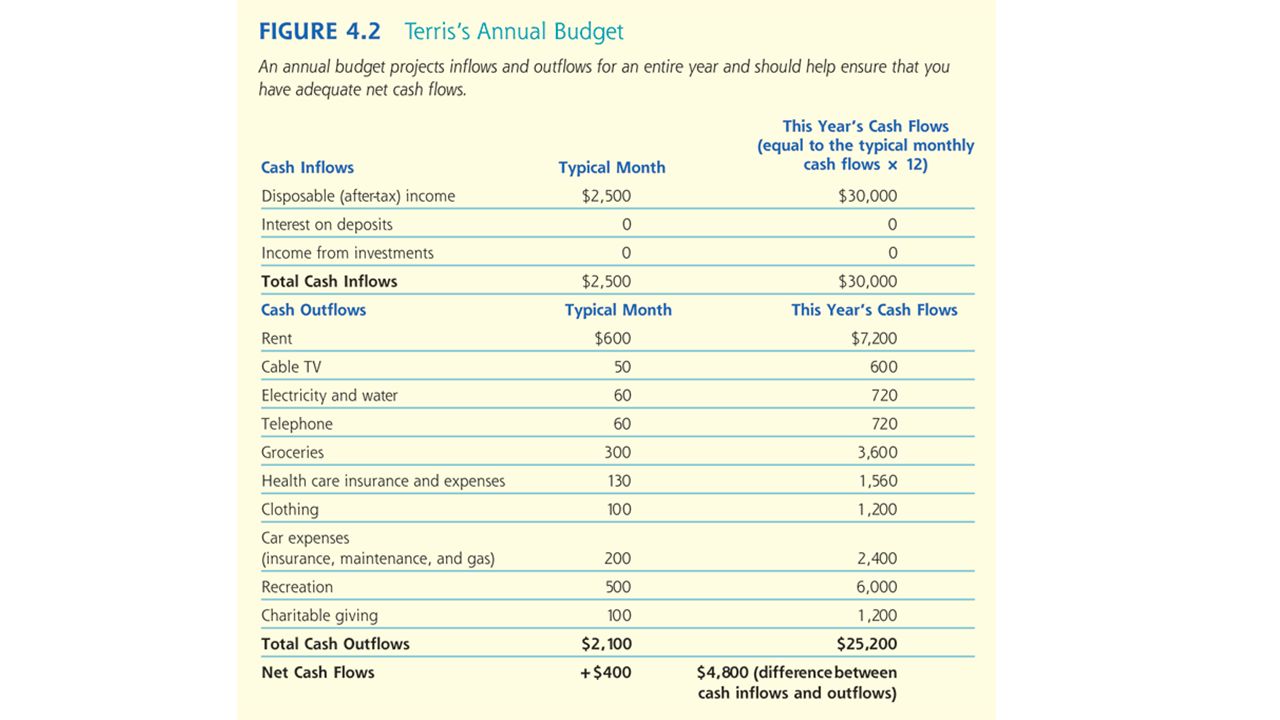

STEP 2: TURN YOUR CASH FLOW STATEMENT INTO A BUDGET Forecast your next cash flows for a period of time into the future Should cover anticipated inflows and outflows for several months to a year or more Consider expected but irregular expenses Activity fees for school functions Money for spring break Money for a yearly vacation Unexpected expenses Car breaks down Medical emergencies

7

WORKING WITH AND IMPROVING YOUR BUDGET A budget will force you to set aside money to take advantage of unexpected opportunities It will help you save money for major purchases, unexpected expenses, and unexpected opportunities Helps you anticipate future cash shortfalls

8

ASSESS THE ACCURACY OF THE BUDGET Periodically evaluate your forecasts and compare those with actual cash flows Best way to know exactly how you spend your money is to keep an EXPENSE JOURNAL Write down everything you spend over the course of a week or month You may underestimate your cash outflow You may have been too optimistic with cash inflow The difference between what you forecast to happen and what actually happened is referred to as a forecast error Finding forecast errors creates a more accurate budget and can adjust inflow and outflow

10

OBJECTIVE 2 - CREATING A PERSONAL BALANCE SHEET

11

PERSONAL BALANCE SHEET A budget tracks cash flows over time, personal balance sheet tells you your financial position at a point in time A summary of all assets (what’s owned), liabilities (what’s owed), and net worth What you use to keep track of your overall wealth (net worth) Knowing where you stand helps you decide how to manage your liquidity, credit, investments, etc.

, liabilities (what’s owed), and net worth What you use to keep track of your overall wealth (net worth) Knowing where you stand helps you decide how to manage your liquidity, credit, investments, etc.")

12

ASSETS Items of value a person owns 1.Liquid assets – QUICK AVAILABILITY = defining characteristic Cash, checking/savings 2.Household assets – owned by a household Cars, houses, furniture Market Value = what something would be worth if you sold it today When creating a balance sheet, you need to evaluate the true market value of your household assets You could use Kelley Blue Book to find the value of your car

13

ASSETS CONTINUED 3.Investments – something you acquire with the ultimate goal of making money Bonds: IOUs, a certificate that promises to repay a certain amount of money at some future time ($1,000 in 10 years plus interest) Some risk because some issuers aren’t always able to pay interest or return the original investment Stocks: certificates that represent fractional ownership of a firm, people buy stocks with the expectation that the company will do well and the value of stock will increase – risk involved Mutual Funds: professional managed investment – allows a larger variety of financial assets (stocks and bonds from many companies) Minimum investment of $500 - $3,000 required - risk is spread so has most protection – 529 College Savings Plan Real Estate: homes, rental property, farms, land

Some risk because some issuers aren’t always able to pay interest or return the original investment Stocks: certificates that represent fractional ownership of a firm, people buy stocks with the expectation that the company will do well and the value of stock will increase – risk involved Mutual Funds: professional managed investment – allows a larger variety of financial assets (stocks and bonds from many companies) Minimum investment of $500 - $3,000 required - risk is spread so has most protection – 529 College Savings Plan Real Estate: homes, rental property, farms, land")

14

LIABILITIES Current and long-term liabilities represent a person’s total debt Current liabilities – debts that must be paid off within one year - most common are credit card balances (you pay a minimum balance every month, when you pay that eliminates current liability) Long-term liabilities – debts that take longer than a year to pay off – student loans, car loans, mortgages Each payment contains interest and principal (the initial amount you owe in a liability)

Long-term liabilities – debts that take longer than a year to pay off – student loans, car loans, mortgages Each payment contains interest and principal (the initial amount you owe in a liability)")

15

NET WORTH Difference between assets and liabilities Net worth = value of your total assets – sum of your total liabilities Easiest way to measure your wealth

16

ANALYSIS OF YOUR PERSONAL BALANCE SHEET Lenders use a debt-to-asset ratio to determine whether or not you’ve borrowed too much money Terris’s Debt = $5,500 Terri’s Assets = $13,900 5,500/13,900 = 39.5% The lower the better

17

OBJECTIVE 3 – BUDGETING AND YOUR FINANCIAL PLAN The balance sheet is a score card that tells you how much your level of wealth is changing Budgeting forces you to evaluate your current financial condition and helps answer the following questions: How can I improve my net cash flows in the near term? How can I improve my net cash flows in the long term? What decisions should I make about using credit, borrowing, and investing?

Similar presentations