Download presentation

Presentation is loading. Please wait.

1

IDEA 2004 Program Requirements and Funding Eligibility

Office of Special Programs April 13, 2011

2

What do you know?

3

IDEA Entitlement Funding

Section 611(school age) and 619 (preschool) To provide students with disabilities aged 3-21, including students who have been suspended or expelled from school, a free appropriate public education, which includes special education and related services, to meet their unique educational needs and to meet other requirements under the act. FAPE must include special education and related services designed to meet a student’s unique needs and prepare him or her for further education, employment, and independent living.

and 619 (preschool) To provide students with disabilities aged 3-21, including students who have been suspended or expelled from school, a free appropriate public education, which includes special education and related services, to meet their unique educational needs and to meet other requirements under the act. FAPE must include special education and related services designed to meet a student’s unique needs and prepare him or her for further education, employment, and independent living.")

4

PROGRAM OBJECTIVES IDEA 2004 Special Education

Section 611, Part B Section 619, Preschool Students Students 3-5 School Age Preschool CFDA: CFDA: children with disabilities have available to them a free appropriate education (FAPE) protect rights assist agencies, districts with the education of students with disabilities (SWDs) assess and ensure effectiveness of efforts to educate children with disabilities The purposes of the Individuals with Disabilities Education Act are to: Ensure that all children with disabilities have available to them a free appropriate public education which emphasizes special education and related services designed to meet their unique needs; Ensure that the rights of children with disabilities and their parents or guardians are protected; Assist States, localities, educational service agencies and Federal agencies to provide for the education of all children with disabilities; and Assess and ensure the effectiveness of efforts to educational children with disabilities.

protect rights. assist agencies, districts with the education of students with disabilities (SWDs) assess and ensure effectiveness of efforts to educate children with disabilities. The purposes of the Individuals with Disabilities Education Act are to: Ensure that all children with disabilities have available to them a free appropriate public education which emphasizes special education and related services designed to meet their unique needs; Ensure that the rights of children with disabilities and their parents or guardians are protected; Assist States, localities, educational service agencies and Federal agencies to provide for the education of all children with disabilities; and. Assess and ensure the effectiveness of efforts to educational children with disabilities.")

5

LOGISTICS – Flow Through

October – Public School Enrollment Count and Low SES Count completed Previous May – Private School Enrollment Count Requested March/April – Allocations received from OSEP March 31 - Out-of-state DHHR student count completed March/April - State and federal allocations released Instructions for completion of on-line plan and funding amounts for the upcoming year are distributed to LEAs

6

LOGISTICS – Flow Through

April-LEAs complete District Self-Assessment as part of needs assessment for strategic plans/LEA application April/May – LEA Budget Completed include LEA state/local expenditures for MOE May 1 – Online plan rolls over to next fiscal year June 1-- LEA online plans due to OSP for review. June-July - Submitted applications are reviewed & upon approval grants are issued. NOTE: SEA receives federal awards in July and October. LEA may obligate up to 25% of total award prior to October 1.

7

LEA Entitlement - “Flow Through”

Entitlement Amount = Base + Population + Poverty Base Allocation (students with disabilities 1998/1996) Population/Poverty Amount = Entitlement – Base Population Amount = 85% [Entitlement – Base] (allocated to LEAs based on most recent public and private school enrollment – all students ) Poverty Amount =15% [Entitlement – Base] (allocated to LEAs based on most recent count of “low SES” students eligible for free/reduced lunch)

Population/Poverty Amount = Entitlement – Base. Population Amount = 85% [Entitlement – Base] (allocated to LEAs based on most recent public and private school enrollment – all students ) Poverty Amount =15% [Entitlement – Base] (allocated to LEAs based on most recent count of low SES students eligible for free/reduced lunch)")

8

Example Total Entitlement = $61,649,797 Base $22,891, 709 Population 85% [$61,649,797 - $22,891,709 ] = $32, Poverty 15% [$61,649,797 - $22,891,709 ] = $5,813,713

![Example Total Entitlement = $61,649,797. Base $22,891, 709. Population. 85% [$61,649,797 - $22,891,709 ] = $32,](http://slideplayer.com/slide/755690/2/images/8/Example+Total+Entitlement+%3D+%2461%2C649%2C797.+Base+%2422%2C891%2C+709.+Population.+85%25+%5B%2461%2C649%2C797+-+%2422%2C891%2C709+%5D+%3D+%2432%2C.jpg "Poverty. 15% [$61,649,797 - $22,891,709 ] = $5,813,713.")

9

FUNDING ALLOCATIONS

10

USE OF FUNDS Allowable Cost

RTI and Coordinated Early Intervening Services High cost fund Excess Cost Maintenance of Effort Private Schools

11

IDEA Part B and OMB Circular A-87 OSEP Clarifications

Allowable Costs IDEA Part B and OMB Circular A-87

12

U.S. Dept. of Ed Requirements

EDGAR – Education Department General Administrative Regulations Gives authority to OMB circulars General Education Provisions Act - GEPA Office of Management and Budget (OMB) OMB Circular A-133 – Single Audit Compliance Supplement Part 4 OMB Circular A-87

OMB Circular A-133 – Single Audit. Compliance Supplement Part 4. OMB Circular A-87.")

13

Allowable Cost § 300.202 Use of amounts.

Must be expended in accordance with the applicable provisions of this part. Must be used only to pay the excess costs of providing special education and related services to children with disabilities. Must be used to supplement State, local, and other Federal funds and not to supplant those funds.

14

IDEA Permissive Use of Funds

§ (1) Services and aids that also benefit nondisabled children. (2) Coordinated Early intervening services High cost special education/ related services. (b) Administrative case management. Purchase appropriate technology for recordkeeping, data collection, and related case management activities

Services and aids that also benefit. nondisabled children. (2) Coordinated Early intervening services. High cost special education/ related services. (b) Administrative case management. Purchase appropriate technology for recordkeeping, data collection, and related case management activities.")

15

Basic Guidelines of Cost Principles

All costs must be: Necessary Reasonable Allocable

16

Helpful Questions to Ask to Determine if a Cost is Allowable

Is the proposed cost consistent with federal cost principles? Is the proposed cost allowable under the relevant program? Is the proposed cost consistent with an approved program plan and budget? Is the proposed cost consistent with program specific fiscal rules? Is the proposed cost consistent with EDGAR?

17

OMB Circular A-87 Allowable Costs

Establishes principles and standards for determining allowable costs You have to read A-87 in conjunction with the IDEA to understand how it applies To the degree there is any conflict, IDEA requirements take precedence

18

Do I need to spend these funds to meet the purposes and needs of the program?

Costs must be necessary and reasonable for proper and efficient performance Costs are necessary and reasonable if, in nature and amount, they do not exceed that which would be incurred by a prudent person under the circumstances prevailing at the time the decision was made to incur the cost

19

Basic Guidelines: Reasonable

Practical aspects of “reasonable” Is the expense targeted to a valid programmatic or administrative consideration? Do I have the capacity to use what I am purchasing? Did I pay a fair rate? Can I prove it? Would I be comfortable defending this purchase?

20

Basic Guidelines: Allocable

Practical aspects of “allocable” Can I prove the program benefited? Can I prove other programs are not benefiting? Ensuring only authorized use Incidental benefit

21

Basic Guidelines: Allocable

Can only charge in proportion to the value received by the program Example: LEA purchases a computer to use 50% in federal program and 50% in a state program Can only charge half of the cost to the federal program

22

OMB Circular A-87 Allowable Costs

Appendix B of A-87 lists 43 selected items of cost – examples Alcoholic beverages are unallowable Conference/meeting costs are allowable if primary purpose is dissemination of technical information (meals, transportation, rental of facilities, speakers’ fees, etc.) but see Appendix B, item 14 regarding Entertainment Costs Costs of professional organizations and subscriptions are allowable Memberships in civic, community or social organizations are allowable with the approval of the Federal awarding agency Costs of membership in organizations whose primary purpose is lobbying are unallowable

but see Appendix B, item 14 regarding Entertainment Costs. Costs of professional organizations and subscriptions are allowable. Memberships in civic, community or social organizations are allowable with the approval of the Federal awarding agency. Costs of membership in organizations whose primary purpose is lobbying are unallowable.")

23

Selected Items of Cost (examples)

Advertising & Public Relations Costs Generally not allowable, except as specified in OMB Circular A-87, Attachment B Entertainment Amusement, field trip or social activities (tickets to shows or sporting events, meals, lodging, etc.) are generally not allowable

are generally not allowable.")

24

Selected Items of Cost (examples)

Salaries and Wages Allowable if proper time distribution records Travel Costs Transportation, lodging, subsistence, and related items, when traveling on business are allowable with certain restrictions Training Training for employee development is allowable; for IDEA, professional development for special education personnel or for general education teachers regarding how to teach students with disabilities

25

NCRTI/OSEP Clarification

IDEA Part B specific examples of use of funds: FAPE Special education teachers and administrators Related services providers Materials and supplies for students with disabilities Professional development for special education personnel or to assist general education personnel in teaching special education students

26

NCRTI/OSEP Clarification

Specialized equipment or devices to assist children with disabilities Two exceptions: Title I/IDEA schoolwide programs Coordinated early intervening services for students without disabilities needing academic or behavioral support to succeed in general education

27

Coordinated Early Intervening Services

Purpose from Congressional Committee Report: …and early intervening services to reduce the need to label children as disabled in order to address the learning and behavioral needs of such children U.S. Department of Education Office of Special Education Programs Building the Legacy 2004

28

CEIS With an approved plan, the LEA may (or in some cases is required to) use up to 15% of IDEA funds for: Professional development Providing educational and behavioral evaluations, services, and supports, including scientifically-based literacy instruction Providing educational and behavioral evaluations, services, and supports including scientifically based literacy instruction U.S. Department of Education Office of Special Education Programs Building the Legacy 2004

29

Core Instruction A Conceptual Framework for RTI

High Need Increasingly Intensive Instructional Interventions Level of need for student to be successful in core instruction Services for Students with IEPs Core Instruction We have reviewed the components of RTI used in this presentation. Now let’s look at a visual representation that illustrates a possible RTI framework and focuses on the services provided to students. This illustration is a triangle. The base of the triangle, which is red, comprises the largest section and is labeled “core instruction.” The top section is blue and is labeled “increasingly intensive instructional interventions.” Within the larger triangle, there is a narrow green triangle that runs from the base of the triangle to the tip and is labeled “Services for Students with IEPs.” The arrow to the right of the triangle illustrates the increasing level of student need and intervention. In this conceptual framework for RTI, the large triangle represents a continuum of services that a student may receive. It is important to note that this framework illustrates the type of instruction and interventions that are provided. One student could receive instruction and interventions in both levels. All students must have access to core instruction, denoted in red at the base of the triangle. As previously noted, core instruction includes whole-group and small-group instruction (such as reading groups). Most students require little more than high-quality core instruction to be academically successful; however, a small number of students will require more supports. As we move up the triangle, two events are occurring: First, the interventions are becoming increasingly intensive. Second, as the interventions become increasingly intensive, there is a corresponding decrease in the number of students who need to be served. In the top of the triangle, denoted in blue, are various interventions that are provided to a subset of students who are identified as needing additional supports in order to meet State academic achievement standards. These interventions may vary in intensity, meaning that they may vary in terms of the teacher-student ratio, length of session, frequency, and duration of the intervention. Children with disabilities may receive services in all areas of the triangle as evidenced by the narrow green triangle. LEP students may also receive services in all areas of the triangle. Low Need Students may receive services in all areas of the pyramid at any one point in time

. Most students require little more than high-quality core instruction to be academically successful; however, a small number of students will require more supports. As we move up the triangle, two events are occurring: First, the interventions are becoming increasingly intensive. Second, as the interventions become increasingly intensive, there is a corresponding decrease in the number of students who need to be served. In the top of the triangle, denoted in blue, are various interventions that are provided to a subset of students who are identified as needing additional supports in order to meet State academic achievement standards. These interventions may vary in intensity, meaning that they may vary in terms of the teacher-student ratio, length of session, frequency, and duration of the intervention. Children with disabilities may receive services in all areas of the triangle as evidenced by the narrow green triangle. LEP students may also receive services in all areas of the triangle. Low Need. Students may receive services in all areas of the pyramid at any one point in time.")

30

RTI and CEIS CEIS (and IDEA) funds may not be used for Tier 1

CEIS (and IDEA) funds may not be used for universal screening CEIS funds may be used for Tier 2 and Tier 3, but special education students should not be included CEIS may be used for RTI training

funds may not be used for universal screening. CEIS funds may be used for Tier 2 and Tier 3, but special education students should not be included. CEIS may be used for RTI training.")

31

CEIS and Supplement Not Supplant

CEIS funds may be used to supplement but not to supplant services provided with funds available under the ESEA (e.g. after school tutoring, school improvement activities) Violations include: Funding services otherwise required by state, federal or local law Funding services paid in prior year, e.g. previously paid by Title I This may be rebutted if the services would not have been funded from other sources if CEIS were not available

Violations include: Funding services otherwise required by state, federal or local law. Funding services paid in prior year, e.g. previously paid by Title I. This may be rebutted if the services would not have been funded from other sources if CEIS were not available.")

32

Progress Monitoring Progress monitoring is a scientifically based practice that is used to assess students’ academic performance and evaluate the effectiveness of instruction and instructional interventions. Generally, Title I, Title III, and CEIS funds may be used to fund progress monitoring (but not universal screening) if the progress monitoring is used to determine the response to an intervention that is supportable with Title I, Title III, or CEIS funds. As defined for this presentation, progress monitoring is the fourth component of RTI and is used to make instructional decisions based on a student’s response to research-based interventions. Progress monitoring is a critical component of RTI because it allows a comparison between a student’s performance and his or her learning goals. Progress is measured by comparing expected and actual rates of learning. Progress monitoring occurs frequently during the course of an intervention to determine if the student is responding to the intervention. Progress monitoring is an allowable use of Title I, Title III and CEIS funds when it is used to determine the response to an intervention that is supportable with these funds.

if the progress monitoring is used to determine the response to an intervention that is supportable with Title I, Title III, or CEIS funds. As defined for this presentation, progress monitoring is the fourth component of RTI and is used to make instructional decisions based on a student’s response to research-based interventions. Progress monitoring is a critical component of RTI because it allows a comparison between a student’s performance and his or her learning goals. Progress is measured by comparing expected and actual rates of learning. Progress monitoring occurs frequently during the course of an intervention to determine if the student is responding to the intervention. Progress monitoring is an allowable use of Title I, Title III and CEIS funds when it is used to determine the response to an intervention that is supportable with these funds.")

33

RTI and IDEA Funding (not CEIS)

A special education teacher fully funded by IDEA (non-CEIS) funds who is providing special education to students with disabilities may include one or more “at-risk” students in this group. E.g. – if a replacement reading program, such as Wilson, is being taught to special education students in a pull-out period, Tier 3 RTI students could participate for a limited period of time, provided this arrangement does not exceed the Policy 2419 per period caseload and does not displace any special education student from IEP services

funds who is providing special education to students with disabilities may include one or more at-risk students in this group. E.g. – if a replacement reading program, such as Wilson, is being taught to special education students in a pull-out period, Tier 3 RTI students could participate for a limited period of time, provided this arrangement does not exceed the Policy 2419 per period caseload and does not displace any special education student from IEP services.")

34

RTI and IDEA Funding (not CEIS)

The special education teacher or related services personnel fully-funded by IDEA cannot be scheduled to provide special education services part of the day and other duties (e.g., interventions for students without disabilities) during another part of the day. IDEA funds may not be used for universal screening (conducted for all students) for RTI

during another part of the day. IDEA funds may not be used for universal screening (conducted for all students) for RTI.")

35

High Cost/High Acuity Funds

36

Division of Instructional & Student Services

High Cost Fund For the purpose of assisting districts in addressing the needs of high need students with disabilities, each State has the option to reserve for each fiscal year 10% of the amount it reserves for State-level activities. Each State must: develop and make available a high cost plan consult with districts develop a funding mechanism and schedule for fund distribution WV includes state high acuity funds in this plan Another option that has been provided to States is the opportunity to use a maximum amount of its discretionary monies to establish a fund to support counties with “high need students”. In accordance with this requirement, States choosing to exercise this option must develop a plan, that includes a definition of a high need student based upon input from LEAs and develop a funding mechanism and schedule of distribution., WV has developed such a plan, has disseminated it across the state and the memo and corresponding application are on the OSE website Division of Instructional & Student Services

37

High Cost Fund Stakeholder involvement

Definition: Individual application for an eligible SWD who: is 3-21 years of age has a current IEP lives within the LEA requesting funds or receives special education and related services within the LEA cost is equal to or greater than $45,000 per year

38

IDEA 2004 Excess Cost

39

Excess Cost The excess cost requirement prevents an LEA from using funds provided under Part B of the Act to pay for all of the costs directly attributable to the education of a child with a disability, subject to paragraph (b)(1)(ii) of this section. Excess costs are those costs for the education of an elementary school or secondary school student with a disability that are in excess of the average annual per student expenditure in an LEA during the preceding school year for an elementary or secondary student.

(1)(ii) of this section. Excess costs are those costs for the education of an elementary school or secondary school student with a disability that are in excess of the average annual per student expenditure in an LEA during the preceding school year for an elementary or secondary student.")

40

Excess Cost – Elementary vs. Secondary

Section 602(8) of the Act and § require the LEA to compute the minimum average amount separately for children with disabilities in its elementary schools and for children with disabilities in secondary schools. The formula for these calculations are provided in 34 CFR, Appendix A to Part 300. The form and calculations to meet this requirement are in Section VIII of the LEAs on-line strategic plan.

of the Act and § require the LEA to compute the minimum average amount separately for children with disabilities in its elementary schools and for children with disabilities in secondary schools. The formula for these calculations are provided in 34 CFR, Appendix A to Part 300. The form and calculations to meet this requirement are in Section VIII of the LEAs on-line strategic plan.")

41

Excess Cost – Elementary vs. Secondary

Data on the form is primarily self-filling and calculating and is pulled from the LEA’s general ledger information stored in WVEIS. To calculate the amounts required for elementary vs. secondary, as required by law, total expenditures for the provision of special education services are pro-rated and entered in the form from a table that was developed in conjunction with the Office of Technology and the Office of School Finance.

42

Excess Cost – Elementary vs. Secondary

This table was established based upon the following premises: Sums the salary expense of teachers by location within the general ledger. Pre-kindergarten through grade six was defined as elementary Grades seven through 12 were defined as secondary. Using the above definitions to segregate total salary expense, a prorated percentage to total expenses was assigned to each elementary and secondary. The total expense pulled from WVEIS in each of the fund categories was then multiplied by the resulting factor which provides the amounts to be used in each of the calculations for elementary or secondary results. The child counts used in the calculations were divided based on the assumption of ages 3-12 as elementary and as secondary.

43

IDEA 2004 Maintenance of Effort

44

IDEA’s MOE Requirements

SEA – IDEA prohibits a state from reducing state financial support for special education below the amount of that support for the preceding fiscal year. (34 CFR § ) LEAs – IDEA requires that LEAs must budget the same amount of local funding for special education as it expended in the previous fiscal year. (34 CFR § )

LEAs – IDEA requires that LEAs must budget the same amount of local funding for special education as it expended in the previous fiscal year. (34 CFR § )")

45

MOE – Two Comparisons Eligibility Compliance

Determining whether an LEA is “eligible” to receive the IDEA Part B Funds Budget to Actual Expenditure Comparison Estimate based on most recent year reviewed in June 1 submission Reviewed and revised after year is closed Compliance Determine if the LEA met the requirements of IDEA’s maintenance of effort Actual to Actual Expenditure Comparison

46

SO IMPORTANT TO UNDERSTAND

This is the eligibility test based on expenditures pulled from the WVEIS financial management system from the most recent year compared to the LEA-provided budget amount. COMPLIANCE is met through actual to actual expenditure comparison. If compliance is not met, the LEA must pay back the difference in non-federal funds. REPAYMENT

47

Part B LEA MOE Requirement: Supplement/Not Supplant

Funds under Part B must be used to supplement State, local and other Federal funds and not to supplant them See 34 CFR § (a)(3) If an LEA maintains its fiscal effort, it will only be using Part B funds to supplement local, or State and local, funds, and not to supplant them IDEA does not require a “particular cost” test – This is contrary to Title I and confusing to many WV LEAs 47 47

(3) If an LEA maintains its fiscal effort, it will only be using Part B funds to supplement local, or State and local, funds, and not to supplant them IDEA does not require a particular cost test – This is contrary to Title I and confusing to many WV LEAs")

48

Four Tests to Meet MOE An LEA needs to only meet ONE of the following comparison tests: Local & State expenditures in total for SWD Local Only expenditures for SWD The per student capita amount of Local & State expenditures for SWD The per student capita amount of Local Only expenditures for SWD LEAs can meet this eligibility requirement by passing one of four tests of funding. Test #1 is a comparison of State and Local actual expenditures from last year compared to what is budgeted for state and local expenditures this year. Test #2 is a comparison of the amount that was transferred from Fund 10 to Fund 27 last year compared to what is budgeted as a transfer this year. Test #3 is a comparison of state and local costs broken out per pupil, based on last year’s Child Count, compared to that same test using this year’s budgeted amounts. Test #4 is a comparison of the Fund 10 transfer costs broken out per pupil, based on last year’s Child Count, compared to that same test using this year’s budgeted amounts. The LEA only needs to meet one of the four tests to have made eligibility. The LEA could fail tests 1, 3, or 4, but if the LEA meets test 2, then MOE eligibility and eventually compliance, have been met.

49

Medicaid and MOE § (g)(2) Methods of ensuring services If a public agency spends reimbursements from Federal funds (e.g., Medicaid) for services under this part, those funds will not be considered ‘‘State or local’’ funds for purposes of the maintenance of effort provisions Medicaid revenues and expenditures must be specifically coded in WVEIS accounting

(2) Methods of ensuring services If a public agency spends reimbursements from Federal funds (e.g., Medicaid) for services under this part, those funds will not be considered ‘‘State or local’’ funds for purposes of the maintenance of effort provisions Medicaid revenues and expenditures must be specifically coded in WVEIS accounting")

50

Other Post Employment Benefits – OPEB

Beginning with FY10, LEAs are required to account for future post employment benefits for employees Expenditures are recorded; should be attributed to 2xxxx as applicable When OPEB expenditures are recorded, they are pulled when WVDE calculates MOE Procedures for recording expenditures must be consistent year to year to avoid complications with MOE calculation

51

IDEA 2004 Private Schools

52

Private Schools The LEA is responsible for child find and services to children with disabilities enrolled by their parents in private schools within the school district Amount to be expended by the LEA for the provision of those services shall be equal to a proportionate amount of Federal funds made available under this part. In calculating the proportionate amount, the LEA shall consult with the private schools and conduct a thorough and complete child find process.

53

Preschools And what about “parentally placed” preschoolers?

Children aged 3-5 are considered to be parentally-placed private school children with disabilities enrolled by their parents in private, including religious, elementary schools, if they are enrolled in a private school that meets the definition of elementary school in 34 CFR §300.13 34 CFR § (a)(2)(ii)

(2)(ii)")

54

Consultation To ensure timely and meaningful consultation, an LEA (or SEA) must consult with private school representatives and representatives of parents of parentally-placed private school children with disabilities during the design and development of special education and related services . . . 34 CFR §

must consult with private school representatives and representatives of parents of parentally-placed private school children with disabilities during the design and development of special education and related services CFR §")

55

Consultation What must the consultation process involve?

Child find process Determining the proportionate share of IDEA funds available Determining the consultation process to be used How, where, and by whom services will be provided Disagreement process for LEA

56

Child Find Requirements

If private schools are located within the district, conduct child find for children in private schools. Records must be maintained on: 1) the number of children evaluated; 2) the number found eligible as part of child find, and 3) the number of children served.

the number of children evaluated; 2) the number found eligible as part of child find, and. 3) the number of children served.")

57

Expenditures Number of eligible children with disabilities $152,500

320 In public schools 300 In private schools + 20 320 $ a student Federal Part B Flow-Through $$ LEA receives x 20 students $152,500 $9, for proportionate share

58

Expenditures/ Proportionate Share

State and local funds may supplement but not supplant federal funds for this population 34 CFR § (d) Cost of child find may not be considered in proportionate share obligation 34 CFR § (d) Amount is calculated within the Five-Year Online Strategic Plan when district enters child count numbers Budget and services are included in plan; funds coded in WVEIS under program/function code 51510

Cost of child find may not be considered in proportionate share obligation. 34 CFR § (d) Amount is calculated within the Five-Year Online Strategic Plan when district enters child count numbers. Budget and services are included in plan; funds coded in WVEIS under program/function code")

59

Use of Carry-Over Funds

If the LEA has not spent all the funds within the initial year of the grant award, it must obligate those funds for special education and related services for students parentally placed in private school during the one-year carry-over period If all requirements are met, and funds remain at the end of the carry-over period, the LEA may request approval to transfer the funds to other allowable expenditures under IDEA

60

Budget Revision Request for Private School Expiring Funds Includes:

A list of private schools within the district; A brief description of the child find process, The district’s count on December 1, 2008 and December 1, 2009 of: 1) private school students evaluated, 2) students found eligible and 3) students receiving services through a Services Plan; Copies of the completed and signed Documentation of Consultation forms for the and Documentation of attempts to consult with private schools that have not signed the affirmation, if any; A brief explanation of reasons why the funds could not be expended; and Budget revision request forms and journal entry

private school students evaluated, 2) students found eligible and 3) students receiving services through a Services Plan; Copies of the completed and signed Documentation of Consultation forms for the and Documentation of attempts to consult with private schools that have not signed the affirmation, if any; A brief explanation of reasons why the funds could not be expended; and. Budget revision request forms and journal entry.")

61

Questions OSP Fiscal Resources Web Page

Sandra McQuain, Ed. D. Office of Special Programs (304) Janice Hay Office of Internal Operations (304) , ext

Janice Hay. Office of Internal Operations. (304) , ext")

62

Significant Disproportionality and CEIS

Special Education Directors’ Meeting September 2010 and April 2011 Dr. Lanai Jennings Coordinator, Office of Special Programs

63

What is Significant Disproportionality

States must annually collect and examine data to determine if Significant Disproportionality is occurring based on race or ethnicity. Authority: Section 618(d) of the IDEA and the implementing regulations in 34 CFR §

of the IDEA and the implementing regulations in 34 CFR §")

64

What is Significant Disproportionality

Data analyses by race/ethnicity must include the following: identification of children as children with disabilities; identification of children as children with a particular disability; placement of children with disabilities in particular educational settings; and the incidence, duration, and type of disciplinary actions, including suspensions and expulsions.

65

What is Significant Disproportionality

Statistical results stand alone A review to determine whether the significant disproportionality is the result of inappropriate identification is not applicable SEA must require any LEA identified as having significant disproportionality in any of the four above-mentioned analysis categories to reserve the maximum amount of funds for comprehensive Coordinated Early Intervening Services (CEIS). 15% of IDEA funds

. 15% of IDEA funds.")

66

Defining “Significant Disproportionality”

States have the authority to define for LEAs State determines criteria for what level of disproportionality is significant

67

How does WV define Significant Disproportionality

Cell size = 20 Relative Risk Ratios (RRR) must be greater than or equal to 3.0 Placement and identification are examined Discipline: type, duration, and incidence Consecutive year provision Revised procedures defined in Director’s Memo issued on 12/11/2009

must be greater than or equal to 3.0. Placement and identification are examined. Discipline: type, duration, and incidence. Consecutive year provision. Revised procedures. defined in. Director’s Memo. issued on 12/11/2009.")

68

Additional OSP Business Rules

No rounding occurs for the resultant RRR. a RRR of does not trigger consequences for the district When fewer than 20 students in a single minority group are identified as having a disability, placement in an LRE, or assigned OSS, ISS, or total removals, the RRR is not required to be calculated However, OSP may choose to do so to report to districts for tracking purposes.

69

Significant Disproportionality is not SPP/APR Indicators 4B, 9, or 10

70

Side-by-Side Comparison

Significant Disproportionality Indicator 4B Relative Risk Ratio calculation is used for ISS, OSS, and total removals and must equal or exceed 3.0 Relative difference calculation addresses long term OSS only Significant disproportionality triggered by just a numerical examination of data More than just an examination of numerical information is necessary. Use monitoring data, review of policies, procedures, and practices etc. to determine if significant discrepancy results from inappropriate identification Two consecutive years of data are considered One year of data is considered 15% set aside is required Fiscal set aside is not required

71

Side-by-Side Comparison

Significant Disproportionality Indicators 9 and 10 Data source and RRR calculation is the same for Indicators 9 and 10 However, RRR Criterion is higher = 3.0 RRR Criterion = 2.0 Includes an additional test of statistical significance criterion Significant disproportionality triggered by just a numerical examination of data More than just an examination of numerical information is necessary Use monitoring data, review of policies, procedures, and practices etc. to determine if significant discrepancy results from inappropriate identification Two consecutive years of data are considered One year of data is considered 15% set aside is required Fiscal set aside is not required Considers only disproportionality of minority categories RRR of 3.0 or higher are not considered for white subgroup White subgroup is included Analysis based on just overidentification All SWDs and six categories are included Analysis includes both over- and under-identification of the

72

Has Significant Disproportionality been identified in your district?

OSP Significant Disproportionality and CEIS Resources

73

What happens when significant disproportionality is identified?

74

For Determinations of Significant Disproportionality

States must: Require LEAs to use 15% of Part B funds for Coordinated Early Intervening Services (CEIS) …particularly, but not exclusively, for children in those groups significantly over identified.

…particularly, but not exclusively, for children in those groups significantly over identified.")

75

For Determinations of Significant Disproportionality

LEA must: Publicly report on the revision of policies, practices, and procedures

76

What are Coordinated Early Intervening Services (CEIS)?

77

CEIS Services provided through IDEA funding for at-risk students who do not receive special education services K-12 only Direct academic or behavioral interventions Professional development

78

Mandatory or Voluntary CEIS

Mandatory Use of CEIS: LEA is identified with Significant Disproportionality by race/ethnicity in LRE, identification or discipline LEA must reserve the maximum amount (i.e., 15% IDEA funds) Funds are used to address the Significant Disproportionality No option to reallocate funds Voluntary Use of CEIS: LEA opts to set aside IDEA funds for the provision of services to students without disabilities (SWODs) LEA may use up to the maximum amount Funds address district determined need LEA may also reallocate any unspent funds while funds are available for obligation

Funds are used to address the Significant Disproportionality. No option to reallocate funds. Voluntary Use of CEIS: LEA opts to set aside IDEA funds for the provision of services to students without disabilities (SWODs) LEA may use up to the maximum amount. Funds address district determined need. LEA may also reallocate any unspent funds while funds are available for obligation.")

79

How does a district set aside CEIS funds?

CEIS funds must be specified in a district’s special education plan and proposed budget. Go to: Compliances/ LEA Special Education / LEA Early Intervening

80

Coordinated Early Intervening Services Narrative

Need for program Entrance criteria Description of services and targeted grades, subjects, etc. Method of monitoring progress Exit criteria How funds will be spent

81

Related Areas on Plan 1) LEA Allocation Screen

CEIS set aside should be updated 2) CEIS portion of budget should reflect services to students without disabilities and be aligned with CEIS narrative 5 digit program function code should begin with 1 3) When applicable, professional development plan and goals / objectives / actions should also align.

CEIS portion of budget should reflect services to students without disabilities and be aligned with CEIS narrative. 5 digit program function code should begin with 1. 3) When applicable, professional development plan and goals / objectives / actions should also align.")

82

Reporting Requirements

CEIS is a new 618 report Two required reporting mechanisms: LEA Application CEIS program description Total number of students who received CEIS during the school year Total number of students who received CEIS in prior school years and who later qualified for special education and/or related services WVEISweb Intervention Screens Identifies students by WVEIS number Specify only students who received CEIS during the prior school year

83

Special Education Plan Report

Required at the time of LEA application submission

84

WVEISweb tracking Required by June 15 each school year after CEIS are provided Click Yes here (Default setting is No)

![]()

85

Why is Significant Disproportionality Important?

Minority students More likely to be assigned to segregated classrooms or placements More likely to be assigned long term suspensions Have limited access to inclusive and general educational environments Experience higher dropout rates and low academic performance Often exposed to substandard and less rigorous curricula May be missclassified or inappropriately labeled

86

Why is Significant Disproportionality Important?

Minority students May receive services that do not meet their needs; and Are less likely than their white counterparts to return to general education classrooms.

87

Why is Significant Disproportionality Important?

Minority students Are more likely to become dropouts or receive a certificate of attendance and/or experience High unemployment rates Lack of preparation for the workforce Difficulty in gaining access to postsecondary education

88

Other factors that may contribute to Significant Disproportionality:

Language Intrinsic deficits Child poverty & associated risk factors Assumptions about intelligence Wait-to-fail model Research to practice gap

89

Federal Program Requirements

Office of Special Programs April 13, 2011

90

AGENDA Federal Grants Management Federal Programs Compliance

OMB Circulars and EDGAR Audits Time and Effort Obligation and Liquidation Inventory Management

91

FEDERAL PROGRAMS COMPLIANCE

Common federal grants management rules apply to all federal education funds GEPA (General Education Provisions Act) EDGAR (Education Department General Administrative Regulations) OMB Circulars (Primarily A-133 and A-87) Specific program (e.g. IDEA) rules apply District and state financial procedures apply Policy 8200-Purchasing Capital Assets Manual (inventory) Chart of Accounts (budget codes) Federal and state monitoring may review compliance with all of the above Special attention paid to procedures used when ARRA funds are involved

EDGAR (Education Department General Administrative Regulations) OMB Circulars (Primarily A-133 and A-87) Specific program (e.g. IDEA) rules apply. District and state financial procedures apply. Policy 8200-Purchasing. Capital Assets Manual (inventory) Chart of Accounts (budget codes) Federal and state monitoring may review compliance with all of the above. Special attention paid to procedures used when ARRA funds are involved.")

92

Education Department General Administrative Regulations (EDGAR)

Contains specific rules governing systems: Financial Management § 80.20 § 74.21 Procurement § 80.36 § Inventory § 80.32 § 74.34 Gives authority to OMB circulars

93

OMB Circular A-133 What is it? Who uses it? Why is it important?

Auditors use it to determine which programs they audit What - Audits of States, Local Governments, and Non-Profit Organizations Who – auditors Why – Stipulates an auditee’s responsibilities and what federal programs are audited. Not all programs are audited.

94

Single Audit Act and A-133 Requires annual audit

Type A programs ($500,000) At-risk Type B programs ($100,000) Completed audit reports to Federal Audit Clearinghouse which distributes to Federal agencies Agencies have 6 months from issue date of report to resolve audit findings

At-risk Type B programs ($100,000) Completed audit reports to Federal Audit Clearinghouse which distributes to Federal agencies. Agencies have 6 months from issue date of report to resolve audit findings.")

95

What do auditors look at?

Depends on the program This is covered in the A-133 compliance supplement Matrix of Compliance Requirements

96

Types of Compliance Requirements

CFDA Types of Compliance Requirements A. Activities Allowed or Unallowed B. Allowable Costs/Cost Principles C. Cash Management D. Davis-Bacon Act E. Eligibility F. Equipment and Real Property Management G. Matching, Level of Effort, Earmarking H. Period of Availability of Federal Funds I. Procurement Suspension Debarment J. Program Income K. Real Property Acquisition/ Relocation Assistance L. Reporting M. Subrecipient Monitoring N. Special Tests And Provisions 66 – Environmental Protection Agency (EPA) 66.458 Y 66.468 81 – Department of Energy (DOE) 81.042 84 – Department of Education (ED) 84.002 84.010 84.011 G L 84.041 84.048 84.126 84.181 84.186 84.282 This is what the auditors use to formulate their audit plan. Their audit plan are the steps they will perform to conduct their audit. They are not program experts so they have to use this supplement in order to conduct audits of federal programs.

Y – Department of Energy (DOE) – Department of Education (ED) G L This is what the auditors use to formulate their audit plan. Their audit plan are the steps they will perform to conduct their audit. They are not program experts so they have to use this supplement in order to conduct audits of federal programs.")

97

OMB A-133 Compliance Requirements

IDEA-Related Requirements Activities Allowed or Unallowed Allowable Costs/Cost Principles Cash Management Davis-Bacon Act (Not Applicable) Eligibility (Not Applicable) Equipment and Real Property Management Matching, Level of Effort, Earmarking Period of Availability of Federal Funds Procurement and Suspension and Debarment Program Income (Not Applicable) Real Property Acquisition/Relocation Assistance (Not Applicable) Reporting Subrecipient Monitoring Special Tests and Provisions Activities Allowed or Unallowed - Most of guidance will come from Circular A-87 and IDEA regulations. Also may be limited by purpose stated on grant agreement (grants issued to district by WVDE for substitutes, professional development, etc.) Allowable Costs/Cost Principles - Includes time and effort record. Cash Management –Cash Management Improvement Act of 1990– will hear referred to as the three-day rule. Provides for the efficient transfer of federal financial assistance between the federal government and the states and establishes procedures to minimize the time elapsing between the transfer of funds from the one entity to another. US Treasury to State – State to District – District to Vendor. Requires remittance of interest earned in excess of $100 per year, and must be remitted on a quarterly basis. Davis-Bacon Act – Deals with prevailing wage rates to laborers and mechanics-generally not applicable to IDEA CFDA’s Eligibility – Specifies the criteria for determining whether subrecipients can participate – generally not applicable to IDEA CFDA’s Equipment and Real Property Management – Must use, manage, and dispose of equipment acquired under a Federal grant in accordance with State laws and procedures and applicable federal regulations. Matching, Level of Effort, Earmarking – includes maintenance of effort, high cost fund, CEIS funds Period of Availability of Federal Funds Procurement and Suspension and Debarment-All purchases with federal funds must follow established policies and procedures which must include any clauses required by governing federal regulations. Further, non-federal entitles are prohibited from contracting with or making subawards to parties that are suspended or debarred. Program Income – not applicable Real Property Acquisition – not applicable Reporting – applies to financial and child count reporting Subrecipient Monitoring – State responsible for monitoring the district’s use of awards through reporting, site visits, regular contact, or other means to provide reasonable assurance that the district administers the award in compliance with laws and regulations. Special Tests/Provisions – Participation of Private School Children, Charter Schools, School wide Programs 97 97

Eligibility (Not Applicable) Equipment and Real Property Management. Matching, Level of Effort, Earmarking. Period of Availability of Federal Funds. Procurement and Suspension and Debarment. Program Income (Not Applicable) Real Property Acquisition/Relocation Assistance (Not Applicable) Reporting. Subrecipient Monitoring. Special Tests and Provisions. Activities Allowed or Unallowed - Most of guidance will come from Circular A-87 and IDEA regulations. Also may be limited by purpose stated on grant agreement (grants issued to district by WVDE for substitutes, professional development, etc.) Allowable Costs/Cost Principles - Includes time and effort record. Cash Management –Cash Management Improvement Act of 1990– will hear referred to as the three-day rule. Provides for the efficient transfer of federal financial assistance between the federal government and the states and establishes procedures to minimize the time elapsing between the transfer of funds from the one entity to another. US Treasury to State – State to District – District to Vendor. Requires remittance of interest earned in excess of $100 per year, and must be remitted on a quarterly basis. Davis-Bacon Act – Deals with prevailing wage rates to laborers and mechanics-generally not applicable to IDEA CFDA’s. Eligibility – Specifies the criteria for determining whether subrecipients can participate – generally not applicable to IDEA CFDA’s. Equipment and Real Property Management – Must use, manage, and dispose of equipment acquired under a Federal grant in accordance with State laws and procedures and applicable federal regulations. Matching, Level of Effort, Earmarking – includes maintenance of effort, high cost fund, CEIS funds. Period of Availability of Federal Funds. Procurement and Suspension and Debarment-All purchases with federal funds must follow established policies and procedures which must include any clauses required by governing federal regulations. Further, non-federal entitles are prohibited from contracting with or making subawards to parties that are suspended or debarred. Program Income – not applicable. Real Property Acquisition – not applicable. Reporting – applies to financial and child count reporting. Subrecipient Monitoring – State responsible for monitoring the district’s use of awards through reporting, site visits, regular contact, or other means to provide reasonable assurance that the district administers the award in compliance with laws and regulations. Special Tests/Provisions – Participation of Private School Children, Charter Schools, School wide Programs")

98

Federal Grants Management and Compliance Considerations

Time and Effort Timely Obligation and Liquidation/Cash Management Inventory Management Budget Transfers

99

TIME AND EFFORT (A Common Audit Finding)

Largest expenditure category in special education budgets : Personnel Audit Standard: Must be able to document amount of time under each grant Policies/procedures to determine percentages of time devoted to individual Federal programs and awards Time and effort certification or personnel activity report (PAR)

")

100

Time and Effort If federal funds are used for salaries “time distribution records” must be kept Must demonstrate that employees paid with federal funds actually worked on the specific federal program Type of documentation depends on the number of “cost objectives” the employee worked on These cost objectives must be connected to the employee’s salary source

101

Time and Effort If an employee works on a single cost objective:

What is a cost objective? A specific grant award, or other category of costs, that requires the grantee to track specific cost information If an employee works on a single cost objective: Semi-Annual Certification Signed by employee and supervisor every six months Example: “I hereby certify that for the period January 1, 2011 through June 30, 2011 one-hundred percent (100%) of my time and effort was spent on IDEA, Part B Administration.”

of my time and effort was spent on IDEA, Part B Administration.")

102

Time and Effort If an employee works on multiple cost objectives then a Personnel Activity Report (PAR) must be maintained: After-the-fact-record Completed at least monthly Must include total activity for which the employee is compensated Signed and dated by employee (supervisor may also sign)

")

103

Time and Effort Quarterly comparisons of actual costs to budgeted distributions If a variance of 10% or greater exists Adjust expenditures to reflect costs of the actual time reported. In order to minimize future differences, adjust estimated distributions for future payrolls to activity performed in the previous quarter. This should help minimize the difference in actual wages paid to time recorded. If difference is less than 10%, may make adjustment annually. Employees salaries and wages may be assigned to federal grants initially based on budgets or other estimated distribution percentages and should produce reasonable approximations of the actual employee time distributions that are subsequently reported. When estimates are used, districts must compare actual costs based on monthly time and effort reported to the estimates used for coding payroll expenditures. This much occur at least quarterly. If the comparison shows that the difference of the time reported and actual payroll expenditures is greater than 10 percent, then the district must do two (2) things. First, the county must adjust the accounting records/expenditures to reflect costs of the actual time reported. Second, in order to minimize future differences, the estimated distributions used to charge payroll for the following quarter must be changed to reflect the reported actual distributions of the previous quarter.

things. First, the county must adjust the accounting records/expenditures to reflect costs of the actual time reported. Second, in order to minimize future differences, the estimated distributions used to charge payroll for the following quarter must be changed to reflect the reported actual distributions of the previous quarter.")

104

OBLIGATION AND LIQUIDATION Definitions

Obligation – EDGAR §76.707 Liquidation-The issuance of payment for an obligation. If the obligation is for-- The obligation is made-- (a) Acquisition of real or personal property On the date on which a binding written commitment to acquire the property. (b) Personal services by an employee When the services are performed. (c) Personal services by a contractor who is not an employee On the date on which a binding written commitment is made to obtain the services. (d) Performance of work other than personal services On the date on which a binding written commitment is made to obtain the work. (e) Public utility services When the services are received. (f) Travel When the travel is taken. (g) Rental of real or personal property When the property is used.

Acquisition of real or personal property. On the date on which a binding written commitment to acquire the property. (b) Personal services by an employee. When the services are performed. (c) Personal services by a contractor who is not an employee. On the date on which a binding written commitment is made to obtain the services. (d) Performance of work other than personal services. On the date on which a binding written commitment is made to obtain the work. (e) Public utility services. When the services are received. (f) Travel. When the travel is taken. (g) Rental of real or personal property. When the property is used.")

105

Obligation and Liquidation

Cash Management Improvement Act LEAs must draw down cash from grant awards to pay expenses only as they are incurred. Interest earned on federal cash draws held in excess of three days require the remission to the SEA of interest earned on that excess. Exhaust FY 11 funding before using FY 12 funding. Check balances of FY 10 funding – Ending obligation date is September 30, 2011 and ending liquidation date is December 31, 2011.

106

Obligation and Liquidation-Timelines

Availability of IDEA Funds FY 10 (IDEA regular and ARRA) Obligation period July 1, 2009 – September 30, 2011 Ending liquidation date December 31, 2011 FY 11 July 1, 2010 – September 30, 2011 December 31, 2012 FY 12 July 1, 2011 – September 30, 2013 December 31, 2013

Obligation period. July 1, 2009 – September 30, Ending liquidation date. December 31, FY 11. July 1, 2010 – September 30, December 31, FY 12. July 1, 2011 – September 30, December 31,")

107

Obligation and Liquidation-Use of Budget Revision Process

When are budget revisions required? What is the process? WVDE forms and GNL 520 (please print entry with object text description) Who do you contact? OSP Budget Revisions Memo – February 2010 (Copy of memo recently ed to the Special Education Director’s ListServ on 2/18/2011). Be sure to monitor budget and expenditures and submit a request for a revision, if required, in order to make changes and have time to obligate funds before end of obligation period. Will distribute memo/policy and discuss later if time allows.

Who do you contact OSP Budget Revisions Memo – February (Copy of memo recently ed to the Special Education Director’s ListServ on 2/18/2011). Be sure to monitor budget and expenditures and submit a request for a revision, if required, in order to make changes and have time to obligate funds before end of obligation period. Will distribute memo/policy and discuss later if time allows.")

108

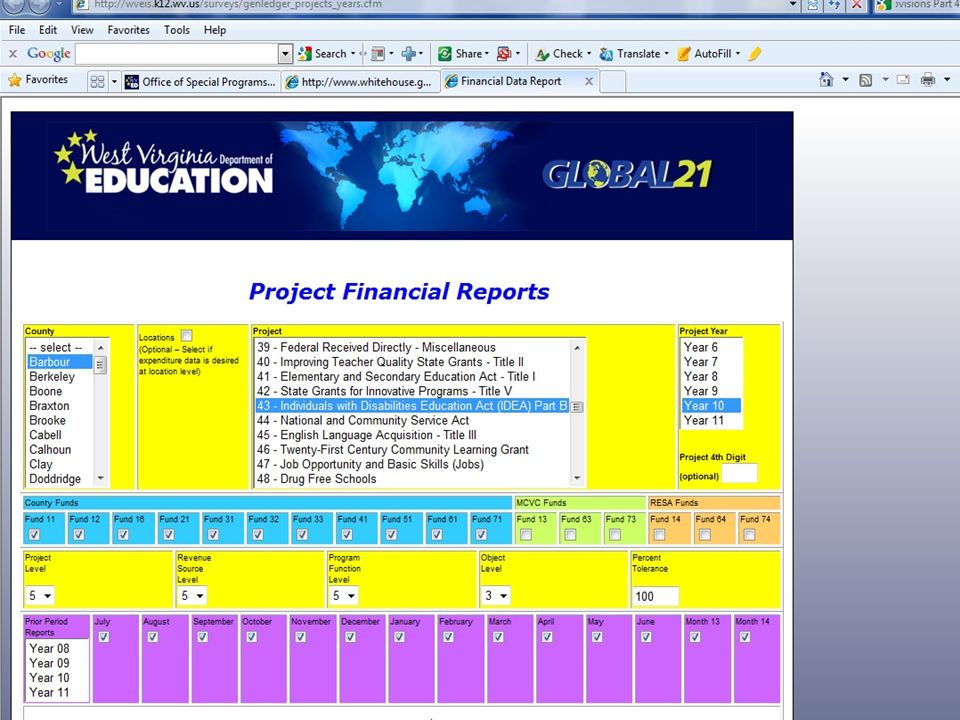

Project Financial Reports Good tool to assist in monitoring budget/expenditures

Select county Select project 02 – state special education 43 – IDEA funds Select fiscal year May select specific months A good source available to Director’s to review financial records. Contains budget for the IDEA grants as well as expenditures.

111

INVENTORY MANAGEMENT EDGAR §80.32(c)-(e)

Equipment Federal definition of Equipment (OMB Circular A-122) Tangible personal property Useful life of more than one year Acquisition cost of $5,000 or more For purposes of maintaining IDEA Inventory As above, except Useful life of more than one year, regardless of acquisition cost Example: PDAs, Computers, Cell phones, Copiers, Projectors, Digital Cameras, Etc. See also WVDE Capital Assets Manual

Tangible personal property. Useful life of more than one year. Acquisition cost of $5,000 or more. For purposes of maintaining IDEA Inventory. As above, except. Useful life of more than one year, regardless of acquisition cost. Example: PDAs, Computers, Cell phones, Copiers, Projectors, Digital Cameras, Etc. See also WVDE Capital Assets Manual.")

112

Inventory Management - Equipment

Must have adequate controls in place to account for: Location of equipment Custody of equipment Security of equipment LEA should have procedures in place and documentation to track and account for the location and assignment of equipment at all times A tracking system must be implemented for requesting and signing out equipment to be used off-site

113

Inventory Management-Equipment

Must protect against unauthorized use May use for other projects as long as use is incidental and does not interfere with authorized use When property is no longer needed, must follow disposition rules Transfer to another federal program Over $5,000 – Keep or sell, but must pay a share based on the percentage of federal ED participation at initial acquisition Under $5,000 – May keep, sell, or dispose of it with no obligation to ED When property is lost, damaged or stolen Follow procedures in the WVDE Procedures Manual Capital Asset System (Send copy of documentation to SEA)

")

114

Monitoring and Compliance

Section 618 Determinations Fiscal management a monitoring focus of OSEP for states and districts Timely and accurate submission of data and LEA application Timely liquidation Time and effort documentation Audit findings

115

Report On The ARRA Grant Funds

Report FTE jobs funded with ARRA IDEA funds Report project status (activities) Report quarterly on the expenditure of ARRA IDEA funds Enter in Five Year Online Strategic Plan –ARRA Reporting by end of each quarter Report vendors receiving payments $25,000 and over, including name, product description

Report quarterly on the expenditure of ARRA IDEA funds. Enter in Five Year Online Strategic Plan –ARRA Reporting by end of each quarter. Report vendors receiving payments $25,000 and over, including name, product description.")

116

Where to Find Federal Education Grants Management Requirements

Office of Management & Budget (OMB) Circulars : A -87; A Circular A-133 Compliance Supplement (2009):

Circulars : A -87; A Circular A-133 Compliance Supplement (2009):")

117

Where to Find Federal Education Grants Management Requirements

Program Rules: Statutes Regulations Guidance General Education Provisions Act (GEPA): Education Department General Administrative Regulations (EDGAR):

: Education Department General Administrative Regulations (EDGAR):")

118

WVDE Financial Requirement Manuals/Forms

119

Contacts Janice Hay (304) Coordinator Office of Internal Operations Sandra McQuain (304) Assistant Director Office of Special Programs

Coordinator Office of Internal Operations Sandra McQuain (304) Assistant Director Office of Special Programs")

120

Medicaid and Education

Additional Source of Funding April 13, 2011

123

State Plan Each state determines its State Plan within the general guidelines of the federal CMS.

124

Medicaid and Education Timeline

1989 1990 2000 Medicaid State Plan Amended IDEA U.S. Congress WV Code b The Medicare Catastrophic Coverage Act changed the section of the Soc. Sec. Act to provide that Medicaid would pay for services provided by the education system to children with IEPs. Each county school district was enrolled by WV Medicaid as a group provider and individual treatment providers for Audiology, Speech, PT, OT, Private Duty Nursing, and Psychology were enrolled if they met Medicaid qualifications. Each county school district was given a second group provider for a group of services that are “cost-based” for treatment planning, care coordination, personal care aide, and transportation (aide and vehicle). …for children with IEPs Added IEPs, Care Coor, Sp. Trans. Personal Aides Only Therapies

. …for children with IEPs. Added. IEPs, Care Coor, Sp. Trans. Personal Aides. Only Therapies.")

125

WV Code b (a) The state board shall become a Medicaid provider and seek out Medicaid eligible students for the purpose of providing Medicaid and related services to students eligible under the Medicaid program and to maximize federal reimbursement for all services available under the Omnibus Budget Reconciliation Act of one thousand nine hundred eighty-nine, as it relates to Medicaid expansion…

The state board shall become a Medicaid provider and seek out Medicaid eligible students for the purpose of providing Medicaid and related services to students eligible under the Medicaid program and to maximize federal reimbursement for all services available under the Omnibus Budget Reconciliation Act of one thousand nine hundred eighty-nine, as it relates to Medicaid expansion…")

126

IDEA A noneducational public agency described in paragraph (b)(1)(i) of this section may not disqualify an eligible service for Medicaid reimbursement because that service is provided in a school context… Reinforced that Medicaid would reimburse covered services provided by the school.

(1)(i) of this section may not disqualify an eligible service for Medicaid reimbursement because that service is provided in a school context… Reinforced that Medicaid would reimburse covered services provided by the school.")

127

IDEA A public agency may use the Medicaid or other public benefits or insurance programs in which a child participates to provide or pay for services required under this part, as permitted under the public benefits or insurance program…

128

IDEA If a public agency spends reimbursements from Federal funds (e.g., Medicaid) for services under this part, those funds will not be considered "State or local" funds for purposes of the maintenance of effort provisions in Sec. Sec and

for services under this part, those funds will not be considered State or local funds for purposes of the maintenance of effort provisions in Sec. Sec and")

129

IDEA Reduction of Other Benefits.--Nothing in this part shall be construed to permit the State to reduce medical or other assistance available or to alter eligibility under title V of the Social Security Act… or title XIX of the Social Security Act (relating to Medicaid for infants or toddlers with disabilities) within the State.

within the State.")

130

Therapy Provider # 0 00XXXXXXXX

1990 2000 Each School District – 1st # Therapy Provider # XXXXXXXX Audiology # OT # PT # SLP # RN # Psychology # Each School District – 2nd # Cost-Based Provider # 15XXXXXXXX - New Initial/Triennial IEP Annual IEP Personal Care (full) Personal Care (part) Sp. Trans. Vehicle Sp. Trans. Aide Care Coordination

Personal Care (part) Sp. Trans. Vehicle. Sp. Trans. Aide. Care Coordination.")

131

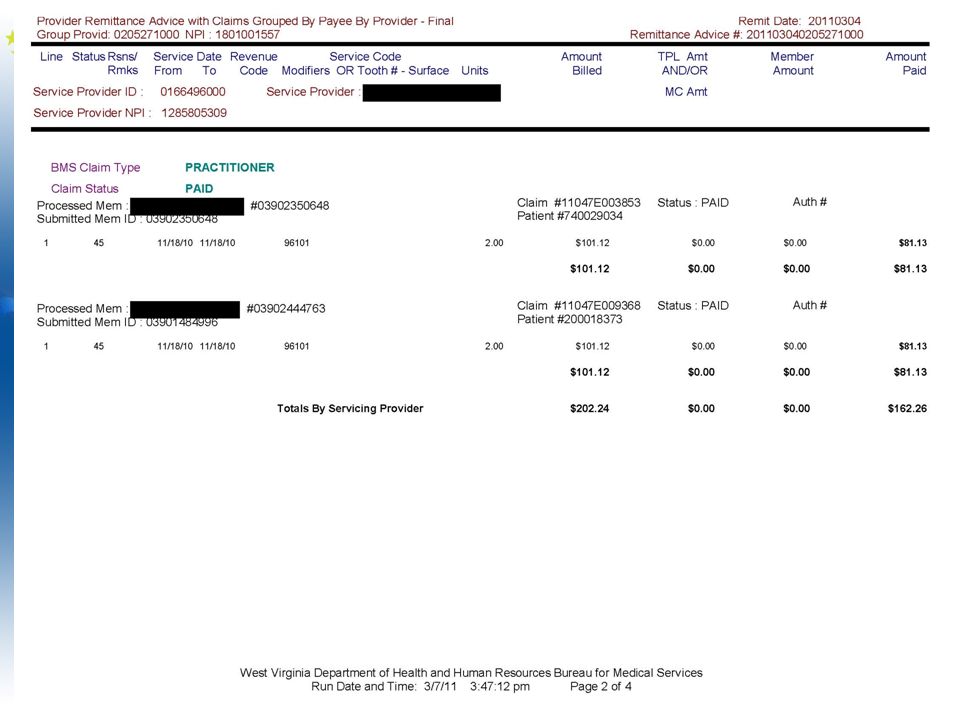

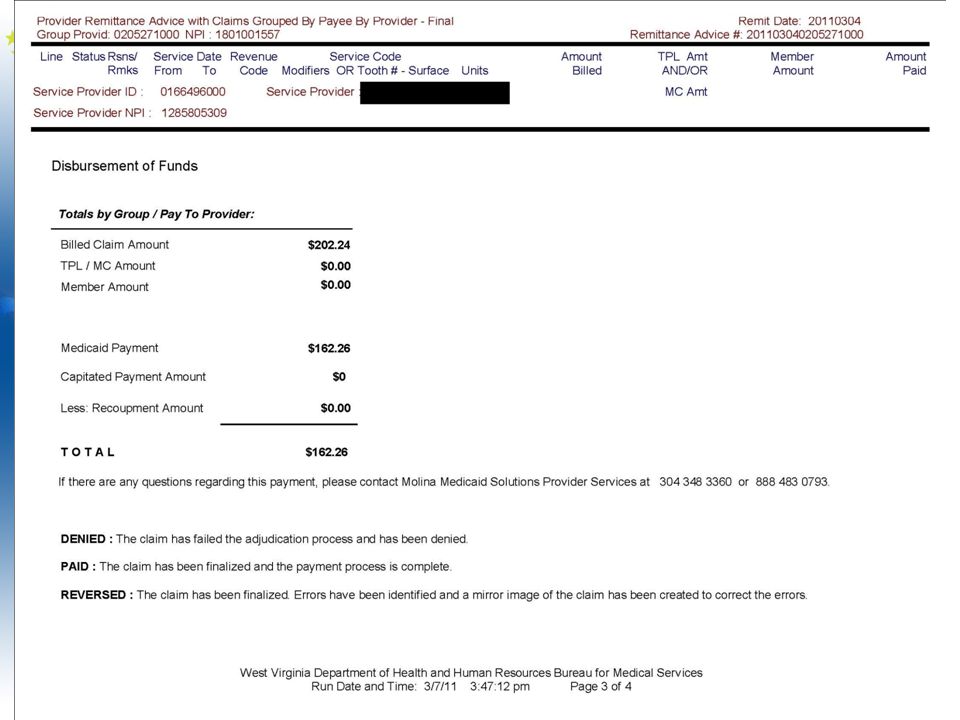

RESA WVDHHR - Molina Processing Agency; LEA Bureau of Medical Services

Billing Form or WVEIS Entry WVDHHR - Molina Processing Agency; Bureau of Medical Services BMS Electronic claim LEA RESA Remittance Advice Denial/pending Payment – Direct Deposit Supporting Documentation: IEP Progress Notes Attendance Records Care Coordination form

132

Documentation Student Related Documentation

Included in IEP services – the IEP form Therapy notes/log: Notes/outcome re: student progress and prognosis The Care Coordination form Personal Care form Specialized Transportation form – number of special education students riding specialized transportation Billing Documentation - WVEIS Maintain documentation in the student’s individual cumulative file in a centralized location.

135

Freedom of Choice Freedom to choose services from providers

outside the school system Medicaid cannot cover duplicate services Establish in writing that the School System is not to seek reimbursement for services that are provided by an outside agency. (Consent form)

")

136

Frequently Asked Questions

Personal care : Services must be provided on a full-time basis. The aide must not be responsible for any other student. Not specific to the aide Full-time / Full Day = $150.94/day ($3,018.80/month – 20 days) Full-time/ Partial Day = $75.47/day ($ /month – 20 days)

Full-time/ Partial Day = $75.47/day ($ /month – 20 days)")

137

Frequently Asked Questions

Care Coordination : Coordinate delivery of services related to IEP. Check all activities completed during that month, but may bill even if only one activity was checked. 1 billing per month/per student = $77.09/mo.

139

Menu

151

January 21 to February 15

152

IDEA Discussion: In order for a public agency to use the Medicaid or other public benefits or insurance program in which a child participates to provide or pay for services required under the Act, the public agency must provide the benefits or insurance program with information from the child's education records (e.g., services provided, length of the services).

.")

153

IDEA Information from a child's education records is protected under the Family Educational Rights and Privacy Act of 1974, (FERPA)… Under FERPA and section 617(c) of the Act, a child's education records cannot be released to a State Medicaid agency without parental consent, except for a few specified exceptions that do not include the release of education records for insurance billing purposes.

… Under FERPA and section 617(c) of the Act, a child s education records cannot be released to a State Medicaid agency without parental consent, except for a few specified exceptions that do not include the release of education records for insurance billing purposes.")

156

ASSISTIVE TECHNOLOGY FUNDING

Kathy Knighton Office of Special Programs West Virginia Department of Education

157

What is Assistive Technology?

“Any item, piece of equipment, or product system, whether acquired commercially or off the shelf, modified, or customized, that is used to maintain, or improve functional capabilities of individuals with disabilities” Individuals with Disabilities Education Act (IDEA). Tremendous potential to promote equity for students with disabilities…… independent self-confident productive integrated into school and society. THIS IS THE FEDERAL DEFINITION OF ASSISTIVE TECHNOLOGY ACCORDING TO THE INDIVIDUALS WITH DISABILITIES EDUCATION ACT – IT IS THE RESPONSIBILITY OF THE IEP COMMITTEE TO DETERMINE THE ASSISTIVE TECHNOLOGY DEVICES OR SERVICES THAT MAY BE NECESSARY FOR A STUDENT WITYH A DISABILITY TO RECEIVE FAPE….IF THE IEP TEAM DETERMINES THAT ASSISTIVE TECHNOLOGY IS NEEDED - IT IS THE RESPONSIBILITY OF THE SCHOOL DISTRICT TO PROVIDE IT. OUR PURPOSE TODAY IS NOT TO DELVE IN TO THE LEGAL ASPECTS OF TECHNOLOGY, BUT TO GIVE YOU A BRIEF OVERFVEW OF ASSISTIVE TECHNOLOGY AND HOW IT CAN BE USED IN THE CLASSROOM WITH ALL STUDENTS.

. Tremendous potential to promote equity for students with disabilities…… independent. self-confident. productive. integrated into school and society. THIS IS THE FEDERAL DEFINITION OF ASSISTIVE TECHNOLOGY ACCORDING TO THE INDIVIDUALS WITH DISABILITIES EDUCATION ACT – IT IS THE RESPONSIBILITY OF THE IEP COMMITTEE TO DETERMINE THE ASSISTIVE TECHNOLOGY DEVICES OR SERVICES THAT MAY BE NECESSARY FOR A STUDENT WITYH A DISABILITY TO RECEIVE FAPE….IF THE IEP TEAM DETERMINES THAT ASSISTIVE TECHNOLOGY IS NEEDED - IT IS THE RESPONSIBILITY OF THE SCHOOL DISTRICT TO PROVIDE IT. OUR PURPOSE TODAY IS NOT TO DELVE IN TO THE LEGAL ASPECTS OF TECHNOLOGY, BUT TO GIVE YOU A BRIEF OVERFVEW OF ASSISTIVE TECHNOLOGY AND HOW IT CAN BE USED IN THE CLASSROOM WITH ALL STUDENTS.")

158

Legal Aspects…… School districts are mandated to make assistive technology available to all students with disabilities if appropriate to receive a free, appropriate public education (FAPE). IEP Team Decision Home Use Funded by district Provide devices/services Consideration of special factors. Assistive technology must be considered for ALL students in the special education process. IDEA is very clear about the responsibility of the school district Home use – big issue AT must be considered for ALL children going through special ed process and checked on the IEP

. IEP Team Decision. Home Use. Funded by district. Provide devices/services. Consideration of special factors. Assistive technology must be considered for ALL students in the special education process. IDEA is very clear about the responsibility of the school district. Home use – big issue. AT must be considered for ALL children going through special ed process and checked on the IEP.")

159

Challenges of Delivering Assistive Technology

Lack of Information Current/accurate information Lack of Expertise Skills/Knowledge High Rate of Abandonment 1/3 abandoned after first year Lack of Funding Significant barrier Inclusion and Lack of Assistive Technology

160

Implications for Schools

PLANNING School district’s long range technology and special education plans, procedures, services, and budget include assistive technology. TRAINING All staff are able to appropriately “consider” students for assistive technology services and/or devices. Staff are trained to integrate technology in teaching to help students with disabilities gain skills and achieve higher standards. INCLUSION Assistive technology is used to support the inclusion of students with disabilities in regular education placements and access to the general curriculum. As a result of legislation and the districts obligation – there are several implication for school districts.

161

FUNDING QUESTIONS ARE SCHOOL DISTRICTS REQUIRED TO PAY FOR ASSISTIVE TECHNOLOGY DEVICES AND SERVICES? Yes. District must provide the equipment, services or programs recommended in the IEP. Use federal, state, or local funds Access other sources such as Medicaid, Vocational Rehabilitation, and/or private health insurance policies to pay for the devices and services. CAN SCHOOL DISTRICTS REQUIRE PARENTS TO USE THEIR PRIVATE INSURANCE TO PAY FOR NECESSARY ASSIS5IVE TECHNOLOGY DEVICES AND SERVICES? No. “Free” in FAPE is extremely significant regarding children with disabilities who may require assistive technology devices or services. As stated in IDEA and its regulations, all aspects of special education and related services must be provided "at no cost to the parents." If family agrees to allow the district to access private insurance Decision must be strictly voluntary.

162

Funding…….. CAN FAMILIES BE ASKED TO PURCHASE THE DEVICES OR AUGMENT THE IDENTIFIED ASSISTIVE TECHNOLOGY NEEDS OF THEIR CHILD? Shared responsibility between school, families, employers, and community Parents must agree to Joint funding If family does purchase the AT device, schools cannot mandate that the device be brought to school. Families can insist that another device be provided for school use. ARE THERE OTHER OPTIONS FOR SCHOOLS TO CONSIDER IN LIEU OF PURCHASING THE ASSISTIVE TECHNOLOGY DEVICE? Yes. Purchase of equipment or devices is not always necessary or even advisable Temporary condition or expected to improve or deteriorate Need to try-out equipment before purchase for a student Consider rental or long-term lease - purchase options Long-term leasing or lease/ purchase agreements benefits no obligation on behalf of the school to purchase device; reduction of obsolete inventory use of equipment without a lump sum purchase; flexible leasing terms; upgrading equipment as more improved technology becomes available; and, upgrading equipment as the student's needs change.

163

Funding…… CAN SCHOOL DISTRICTS SHARE THE FUNDING RESPONSIBILITIES OF PROVIDING ASSISTIVE TECHNOLOGY DEVICES AND SERVICES? YES. Transitioning from WV Birth to Three programs to public school preschool programs Transitioning from public school to adult services through Rehabilitation Services Ownership of the device is an important issue to consider by IEP Teams DO SCHOOL DISTRICTS HAVE THE RESPONSIBILITY TO PAY FOR AN INDEPENDENT EDUCATION EVALUATION (IEE) REGARDING ASSISTIVE TECHNOLOGY? YES. Parent has right to an IEE at public expense if the parent disagrees with an evaluation obtained by the public agency. Requirements in WV Policy 2419: Regulations for the Education of Exceptional Students. ARE SCHOOL DISTRICTS RESPONSIBLE FOR CUSTOMIZATION, MAINTENANCE, REPAIR AND REPLACEMENT OF ASSISTIVE TECHNOLOGY DEVICES? YES. If family owned AT is used by the school, on the IEP, and is necessary for providing Free Appropriate Public Education (FAPE) District responsible for maintenance, repair, and re-placement

REGARDING ASSISTIVE TECHNOLOGY YES. Parent has right to an IEE at public expense if the parent disagrees with an evaluation obtained by the public agency. Requirements in WV Policy 2419: Regulations for the Education of Exceptional Students. ARE SCHOOL DISTRICTS RESPONSIBLE FOR CUSTOMIZATION, MAINTENANCE, REPAIR AND REPLACEMENT OF ASSISTIVE TECHNOLOGY DEVICES YES. If family owned AT is used by the school, on the IEP, and is necessary for providing Free Appropriate Public Education (FAPE) District responsible for maintenance, repair, and re-placement.")

164

ASSISTIVE TECHNOLOGY SUPPLEMENTAL FUNDING GRANT

PURPOSE OF SUPPLEMENTAL FUNDING GRANT Resource when unanticipated costly assistive technology device and/or service for a specific student with a disability and other funding sources are not available. Reimbursement for assistive technology devices and/or services is contingent upon an approved application with corresponding required documentation and funding availability. Responsibility of district to purchase AT immediately after identified. Districts required to ensure that AT is provided regardless of any funding opportunities from the Office of Special Programs. PRIORITIES OF SUPPLEMENTAL FUNDING GRANT Newly identified students with costly assistive technology needs as determined by an IEP team. Not students who have previously been identified and should have been receiving assistive technology devices and/or services.

165