Download presentation

Presentation is loading. Please wait.

1

The Behavior of Interest Rates

Chapter 5

3

Nominal Interest Rates

Nominal interest rates on 3-mo. Treasury Bills were about 1% in the fifties. In the eighties they were 15%. At the end of 2000, they were above 6%; in the middle of 2003, they were 1%. What is the explanation for these interest rate fluctuations? The explanation for “the” nominal interest rate should apply to all nominal rates since interest rates usually move together.

4

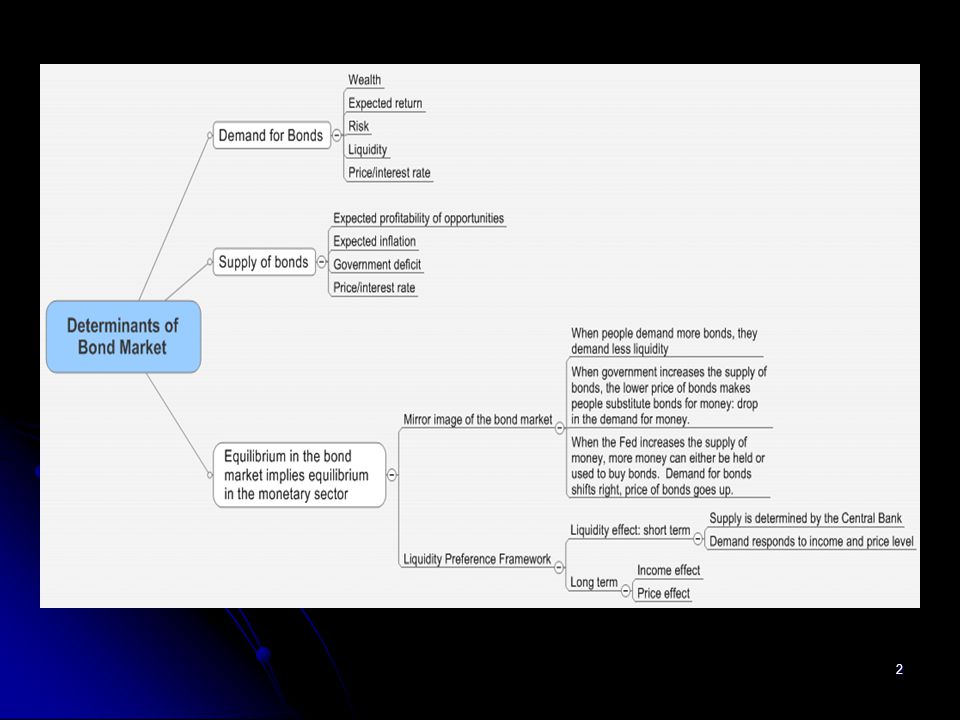

Determinants of Asset Demand

The higher the wealth of an individual, the higher will be her demand for assets, both financial and real. The higher the expected return from an asset compared to other assets, the higher the demand for that asset. The riskier an asset is, the less there will be a demand for it. The more liquid an asset is, the higher the demand will be.

5

Bond Price and Interest Rate

Bond prices and interest rates are always inversely related. A discount bond that matures a year from now and priced at $900 carries an interest rate of ( )/900=11.1%. A discount bond that matures a year from now and priced at $800 carries an interest rate of ( )/800=25%. A console that pays $100 per year and sells for $1000 carries an interest rate of 10%. The same console when sold at $1250 carries an interest rate of 8%.

/900=11.1%. A discount bond that matures a year from now and priced at $800 carries an interest rate of ( )/800=25%. A console that pays $100 per year and sells for $1000 carries an interest rate of 10%. The same console when sold at $1250 carries an interest rate of 8%.")

6

Demand for Bonds In boom times wealth (and income) rise. Demand for bonds will rise, too. During recessions demand for bonds will fall. If interest rates in the future are expected to fall, long-term bonds will have capital gains and increased returns, raising the demand for bonds. If the prices of bonds become more volatile, the demand for bonds will fall. If bonds became more liquid relative to other assets, the demand for bonds will increase.

7

Measuring Demand for Bonds

Typical demand curve would have price of bonds on the vertical axis and quantity of bonds on the horizontal axis. If bonds were the only form for funds to be raised, then those who demand to purchase bonds are the ones who supply funds. Demand for bonds is mirror image of supply of loanable funds.

8

Bond Price and Interest Rate

25% $800 $900 11.1% 11.1% $900 25% $800 Quantity of bonds Loanable funds An increase in the demand for bonds is the same as an increase in the supply of loanable funds.

9

Demand and Supply As the price of bonds falls, lender-savers will want to buy more: demand is downward sloping. As the interest rate rises, lender-savers will want to supply more funds into the market: supply of loanable funds is upward sloping.

10

Demand and Supply As the price of bonds falls, borrower-investors will be more reluctant to issue bonds: the supply of bonds will be upward sloping. As the interest rate rises, borrower-investors will be more reluctant to borrow: demand for loanable funds will be downward sloping.

11

Shifts in the Demand for Bonds

Wealth: in an expansion with growing wealth, the demand curve for bonds shifts to the right Expected Returns: higher expected interest rates in the future lower the expected return for long-term bonds, shifting the demand curve to the left Expected Inflation: an increase in the expected rate of inflations lowers the expected return for bonds, causing the demand curve to shift to the left Risk: an increase in the riskiness of bonds causes the demand curve to shift to the left Liquidity: increased liquidity of bonds results in the demand curve shifting right

12

Supply of Bonds Increased confidence of producers means higher expected profits: they tend to borrow more. Increase supply of bonds = Increase demand for loanable funds A rise in the expected inflation, given nominal interest rates, would lower the cost of borrowing (real interest rate). Higher government deficits are financed by government borrowing.

. Higher government deficits are financed by government borrowing.")

13

Impact on Interest Rates of a Sudden Increase in the Volatility of Gold Prices

Gold becomes a riskier asset. Bonds become relatively attractive. Demand for bonds increases. Price of bonds rise and interest rate falls. P P Q of bonds

14

Impact on Interest Rates When Real Estate Prices Are Expected to Rise

The expected returns from real estate increases. Bonds become less attractive; demand drops. Price of bonds fall and interest rates rise. P i P i Quantity of bonds

15

Impact on Interest Rates When Recession Occurs

During recessions, investment opportunities dry up. Businesses scrap expansion plans. New bonds are not issued. Supply of bonds falls. The wealth effect of the recession will reduce the demand for bonds, too. The net result is increase in the price of bonds and decrease in the interest rates. P i P i

16

Business Cycle and Interest Rates

17

Impact on Interest Rates When Expected Inflation Falls

the expected return on bonds rises: bondholders expect capital gains. Demand shifts to the right. On the other hand, at a given nominal interest rate, the fall in expected inflation raises the real interest rate. The cost of borrowing increases, lowering the supply of bonds. Price rises, interest rate falls. P i P i Q of bonds

18

Expected Inflation and Interest Rates (Three-Month Treasury Bills), 1953–2008

Source: Expected inflation calculated using procedures outlined in Frederic S. Mishkin, “The Real Interest Rate: An Empirical Investigation,” Carnegie-Rochester Conference Series on Public Policy 15 (1981): 151–200. These procedures involve estimating expected inflation as a function of past interest rates, inflation, and time trends.

: 151–200. These procedures involve estimating expected inflation as a function of past interest rates, inflation, and time trends.")

19

Japan Japan experienced a prolonged recession for two decades.

Demand and supply of bonds both fell, raising the price of bonds and lowering the interest rate. Prolonged recession created deflation, making the expected return on real assets negative. Money (cash) became more desirable. Bonds less desirable than money but still preferable to real assets. Interest rates in Japan were close to zero.

became more desirable. Bonds less desirable than money but still preferable to real assets. Interest rates in Japan were close to zero.")

20

Response to a Business Cycle Expansion

If this depiction is true, what should we see happen to interest rates?

22

Impact on Interest Rates When U. S

Impact on Interest Rates When U.S. Started To Retire Long-Term Debt in 1999 i P The announcement that the Treasury will buy back 30-yr bonds raised the price of these bonds and reduced the interest rate on these bonds. As a result, the yield curve turned down at the long-term maturity end. P i

23

Impact of Low Savings on Interest Rates

US personal savings rate (Personal income - Consumption) was at all time low in Low savings imply shrinking of lender-saver funds. As loanable funds shrink the demand for bonds falls. The price of bonds falls and interest rate rises.

was at all time low in Low savings imply shrinking of lender-saver funds. As loanable funds shrink the demand for bonds falls. The price of bonds falls and interest rate rises.")

24

Liquidity Preference Framework

We have seen that interest rates can be determined using the equilibrium in the bond market or its mirror image, loanable funds market. Those who buy bonds are the ones who loan funds and those who sell bonds are the ones who borrow. If bonds and money are the two categories of assets people use to store wealth, then equilibrium in bond market will imply equilibrium in the market for money.

25

How To Divide Assets Into Money and Bonds

Currency Demand deposits Bonds Savings deposits Time deposits Stocks

26

Equilibrium in Bond Market = Equilibrium in Money Market

Total supply of wealth has to equal to total demand for wealth: Ms + Bs = Md + Bd If the bond market is in equilibrium, Bs = Bd. Therefore, the market for money must be in equilibrium, Ms = Md.

27

Bond vs. Money Market Equilibrium in the bond market determines bond prices and interest rates, since each bond price is associated with a unique interest rate. Equilibrium in the market for money also determines the interest rate. The approaches are interchangeable, though the effects of some variable changes are easier to observe in one approach over the other.

28

Liquidity Preference Why do people want to hold money?

To conduct purchases; for transaction purposes. Keynesian definition of money concentrates on the medium of exchange function and assumes that the return on money is zero. What makes people to hold more money? Income increases. Price level increases. Interest rate drops. Opportunity cost of holding money drops.

29

Liquidity Preference = Md

The demand for money is drawn with interest rate on the vertical axis and quantity of money on the horizontal axis. The higher the interest rate, the higher is the opportunity cost of holding money, and the lower is the amount of money held. The demand for money becomes a downward sloping curve, a typical demand curve. Increases in income and/or the price level shift the curve to the right.

30

Equilibrium in the Market for Money

For the time being, we will assume that the supply of money is determined by the monetary authority, the central bank. Equilibrium between supply and demand for money takes place at a unique interest rate. If at a given interest rate, Md > Ms, then people will sell bonds to convert them to cash. Bond prices will go down. Interest rates will go up, reducing Md. If Md<Ms, people will convert money into bonds. The price of bonds will go up, lowering the interest rate until Md=Ms.

31

Impact of an Increase In Income (Business Boom) on Interest Rates

Q of bonds

32

Impact on Interest Rates of an Increase in the Price Level

Q of bonds Price level increase forces people to hold more money to make the same purchases. The adjustment in the liquidity preference framework comes about as people sell their bonds and keep cash. In the bond market, the supply of bonds rises, lowering the price and raising the interest rate.

33

Impact on Interest Rates of an Increase in Ms

Q of bonds In the liquidity preference framework, increase in the money supply is shown by a rightward shift of Ms. An excess of Ms over Md prompts people to buy bonds and thus raise the price of bonds, lowering the interest rate.

34

Impact on Interest Rates of A Rise in Expected Inflation

Q of bonds M An increase in the expected inflation will lower the expected returns on bonds because interest rates will rise forcing capital losses on bonds. On the other hand, bond issuers will expect to pay lower real interest rates in the future and increase their supply. Prices of bonds will fall and interest rates will rise. In the liquidity preference framework, the reluctance of bondholders to hold bonds translates into an increase in the demand for money and a rise in the interest rate.

35

A Rise in the Money Supply May Not Lower Interest Rates in The Long-Run

Ms up => i down (liquidity effect) i down => I up => Y up (income effect) => Md up Y up => P up (price level effect) => Md up P up => expected inflation up (expected inflation effect) => Md up In the liquidity preference framework, income and price level effects will directly translate into a rightward shift of Md.

i down => I up => Y up (income effect) => Md up. Y up => P up (price level effect) => Md up. P up => expected inflation up (expected inflation effect) => Md up. In the liquidity preference framework, income and price level effects will directly translate into a rightward shift of Md.")

36

Possible Outcomes If the liquidity effect is larger than the other effects, an increase in Ms will lower interest rates. If the liquidity effect is smaller than other effects but expectations adjust slowly, an increase in Ms will lower the interest rates initially but will raise them in the long run. If the liquidity effect is smaller than other effects and expectations adjust quickly, an increase in Ms will only bring an increase in interest rates.

38

Quarterly Money Growth Rates and Short Term Interest Rate

39

Annual Money Growth Rates and Short Term Interest Rate

40

Annual Money Growth Rates and Short Term Interest Rate

Similar presentations

Lecturer: Mr S. Puran Topic: Central Banking and the Monetary System.>")