Download presentation

Presentation is loading. Please wait.

1

Ohio Department of Taxation’s Casino Training

Tuesday, April 24, 2012 10:30 a.m. to 12:30 p.m. gotomeeting.com/join/

2

Agenda Welcome and Introduction

Stacey Savarise, Administrator of Organizational Development Employer Withholding & Winners Withholding Richard Six, Assistant Administrator of Business Tax Division Sales & Use Tax Phyllis Shambaugh, Counsel for Sales & Use Tax Division Keith Wilson, Assistant Administrator of Sales & Use Tax Division Commercial Activity Tax (CAT) Charles Willis, Assistant Administrator of Commercial Activity Tax Division

Charles Willis, Assistant Administrator of Commercial Activity Tax Division.")

3

Winners & Employer Withholding

Richard Six Assistant Administrator Ohio Department of Taxation 3

4

Winners Withholding – Requirements

Withhold at rate of 6% on winnings reported to IRS on Form W-2G. $1,200 on slot winnings, $5,000 table games Issue receipt to winner showing taxes deducted Winner statement “default under a support order” Proposed change would send statement to ODJFS Statutory reference: R.C 4

5

Winners Withholding – Responsibility

Casino operator is personally liable For amounts withheld and not remitted Interest / Penalty Interest for late payment – statutory rate (3% for 2012) Penalty Late filing, late payment, nonpayment Up to $1,000 per occurrence Assessed in the same manner as income tax withholding collected by an employer. Transfer/Sale: successor must withhold from purchase money: tax, interest and penalty due. Statutory reference: R.C (3)(a) and (b) 5

Penalty. Late filing, late payment, nonpayment. Up to $1,000 per occurrence. Assessed in the same manner as income tax withholding collected by an employer. Transfer/Sale: successor must withhold from purchase money: tax, interest and penalty due. Statutory reference: R.C (3)(a) and (b) 5.")

6

Winners Withholding – Filing

Monthly winners report filed electronically with Ohio Dept. of Taxation Identify winners and tax withholding Upload report through FTP : Sample template Format = Excel (.csv) comma delimited Report is due by the 10th banking day of the subsequent month (May 2012 due June 14, 2012) Proposed change to 10th day of subsequent month Year-end report to reconcile – form IT-941 W-2G report at year-end 6

comma delimited. Report is due by the 10th banking day of the subsequent month (May 2012 due June 14, 2012) Proposed change to 10th day of subsequent month. Year-end report to reconcile – form IT-941. W-2G report at year-end. 6.")

7

Winners report in Excel format – next slide shows saving as CSV (comma delimited file) for FTP

7

8

After you save your report, you will send your monthly report to us via FTP.

8

9

Winners Withholding – Payment

Monthly payment of taxes withheld Must be paid electronically Due by the 10th banking day of the month Proposed change to 10th day of subsequent month Payment made through Ohio Business Gateway or Treasurer of State (TOS) If through TOS, need to pre-register (fax in form to TOS) If OBG, register for employer withholding account and file and pay using IT-501 File year end-report form IT-941 to reconcile account and pay any remaining tax due. 9

If through TOS, need to pre-register (fax in form to TOS) If OBG, register for employer withholding account and file and pay using IT-501. File year end-report form IT-941 to reconcile account and pay any remaining tax due. 9.")

10

Business Filings on the Ohio Business Gateway (OBG) http://business

TAX FILING FOR BUSINESSES: “MORE INFORMATION. LESS PAPER.” OBG is the method for businesses to electronically register and file/pay. It cuts down greatly on processing errors and most of the services are free. Businesses receive confirmation that reports are filed. It also provides a quick and easy way to comply with government requirements through self service. We strive to greatly expand these options for added convenience. Reporting is available for 8 different state agencies and more than 500 municipalities, listed below: Unemployment & Ohio Means Jobs (ODJFS) Worker’s Comp (BWC) Ohio Dept. of Taxation Municipal Income Tax - over 500 municipalities (Net Profits and Withholding) Ohio Dept. of Commerce (unclaimed funds reports) Services and Transactions in alphabetical order by agency Ohio Department of Administrative Services Equal Opportunity Division Affirmative Action Program Verification Certificate Of Compliance Application Construction Contract I-29 Unified Application Recertification Affidavit EDGE Cross Certification EDGE Mediation Complaint Ohio Office of Budget and Management Declaration of Material Assistance/Nonassistance Ohio Department of Commerce Division of Unclaimed Funds Unclaimed Funds Report Unclaimed Funds Negative (None) Report Ohio Department of Job and Family Services Unemployment Compensation Tax Employer's Report of Wages (JFS-66111, formerly UCO-2QR) OhioMeansJobs Company Registration Employee Registration Search for Ohio Resumes Municipal Income Tax Agencies and Administrators Business Income (Net Profits) Taxes Estimated Payments Extension Requests Income (Net Profits) Tax Returns Employer Withholding Taxes Withholding Returns and Payments Ohio Public Employees Deferred Compensation Program Employer Contributions Notification, billing, collection, and reconciliation of 457 plan contribution payments Employer Contact Information update Ohio Rehabilitation Services Commission Bureau of Services for the Visually Impaired - Business Enterprise Program Monthly Operating Report Ohio Department of Taxation Commercial Activity Tax CAT Returns (Semi-Annual, Annual, Minimum Fee, Annual, and Quarterly) Payment only (return already filed) CAT Assessment Payments Billing Notice Payment Address/contact, filing frequency, corporate structure, and cancel account updates Employer Withholding Withholding Tax Reports IT-501 Employer's Withholding IT-941 Employer's Annual Reconciliation IT-942 Quarterly and 4th Quarter/Annual Reconciliations School District Withholding Tax Reports SD-101 Employer's School District Withholding SD-141 Employer's School District Reconciliation Assessment Payment Withholding account number maintenance Sales Tax State, County, and Transit Sales Tax Returns (UST-1) Cumulative Filing Report for Destination and Origin Sales (CRDO) Accelerated Sales Tax Payments Tax Licenses and Registrations Ohio School District Withholding Ohio Employer Withholding Sales/Use Tax County Vendor's Licenses Consumer's Use Tax Delivery License Transient License Service License Out-of-State Sellers License Ohio Bureau of Workers' Compensation Payroll Report 10

Worker’s Comp (BWC) Ohio Dept. of Taxation. Municipal Income Tax - over 500 municipalities (Net Profits and Withholding) Ohio Dept. of Commerce (unclaimed funds reports) Services and Transactions in alphabetical order by agency. Ohio Department of Administrative Services. Equal Opportunity Division. Affirmative Action Program Verification. Certificate Of Compliance Application. Construction Contract I-29. Unified Application. Recertification Affidavit. EDGE Cross Certification. EDGE Mediation Complaint. Ohio Office of Budget and Management. Declaration of Material Assistance/Nonassistance. Ohio Department of Commerce. Division of Unclaimed Funds. Unclaimed Funds Report. Unclaimed Funds Negative (None) Report. Ohio Department of Job and Family Services. Unemployment Compensation Tax. Employer s Report of Wages (JFS-66111, formerly UCO-2QR) OhioMeansJobs. Company Registration. Employee Registration. Search for Ohio Resumes. Municipal Income Tax Agencies and Administrators. Business Income (Net Profits) Taxes. Estimated Payments. Extension Requests. Income (Net Profits) Tax Returns. Employer Withholding Taxes. Withholding Returns and Payments. Ohio Public Employees Deferred Compensation Program. Employer Contributions. Notification, billing, collection, and reconciliation of 457 plan contribution payments. Employer Contact Information update. Ohio Rehabilitation Services Commission. Bureau of Services for the Visually Impaired - Business Enterprise Program. Monthly Operating Report. Ohio Department of Taxation. Commercial Activity Tax. CAT Returns (Semi-Annual, Annual, Minimum Fee, Annual, and Quarterly) Payment only (return already filed) CAT Assessment Payments. Billing Notice Payment. Address/contact, filing frequency, corporate structure, and cancel account updates. Employer Withholding. Withholding Tax Reports. IT-501 Employer s Withholding. IT-941 Employer s Annual Reconciliation. IT-942 Quarterly and 4th Quarter/Annual Reconciliations. School District Withholding Tax Reports. SD-101 Employer s School District Withholding. SD-141 Employer s School District Reconciliation. Assessment Payment. Withholding account number maintenance. Sales Tax. State, County, and Transit Sales Tax Returns (UST-1) Cumulative Filing Report for Destination and Origin Sales (CRDO) Accelerated Sales Tax Payments. Tax Licenses and Registrations. Ohio School District Withholding. Ohio Employer Withholding. Sales/Use Tax. County Vendor s Licenses. Consumer s Use Tax. Delivery License. Transient License. Service License. Out-of-State Sellers License. Ohio Bureau of Workers Compensation. Payroll Report. 10.")

11

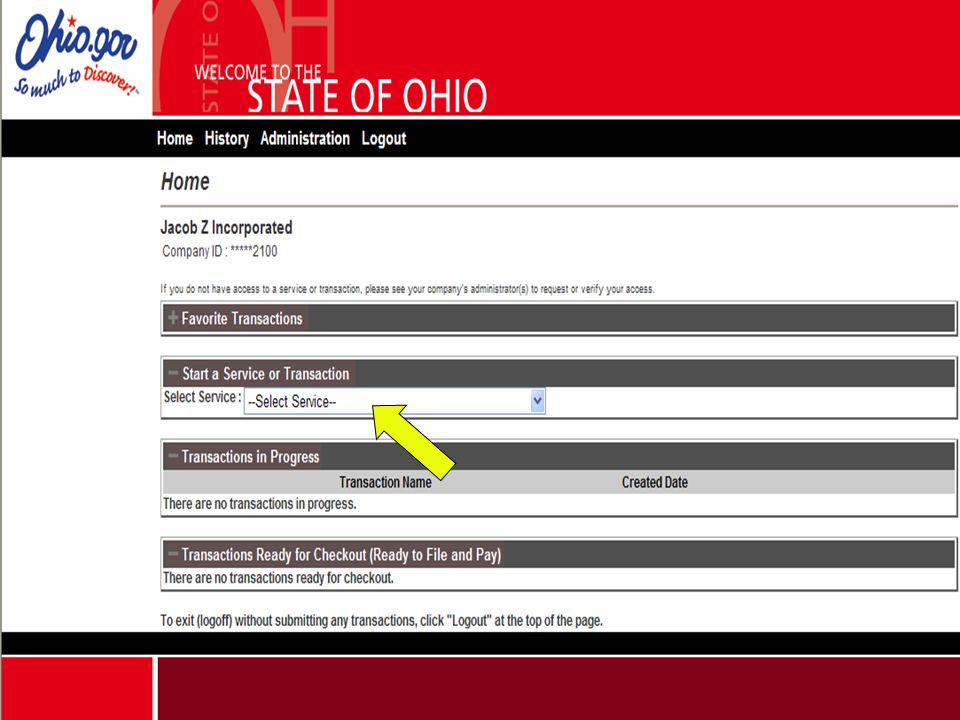

After you have logged in under your username and password, you will see the following screen where you can select the “service” or “transaction.” 11

12

12

13

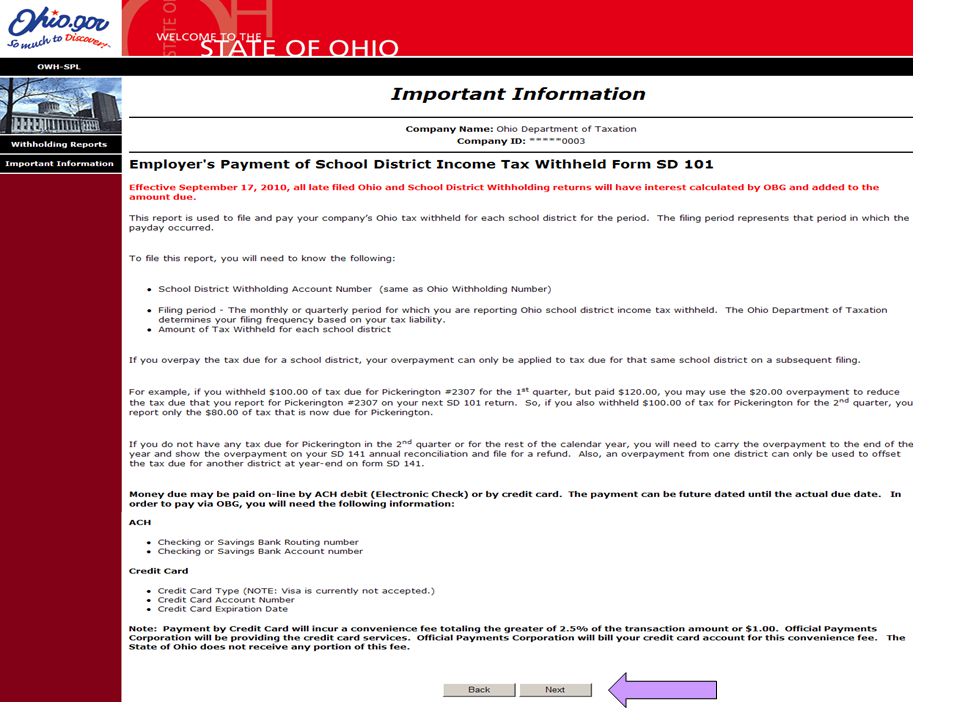

This is an informational page

This is an informational page. Click next button at the bottom of page to advance. 13

14

14

15

OBG shows that the due date for a monthly return is on the 15th of the month. However, payment of the tax withheld on winners is due by the 10th banking day after the end of the month. 15

16

16

17

If you click “Immediately,” STEP 3 will ask how you would like to pay.

17

18

ACH Debit is the only EFT choice on OBG. Credit card incurs a fee of 2

ACH Debit is the only EFT choice on OBG. Credit card incurs a fee of 2.5% charged by OPC. 18

20

20

21

21

22

22

24

If you want to, you can also make a screen shot of the filing for your records.

Also, transactions can be located via the OBG confirmation #. 24

25

Click on History at the top. You can view reports that you have filed.

26

Employer and School District Withholding (Employee Payroll) – Requirements

Withhold income tax on compensation that is earned or received in Ohio. Exception: residents of neighboring states, refer to ORC (A)(3) The amount of Ohio income tax to withhold is “an amount substantially equivalent to the tax reasonably estimated to be due from the employee for the taxable year…” ORC (A) The Tax Commissioner publishes withholding tables for employers to use to determine the amount of income tax to withhold. Last revision eff. 1/1/09. Tables: tax.ohio.gov (Employer Withholding page) 26

(3) The amount of Ohio income tax to withhold is an amount substantially equivalent to the tax reasonably estimated to be due from the employee for the taxable year… ORC (A) The Tax Commissioner publishes withholding tables for employers to use to determine the amount of income tax to withhold. Last revision eff. 1/1/09. Tables: tax.ohio.gov (Employer Withholding page) 26.")

27

Employer and School District Withholding (Employee Payroll) – Requirements

Withhold on: Compensation (required): Reported on form W-2. Wages, salaries, tips, bonuses, commissions, severance pay, stock options, buyouts, back pay, etc. and other types of compensation. Pensions (voluntary): Reported on form 1099-R. Withholding is voluntary upon request of the recipient. Note: Do not withhold on payments properly reported on IRS Form MISC, such as on payments made to Independent Contractors. 27

: Reported on form W-2. Wages, salaries, tips, bonuses, commissions, severance pay, stock options, buyouts, back pay, etc. and other types of compensation. Pensions (voluntary): Reported on form 1099-R. Withholding is voluntary upon request of the recipient. Note: Do not withhold on payments properly reported on IRS Form 1099-MISC, such as on payments made to Independent Contractors. 27.")

28

Employer and School District Withholding (Employee Payroll) – Overview

Steps: Register for an Ohio withholding number Canvass employees for exemptions and school district of residence Employee Exemption Certificate (Form IT 4) Withhold taxes Pay taxes File payment forms: IT 501 and SD 101 Reconciliation forms at year-end File forms: IT-941 (or IT-942) & SD 141 W-2 filing (Form IT-3) 28

Withhold taxes. Pay taxes. File payment forms: IT 501 and SD 101. Reconciliation forms at year-end. File forms: IT-941 (or IT-942) & SD 141. W-2 filing (Form IT-3) 28.")

29

Employer and School District Withholding (Employee Payroll) – Registration

Employers must register with ODT within 15 days from the date that liability begins. An account number is assigned to the Ohio Withholding Agent after the registration has been completed. The Ohio withholding account number is reported on tax return filings and forms W-2 issued to the employees. 29

30

Employer and School District Withholding (Employee Payroll) – Personal Exemptions

Canvass employees to determine: Number of Personal & Dependent Exemptions (used to determine amount of tax to withhold) School District of Residence State of Residency Applicable Forms (retain in employee’s personnel file): IT 4 (Employee Exemption Certificate) IT 4NR (Employee Resident of Neighboring State) IT-MIL SP (Military Spouse Nonresident) IT 4 MIL (Military employees only) Withholding Tables (Effective 1/1/2009) 30

School District of Residence. State of Residency. Applicable Forms (retain in employee’s personnel file): IT 4 (Employee Exemption Certificate) IT 4NR (Employee Resident of Neighboring State) IT-MIL SP (Military Spouse Nonresident) IT 4 MIL (Military employees only) Withholding Tables (Effective 1/1/2009) 30.")

31

Employer and School District Withholding (Employee Payroll) – Personal Exemptions

Employee can claim one exemption each for: Self Spouse Dependents (same as IRS) Note: Make sure that employees do not claim an excessive number of personal exemptions. Report to Ohio Dept. of Taxation: More than 9 exemptions that cannot be substantiated Send us a copy of the employee’s Form IT 4 Withhold tax using zero exemptions until employee properly completes his/her Form IT 4 Source: Information Release IT Proper Completion of Form IT-4 (August 31, 2001) 31

Note: Make sure that employees do not claim an excessive number of personal exemptions. Report to Ohio Dept. of Taxation: More than 9 exemptions that cannot be substantiated. Send us a copy of the employee’s Form IT 4. Withhold tax using zero exemptions until employee properly completes his/her Form IT 4. Source: Information Release IT Proper Completion of Form IT-4 (August 31, 2001) 31.")

32

Employer Withholding-Personal Exemptions

Form IT 4 (Employee Exemption Certificate) Employees cannot claim to be exempt 32

Employees cannot claim to be exempt. 32.")

33

Employer and School District Withholding (Employee Payroll) – Personal Exemptions

Employees can use the "Finder” database to determine school district of residence. 33

34

Employer and School District Withholding (Employee Payroll) – Personal Exemptions

“Finder” will display SD name and four digit number. IT-4: Employee can check SD residence by using the “Finder” on our website and indicate the 4 digit number on the IT-4. If the employee is not sure, they can check with County Board of Elections or County Auditors office to verify SD based on their address. 34

35

Employer and School District Withholding (Employee Payroll)

Residents of Neighboring states (IN, KY, WV, PA and MI) Owe state income tax to his/her home state (due to reciprocal agreements) Employee completes form IT 4NR to exempt Do not withhold Ohio state income tax. Exemption does not apply to city (municipal) income tax withholding. Statutory reference: R.C (A)(3) 35

Owe state income tax to his/her home state. (due to reciprocal agreements) Employee completes form IT 4NR to exempt. Do not withhold Ohio state income tax. Exemption does not apply to city (municipal) income tax withholding. Statutory reference: R.C (A)(3) 35.")

36

Employer and School District Withholding (Employee Payroll)

Form IT 4NR - Residents of Neighboring States 36

37

Employer and School District Withholding (Employee Payroll)

Spouse of military member is not subject to withholding on wages earned in Ohio if the military member is a nonresident who is stationed in Ohio. 37

38

Employer Withholding – Website

38

39

Employer Withholding – Tax Tables

Ohio Withholding Tables for pay periods: 39

40

Employer Withholding – Filing/Payment

Look-Back Period: The filing/payment frequency (“filing status”) for each year is determined by way of a 12 month “look-back period,” which ends on June 30th of the preceding calendar year. For calendar year 2012, the applicable look-back period is July 2010 through June 2011. The filing status for the calendar year (2012) is determined by the combined amount of Ohio and school district tax liability during the “look-back period.” A new business will default to a quarterly filing status because there was no withholding liability during the look-back period. Statutory Reference: R.C 40

for each year is determined by way of a 12 month look-back period, which ends on June 30th of the preceding calendar year. For calendar year 2012, the applicable look-back period is July 2010 through June The filing status for the calendar year (2012) is determined by the combined amount of Ohio and school district tax liability during the look-back period. A new business will default to a quarterly filing status because there was no withholding liability during the look-back period. Statutory Reference: R.C")

41

Employer Withholding – Filing/Payment

Partial-Weekly periods: Two periods each week: Saturday through Tuesday Wednesday through Friday A partial weekly period cannot extend from one calendar year into the next. For 2011, Dec 31st was a Saturday; resulting in a one-day period. For 2012, Dec 31st ends on a Monday; so Saturday, Sunday and Monday will constitute one period and Tuesday 1/1/2013 is a separate period. 41

42

Employer Withholding – Filing/Payment

Filing Requirements: $100,000 or more accumulation rule. Payment is due by the end of the next banking day Partial-weekly (EFT) filer: Look-back period liability of $84,000 or more. Payment by EFT to Treasurer of State Payment is due within 3 banking days after the end of the partial weekly period. Tues. ---> due Fri Fri. ---> due Wed. Reports: Quarterly IT 942 (OBG) 4th Qtr/Annual IT 942 (OBG) 42

filer: Look-back period liability of $84,000 or more. Payment by EFT to Treasurer of State. Payment is due within 3 banking days after the end of the partial weekly period. Tues. ---> due Fri. Fri. ---> due Wed. Reports: Quarterly IT 942 (OBG) 4th Qtr/Annual IT 942 (OBG) 42.")

44

Employer Withholding – Filing/Payment

Monthly. Look-back period liability of more than $2,000 but less than $84,000. Return and payment are due by the 15th day following the end of each month. Quarterly. Look-back period liability of $2,000 or less. Return and payment are due by the end of the subsequent month following the end of the quarter. Reports: IT 501 (OBG or paper) Annual IT 941 (OBG or paper) 44

Annual IT 941 (OBG or paper) 44.")

46

Employer Withholding – Reconciliation

Reconciliation return: Form IT 941, Annual Reconciliation or Form IT 942, 4th Quarter/Annual (EFT filers only) Due: by January 31st Any refund should be requested on the applicable annual return or amended return. Annual form IT 942: make sure that you show the total withholding for the year. Form WT AR, Withholding Tax Application for Refund, should generally be used to file only for refunds of payments made or applied to an Assessment. 46

Due: by January 31st. Any refund should be requested on the applicable annual return or amended return. Annual form IT 942: make sure that you show the total withholding for the year. Form WT AR, Withholding Tax Application for Refund, should generally be used to file only for refunds of payments made or applied to an Assessment. 46.")

47

47

48

48

49

49

50

Reporting year is the calendar year.

50

51

Enter the Ohio gross payroll and state tax withholding amounts for each month during the calendar year. Quarterly filer would indicate wages and tax for periods 51

52

Enter the amount of state tax paid on previously filed forms IT 501

Enter the amount of state tax paid on previously filed forms IT If overpaid, then you can request a refund of the overpayment on this return. If you select credit, be sure to reduce the tax due on your first 501 report of the subsequent year. 52

53

53

54

54

55

55

56

56

57

57

59

School District Withholding

Every employer, including the state and its political subdivisions, is required to withhold Ohio school district income tax from compensation paid to employees who reside in a school district that has enacted a tax. Ballot issue approved by voters residing in the district. Generally in effect for 5 years or CPT (continuing period of time) Increments of 0.25% Important: Tax is assessed based on residency of employee; employee residing in a taxing district Statute: ORC Chapter 5748 and

Increments of 0.25% Important: Tax is assessed based on residency of employee; employee residing in a taxing district. Statute: ORC Chapter 5748 and")

60

School District Withholding

Two tax bases: Traditional & Earned Income Traditional: Starts with Ohio Taxable Income (Line 5 of Ohio IT-1040) Includes earned income, retirement, capital gains, etc. Excludes items deducted on line 2 of the IT-1040 e.g. Social Security benefits, Federal interest & dividends, disability benefits) Includes deduction for personal exemptions Earned Income: Earned income only e.g. Wages, Salaries, Tips, Self Employment income No deduction for personal exemptions

Includes earned income, retirement, capital gains, etc. Excludes items deducted on line 2 of the IT e.g. Social Security benefits, Federal interest & dividends, disability benefits) Includes deduction for personal exemptions. Earned Income: Earned income only. e.g. Wages, Salaries, Tips, Self Employment income. No deduction for personal exemptions.")

61

School District Withholding

Traditional: Includes deduction for personal exemptions Deduct $650 annually for each personal exemption, pro-rated over the full calendar year, and multiply the remaining wages by the tax rate for the district. Example (bi-weekly payroll): deduct $25 for each personal exemption claimed ($650 divided by 26 pay periods = $25). Earned Income: No deduction for personal exemption. Withhold at tax rate for the applicable district. 61

: deduct $25 for each personal exemption claimed ($650 divided by 26 pay periods = $25). Earned Income: No deduction for personal exemption. Withhold at tax rate for the applicable district. 61.")

63

School District Withholding

School District Withholding (use of Form IT 4) ORC (E) – To ensure that taxes imposed pursuant to Chapter 5748 of the Revised Code are deducted and withheld as provided in this section: (1) Each employer shall request that each of his employees furnish the name of the employee's school district of residence; (2) Each employee shall furnish his employer with sufficient and correct information to enable the employer to withhold the taxes imposed under Chapter of the Revised Code. The employee shall provide additional or corrected information whenever information previously provided by him to his employer becomes insufficient or incorrect. (3) If the employer complies with the requirements of division (E)(1) of this section and if the employee fails to comply with the requirements of division (E)(2) of this section, the employer is not required to withhold and pay the taxes imposed under Chapter of the Revised Code and is not subject to any penalties and interest otherwise applicable for failing to deduct and withhold such taxes. E) To ensure that taxes imposed pursuant to Chapter of the Revised Code are deducted and withheld as provided in this section: School district withholding requirements: (1) Each employer shall request that each of his employees furnish the name of the employee's school district of residence; (2) Each employee shall furnish his employer with sufficient and correct information to enable the employer to withhold the taxes imposed under Chapter of the Revised Code. The employee shall provide additional or corrected information whenever information previously provided by him to his employer becomes insufficient or incorrect. *** TC Opinion, withhold if employee provides SD name or SD number. Example: Fairborn, or #2903 (employer has sufficient information to withhold tax) (3) If the employer complies with the requirements of division (E)(1) of this section and if the employee fails to comply with the requirements of division (E)(2) of this section, the employer is not required to withhold and pay the taxes imposed under Chapter of the Revised Code and is not subject to any penalties and interest otherwise applicable for failing to deduct and withhold such taxes. 63

ORC (E) – To ensure that taxes imposed pursuant to Chapter 5748 of the Revised Code are deducted and withheld as provided in this section: (1) Each employer shall request that each of his employees furnish the name of the employee s school district of residence; (2) Each employee shall furnish his employer with sufficient and correct information to enable the employer to withhold the taxes imposed under Chapter of the Revised Code. The employee shall provide additional or corrected information whenever information previously provided by him to his employer becomes insufficient or incorrect. (3) If the employer complies with the requirements of division (E)(1) of this section and if the employee fails to comply with the requirements of division (E)(2) of this section, the employer is not required to withhold and pay the taxes imposed under Chapter of the Revised Code and is not subject to any penalties and interest otherwise applicable for failing to deduct and withhold such taxes. E) To ensure that taxes imposed pursuant to Chapter of the Revised Code are deducted and withheld as provided in this section: School district withholding requirements: (1) Each employer shall request that each of his employees furnish the name of the employee s school district of residence; (2) Each employee shall furnish his employer with sufficient and correct information to enable the employer to withhold the taxes imposed under Chapter of the Revised Code. The employee shall provide additional or corrected information whenever information previously provided by him to his employer becomes insufficient or incorrect. *** TC Opinion, withhold if employee provides SD name or SD number. Example: Fairborn, or #2903 (employer has sufficient information to withhold tax) (3) If the employer complies with the requirements of division (E)(1) of this section and if the employee fails to comply with the requirements of division (E)(2) of this section, the employer is not required to withhold and pay the taxes imposed under Chapter of the Revised Code and is not subject to any penalties and interest otherwise applicable for failing to deduct and withhold such taxes. 63.")

64

School District Withholding

Filing frequency/status is based on the Ohio withholding frequency, which is either: Monthly (Partial weekly or monthly), or Quarterly File/Pay with Form SD 101. Only means to file/pay electronically is through the Ohio Business Gateway. 64

, or. Quarterly. File/Pay with Form SD 101. Only means to file/pay electronically is through the Ohio Business Gateway. 64.")

67

Select the districts you want to add by clicking on the letter to display the list, then click on the SD you want to add and click on >

68

Wyoming #3122 now displays on “your list”

69

Now add Troy #5509

70

Troy #5509 now displays on “your list”

71

The districts on “your list” will be saved for future periods

The districts on “your list” will be saved for future periods. If you want to add/delete districts, click on ‘Modify School District’ Enter the tax amounts and click ‘Next.’

72

Click on ‘back’ to change the data. Click on ‘accept data’ if correct.

75

School District Withholding

SDIT Overpayments (during the year): Q: How do I handle overpayments made during the year? A: Apply the overpayment to your next SD 101 return. The overpayment must be applied against the tax due for the same district, but do not reduce the tax due below zero. Example: Assume you overpaid Fairborn #2509 by $70 on the January SD 101 report. You then withhold $50 in Fairborn #2509 tax for each month February and March. Outcome: Feb. and March’s SD 101 reports will show $0.00 and $30 due for SD #2509, respectively. 75

: Q: How do I handle overpayments made during the year A: Apply the overpayment to your next SD 101 return. The overpayment must be applied against the tax due for the same district, but do not reduce the tax due below zero. Example: Assume you overpaid Fairborn #2509 by $70 on the January SD 101 report. You then withhold $50 in Fairborn #2509 tax for each month February and March. Outcome: Feb. and March’s SD 101 reports will show $0.00 and $30 due for SD #2509, respectively. 75.")

76

School District Withholding

SDIT refunds: Q: How do I handle overpayments at year-end? All refunds are requested on: Form SD141, Annual Reconciliation, or Form SD141X, Amended Reconciliation An overpayment not used to reduce the tax due for the same district during the year can be used to offset any tax due for another district at year-end on SD 141. Form WT AR, Withholding Tax Application for Refund, should generally be used to only file for refunds of payments made/applied to Illegal or erroneous assessments. Note: SDWH refunds of erroneous payments made during the year (monthly or quarterly) should not be credited from one district to another separate district. Use overpayments to reduce SD withholding tax due for the same district on a subsequent period within the same calendar year. SD refunds: At the end of the year, any overpayments not used to reduce the tax due for the same district during the year, can then be refunded or credited on to another district. 76

should not be credited from one district to another separate district. Use overpayments to reduce SD withholding tax due for the same district on a subsequent period within the same calendar year. SD refunds: At the end of the year, any overpayments not used to reduce the tax due for the same district during the year, can then be refunded or credited on to another district. 76.")

77

77

79

Enter tax withheld and previous payments only (Do not enter wages)

")

82

Employer Withholding – Forms W2

W2 filing: Due by 2/28 of subsequent year Send with form IT 3 - Wage & Tax Transmittal (paper form) 250 or more forms must use media (CD) with proper layout W-2s on CD using SSA format EFW2 1099-R on CD using IRS Publication 1220 format Important: Not required to send paper W-2 forms. W-2 reporting is required. Statutory reference is (F), which requires the following to be filed with the employer’s annual report: The full name of each employee, the employee’s address, the employee’s school district of residence and the in the case of a nonresident, the employee’s principal county of employment: The social security number of each employee; The total amount of compensation paid to each employee before any deductions; The amount of tax imposed by and Chapter 5748 withheld from compensation. 82

250 or more forms must use media (CD) with proper layout. W-2s on CD using SSA format EFW R on CD using IRS Publication 1220 format. Important: Not required to send paper W-2 forms. W-2 reporting is required. Statutory reference is (F), which requires the following to be filed with the employer’s annual report: The full name of each employee, the employee’s address, the employee’s school district of residence and the in the case of a nonresident, the employee’s principal county of employment: The social security number of each employee; The total amount of compensation paid to each employee before any deductions; The amount of tax imposed by and Chapter 5748 withheld from compensation. 82.")

83

Employer Withholding – Forms W2

Box 1 (Wages, tips, other compensation) and Box 16 (state wages) should be the same amounts. School district taxes enter in box 14 or boxes 19 and 20. Be sure to show tax withheld and identify SD by the 4 digit code: e.g. $ #3122 Instructions for IT 3 Box 1 and box 16 should be the same amounts. Only exception is if employee worked in various states, exclusive of neighboring states. Show SD withholding in boxes 18 through 20 or use box 14 (Other). 83

and Box 16 (state wages) should be. the same amounts. School district taxes enter in box 14 or boxes 19 and 20. Be sure to show tax withheld and identify SD by the 4 digit code: e.g. $ #3122. Instructions for IT 3. Box 1 and box 16 should be the same amounts. Only exception is if employee worked in various states, exclusive of neighboring states. Show SD withholding in boxes 18 through 20 or use box 14 (Other). 83.")

84

Employer and School District Withholding (Employee Payroll)

Send in your completed form IT 3 even if not sending forms W-2 on CD media. 84

85

Employer Withholding – W2 filing

W2 Corrections: Follow Federal Guidelines Use Federal form W-2C or amend W-2 copy and type “Corrected by Employer” Send one copy of each corrected W-2 to Taxation with the amended IT-3 Do not send corrections on media 85

86

Employer Withholding – Maintain Records

Retain for at least 4 years: Names, addresses, school district of residence, and SSNs of all employees (forms IT-4) Periods of Employment Amounts and dates of compensation Amount of compensation paid by payroll period: i.e. payroll registers, earnings cards Annual returns filed with Taxation Statutory Reference: R.C 86

Periods of Employment. Amounts and dates of compensation. Amount of compensation paid by payroll period: i.e. payroll registers, earnings cards. Annual returns filed with Taxation. Statutory Reference: R.C")

87

Interest and/or Penalty

Apply to both employer withholding taxes. Interest: Mandatory on late payments. Interest rate is 3% for 2012 Penalties: Late Payment: Two times the interest plus 10% of tax. Late Filing: Greater of: $50 per month (up to $500) or 5% (up to 50%) of the tax due. Non-Payment: 50% of the tax due on the return. Statutory Reference: R.C (F)(5) and R.C 87

or 5% (up to 50%) of the tax due. Non-Payment: 50% of the tax due on the return. Statutory Reference: R.C (F)(5) and R.C")

88

Employer Withholding – Assessments

Personal Liability of Responsible Party “An employee…having control or supervision of or charged with the responsibility of filing the report and making payment…or an officer, member, manager or trustee…responsible for the execution of the…(entity’s) fiscal responsibility, shall be personally liable for failure to file the report or pay the tax due.” Responsible party liability holds even if the business is closed, files bankruptcy or is dissolved. Statutory Reference: R.C (G); Amplified by OAC 88

fiscal responsibility, shall be personally liable for failure to file the report or pay the tax due. Responsible party liability holds even if the business is closed, files bankruptcy or is dissolved. Statutory Reference: R.C (G); Amplified by OAC")

89

Business Tax Division/Withholding Unit Contact Information Richard Six, Assistant Administrator Phone (614) TPS Phone: Fax: Website: Location Address: 4485 Northland Ridge Blvd. Columbus, OH Mailing Address: P.O. Box 2476 Columbus, OH 89

90

Questions

91

Sales & Use Tax Basics Phyllis Shambaugh

Counsel, Sales & Use Tax Division Ohio Department of Taxation

92

History of Sales & Use Tax

Sales tax enacted effective 1/1/1935 (ORC Chapter 5739) Companion use tax enacted effective 1/1/1936 (ORC Chapter 5741) Creates a level playing field for in-state and out-of-state vendors All states that have a sales tax also have a use tax

Companion use tax enacted. effective 1/1/1936 (ORC Chapter 5741) Creates a level playing field. for in-state and out-of-state vendors. All states that have a sales tax. also have a use tax.")

93

What Is Taxable? All sales of tangible personal property are taxable, unless there is a specific exemption - Furnishing of lodging by a hotel is taxable Only those services specifically identified in ORC (B) are taxable Use tax is imposed on the storage, use or other consumption of tangible personal property and taxable services in Ohio

are taxable. Use tax is imposed on the storage, use or other consumption of tangible personal property and taxable services in Ohio.")

94

What Sales Are Exempt? Purchase for resale

Property used in manufacturing, mining or agriculture Sales of some utilities (natural gas, water and electricity) Food for consumption off-premises Prescription drugs Motor fuel Newspaper and magazine subscriptions

Food for consumption off-premises. Prescription drugs. Motor fuel. Newspaper and magazine subscriptions.")

95

Who Is Liable for the Tax?

Imposed on the consumer, but Ohio vendor is required to collect it at time of sale If tax is not collected by the vendor, then the consumer must self-assess use tax

96

Who Is a Vendor? Person providing the service or transferring the tangible personal property Required to register with Taxation (vendor’s license) Must collect sales tax from the customer at the time of sale Must remit sales tax to Taxation

Must collect sales tax from the customer. at the time of sale. Must remit sales tax to Taxation.")

97

Who Is a Consumer? Person who purchases the taxable tangible personal property or receives the taxable service

98

What Is Included in Price?

Price for calculating the sales or use tax is the total consideration received, including cash, credit and property and includes: All of vendor’s costs including materials, labor & service charges Delivery charges Installation charges Other services necessary to complete the sale Trade-in allowance (Note: A trade-in allowance on the purchase of a new motor vehicle, new watercraft, or new outboard motor is not included in the price.)

")

99

Presumptions If consumer claims purchase is exempt, vendor must obtain a fully completed exemption certificate within 90 days of the date of the sale If vendor obtains exemption certificate, vendor is relieved of liability for sales tax on that purchase

100

Use Tax Basics Some out-of-state vendors are not required to collect Ohio sales tax, making it cheaper to purchase from an out-of-state vendor Use tax corrects this disparity Consumer who does not pay sales tax on tangible personal property or taxable services used in Ohio must pay the use tax

101

Consumer’s Use Tax Amnesty

Began 10/1/2011; runs through 5/1/2013 Emphasis is on educating consumers Consumers who come forward are required to pay consumer’s use tax due and not paid on purchases made on or after 1/1/ Interest and penalty is waived All consumer’s use tax liability on purchases made prior to 1/1/2009 is forgiven

102

Consumer’s Use Tax Amnesty

Consumers not registered for use tax as of 6/1/2011 are eligible for a no-interest payment plan with a term of up to 7 years Consumers are required to continue to report and remit consumer’s use tax on an ongoing basis

103

Questions

104

Commercial Activity Tax

Chuck Willis Assistant Administrator Ohio Department of Taxation

105

Commercial Activity Tax (CAT)

The CAT is a tax on the privilege of doing business in Ohio The CAT is measured by gross receipts Can not deduct cost of goods sold or other expenses All types of entities are subject to the CAT

106

What are Gross Receipts?

Includes sales, services, and rentals or leases – R.C (F)(1) lists what is included in gross receipts R.C (F)(2) lists the exclusions from gross receipts R.C (F)(2)(hh) is the exclusion for casinos to pay CAT only on the amounts in excess of the gross casino revenue for casino gaming. Gross casino revenue is defined in R.C (D)

(1) lists what is included in gross receipts. R.C (F)(2) lists the exclusions from gross receipts. R.C (F)(2)(hh) is the exclusion for casinos to pay CAT only on the amounts in excess of the gross casino revenue for casino gaming. Gross casino revenue is defined in R.C (D)")

107

What are Gross Receipts?

Other gross receipts would be food and drink sales, merchandise sales, etc Items that are given (complimentary) to patrons are considered gross receipts at the fair market value of the items

to patrons are considered gross receipts at the fair market value of the items.")

108

Tax Rate An annual minimum tax of $150 is paid in the 1st quarter of each year. Taxpayers receive a $1 million dollar exclusion per calendar year, $250,000 per quarter. Taxable gross receipts in excess of the quarterly exclusion are taxed at the rate of .26% (.0026)

")

109

Dues Dates of Returns Quarterly returns are due as follows:

1st quarter (Jan. 1 to Mar. 31) is due May 10 2nd quarter (Apr. 1 to June 30) is due Aug. 10 3rd quarter (July 1 to Sept. 30) is due Nov. 10 4th quarter (Oct. 1 to Dec. 31) is due Feb. 10 Quarterly filers must file and pay electronically using the Ohio Business Gateway

is due May 10. 2nd quarter (Apr. 1 to June 30) is due Aug rd quarter (July 1 to Sept. 30) is due Nov th quarter (Oct. 1 to Dec. 31) is due Feb. 10. Quarterly filers must file and pay electronically using the Ohio Business Gateway.")

110

Filing and Paying CAT Returns on the

Ohio Business Gateway

114

This is an informational page for the taxpayer to read

This is an informational page for the taxpayer to read. Click next button at the bottom of the page.

115

Select reporting period and type of return from the dropdowns and click next button at the bottom of the page.

116

Click next when complete.

Taxpayer must enter taxable gross receipts on line 3 (as shown with arrow) the rest will calculate. Note: Do NOT use commas or decimals. Taxpayer has ability to enter an unused exclusion, CCF, or non-refundable and refundable credits manually by checking override. Click next when complete.

the rest will calculate. Note: Do NOT use commas or decimals. Taxpayer has ability to enter an unused exclusion, CCF, or non-refundable and refundable credits manually by checking override. Click next when complete.")

118

How

119

When

121

How Much

122

This “Edit” button is used to change the payment options associated with the report

123

1 2

124

Enter bank information.

126

This page can be re-created from the history screen

127

Making a deferred payment on OBG

130

Taxpayer can enter date in field or use calendar to select date

Taxpayer can enter date in field or use calendar to select date. Date can not be past the due date.

132

1 2

133

This “Edit” button is used to change the payment options associated with the report

134

1 2

137

This page can be re-created from the history area

138

Viewing History of Returns and Payments made on the OBG

139

To find a report that has already been filed on OBG, select the “History” link

140

To find a specific report, you can search by “Service Area,” “Filing Date Range,” or by OBG Confirmation Number When you have found a specific report that you want to review, select the “View Receipt” button beside the report.

141

To view the actual report, select the “View” button.

The Transaction Confirmation and Receipt shows what you filed, when you filed and associated payment information. To view the actual report, select the “View” button.

143

You may navigate from this page using the links on top or by using the “Home” button on the bottom of the page.

144

CAT Contact Information Chuck Willis, Assistant Administrator Phone Phone: Fax: Website: tax.ohio.gov Address: Commercial Activity Tax Division P.O. Box 16158 Columbus, OH

145

Automatic E-Mail Notification

Subscribe to the Department’s tax practitioner ing list. Click on ODT web site at: Tax.Ohio.Gov

146

Questions

Similar presentations