Download presentation

Presentation is loading. Please wait.

1

An Introduction to Accounting Courtesy: Dr Gagan Pareek

2

Dr Gagan Pareek alias Dr Harish Pareek M.Com, A.I.C.W.A, PhD

Area of Expertise : Accounting & Finance, Credit Risk Management Strategic Management Corporate Trainer & Key Resource Person : In the area of Finance and Strategy, Leadership, Team Building and Motivation ; Mobile: Research: Awarded PhD degree on “Operation of NBFCs in India- a changing profile “ in the Dept of Commerce, Calcutta University. Industry Exp: Having 12 years of experience in the area of accounting and finance, credit and risk analysis. Worked for companies like Kesoram Industries Ltd (B.K. Birla Group of Companies), UTI-ISL, Magma Fincorp Ltd. He has also been associated with academic research for the last 9 years.

, UTI-ISL, Magma Fincorp Ltd. He has also been associated with academic research for the last 9 years.")

3

Accounting It enables a person to ascertain accurately and with little trouble as possible The amount he has gained or lost in the business during a given period The amount of his assets, liabilities and capital on any particular date. How the amount he has gained or lost is made up. What amount is owing to him by each of his customers or debtors. What amount is owing by him to each of his creditors. What is his liability for payment of taxes to Govt. How his business stands in comparison to other similar business.

4

Accounting is a must…… for

Capital Maintenance Productive Capital Profitable Operations

5

Accounting World Events/Actions affecting the business

Rules /Management Decisions Financial Statements

6

Events/Actions affecting the business

Accounting World Financial Accounting translates events into financial statements General Accepted Accounting Principles Events/Actions affecting the business Rules / Management Decisions Selection of different alternatives rules on the basis of GAAP Financial Statements

7

Users of Accounting Information

Investors Government Community Board of Directors Management Employees Analysts Suppliers Employees Customers Creditors

8

Double Entry Double entry is the only system of book keeping by the employment of which all the objectives of accounting can be achieved. It enable the businessmen to obtain the permanent record of his dealings with those with whom he transacts his business, and of the exact state of relationship with each of those individuals at any given date. It further helps him to ascertain whether the result of his transactions has been profitable or otherwise, and what his exact financial position is at any time

9

Assets Probable future economic benefits What a business “owns”

Examples Cash Investments Buildings Plant and machinery Patents and copyrights

10

Liabilities Probable future sacrifices of economic benefits

What a business “owes” Contractual, statutory, or constructive Examples Loans payable Warranty obligations Pensions payable Income tax payable

11

Equity Residual interest of owners Examples Share capital

Share premium Revenues Expenses Dividends Retained profit

12

Financial Statements Profit and loss account

Statement of financial performance Balance sheet Statement of financial position Statement of cash flows Statement of cash receipts and cash payments

13

Types of Account Personal Account: These accounts record a traders dealings with other persons, firms or companies. A separate account is kept for each person, firm or company from whom goods have been purchased or to whom goods have been sold on credit, so that the amount owing to and by the trader can be readily ascertained at any time.

14

Real Account These accounts record dealings in or with property, assets or possessions. A separate account is kept for each class of property such as cash, stock in trade, plant &machinery, furniture etc, so that by recording therein particulars of each such assets received or given away, the trader can ascertain the value of each asset on hand on any particular date.

15

Nominal Account These accounts record a trader’s expenses or gains.

A separate account is opened for each head of expenditure or income, such as rent, salaries, wages, printing, stationery, cartage, interest, discount, commission etc, so that the trader can see the amount expended lost or gained under each heading. Each such account is debited when an expense is incurred and is credited when there is any gain.

16

Rules of Debits and Credits: Golden Rule

Personal Accounts- Debit the receiver , and credit the giver Real Accounts- Debit what comes in, and credit what goes out. Nominal Accounts-Debit expenses and losses, and credit gains.

17

Ledger The ledger is the chief books of accounts, and it is in this book that all the business transactions would ultimately find their place under their respective accounts in a duly classified form. The process of transferring the transactions which have been previously recorded in the Journal into the appropriate accounts in the Ledger is called POSTING. The debit aspects of the transactions as entered in the debit column of the Journal are posted to the debit side of the Ledger Accounts concerned, while the credit aspects are entered on the credit side.

18

Balancing of Account The difference between the debit total and the credit total in any account is called the balance. If the debit total is larger, the balance is a debit balance. This balance will be placed on the credit side to make the two side equal, and will be again brought down on the debit side, after closing the account. If the credit total is heavier, the balance is a credit balance. This balance will be placed on the debit side to make the two sides equal, and will be again brought down on the credit side after closing the account.

19

Debit and Credit Entries

Receipts of cash are on the debit side. Payments of cash are on the credit side. The difference between the debit total and the credit total is called the balancing figure

20

Entries Types Opening Entries Transfer from one account to another

Rectification of errors Adjustment Entries Closing Entries

21

Accounting Concepts Entity Concept Dual Aspect Concept

Going Concern Concept Periodicity Concept Money Measurement Concept Revenue Recognition Concept Matching Concept Accrual Concept

22

Entity Concept The business is treated as a unit or entity apart from its owners, creditors and others. The proprietor of an enterprise is always considered to be separate and distinct from the business which he controls. The proprietor is treated as a creditor to the extent of his capital.

23

E.g. If there is purchase of goods- it involves two aspects:

Dual Aspect Concept In each transaction there are two aspects to be recorded from the point of view of entity. E.g. If there is purchase of goods- it involves two aspects: One aspect is the receipt of goods The other aspect is the immediate payment of cash(in case of cash purchase) or the acknowledgment of the debt to the supplier (in case of credit purchases). The recognition of two aspects of every transactions is known as dual aspect

or the acknowledgment of the debt to the supplier (in case of credit purchases). The recognition of two aspects of every transactions is known as dual aspect.")

24

Going Concern Concept This concept assumes the enterprise will continue to exist in the foreseeable future. It is assumed that the enterprise has neither the intention nor the necessity of liquidation or of curtailing materially the scale of its operation.

25

Accounting Period Concept

Time duration for which the income/loss is measured is called the accounting period . Under the Companies Act, and Banking Regulation Act, financial statements are to be prepared for a twelve month period.

26

Money Measurement Concept

It underlines that the fact that in accounting, every worth recording event, happening or transactions is recorded in terms of money.

27

Cost Concept The underlying idea of cost concept is that:

Asset is recorded at the price paid to acquire it, that is, at cost, and This cost is the basis for all subsequent accounting for that asset. The cost concept also implies that if nothing has been paid for acquiring something then it would not be shown in the accounting books as an asset.

28

Revenue Recognition Concept

At what stage the revenue should be recognized and recorded. If we take for instance of sale of goods, there are several stages like the receipt of order from the customer, the production of goods after the receipt of order delivering the goods to the customer & invoicing receipt of cash from the customer. Usually, enterprise dispatch the goods to the customer and an invoice is simultaneously made out. At this stage sale is recorded.

29

Matching Concept After the revenue recognition, all costs, which are applicable to the revenue of the period, should be charged against that revenue in order to determine the net income of the business.

30

Accrual Concept Revenue recognition depends on its realisation and not on actual receipt, likewise costs are recognised when they are incurred and not when they are paid. In relation to revenue, the amount should exclude amount relating to subsequent period and provide for revenue recognised but not received in cash. In relation to costs, the accounts should provide for costs incurred but not paid and exclude costs paid for subsequent periods.

31

Objectivity Concept All accounting must be based on objective evidence. The transaction records should be supported by verifiable documents.

32

Accounting Conventions 1

Accounting Conventions 1.Conservatism: “Anticipate no profit but provide for all possible losses”. In other words the policy of playing safe. The inventory is valued at “cost or market price which ever is less”. Similarly a provision is made for possible bad and doubtful debts out of current years profits.

33

2.Full Disclosure: Accounting reports should disclose fully and fairly the information they purport to represent. They should be honestly prepared and sufficiently disclose information which is of material interest to shareholders, present and potential creditors and investors.

34

3.Consistency : Accounting practices should remain unchanged from one period to another. For example , if stock is valued at “cost or market price whichever is less”, this principle should be followed year after year. Necessary for the purposes of comparison. Does not forbid introduction of improved accounting techniques. However, if adoption of such a technique results in inflating or deflating the figures of profit as compared to the previous years, a note to the effect should be given in the financial statements.

35

4.Materiality: Material details to be provided and ignore insufficient details. This is because otherwise accounting will be unnecessarily overburdened with minute details.

36

Accounting Standards-setting Organization in Selected Countries

Country Policy Setting Board Australia Australian Accounting Standards Board (AASB) sets GAAP Canada Canadian Accounting Standards Board (CASB) of the Canada Institute of Chartered Accountants (CICA) sets GAAP India Accounting Standards Board (ASB) of the Institute of Chartered Accountants of India (ICAI) is the body entrusted with the work of preparing the standards. U.K. Accounting Standards Board (ASB) is comprised of nine members drawn from different user groups. U.S.A. Financial Accounting Standards Board (FASB) is the body solely in charge of issuing standards.

sets GAAP. Canada. Canadian Accounting Standards Board (CASB) of the Canada Institute of Chartered Accountants (CICA) sets GAAP. India. Accounting Standards Board (ASB) of the Institute of Chartered Accountants of India (ICAI) is the body entrusted with the work of preparing the standards. U.K. Accounting Standards Board (ASB) is comprised of nine members drawn from different user groups. U.S.A. Financial Accounting Standards Board (FASB) is the body solely in charge of issuing standards.")

37

TRANSACTION (a) Dr. X starts a Medical Health Care Unit, by investing Rs50,000 in his practice.

38

Dr. X invests Rs50,000 to start a Medical Health Unit

Cash Flows Income Statement Balance Sheet Assets = Liabilities Equity Cash = + Capital Invested 50,000 Financing 50,000

39

TRANSACTION (b) Medical Health Care Unit , borrows Rs20,000 to finance the practice.

40

Receipt of Loan Assets = Liabilities + Equity Cash = Loan Capital Bal

Cash Flows Income Statement Balance Sheet Assets = Liabilities Equity Cash = Loan Capital Bal 50,000 20, = 20,000 70, = 20, Financing 20,000

41

TRANSACTION (c) Medical Health Care Unit, bought Equipments worth Rs 10,000/=for practice.

42

Bought Equipments for Rs 10,000

Cash Flows Income Statement Balance Sheet Assets = Liabilities Equity Cash Equipment = Loan Capital Balance 70,000 20,000 50,000 Equipments -10, ,000 60, , = 20, Equipments -10,000

43

TRANSACTION (d) Family Health Care, received fees for providing services to patients.

44

Receipt of Fees Assets = Liabilities + Equity Cash + Equipment =

Cash Flows Income Statement Balance Sheet Assets = Liabilities Equity Cash + Equipment = Loan Capital+ Revenue Balance 60, , = 20, 50,000 Fees 15, = 15,000 75, , = 50, ,000 Fees Earned ,000 Fees(cash) 15,000

15,")

45

TRANSACTION (e) Medical Health Care Unit paid wages, rent, electricity bills, interest and miscellaneous expenses.

46

Paid monthly expenses Assets = Liabilities + Equity

Cash Flows Income Statement Balance Sheet Assets = Liabilities Equity Cash + Equipments = Loan Capital + Revenue Balance , = 20, 50, ,000 Expenses -9,000 66, , = 5, ,000 Wages ,000 Rent ,000 Electricity ,000 Interest Misc Total ,000 Operating -9,000

47

TRANSACTION (f) Family Health Care, paid a dividend to Dr. X.

48

Paid Dividend Assets = Liabilities + Equity Cash + Equipments = Loan +

Cash Flows Income Statement Balance Sheet Assets = Liabilities Equity Cash Equipments = Loan Capital + Revenue Balance 66, , = 20, 50, ,000 Dividend -2,000 - 2,000 64, , = 50, ,000 Financing –2,000

49

Integrated Financial Statement Framework

Cash Flows Income Statement Balance Sheet Assets = Liabilities Equity Cash + Equipment = Loan Capital + Revenue Invested 50,000 + Loan 20, = 20,000 Land -10, ,000 Fees 15, = 15,000 Expenses -9,000 9,000 Dividend -2,000 Balance 64, , = 20, 50, ,000

50

The effect of Debits and Credits on an account are as follows

Debit and Credit Rules The effect of Debits and Credits on an account are as follows A = L + OE ASSETS Debit for Increase Credit for Decrease LIABILITIES Debit for Decrease Credit for Increase EQUITIES Debit for Decrease Credit for Increase 13

51

Double Entry AccountingThe Equality of Debits and Credits

A = L + OE = Debit balances Credit balances Every transaction is recorded by equal amounts of debits and credits. 13

52

The Account Left side of an account is the “Debit” side

An account is a summarized record of the transactions affecting one person, one kind of property or one class of gains or losses Left side of an account is the “Debit” side Right side of an account is the “Credit” side Account T- Form Account

53

Debits and Credits Double-entry accounting system

Each transaction must affect two or more accounts to keep the basic accounting equation in balance. Recording done by debiting at least one account and crediting another. DEBITS must equal CREDITS.

54

Debits and Credits Transaction #1 Rs10,000 Rs3,000 Transaction #2

If Debits are greater than Credits, the account will have a debit balance. Transaction #1 Rs10,000 Rs3,000 Transaction #2 Transaction #3 8,000 Balance Rs15,000

55

Debits and Credits Transaction #1 Rs10,000 Rs3,000 Transaction #2

If Debits are greater than Credits, the account will have a debit balance. Transaction #1 Rs10,000 Rs3,000 Transaction #2 8,000 Transaction #3 Balance Rs1,000

56

Debits and Credits Summary

Normal Balance Debit Normal Balance Credit

57

Debits and Credits Summary

Balance Sheet Income Statement Asset = Liability + Equity Revenue - Expense = Debit Credit

58

Debits and Credits Summary

Review Question Debits: increase both assets and liabilities. decrease both assets and liabilities. increase assets and decrease liabilities. decrease assets and increase liabilities.

59

Debits and Credits Summary

Discussion Question X, a beginning accounting student, believes debit balances are favorable and credit balances are unfavorable. Is X correct? Discuss. X is incorrect. A debit balance only means that debits amounts exceed credit amounts in an account. Conversely, a credit balance only means that credit amounts are greater than debit amounts in an account. Thus, a debit or credit balance is neither favorable nor unfavorable.

60

Assets and Liabilities

Assets - Debits should exceed credits. Liabilities – Credits should exceed debits. The normal balance is on the increase side.

61

Owner’s Equity Owner’s investments and revenues increase owner’s equity (credit). Owner’s drawings and expenses decrease owner’s equity (debit).

62

Revenue and Expenses The purpose of earning revenues is to benefit the owner(s). The effect of debits and credits on revenue accounts is the same as their effect on Owner’s Capital. Expenses have the opposite effect: expenses decrease owner’s equity.

63

Debits and Credits Summary

Review Question Accounts that normally have debit balances are: assets, expenses, and revenues. assets, expenses, and owner’s capital. assets, liabilities, and owner’s drawings. assets, owner’s drawings, and expenses.

64

Journalizing Oct. 1 In the Books of X Journal

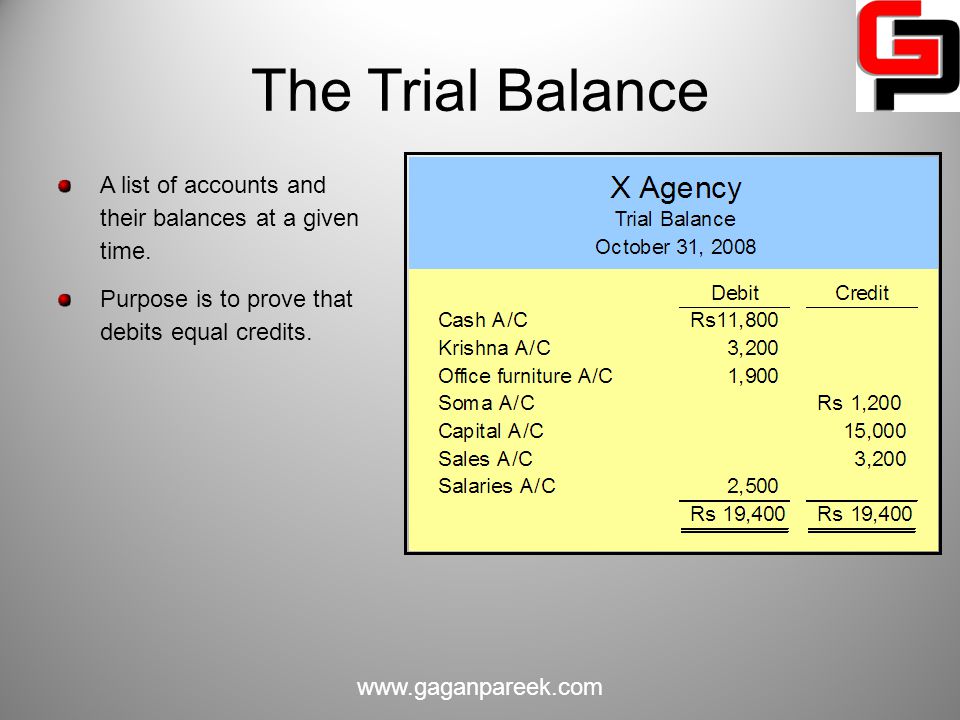

E2-4 (Facts) Presented below is information related to X Agency. X begins business as a merchandiser with a cash investment of Rs15,000. Oct. 1 In the Books of X Journal

Presented below is information related to X Agency. X begins business as a merchandiser with a cash investment of Rs15,000. Oct. 1. In the Books of X. Journal.")

65

THE RECORDING PROCESS

66

The Recording Process The Account Steps in the Recording Process

The Trial Balance Debits and credits Expansion of basic equation Locating errors Recording of Journal Entries Ledger Posting Balancing of Accounts

67

The Journal Book of original entry (General Ledger).

Transactions recorded in chronological order. Contributions to the recording process: Discloses the complete effects of a transaction. Provides a chronological record of transactions. Helps to prevent or locate errors because the debit and credit amounts can be easily compared.

68

Journalizing Journalizing - Entering transaction data in the journal.

Presented below is information related to X Agency. Oct. 1 X begins business as a merchandiser with a cash investment of Rs15,000. 3 Purchases office furniture for Rs1,900, on account from Soma. 6 Sold goods to Krishna; bills Krishna Rs3,200 . 27 Pays Rs700 on balance related to transaction of Oct. 3. 30 Pays the administrative assistant Rs2,500 salary for Oct. Journalize the transactions

69

Journalizing Oct. 3 General Journal

Purchases office furniture for Rs1,900, on account from Soma. General Journal

70

Journalizing Oct. 6 General Journal

Sold goods to Krishna; bills Krishna Rs3,200. General Journal

71

Journalizing Oct. 27 General Journal

Pays Rs700 on balance related to transaction of Oct. 3. General Journal

72

Journalizing Oct. 30 General Journal

Pays the administrative assistant Rs2,500 salary for Oct. General Journal

73

Journalizing Simple Entry – Two accounts, one debit and one credit.

Compound Entry – Three or more accounts. Example – On June 15,purchased equipment from UV Ltd for Rs15,000 by paying cash of Rs10,000 and the balance on account (to be paid within 30 days) General Journal

General Journal.")

74

The ledger Ledger contains the entire group of accounts maintained by a company. A general ledger contains all the asset, liability, owner’s equity, revenue, and expense accounts. Chart of Accounts

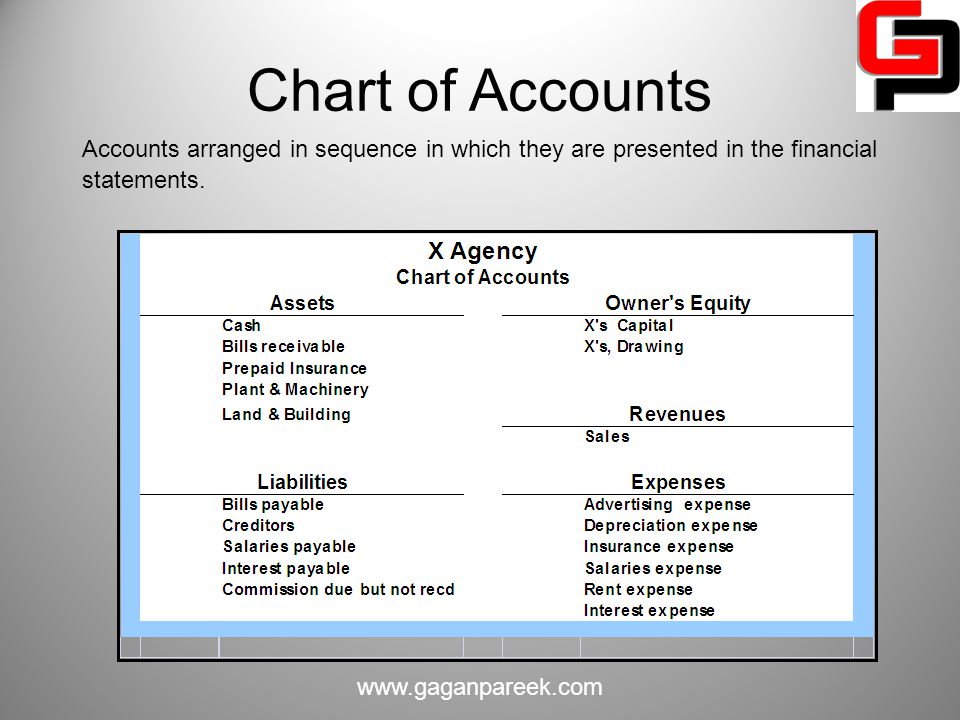

75

Chart of Accounts Accounts arranged in sequence in which they are presented in the financial statements.

76

Standard Form of Account

T-account form used in accounting textbooks. In practice, the account forms used in ledgers are much more structured.

77

Posting Posting – the process of transferring amounts from the journal to the ledger accounts. General Journal J1 101 General Ledger Oct. 1 Capital A/C 15,000 15,000

78

Posting Review Question Posting: normally occurs before journalizing.

transfers ledger transaction data to the journal. is an optional step in the recording process. transfers journal entries to ledger accounts.

79

The Trial Balance A list of accounts and their balances at a given time. Purpose is to prove that debits equal credits.

80

Trial Balance Limitations of a Trial Balance

The trial balance may balance even when a transaction is not journalized, a correct journal entry is not posted, a journal entry is posted twice, incorrect accounts are used in journalizing or posting, or offsetting errors are made in recording the amount of a transaction.

81

The Trial Balance Review Question A trial balance will not balance if:

a correct journal entry is posted twice. the purchase of supplies on account is debited to Supplies and credited to Cash. a Rs100 cash drawing by the owner is debited to Owner’s Drawing for Rs1,000 and credited to Cash for Rs100. a Rs450 payment on account is debited to Accounts Payable for Rs45 and credited to Cash for Rs45.

82

Recording Process Case

X is confused about how accounting information flows through the accounting system. She believes the flow of information is as follows. Debits and credits posted to the ledger. Business transaction occurs. Information entered in the journal. Financial statements are prepared. Trial balance is prepared. Is X correct? If not, indicate to X the proper flow of the information. No, X is not correct . The proper sequence is as follows : ( b ) Business transaction occurs. ( c ) Information entered in the journal. ( a ) Debits and credits are posted to the ledger. ( e ) Trial balance is prepared. ( d ) Financial statements are prepared.

Business transaction occurs. ( c ) Information entered in the journal. ( a ) Debits and credits are posted to the ledger. ( e ) Trial balance is prepared. ( d ) Financial statements are prepared.")

83

Accounting Cycle

84

The Accounting Cycle The accounting cycle is the process by which accountants prepare financial statements for an entity for a specific period of time.

85

Steps in Accounting Cycle

Analyze transactions Record transactions in the journal Post journal entries to the ledger accounts Prepare a trial balance Journalise and post adjusting entries and prepare adjusted trial balance Prepare financial statements Journalise and post closing entries: temporary accounts(transfer to profit and loss account) Carry forward the balance sheet accounts to the next accounting period: permanent accounts

Carry forward the balance sheet accounts to the next accounting period: permanent accounts.")

86

The Accounting Cycle For a new business, begin by setting up ledger accounts. For an established business, begin with account balances carried over from the previous period.

87

The Accounting Work Sheet

What is the work sheet? A work sheet is a multi-columned document used by accountants to help move data from the trial balance to the financial statements. It is an internal document.

88

Use the work sheet to complete the accounting cycle.

89

Recording the Adjusting Entries

The work sheet identifies the accounts that requires adjustments. Adjustment of the accounts requires journalizing and posting of the adjustment entries.

90

Recording the Adjusting Entries

The adjusting entries are recorded in the journal when the accounts are adjusted on the work sheet. Adjustment entries are posted just before the closing entries.

91

Close the revenue, expense, and withdrawal accounts.

92

Closing the Accounts Closing of the accounts that prepares the accounts for recording transactions during the next period.

93

Closing the Accounts Closing Entries Revenues increase Owner’s Equity.

Expenses and Withdrawals decrease Owner’s Equity.

94

Closing the Accounts Revenues and Expense accounts are closed to Income Summary. Income Summary is closed to Capital. Withdrawals are closed to Capital. In a corporation, Dividends are closed to Retained Earnings.

95

Closing the Accounts Income Summary

A debit balance represents net loss. A credit balance represents net income.

96

Postclosing Trial Balance

The accounting cycle ends with the post closing trial balance. The post closing trial balance is dated as of the end of the period for which the statements have been prepared.

97

The Accounting Cycle Recording of Journal Entries Ledger Posting

and balancing of accounts Preparing trial balance. Year end Adjustment Entries. Closing of accounts Preparing adjusted trial balance. Prepare financial statements. Prepare after closing trial balance. Journalizing and post closing entries. 3

98

Permanent Accounts What accounts never close? Assets Liabilities

Owner’s equity Balances of permanent accounts carry over to the next period.

99

Classify assets and liabilities as current or long-term.

100

Current Assets Current assets are cash, or will be converted to cash, in one year or within the normal business operating cycle. What are some other examples? short-term receivables inventory prepaid expenses

101

Current Liabilities Current liabilities are debts or obligations due within one year or within the operating cycle. What are some examples? accounts and salary payables short-term notes payable unearned revenue

102

Long-term Assets and Liabilities

Long-term assets include all other assets. property, equipment, and intangibles Long-term liabilities are all other debts due in longer than one year or the entity’s operating cycle.

103

The Classified Balance Sheet

Debit side Current assets Long-term assets Credit side Current liabilities Long-term liabilities Listed in the order of decreasing liquidity Listed in the order of how soon they must be paid

104

The Classified Balance Sheet

XYZ Ltd March 31, 20XX Assets Liabilities Current assets: Current liabilities: Cash ,000 Accounts payable ,000 Accounts receivable ,000 Salary payable ,000 Closing Stock ,500 Unearned revenue ,500 Total current assets 8, Total Current liabilities 6,500 Gross Block Owner’s equity Equipment 15, Capital ,000 Less Accum. deprec. 7, ,000 Total liabilities and Total assets 16,500 owner’s equity ,500

105

Transactions Effecting Balance Sheet

Possibility Example An increase in assets followed by an increase in liabilities and vice versa Purchase of a machinery through bank loan A decrease in assets followed by a decrease in liabilities and vice versa Repayment of a bank loan An increase in assets followed by an increase in equity and vice versa Interest earned on the savings deposit increasing the net worth A decrease in assets followed by a decrease in equity and vice versa Theft of some personal possessions leads to decrease in owners equity An increase in an asset followed by a decrease in another asset and vice versa Purchase of car in cash An increase in a liability followed by a decrease in another liability and vice versa Payment to a creditor through bank loan

106

The following are typical accounts that are classified as assets, liabilities, and , equity accounts

Land Building Equipment Vehicles Inventory Prepaid expenses Accounts receivable Cash Mortgage payable Unearned revenue Taxes payable Salaries payable Accounts payable Capital Retained Earnings

107

A good general rule of thumb is that any account that has the word receivable in its title will be an asset, and any account that has the word payable in its title will be a liability. Any account that has the word expense in its title is likely to be classified as an expense on the Income Statement, except for the account Prepaid expenses, which is an asset. Any account with the word income or revenue in its title is classified as revenue on the Income Statement, except for the account Unearned revenue, which is a liability.

108

References: 1. Williams Haka Bettner Meigs , Financial & Managerial Accounting, 12th Edition, The McGraw Hill Companies , Inc,2002. 2. Prof. Ramachandran. N. & Prof. Kakani Ram Kumar , Financial Accounting for Management ,Tata McGraw Hill. 3. Prof. Mukherjee. A. & Prof Hanif. M, Modern Accountancy, 2nd Edition,, Tata McGraw Hill. 4. Duchac , Reeve, & Warren ,Financial Accounting, 2nd Edition,, Thomson South-Western, a part of The Thomson Corporation. Thomson. 5. Narayanaswamy. R, Financial Accounting: A Managerial Perspective 2nd Edition, Prentice Hall of India Pvt Ltd

Similar presentations