Download presentation

Presentation is loading. Please wait.

0

2nd+ Generation Healthcare Consumerism Ronald Bachman, FSA, MAAA

A Workbook for Developing a Vision and Roadmap to 2nd+ Generation Healthcare Consumerism Ronald Bachman, FSA, MAAA President & CEO Healthcare Visions, Inc. Senior Fellow, Center for Health Transformation

1

Table of Contents Page # Topic . 2 Agenda 3 Scope of Work

4 Background Info 5 Task #1 – Setting Principles for Change 8 Task #2 – Vision Statement Development 11 Task #3 – Identification of Acceptable Stategies 14 Change Formula 18 Actuarial Issues 20 Consumerism 40 Task #4 – Personal Care Accounts 65 Task #5 – Wellness, Prevention, & Early Intervention 78 Task #6 – Disease Management 93 Task #7 – Decision Support Tools 102 Task #8 – Incentives & Rewards 111 Task #9 – Viewing Consumerism by Generations 145 Task #10 – Create Consumerism Plans 154 Task #11 – Setting Time Frame for Implementation 158 Integrated Health Management 161 Potential Savings from Healthcare Consumerism 164 Actual Industry Experience Results 170 Task #12 (summary) – Potential Savings 171 Consumer-driven Healthcare Surveys of Growth

– Potential Savings. 171 Consumer-driven Healthcare Surveys of Growth.")

2

Agenda Day# Goal 1 Morning Agenda, Scope of Work, Background, (T1-3), Change Formula, Actuarial Issues, Consumerism, Building Blocks (T4), Building Blocks (T5) 1 Afternoon Building Blocks T(6-8), Multi-generational Issues (T9), Create MSFT Plans (T10), Time Frame for Implementation (T11) Review Decisions from Tasks 1-11, Financials Task 12, Final Input to Roadmap Tasks To Be Completed During 1.5 Day “Extreme” Consumerism 1. Principles Decision Support Tools 2. Consumerism Vision Statement 8. Incentives & Rewards 3. Strategies Viewing by Generations 4. Personal Care Accounts 10. Create Consumerism Plans 5. Wellness Time Frames 6. Disease Management 12. Financial Analysis

, Change Formula, Actuarial Issues, Consumerism, Building Blocks (T4), Building Blocks (T5) 1 Afternoon Building Blocks T(6-8), Multi-generational Issues (T9), Create MSFT Plans (T10), Time Frame for Implementation (T11) 2 Review Decisions from Tasks 1-11, Financials Task 12, Final Input to Roadmap. Tasks To Be Completed During 1.5 Day Extreme Consumerism. 1. Principles 7. Decision Support Tools. 2. Consumerism Vision Statement 8. Incentives & Rewards. 3. Strategies 9. Viewing by Generations. 4. Personal Care Accounts 10. Create Consumerism Plans. 5. Wellness 11. Time Frames. 6. Disease Management 12. Financial Analysis.")

3

Scope of Work for Developing the Roadmap and Beyond

Diagnostic and Readiness Assessment Perform Financial & Actuarial Analysis (set metrics) Design Benefits and Contrib. Strategy (The Road Map) Evaluate, Select, Implement Vendors Develop and Implement Education, Comm., Training, etc. Monitor and Evaluate Evaluate current plans Interview stakeholders Identify Basic Principles for Change Create Consumer Vision Stmt Select Strategies Develop Obj. & scope, set timeframe Match HR/business plan Develop baseline costs Co.& Ee contrib. level Model options Evaluate cost impact and revise Develop measures of success Est. Rel. Value of Components HDHP & Accts Wellness & DM Transition strategy Optional Coverages Carve-out Programs Support services Health vs. Healthcare Debit/Credit Cards Incentive Programs Vendors Technology Services Performance Accountability Reliability Communication Strategy Web-based Training, education Print, video, other media uses Internal vs. External Services Periodic reevaluation of baseline metrics Consumer scorecards Survey, measure success, acceptance Vendor/supplier audits Reassess & modify as appropriate

Design. Benefits. and. Contrib. Strategy. (The Road. Map) Evaluate, Select, Implement. Vendors. Develop. and. Implement. Education, Comm., Training, etc. Monitor. and. Evaluate. Evaluate current. plans. Interview. stakeholders. Identify Basic. Principles for Change. Create Consumer. Vision Stmt. Select Strategies. Develop Obj. & scope, set timeframe. Match HR/business plan. Develop baseline costs. Co.& Ee contrib. level. Model options. Evaluate cost impact and revise. Develop measures of success. Est. Rel. Value. of Components. HDHP & Accts. Wellness & DM. Transition. strategy. Optional. Coverages. Carve-out Programs. Support services. Health vs. Healthcare. Debit/Credit Cards. Incentive Programs. Vendors. Technology. Services. Performance. Accountability. Reliability. Communication Strategy. Web-based Training, education. Print, video, other media uses. Internal vs. External Services. Periodic reevaluation of baseline metrics. Consumer scorecards. Survey, measure success, acceptance. Vendor/supplier audits. Reassess & modify as appropriate.")

4

Background & Issues Current Benefits, Design Issues, Service Issues,

General Concerns, Anti-selection Reasons for Change, Interests in Consumerism, Driving Forces for Change, Perceptions of Employee Satisfaction, Dissatisfaction Other Problems and Positives with Current Plans

5

Task #1 – Setting Principles for Change

Important…Not Important 1. Have the Right Vision & Vision Stmt 2. Have a 3-5 Year Roadmap/Strategic Plan 3. Consider Other Related Corporate Initiatives 4. Create plan as part of Employer of Choice 5. Consider other HR metrics impacted by Healthcare 6. Provide Information on Rx Costs & Alternatives 7. Provide Information on Dr. & Medical Service Costs 8. Provide Information on Hospital Costs 9. Provide Information on the Quality of Dr. Care 10. Provide Information on the Quality of Hospital Care 11. Focus on Discretionary Costs (Rx and OV) 12. Focus on High Cost Claims & Claimants 13. Focus on Wellness and Preventive Care 14. Focus on an Individual Behavior Changes 15. Focus on Group Behavior Changes

Focus on High Cost Claims & Claimants Focus on Wellness and Preventive Care Focus on an Individual Behavior Changes Focus on Group Behavior Changes")

6

Task # 1 – Setting Principles for Change

Important…Not Important 16. Use Incentives and Compliance Rewards 17. Increase Costsharing to Change Behaviors 18. Increase Employee Contributions to Offset Costs 19. Focus on Overall Plan Cost Reduction 20. Set the Right Measurements for Monitoring Progress 21. Build Broad Employee Agreement for Change 22. Minimize Change from Current Plans 23. Make Choices and Plan Options available 24. Improve Access to Care 25. Maintain Existing Network of Providers 26. Provide $ for post-65 retirement healthcare 27. Provide $ for pre-65 retirement healthcare 28. Provide $ for non-plan medical 29. Provide $ for terminated ee’s healthcare 30. Provide $ for non-healthcare expenses 31. Alternative to cutting benefits or initiating contributions

7

Task #2 – Sample Vision Statement Positioning to Balance Cost, Quality, and Access

Sample Vision Statement: Create health and healthcare program options valued by employees that adapt effectively to environmental trends that increase the quality of services, improve access to care, and lower costs. Uncertain, Clinically Oriented Quality Consumer Valued Quality Demand Driven Controls Supply Driven Controls Access Third Party Reimbursement Consumer Involvement & Transparency Cost

8

Task #2 – Create a Consumerism Vision Statement

Sample Vision Statements: Providing high performing highly educated employees and their families with the security of comprehensive health and healthcare coverage that meets their diverse needs and rewards their personal involvement and responsibility as wise users of services to optimize their individual health status and functionality. 2. Affect employee behavior change towards healthier lifestyles and greater consumerism through the use of rewards and incentives. 3. Make employees better consumers of healthcare services by providing them with the necessary health education, decision support tools and useful information including provider cost and quality data. 4. Encourage greater employee awareness and involvement in healthcare and financial decision making, as a building block towards a defined contribution strategy for healthcare in the future.

9

__________________________________

Task #2 - Key Words / Phrases for Consumerism Vision Statement or Addition to Guiding Principles __________________________________

10

Task #3 - Identification of Acceptable Strategies

High Priority...Low Priority 1.Create Transparency – support “employee’s right to know,” minimize distortions of third-party reimbursement system, create transparency in costs, provide education/ training on healthcare costs, use decision support programs 2.Create Personal Involvement – establish greater financial involvement through HDHPs, HRAs or HSAs, reward good behavior, offer valued options, provide long term incentives, provide immediate feedback 3. Be Bold and Creative - Shift from supply-side controls to demand-side control designs. Be an early adopter/fast follower, consider out-of-the box ideas 4. Focus on High Cost “Pareto” Population - Provide financial protection to families in need due to high unexpected medical costs and/or chronic conditions

11

Task #3 - Identification of Acceptable Strategies Continued

Important…Not Important 5. Focus on Saving Lives and Improving Health – Focus on improving the health of the entire population regardless of plan design selected. Implement prevention & wellness for long term savings and DM for immediate impact 6. Focus on Preventive Care – Create incentive programs that change behaviors towards acceptance and compliance with wellness and early intervention, including pre-natal, non-smoking, diet, exercise, and safety 7. Minimize Impact of Cost Shifting – Use consumerism as an alternative to increased cost shifting or higher contributions 8. Implement Optional Consumerism – Provide new programs and plan options on a voluntary basis

12

Task #3 - Identification of Acceptable Strategies Continued

High Priority…Low Priority 9. Implement Change on a Multi-Year Program – Establish a consumer-centric program with a pre- determined multi-year introduction of options and use of accumulated HRAs and/or options 10. Focus on Information Sharing Only– Provide ees with decision support systems and information sources w/o accounts or incentives to reward behavioural change 11. Use Packaged Programs – use full integration of plan design, information, disease management, and decision support systems from single vendor 12. Use Existing Vendors – develop consumerist programs through current vendor relationships only 13. Use “Best of Class” Programs – use selected vendors that May overlay core benefit designs as long as integration is Non-disruptive and transparent to members

13

A Reason To Consider Change

The Definition of Insanity: “Endlessly repeating the same process, hoping for a different result.” - Albert Einstein

14

Employee Perceptions Lead to a sense of entitlement…

Employees underestimate total premium cost Employees overestimate their share of cost 63% Underestimate 16% Close 21% Overestimate 20% Underestimate 11% Close 69% Overestimate Source: Watson Wyatt

15

Requirements & Stages of Change

NO CHANGE Without Desire – “Back Burner” Without Vision – False Starts Without Process – Frustration Requirements & Stages of Change Alignment C H A N G E CHANGE No C H A N G E Threshold Gather Info Pros & Cons Awareness + + =

16

The Formula for Making Change Happen

Set by Mgmt’s Direction Task at Hand Later - Next Steps Results Desire for Change Vision / Roadmap Process for Change POSITIVE CHANGE + + = Desire for Change Vision / Roadmap Process for Change Put on Back Burner + + = Desire for Change Vision / Roadmap Process for Change Expensive False Starts + + = Desire for Change Vision / Roadmap Process for Change Frustration + + =

17

Preliminary Actuarial Work & Issues (NOT performed by CHT)

1. Data Collection and Population Profiling 2. Distribution of claims (low-medium-high-catastrophic claims) 3. Types and Analysis of Chronic & Persistent Conditions 4. Review of Industry Data on Consumerism 5. Use of Actuarial Pricing Model 6. Behavioral Modification Recognition 7. Cost Impact of Strategies and Plan Designs Selected

3. Types and Analysis of Chronic & Persistent Conditions. 4. Review of Industry Data on Consumerism. 5. Use of Actuarial Pricing Model. 6. Behavioral Modification Recognition. 7. Cost Impact of Strategies and Plan Designs Selected.")

18

Purpose of Actuarial Work

Perform the actuarial and financial analysis to determine the impact of options available under a Consumerism Plan. Determine Potential: Plan designs Savings Elements / HRA, HSA, & Account Credits Combinations and interactions of “Building Blocks” Costsharing structure Contribution strategies Participation

19

Reform is Not Enough, Transformation is Required

Consumerism Supply Controls vs. Demand Controls “Them” or “You” Reform is Not Enough, Transformation is Required

20

Supply Controls or Demand Controls

Plan Sponsors and Members have two basic choices to control costs: 1. Managed care & HMOs - The “supply of care” is limited by a third party who controls the access to medical services (e.g. utilization reviews, medical necessity, gatekeepers, formularies, scheduling, types of services allowed), or 2. Healthcare Consumerism - The member controls their “demand for care” because of a direct and significant financial involvement in the cost of care, rewards for compliance, and the information to make wise health and healthcare value driven decisions.

, or. 2. Healthcare Consumerism - The member controls their demand for care because of a direct and significant financial involvement in the cost of care, rewards for compliance, and the information to make wise health and healthcare value driven decisions.")

21

Supply Controls Are Failing

High Healthcare Costs Climbing Higher Patients have lost control of their own healthcare, and are not truly engaged in the process of managing their health Patients are frustrated with managed care “rules” and the impact on time and productivity Patients don’t understand healthcare costs – costs are not transparent “Every System is perfectly designed for the results achieved.”

22

Mega Trends Leading to Demand Control

Personal Responsibility Self-Help, Self-Care Individual Ownership Portability Transparency (the Right to Know) Consumerism (Empowerment)

Consumerism (Empowerment)")

23

Healthcare Consumerism - Defined

Healthcare Consumerism is about transforming an employer’s health benefit plan into one that puts economic purchasing power—and decision-making—in the hands of participants. It’s about supplying the information and decision support tools they need, along with financial incentives, rewards, and other benefits that encourage personal involvement in altering health and healthcare purchasing behaviors. “The job of a leader is to create the possible” – Condi Rice 23

24

Consumerism – Saving Lives & Saving Money

The Moral Imperative for Consumerism: Increasing the Quality of Care, Better Health, and Improving Lives The Economic Imperative for Consumerism: Saving Money (Lower Product Prices and More Jobs)

")

25

Objectives Of Consumerism

Change participant health and healthcare purchasing behaviors Narrow market cost and quality variations using patient decisions Increase transparency of healthcare costs to plan participants Give plan participants more control over and “shared responsibility” for managing own healthcare and related costs Supply participants with the tools to act as better informed healthcare consumers Reduce costs for “discretionary care” through informed purchasing & incentives Reduce long term costs with added incentives for “good health” Reduce costs of Chronic Conditions through improved compliance with treatments and disease management programs Reduce Acute Care costs with incentive hospital tiering based upon cost and quality

26

Basic Requirements for Successful Healthcare Consumerism

Must work for the sickest members, as well as the healthy Must work for those not wanting to get involved in decision-making, as well as those that do

27

The Core of Consumerism

The Unifying Theme for a Health and Healthcare Strategy is: Behavioral Change “Implement only if it supports behavioral change consistent with the strategy”

28

Healthcare Consumerism Roles & Responsibilities / Implications

Employers Facilitators of change Provide increased information and decision making tools Improved employee morale with choice and access Link to productivity, absenteeism, disability, turnover, etc. Consumerism can improve costs/budgeting (current & future) Payers (Self-Insured Employers) Focus on high cost case mgmt/disease mgmt/population mgmt Will become responsible for more communications, training, education direct to consumers Value added services may change, including transactions and asset management Diminished role of managed care for routine care

Payers (Self-Insured Employers) Focus on high cost case mgmt/disease mgmt/population mgmt. Will become responsible for more communications, training, education direct to consumers. Value added services may change, including transactions and asset management. Diminished role of managed care for routine care.")

29

Healthcare Consumerism Roles & Responsibilities / Implications

Employees Increased responsibility for own health & healthcare Involved in own treatment and medical necessity decisions Improved access to care Involved in financial costs of health & healthcare (P4C) Providers More direct involvement with patients and treatment Service and quality will be determined by consumers Pricing will become more flexible and visible (P4P) Overall implications Roles will change for all players The picture change quickly - your strategy must prepare you for rapid market changes

Providers. More direct involvement with patients and treatment. Service and quality will be determined by consumers. Pricing will become more flexible and visible (P4P) Overall implications. Roles will change for all players. The picture change quickly - your strategy must prepare you for rapid market changes.")

30

Consumerism Choices Involve Options for Behavioral Change

Wellness Preventive care Early Intervention Lifestyle Options (diet, exercise, smoking, safety) Self-help, self care Discretionary Expenses (e.g. OV, ER, Rx) Value purchasing (e.g. DXL, o/p vs. in/p) Participation in Disease Management Programs Compliance with Evidence Based Medicine Treatment Plans

Self-help, self care. Discretionary Expenses (e.g. OV, ER, Rx) Value purchasing (e.g. DXL, o/p vs. in/p) Participation in Disease Management Programs. Compliance with Evidence Based Medicine. Treatment Plans.")

31

Consumerism – Much Broader than HDHP & Consumer-Driven Healthcare

Consumerism is A Strategy ****************** It’s about moving from a “benefit” to an “accumulating asset.”

32

Evolution of Healthcare Consumerism

Focus Impact Choices First Generation High Deductible Plans with HRAs or HSAs, Decision Support Tools Discretionary Expenses: Rx, ER, OV, D-X-L Initial Level and Type of Accounts with CDHC / HDHP Designs, Information and Decision Support Services Second Generation Behavior Change Through Rewards Chronic and Persistent Conditions, Pre-natal, Preventive Care Covered Benefits, Type and Level of Matching Funds and P4C / P4P Incentives for Prevention, Wellness, and Disease Management Programs Third Generation Health and Performance Organizational Health, Turnover, Absenteeism, Productivity, Disability, and Presenteeism Group rewards, Importance and Impact on non-health Corporate metrics Fourth Generation Personalized Health and Lifestyle Needs Personalized Health and Performance Outcomes, Genetic Predispositions Lifecycle Needs, Culturally Sensitive DM, Holistic Care, Information Therapy

33

Behavioral Change and Cost Management Potential

The Evolution of Healthcare Consumerism Future Generations of Healthcare Consumerism 2nd Generation Consumerism Focus on Behavior Changes Traditional Plans with Consumer Information 1st Generation Consumerism /CDHC Focus on Discretionary Spending 4th Generation Consumerism Personalized Health & Healthcare 3rd Generation Consumerism Integrated Health & Performance Traditional Plans Behavioral Change and Cost Management Potential Low Impact High Impact

34

The Promises of Consumerism

Major Building Blocks of Consumerism Personal Care Accounts The Promise of Demand Control & Savings It is the creative development, efficient delivery, efficacy, and successful integration of these elements that will prove the success or failure of consumerism. Wellness/Prevention Early Intervention The Promise of Wellness Disease and Case Management The Promise of Health Information Decision Support The Promise of Transparency Incentives & Rewards The Promise of Shared Savings

35

The Consumerism Grid Incentives & Rewards Personal Accounts

2nd Generation Consumerism Focus on Behavior Changes 1st Generation Consumerism Focus on Discretionary Spending 4th Generation Consumerism Personalized Health & Healthcare The Consumerism Grid 3rd Generation Consumerism Integrated Health & Performance Personal Accounts Initial Account Only Activity & Compliance Rewards Indiv. & Group Corporate Metric Rewards Specialized Accts, Matching HRAs, Expanded QME 100% Basic Preventive Care Web-based behavior change support programs Worksite wellness, safety, stress & error reduction Genomics, predictive modeling push technology Information, health coach Compliance Awards, disease specific allowances Population Mgmt, IHM, Integrated Back-to-Work Wireless cyber –support, cultural DM, Holistic care Passive Info Discretionary Expenses Personal health mgmt, info with incentives to access Health & performance info, integrated health work data Arrive in time info and services, information therapy Cash, tickets, Trinkets Health Incentive Accounts, activity based incentives Non-health corporate metric driven incentives Personal development plan incentives, health status related Wellness/Prevention Early Intervention Disease Management Information Decision Support Incentives & Rewards

36

Creating Healthcare Consumerism Plans

Understand Basic Consumerism Plan Designs Including Consumerism in All Plan Options Building Blocks 1. Understanding HRAs/HSAs to Create Personal Care Accts as a Basis for Health “Asset Accumulation” 2. Include Wellness Programs that Encourage Healthy Habits 3. Include Disease Management Programs that Encourage Compliance 4. Include Decision Support Tools for All Plans 5. Include Incentives/Disincentives to Change Behavior

37

Basic Plan Design Options & Healthcare Consumerism

Traditional Health Plans Most Healthcare Consumerism Plan Designs Personal Accounts HMO & FSAs HRAs? PPO & FSAs HRAs? PPO & FSAs with HRAs HDHP PPO & Ltd FSAs HSAs HDHP PPO & Ltd FSAs HSAs Ltd HRAs Typical CDHP Must Meet HSA / HDHP Legal Definition Wellness/Prevention Early Intervention Disease Management Case Management Information Decision Support Incentives & Rewards

38

Potential Use of PCAs to Support Consumerism Plan Designs

Traditional Health Plans Most Healthcare Consumerism Plan Designs Personal Accounts HMO PPO PPO HDHP PPO HDHP PPO Typical CDHP Must Meet HSA / HDHP Legal Definition Wellness/Prevention Early Intervention Minimum Co-Payment Designs Disease and Case Management High Ded & Co-Insurance Designs Health Incentive Accounts? Information Decision Support Initial $500-$1000 HRA with Incentive HRAs Initial Er HSA Contribution Initial Er HSA Contribution With HRA Match & Incentive HRAs & HSAs Incentives & Rewards

39

PPO/HRA and PPO/HSA High Deductible Health Plans

Four components that work together to improve quality, outcomes, and lower cost. Personalized Health Care Web- and Phone- Based Tools Health Tools and Resources Wellness, Condition care Programs, Information and Decision Support Tools and Resources. 3. HRA – ER provided $s HSA - ER and/or EE Provided $s HRA/HSA – Individual & Group Reward $s Incentives and Rewards Health Accounts (HRAs or HSAs) “Benefit dollars” to pay for healthcare expenses. Preventive 100% Coverage Health Account (HRA/HSA) The Definity Health benefit features three key components. The Personal Care Account is an allotment of benefit dollars provided by employers that members use to pay for their medical needs. Doctor visits and prescription drugs, among other medical services, are paid directly from the PCA without the hassle of co-payments. Health Coverage is a repackaging of typical health insurance plans. It features a Preventive Care component that encourages members to be actively involved in managing their health. The third component of the Definity Health benefit is Health Tools and Resources. It provides members with care management services and advanced Web- and phone-based information, tools and resources that encourage them to become true consumers of healthcare. Lets look at these three components in more detail. Deductible Gap PPO Additional Health Coverage beyond the HRA/ HSA. 1. 2. 4.

Benefit dollars to pay for healthcare expenses. Preventive 100% Coverage. Health. Account (HRA/HSA) The Definity Health benefit features three key components. The Personal Care Account is an allotment of benefit dollars provided by employers that members use to pay for their medical needs. Doctor visits and prescription drugs, among other medical services, are paid directly from the PCA without the hassle of co-payments. Health Coverage is a repackaging of typical health insurance plans. It features a Preventive Care component that encourages members to be actively involved in managing their health. The third component of the Definity Health benefit is Health Tools and Resources. It provides members with care management services and advanced Web- and phone-based information, tools and resources that encourage them to become true consumers of healthcare. Lets look at these three components in more detail. Deductible Gap. PPO. Additional. Health Coverage. beyond the HRA/ HSA")

40

Task #4 - Personal Care Accounts

The Promise of Demand Control & Savings HSAs, HRAs, FSAs, FHSAs “Of the 5 building blocks, the greatest among them is the Personal Care Account”

41

HSAs and HRAs - Two Very Different Accounts to Support Consumerism

HSA (2003 MMA) - A law, with specific requirements and benefit design requirements. - Most TAX ADVANTAGED vehicle ever created HRAs (6/26/2002) - A regulatory creation based upon an IRS ruling - Most FLEXIBLE vehicle ever created

- A law, with specific requirements and benefit design requirements. - Most TAX ADVANTAGED vehicle ever created. HRAs (6/26/2002) - A regulatory creation based upon an IRS ruling. - Most FLEXIBLE vehicle ever created.")

42

Health Savings Accounts – Advantage Employees

Tax-free savings vehicles for medical expenses, no use-it-or-lose-it rule Effective January 1, 2004 Eligibility: must be covered under high deductible health plan (HDHP) Portable

Portable.")

43

Health Savings Accounts

Individual accounts To permit saving for qualified medical and retiree health expenses on a tax-free basis Must be offered in conjunction with a legally defined HDHP - “High Deductible Health Plan” Portable An HSA is owned by the individual, similar to IRAs, and transfers if the employee changes jobs Held in a trust or custodial account; trustees – banks, insurance companies, approved non-bank trustees

44

Health Savings Accounts: Contributions

Contribution limits determined monthly based on status, eligibility, HDHP coverage as of first day of month (offset by other HSA contributions) 2005 Monthly limit – 1/12th of lesser of deductible or $2,650 (self-only), $5,250 (family), indexed Catch-up contributions, age 55 to 64, $600 in 2005, phased up to $1,000 annually in 2009

2005 Monthly limit – 1/12th of lesser of deductible or $2,650 (self-only), $5,250 (family), indexed. Catch-up contributions, age 55 to 64, $600 in 2005, phased up to $1,000 annually in")

45

HSAs – Real Dollars, Portable, Vested

Can be used or taken in cash at anytime, even when no longer eligible to make contributions Tax-free if used to pay for qualified medical expenses (IRC Section 213(d)) For other purposes, subject to income tax and 10% penalty - 10% penalty waived in case of death or disability - 10% penalty waived for distributions after age 65 or older HSA can be transferred tax-free to spouse on death; otherwise taxable to estate or beneficiary Transfers upon divorce, nontaxable, becomes spouse’s HSA

) For other purposes, subject to income tax and 10% penalty. - 10% penalty waived in case of death or disability. - 10% penalty waived for distributions after age 65 or older. HSA can be transferred tax-free to spouse on death; otherwise taxable to estate or beneficiary. Transfers upon divorce, nontaxable, becomes spouse’s HSA.")

46

HSA Eligible HDHP High Deductible Health Plan – By Law

Self-only: a deductible of at least $1,000; maximum HSA is $2,650; no more than $5,100 maximum out-of pocket expenses (incl. Ded.) Family coverage: a deductible of at least $2,000; maximum HSA is $5250; no more than $10,200 on out-of pocket expenses (incl. Ded.) 2005 Age 55 and over catch up amount of $600 Preventive services are not subject to the deductible OK for out of network costs to exceed maximum out-of pocket limits THE ABOVE 2005 AMOUNTS ARE SUBJECT TO ANNUAL INDEXING

Family coverage: a deductible of at least $2,000; maximum HSA is $5250; no more than $10,200 on out-of pocket expenses (incl. Ded.) 2005 Age 55 and over catch up amount of $600. Preventive services are not subject to the deductible. OK for out of network costs to exceed maximum out-of pocket limits. THE ABOVE 2005 AMOUNTS ARE SUBJECT TO ANNUAL INDEXING.")

47

HRAs- Advantage Employers National Accounts, Er Controlled Rules

Employer does not fund and has cash flow value Employer can determine rules for HRA usage; they are subject to forfeiture; they are not portable, but can be subject to vesting HRAs are more flexible in plan design, can tailor scope of reimbursements, are less costly for employer Employer decides if HRA can used for (1) medical plan expenses not otherwise reimbursed, (2) non-plan QME 213(d), and/or (3) insurance premiums

medical plan expenses not otherwise reimbursed, (2) non-plan QME 213(d), and/or (3) insurance premiums.")

48

Important Differences between Use of HRAs and HSAs for Supporting Behavioral Change

Personal Care Accounts Generation 1 Initial Account Only Generation 2 Activity & Compliance Rewards Generation 3 Indiv. & Group Corporate Metric Rewards Generation 4 Specialized Accts, Matching HRAs, Expanded QME Health Reimbursement Arrangements 1. Any Amount 2. Notional Acct 3. Employer Determined 4. Employer Only Contributions 1. Flexible Activity & Compliance Rewards 2. Employer Determined 3. Can not be cashed out 4. Must be used for healthcare 1. Flexible Indiv & Group Rewards 4. Must be used for healthcare 1. Specialized Notional Accts, 2. Can terminate by employer rules 3. Potential IRS Expanded QME Health Savings Accounts 1. Amounts Set by law 2. Real Dollars in Acct 3. Er or Ee Contrib 4. Contributions up to plan deductible of $ Single $ Family 5. Non-substantiation 1. Ltd Potential – (But For Rule) 2. Must give Cash Option 3. Awards must be same $ amt or same % of deductible 3. HSA can be used (with 10% penalty) for non- healthcare expenses 2. All participants must receive same amount or same % of deductible 3. Difficult to use for Group Incentives 2. 100% Vested & Portable 3. Can use matching HRAs, 4. Potential IRS Expanded QME

2. Must give Cash Option. 3. Awards must be same. $ amt or same % of. deductible. 3. HSA can be used (with. 10% penalty) for non- healthcare expenses. 2. All participants must. receive same amount or. same % of deductible. 3. Difficult to use for Group. Incentives % Vested & Portable. 3. Can use matching. HRAs, 4. Potential IRS. Expanded QME.")

49

HRAs – Best for Larger Groups

HRAs – Best for Larger Groups? HSAs – Best for Individuals and Small Groups? Current State Combination Accounts HRAs HSAs FSAs Employer-based Healthcare Traditional (Ltd Carry-over) Special Purpose Non-Plan Employer-based healthcare Special Purpose Accounts Incentive Matching Individual-based Healthcare Employer-based Healthcare with Individual Accountability Er-Based with HSA Contributions Employer-based Defined Contribution Developments

Special Purpose Non-Plan. Employer-based healthcare. Special Purpose Accounts. Incentive Matching. Individual-based Healthcare. Employer-based Healthcare with Individual Accountability. Er-Based with HSA Contributions. Employer-based. Defined Contribution Developments.")

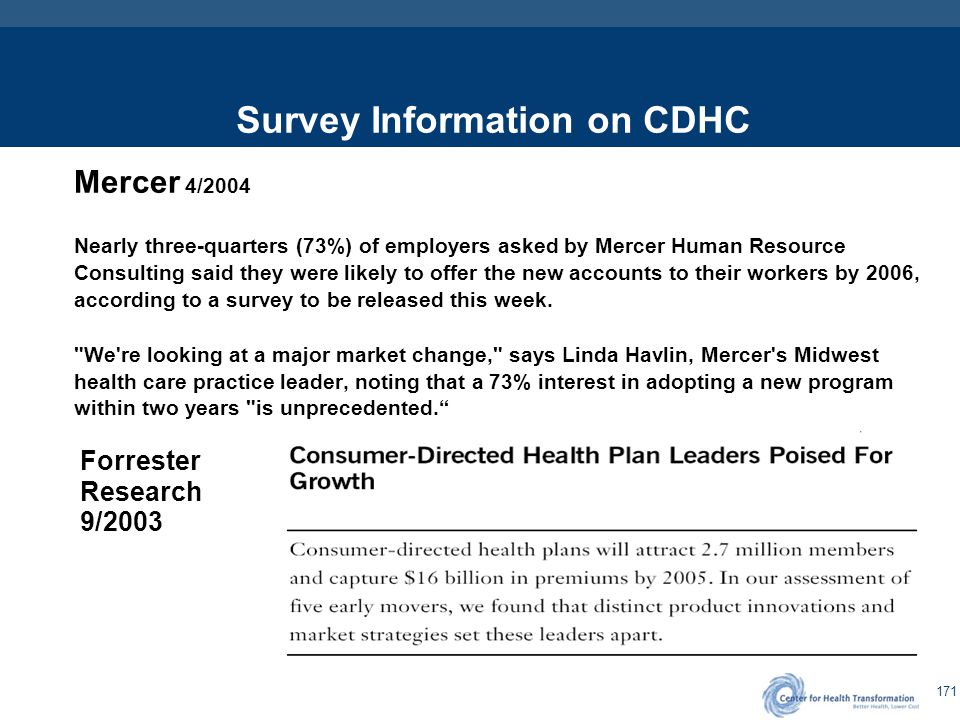

50

Are HSAs the right vehicle for large employer groups?

Yes, If……….. Or No, Because……. Need to Understand the Consumer Movement, Federal Health Policies, & the Market Transformation that is Underway

51

Are HSAs the Wave of the Future? Which Direction will Legislation Take?

Yes, if…. … we recognize the HSA legislation and regulations as a good start and another building block for consumerism and behavioral change. …Er’s and Ee’s recognize current limitation and optimize available uses …there is additional legislation/regulation to support large Er interests in providing HSAs (use for healthcare only, Rx coverage problem, combination accounts). …there is legislative support for the common use of FSAs for targeted needs, HSAs as true “Health Savings Accounts” and HRAs as true “Health Reimbursement Arrangements. No, because…. … they were not legislated/regulated with large employers in mind. … of a desire to promote individual insurance over individual ownership (under employer and individual policies) … they are just a tool to cost shift to employees, they can not reward behavior change … they are only desirable to the young, healthy, and wealthy

. …there is legislative support for the common use of FSAs for targeted needs, HSAs as true Health Savings Accounts and HRAs as true Health Reimbursement Arrangements. No, because…. … they were not legislated/regulated with large employers in mind. … of a desire to promote individual insurance over individual ownership (under employer and individual policies) … they are just a tool to cost shift to employees, they can not reward behavior change. … they are only desirable to the young, healthy, and wealthy.")

52

Summary - PCA Comparisons

53

Summary - PCA Comparisons (cont)

")

54

The Fundamental Federal Policy Question

Will Legislation/Regulation Use HSAs to … mainly promote portable Individual & Small Group Insurance, OR … expand Personal Care Account ownership through in both an employer-based and individual-based healthcare system thru HSAs, HRAs, and FSAs.

55

- The Answer - Flexible Health Savings Accounts (FHSAs)

FHSAs would have the tax advantages of HSAs and the key flexibilities of HRAs. Basic Principles: Retain personal responsibility goal of HSA/HDHPs Focus on Behavior Change Recognize value of Pay for Compliance as a driver for behavior change and shared savings with personal responsibility Expand adoption and funding of HSAs by large employers

56

Flexible Health Savings Accounts (FHSAs) The Next Generation

Four needs that would allow FHSAs the flexibility to: Provide financial Rewards and Incentives for Behavioral Change. 2. Encourage Employer/Carrier FHSA contributions towards healthcare 3. Be provided with plan designs other than HDHPs 4. Address FHSA/HSA Technical Issues

57

FHSA Flexibilty to Provide Financial Rewards and Incentives for Behavioral Change

1. Allow for compliance incentives under disease management programs (e.g. diabetes, asthma, CHF) and wellness initiatives (e.g. wellness assessments, smoking cessation, etc.). 2. Change Comparability Rule to mean all members under a given program of care or treatment, such as, a disease management or wellness program. 3. Rewards and/or incentives should not be limited by the deductible limit, but should be consistent with expected savings from programs for which participation is being rewarded.

and wellness initiatives (e.g. wellness assessments, smoking cessation, etc.). 2. Change Comparability Rule to mean all members under a given program of care or treatment, such as, a disease management or wellness program. 3. Rewards and/or incentives should not be limited by the deductible limit, but should be consistent with expected savings from programs for which participation is being rewarded.")

58

FHSA Flexibility to Encourage Employer Contributions to Healthcare

1. Allow employers/carriers to voluntarily contract with employees to require employer/carrier funded FHSAs to be used only for healthcare expenses while employed and covered under the plan. 2. Remove cap on employer/carrier funded FHSA contributions or expand to at least the plan’s Maximum Out-Of-Pocket total exposure in a given calendar year.

59

FHSAs Flexibility to be Provided with Plan Designs Other than HDHPs

1. Preventive drugs include maintenance drugs. Drugs now defined as preventive by the Treasury Dept. can be covered below the deductible, while the cost of maintenance drugs is now included in the deductible. 2. Allow Rx to exist as carve out benefits at least for prescription drugs associated with chronic and persistent disease states 3. Allow “incentive only based” FHSAs for employer/carrier only funding under non-HDHPs (i.e. no initial FHSA funding or employee funding) 4. Allow some mental health and substance abuse benefits (besides EAPs) to be included under preventive care. 5. Allow use of HSA to pay for pre-65 Retiree and Individual Healthcare premiums

4. Allow some mental health and substance abuse benefits (besides EAPs) to be included under preventive care. 5. Allow use of HSA to pay for pre-65 Retiree and Individual Healthcare premiums.")

60

FHSA Flexibility - Technical Issues

Allow FHSA/HSAs to go into effect on the first day of coverage is effective. 2. Allow FHSA/HSA contributions for a full calendar year regardless of when a plan is effective. 3. Allow FHSA/HSAs to be used to pay for health coverage premiums (other than current limited use for (1) Premiums for coverage under the Consolidated Omnibus Budget Reconciliation Act (COBRA), and (2) premiums for HDHP coverage for those who receive federal or state unemployment compensation). 4. Allow Flexibility to "post-date" the FHSA/HSA effective date so that FHSA/HSA dollars can cover expenses incurred before the account was established. Allow the account to be opened under a "provisional status" until the necessary paperwork is filed, at which time the account becomes active.

Premiums for coverage under the Consolidated Omnibus Budget Reconciliation Act (COBRA), and (2) premiums for HDHP coverage for those who receive federal or state unemployment compensation). 4. Allow Flexibility to post-date the FHSA/HSA effective date so that FHSA/HSA dollars can cover expenses incurred before the account was established. Allow the account to be opened under a provisional status until the necessary paperwork is filed, at which time the account becomes active.")

61

Growth of Personal Care Accounts

HRAs HSAs 2000* None None 2001* , None 2002* 53, None 2003* 394, None 2004(est) M 400,000 2005(est) M ,000,000 2006(est) M ??? 2007(est) M ??? * Deliotte Consulting

1-1.5M 400, (est) 3.2M 1,000, (est) 6.0+M 2007(est) 12-15M * Deliotte Consulting.")

62

The Consumerism Grid Incentives & Rewards Personal Accounts

2nd Generation Consumerism Focus on Behavior Changes 1st Generation Consumerism Focus on Discretionary Spending 4th Generation Consumerism Personalized Health & Healthcare The Consumerism Grid 3rd Generation Consumerism Integrated Health & Performance Personal Accounts Initial Account Only Activity & Compliance Rewards Indiv. & Group Corporate Metric Rewards Specialized Accts, Matching HRAs, Expanded QME 100% Basic Preventive Care Web-based behavior change support programs Worksite wellness, safety, stress & error reduction Genomics, predictive modeling push technology Information, health coach Compliance Awards, disease specific allowances Population Mgmt, IHM, Integrated Back-to-Work Wireless cyber –support, cultural DM, Holistic care Passive Info Discretionary Expenses Personal health mgmt, info with incentives to access Health & performance info, integrated health work data Arrive in time info and services, information therapy Cash, tickets, Trinkets Health Incentive Accounts, activity based incentives Non-health corporate metric driven incentives Personal development plan incentives, health status related Wellness/Prevention Early Intervention Disease Management Information Decision Support Incentives & Rewards

63

Task #4 - Discussion on Type(s) and Use of Personal Care Accounts

____________________________________________________________

64

Task #5 - Wellness, Prevention, and Early Intervention

The Promise of Wellness

65

Wellness - Defined Wellness is a proactive organized program providing lifestyle and medical/clinical assistance to employees and their family members in maintaining good health. Wellness programs encourage voluntary behavior changes and support compliance with proven approaches to maintain health, reduce health risks and enhance their individual productivity.

66

Wellness – The Need For every 100 members:

23-30% smoke (70% want to quit, 35% try each year) 29% have high blood pressure 30% have cardiovascular disease 80% do not exercise regularly 55% or more are overweight or obese 30% are prone to low back pain (many linked to obesity) 6-9% have diabetes 10% are depressed 35% are under significant stress 50% do not wear their seat belts

29% have high blood pressure. 30% have cardiovascular disease. 80% do not exercise regularly. 55% or more are overweight or obese. 30% are prone to low back pain (many linked to obesity) 6-9% have diabetes. 10% are depressed. 35% are under significant stress. 50% do not wear their seat belts.")

67

Wellness – The Desire for Change

For every 100 members: 47% are trying to improve their diet 37% plan to undergo some health screening 30% state they exercise regularly Only 23% are aware of the health promotion and wellness programs offered by their employer sponsored health plans 76% of employers with over 11,000 employees offer health management programs Kaiser Family Foundation Survey, 9/03

68

Wellness - How Does It Impact Employees and Family Members?

e.g., Low Risk, Good Nutrition, Active Lifestyle At-Risk / Acute Condition e.g., Inactivity, High Stress, Overweight, High Blood Pressure, Smoking Chronically-Ill e.g., Diabetes, Musculoskeletal, Heart Disease, Asthma, MH/SA Catastrophic e.g., Cancer, Rare Diseases, Head Trauma No Claims Generally Healthy O/P (Low) In/P (High) Maternity In/P (High) % Ee 15% 48% 14% 3% 12% 4% 1% % $ 0% 5% 21% 20% 63% 17% % $ 32% 56% Prevention Wellness – Lifestyle Wellness - Lifestyle Minimize Acute Episodes Minimize Complications Maximize Recoveries Maximize Stabilization Early Intervention Wellness - Clinical Wellness - Clinical Traditional Wellness Programs

In/P (High) Maternity. In/P (High) % Ee. 15% 48% 14% 3% 12% 4% 1% % $ 0% 5% 21% 20% 63% 17% % $ 32% 56% Prevention. Wellness – Lifestyle. Wellness - Lifestyle. Minimize Acute Episodes. Minimize Complications. Maximize Recoveries. Maximize Stabilization. Early Intervention. Wellness - Clinical. Wellness - Clinical. Traditional Wellness Programs.")

69

Wellness – Examples for Employer Sponsored Programs

Common Programs Weight Management Fitness/exercise/health clubs Smoking cessation Employer Support Communication and awareness (newsletters, health fair, posters) Screening (health awareness profiles, blood pressure check, blood tests, body fat analysis) Education (seminars/classes, self help kits, group discussions, lunch and learn) Behavioral Change (on-site fitness center, flu shots, lunchtime walks, yoga classes)

Screening (health awareness profiles, blood pressure check, blood tests, body fat analysis) Education (seminars/classes, self help kits, group discussions, lunch and learn) Behavioral Change (on-site fitness center, flu shots, lunchtime walks, yoga classes)")

70

Wellness – Working within Consumerism

Traditional Plans Cover selected wellness in benefit plan at 100% Supplement with non-plan wellness and work-site programs Other: same * as below PPO/HRA incentives PPO/HRA Include Employer defined wellness/prevention benefits at 100% Include HRA Incentive for Wellness Appraisal Include HRA Incentives for personal wellness activities Include HRA Incentives for work-site wellness participation PPO/HSA Include IRS defined Preventive Care benefits at 100% Benefits contingent upon HSA contribution? Wellness Appraisal Other: same * as above with PPO/HRA incentives

71

Consumerism - Programs and Services

Prescription Drugs Information Evidence Based Medicine Medical Care Guidelines Health Library Disease Management Condition Specific Assessment Tools Chronic & Persistent Wellness Voluntary Participation Voluntary & Incentive Based Mandatory Participation Mandatory & Incentive Based Self Care Management Information On-Line Health Risk Assessment Personal and Family Tracking Health & Performance Population Management Case Management Cost & Quality Management Stress Management Assessment Tools Self Help Tools Depression Screening Preventive Care – Lifestyle Lifestyle Nutrition Fitness Personal Health Management Preventive Care – Clinical Immunizations Hypertension Screening Cholesterol Testing Mammograms Pap Smears Blood Pressure Checks Colorectal Cancer Testing Diabetes Testing Osteoporosis Testing Chlamydia Tests Early Prevention Wellness Online News Safety Pre-Natal Well Baby Care New Mom Programs Medical Services Support FAQ, Preparation for In/P End of Life Care Provider Cost/Quality Incentives Regional Centers of Excellence

72

Wellness & Preventive Care for HSAs

Preventive care includes, but is not limited to, the following: Periodic health evaluations, including tests and diagnostic procedures ordered in connection with routine examinations, such as annual physicals. Routine prenatal and well-child care. Child and adult immunizations. Tobacco cessation programs. Obesity weight- loss programs. Screening services However, preventive care does not generally include any service or benefit intended to treat an existing illness, injury, or condition.

73

HSA Safe Harbor Preventive Care Screening Services

Infectious Disease Screening Bacteriuria Chlamydial Infection Gonorrhea Hepatitis B Virus Infection Hepatitis C Human Immunodeficiency Virus (HIV) Syphilis Tuberculosis Infection Mental Health/Subst. Abuse Screening Dementia Depression Drug Abuse Problem Drinking Suicide Risk Family Violence Cancer Screening Breast Cancer (e.g., Mammogram) Cervical Cancer (e.g., Pap Smear) Colorectal Cancer Prostate Cancer (e.g., PSA Test) Skin Cancer Oral Cancer Ovarian Cancer Testicular Cancer Thyroid Cancer Heart and Vascular Diseases Screening Abdominal Aortic Aneurysm Carotid Artery Stenosis Coronary Heart Disease Hemoglobinopathies Hypertension Lipid Disorders

Syphilis. Tuberculosis Infection. Mental Health/Subst. Abuse Screening. Dementia. Depression. Drug Abuse. Problem Drinking. Suicide Risk. Family Violence. Cancer Screening. Breast Cancer (e.g., Mammogram) Cervical Cancer (e.g., Pap Smear) Colorectal Cancer. Prostate Cancer (e.g., PSA Test) Skin Cancer. Oral Cancer. Ovarian Cancer. Testicular Cancer. Thyroid Cancer. Heart and Vascular Diseases Screening. Abdominal Aortic Aneurysm. Carotid Artery Stenosis. Coronary Heart Disease. Hemoglobinopathies. Hypertension. Lipid Disorders.")

74

Wellness – Planning Will the wellness program be for employees only, or employees and dependents? Will you purchase from vendor, internally developed, or a combination Consider in conjunction with plan covered wellness benefits (immunizations, mammograms, screening, EAP, physical exams, pre- natal care, well child care, etc.) Consider in conjunction with worksite programs (safety, ergonomics, work-life programs, etc.) Incentives/rewards provided for compliance

Consider in conjunction with worksite programs (safety, ergonomics, work-life programs, etc.) Incentives/rewards provided for compliance.")

75

The Consumerism Grid Incentives & Rewards Personal Accounts

2nd Generation Consumerism Focus on Behavior Changes 1st Generation Consumerism Focus on Discretionary Spending 4th Generation Consumerism Personalized Health & Healthcare The Consumerism Grid 3rd Generation Consumerism Integrated Health & Performance Personal Accounts Initial Account Only Activity & Compliance Rewards Indiv. & Group Corporate Metric Rewards Specialized Accts, Matching HRAs, Expanded QME 100% Basic Preventive Care Web-based behavior change support programs Worksite wellness, safety, stress & error reduction Genomics, predictive modeling push technology Information, health coach Compliance Awards, disease specific allowances Population Mgmt, IHM, Integrated Back-to-Work Wireless cyber –support, cultural DM, Holistic care Passive Info Discretionary Expenses Personal health mgmt, info with incentives to access Health & performance info, integrated health work data Arrive in time info and services, information therapy Cash, tickets, Trinkets Health Incentive Accounts, activity based incentives Non-health corporate metric driven incentives Personal development plan incentives, health status related Wellness/Prevention Early Intervention Disease Management Information Decision Support Incentives & Rewards

76

Task #5 - Discussion on Type(s) and Use of Wellness and Prevention

____________________________________________________________

77

Task #6 - Disease Management Programs

The Promise of Health The “Holy Grail” of Cost and Quality Improvements

78

Disease or Condition Management – the Holy Grail of Potential Savings

Primary cost drivers are chronic disease and serious acute conditions. The direct impact on productivity is comparable to the direct cost of health care 80% of costs Driven by 20% of claimants For a typical employer, 15-30% of costs are driven by controllable health risks 50% of costs Have a behavioral root cause (CDC 1999)

")

79

Disease Management Potential Focus on Hi-Volume / Hi-Cost Users

Cost Curve % Members % Costs 1% > 20% 15% -> 68% 50% -> 95% EBRI -Stakeholders in Consumer-Driven Health Care

80

Disease Management - Defined

Disease Management is an proactive organized program providing lifestyle and medical/clinical assistance to employees and their family members with chronic and persistent conditions. Disease Management programs encourage voluntary behavior changes and support compliance with proven medical practices which stabilize conditions, reduce health risks and enhance their individual productivity.

81

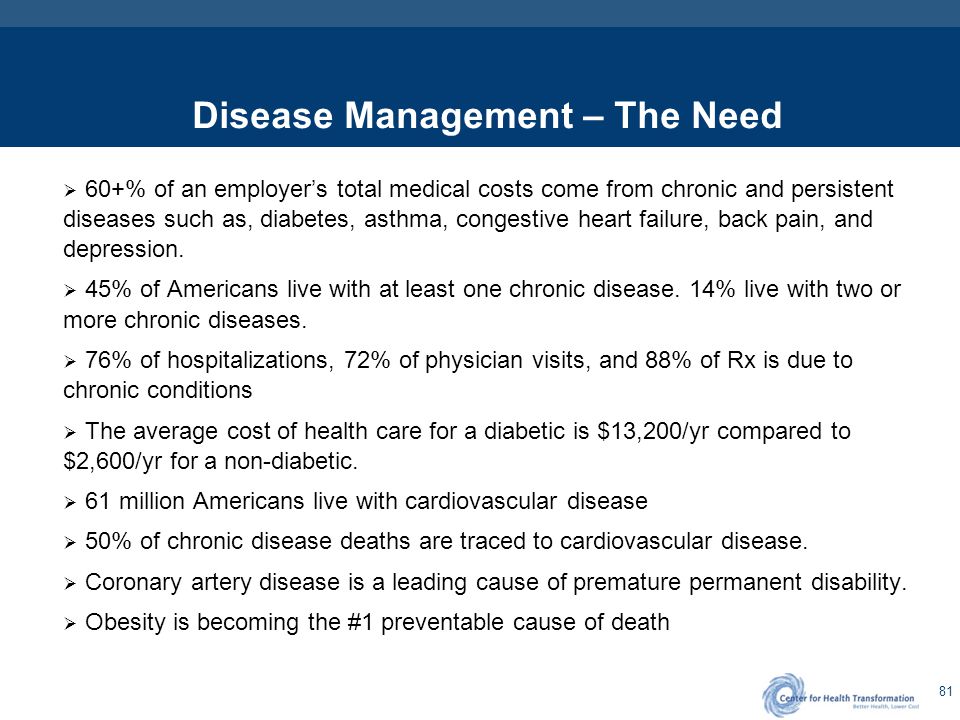

Disease Management – The Need

60+% of an employer’s total medical costs come from chronic and persistent diseases such as, diabetes, asthma, congestive heart failure, back pain, and depression. 45% of Americans live with at least one chronic disease. 14% live with two or more chronic diseases. 76% of hospitalizations, 72% of physician visits, and 88% of Rx is due to chronic conditions The average cost of health care for a diabetic is $13,200/yr compared to $2,600/yr for a non-diabetic. 61 million Americans live with cardiovascular disease 50% of chronic disease deaths are traced to cardiovascular disease. Coronary artery disease is a leading cause of premature permanent disability. Obesity is becoming the #1 preventable cause of death

83

Disease Management – The Desire for Change

Very Little under Traditional System: 50% do not follow recommended standards of care 33% will high blood pressure do not know 33% of diabetics do not know it Patient’s lack of knowledge and information Patients without financial incentives to change health and healthcare behaviors Distortions of current 3rd party reimbursement medical financing system. Plans pay for treatments not prevention or compliance Physicians without incentives to take time and effort to deal effectively with chronic conditions

84

Disease Management – Elements for a Successful Program

There are four elements of a successful disease management: 1. A delivery system of health care professionals and organizations closely coordinating to provide medical care and support the patient’s compliance throughout the course of a disease. 2. A process that monitors the compliance and describes outcome-based care guidelines for targeted patients. 3. A process for continuous improvement that measures clinical behavior, refines treatment standards, and improves the quality of care provided. 4. Incentive awards that support the disease management medical and clinical care services

85

20 Priority Areas per the Institute of Medicine

1. Asthma, supporting and treating those with chronic conditions. 2. Care coordination for patients with multiple chronic conditions. 3. Children with special health and care needs, particularly those with chronic conditions. 4. Diabetes, which can lead to high blood pressure, heart disease, blindness and other complications. 5. End-of-life care for people with advanced organ failures, concentrating on reducing symptoms. 6. Frailty - preventing accidents, treating bedsores and improving advanced care. 7. High blood pressure - left untreated it can lead to heart attack, stroke and kidney failure. 8. Immunization. 9. Evidence-based cancer screening, which can reduce death rates for many cancers, including colorectal and cervical. 10. Ischemic heart disease, also known as coronary heart disease. Efforts should focus on prevention.

86

20 Priority Areas per the Institute of Medicine

11. Major depression, which currently has a much lower treatment rate that other major diseases. 12. Medication management to prevent errors. 13. Noscomal infections. These are infections acquired in the hospital and kill an estimated 90,000 Americans annually. 14. Obesity, which is blamed for as many as 300,000 deaths annually in the United States. 15. Pain control in advanced cancer. 16. Pregnancy and childbirth, especially improving the quality of prenatal care. 17. Self-management and health literacy, using public and private organizations to increase the level of health education. 18. Severe and persistent mental illness; improving mental health care in the public sector, including state hospitals and community centers. 19. Stroke, the third highest cause of death in America. 20. Tobacco-dependence treatment for adults.

87

Disease Mgmt - How Does It Impact Employees and Family Members?

Well e.g., Low Risk, Good Nutrition, Active Lifestyle At-Risk / Acute Condition e.g., Inactivity, High Stress, Overweight, High Blood Pressure, Smoking Chronically-Ill e.g., Diabetes, Musculoskeletal, Heart Disease, Asthma, MH/SA Catastrophic e.g., Cancer, Rare Diseases, Head Trauma No Claims Generally Healthy O/P (Low) In/P (High) Maternity In/P (High) % Ee 15% 48% 14% 3% 12% 4% 1% % $ 0% 5% 21% 20% 63% 17% % $ 32% 56% Prevention Wellness - Lifestyle Wellness – Lifestyle Minimize Acute Episodes Minimize Complications Maximize Recoveries Maximize Stabilization Early Intervention Wellness - Clinical Wellness - Clinical Disease Management Program

In/P (High) Maternity. In/P (High) % Ee. 15% 48% 14% 3% 12% 4% 1% % $ 0% 5% 21% 20% 63% 17% % $ 32% 56% Prevention. Wellness - Lifestyle. Wellness – Lifestyle. Minimize Acute Episodes. Minimize Complications. Maximize Recoveries. Maximize Stabilization. Early Intervention. Wellness - Clinical. Wellness - Clinical. Disease Management Program.")

88

Disease Management Programs

Designed and Financially Aligned for Success

89

Disease Management Program Planning

Identify key populations Focus on Compliance Manage expectations Respect privacy Follow Best practices (EBM, Outcomes Based Medicine) Integrate demand management, disease management and utilization management Give patients their own data Align Incentives for patients, providers, and Employer Disease management buzz grows despite uneven record Despite their questionable return on investment potential, disease management programs are still hot among employers, according to a new study. An article from the Employee Benefit Research Institute (EBRI) reports employers are increasing their offering of disease management programs designed to control chronic illnesses, which account for three-fourths of the nation’s health care costs. Employers are motivated by the potential of the programs to help shield them from the onslaught of double-digit health care cost increases. Research and case studies for the most part, however, have offered evidence of success only in individual programs. There is no conclusive evidence that disease management in general can improve employees’ health or reduce costs in the long term. A 2001 Hewitt Associates survey found 76% of employers provide disease management programs. This month’s issue of EBRI Notes details disease management trends, including prevalence, effectiveness and the outlook for the future. For full-text copies, call BCBSNC Launches Predictive Modeling Initiative By Diana Garber In order to rapidly identify patients with treatable illnesses—and reduce the administrative costs related to providing services to these customers—Blue Cross and Blue Shield of North Carolina (BCBSNC, Durham, NC) and BioSignia Inc. (Durham) are co-developing a software program that will review insurance claims using predictive modeling technology. The program, designed by BioSignia, is being created to identify candidates for BCBSNC's free healthcare management programs. BCBSNC, which is implementing this program in order control expenses, takes patient lists complied by the program and alerts the people on the lists of the availability of existing health management programs. The basis for the predictive modeling program is an algorithm. The program scans claims filed with BCBSNC and records the dollar amounts, diagnosis and procedure codes. The program has 159 distinguishable diseases in its memory. The program then ranks how far the disease has progressed and how treatable and/or preventable it is in its current stage. The system is looking to pinpoint complicated but treatable conditions. If a patient has a medical condition listed as treatable and resource consuming, the patient is considered a prime target for BCBSNC's healthcare management programs. Once these patients are identified, a nurse from the insurance company contacts the patient and discusses the medical treatment the patient is receiving and if any changes should be made. According to Stephen Blackwelder, Ph.D., manager of quality improvement research and biostatistical support of BCBSNC, "the goal [of this program] is to identify and act more quickly on behalf of members who are in the midst of complicated medical situations. By running the claims through this algorithm, we are hoping to identify people in these situations rapidly, and then implement the solutions we already have in place more quickly." BCBSNC will look at the diagnosis on the claim and how much the procedure cost, not the customer's name on the claim. Patient participation in any of the programs is purely optional and will have no impact on premium rates, according to the insurer. Currently the only way for BCBSNC to get patients to use any of its health management programs is by a doctor's referral, or if a patient decides to call the insurance company's number. BCBSNC is hoping to reach a broader audience through the new program. "Potentially, we want to improve quality of the situation customers are experiencing and keep the cost down for the employer and for us," Blackwelder adds. BioSignia, which had developed the software before signing the agreement with BCBSNC, is still refining the system. Although so far it has only licensed the software to BCBSNC, the vendor thinks the program could be beneficial to many companies. According to Guizhou Hu, Ph.D., vice president of research and development at BioSignia, "They can use this system to identify the people [to whom] they can provide a health promotion to help review medical costs. We want to make this a product that can be available to many other managed care companies."

Integrate demand management, disease management and utilization management. Give patients their own data. Align Incentives for patients, providers, and Employer. Disease management buzz grows despite uneven record. Despite their questionable return on investment potential, disease management programs are still hot among employers, according to a new study. An article from the Employee Benefit Research Institute (EBRI) reports employers are increasing their offering of disease management programs designed to control chronic illnesses, which account for three-fourths of the nation’s health care costs. Employers are motivated by the potential of the programs to help shield them from the onslaught of double-digit health care cost increases. Research and case studies for the most part, however, have offered evidence of success only in individual programs. There is no conclusive evidence that disease management in general can improve employees’ health or reduce costs in the long term. A 2001 Hewitt Associates survey found 76% of employers provide disease management programs. This month’s issue of EBRI Notes details disease management trends, including prevalence, effectiveness and the outlook for the future. For full-text copies, call BCBSNC Launches Predictive Modeling Initiative. By Diana Garber. In order to rapidly identify patients with treatable. illnesses—and reduce the administrative costs related to. providing services to these customers—Blue Cross and Blue Shield. of North Carolina (BCBSNC, Durham, NC) and BioSignia Inc. (Durham) are co-developing a software program that will review insurance. claims using predictive modeling technology. The program, designed by BioSignia, is being created to identify. candidates for BCBSNC s free healthcare management programs. BCBSNC, which is implementing this program in order control expenses, takes. patient lists complied by the program and alerts the people on the. lists of the availability of existing health management programs. The basis for the predictive modeling program is an algorithm. The. program scans claims filed with BCBSNC and records the dollar. amounts, diagnosis and procedure codes. The program has 159. distinguishable diseases in its memory. The program then ranks how. far the disease has progressed and how treatable and/or preventable. it is in its current stage. The system is looking to pinpoint. complicated but treatable conditions. If a patient has a medical. condition listed as treatable and resource consuming, the patient is. considered a prime target for BCBSNC s healthcare management. programs. Once these patients are identified, a nurse from the. insurance company contacts the patient and discusses the medical. treatment the patient is receiving and if any changes should be made. According to Stephen Blackwelder, Ph.D., manager of quality. improvement research and biostatistical support of BCBSNC, the goal. [of this program] is to identify and act more quickly on behalf of. members who are in the midst of complicated medical situations. By. running the claims through this algorithm, we are hoping to identify. people in these situations rapidly, and then implement the solutions. we already have in place more quickly. BCBSNC will look at the diagnosis on the claim and how much the. procedure cost, not the customer s name on the claim. Patient. participation in any of the programs is purely optional and will have. no impact on premium rates, according to the insurer. Currently the only way for BCBSNC to get patients to use any of its. health management programs is by a doctor s referral, or if a patient. decides to call the insurance company s number. BCBSNC is. hoping to reach a broader audience through the new program. Potentially, we want to improve quality of the situation customers. are experiencing and keep the cost down for the employer and for us, Blackwelder adds. BioSignia, which had developed the software before signing the. agreement with BCBSNC, is still refining the system. Although so far. it has only licensed the software to BCBSNC, the vendor thinks the. program could be beneficial to many companies. According to Guizhou. Hu, Ph.D., vice president of research and development at BioSignia, They can use this system to identify the people [to whom] they can. provide a health promotion to help review medical costs. We want to. make this a product that can be available to many other managed care. companies.")

90

The Consumerism Grid Incentives & Rewards Personal Accounts

2nd Generation Consumerism Focus on Behavior Changes 1st Generation Consumerism Focus on Discretionary Spending 4th Generation Consumerism Personalized Health & Healthcare The Consumerism Grid 3rd Generation Consumerism Integrated Health & Performance Personal Accounts Initial Account Only Activity & Compliance Rewards Indiv. & Group Corporate Metric Rewards Specialized Accts, Matching HRAs, Expanded QME 100% Basic Preventive Care Web-based behavior change support programs Worksite wellness, safety, stress & error reduction Genomics, predictive modeling push technology Information, health coach Compliance Awards, disease specific allowances Population Mgmt, IHM, Integrated Back-to-Work Wireless cyber –support, cultural DM, Holistic care Passive Info Discretionary Expenses Personal health mgmt, info with incentives to access Health & performance info, integrated health work data Arrive in time info and services, information therapy Cash, tickets, Trinkets Health Incentive Accounts, activity based incentives Non-health corporate metric driven incentives Personal development plan incentives, health status related Wellness/Prevention Early Intervention Disease Management Information Decision Support Incentives & Rewards

91

Task #6 - Discussion on Type(s) and Use of Disease Management Programs

____________________________________________________________

92

Task #7 - Decision Support Tools

The Promise of Transparency & The “Right to Know”

93

Healthcare Consumerism – Already Active Consumers

Consumers Search Internet for Medical Content Consumers Ask Physicians for Genetic Testing Consumers Work with Providers on Personalized Health Plans Consumers Monitor and Track Their Own Medical Status Regularly Consumers and Providers Coordinate Care and Understanding through Integrated Clinical and Information Therapies

94

Decision Support Tools Survey of Attitudes

Patient decision making preferences “INFORMED” PARENTAL INTERMEDIATE SHARED DECISION MAKING PATIENT AS DECISION-MAKER 17.1% 45% 11% 22.5% 4.8% The four areas of consumer choice highlight the need for a strategic plan and the proper selection of vendor partners. Employer Role: Recognize the “consumer-preference spectrum” Provide consumer-focused decision support tools for: Choice of Health Plan Choice of Provider Choice of Treatment Current and Future Financial Considerations

95

Decision Support Tools for Consumerism

Basic Design Information Provider Selection Support HRA Fund Accounting Physician Quality Comparison Underlying PPO Plan Design Physician Cost Comparison Disease and/or Medical Management Hospital Quality Comparison HSA Fund Accounting Hospital Cost Comparison Debit/Credit Card Personal Benefit Support Care Support Plan Comparison Cost Estimator On-line Provider Directory Account Balance Provider Scheduling On-line Claim Inquiry On-line Rx Comparisons SPD On-line Patient Decision Support 24/7 Nurse Line Personal Health Management Health Risk Appraisal Health & Wellness Information Targeted Health Content Medical Record, History Health Coach

96

Decision Support Tools Employer Considerations

Employee Readiness Sophistication and orientation Internet competency and access Due Diligence Accuracy Usability Independence Stability Integration issues Targeted Clinical Support: Value-based Evidence Based Medicine Personalized Chronic Care Management Tools Consumer-Focused Stress Management

97

Consumerism – a new force

can be a force to address quality and cost variations in a given market

98

Decision Support Tools for Cost & Quality Information

Variation in Cost & Quality Hospitals – CABG* Lower LOS Lower Cost Episodes of Care Align Strategy with the “Value Purchasing” Awareness Pay for Performance Tiered Networks Regional Centers of Excellence Cost Efficiency Quality Fewer Adverse Affects Lower Complication Rates Lower Mortality * Healthshare/SelectQualityCare weighted averages

99

The Consumerism Grid Incentives & Rewards Personal Accounts

2nd Generation Consumerism Focus on Behavior Changes 1st Generation Consumerism Focus on Discretionary Spending 4th Generation Consumerism Personalized Health & Healthcare The Consumerism Grid 3rd Generation Consumerism Integrated Health & Performance Personal Accounts Initial Account Only Activity & Compliance Rewards Indiv. & Group Corporate Metric Rewards Specialized Accts, Matching HRAs, Expanded QME 100% Basic Preventive Care Web-based behavior change support programs Worksite wellness, safety, stress & error reduction Genomics, predictive modeling push technology Information, health coach Compliance Awards, disease specific allowances Population Mgmt, IHM, Integrated Back-to-Work Wireless cyber –support, cultural DM, Holistic care Passive Info Discretionary Expenses Personal health mgmt, info with incentives to access Health & performance info, integrated health work data Arrive in time info and services, information therapy Cash, tickets, Trinkets Health Incentive Accounts, activity based incentives Non-health corporate metric driven incentives Personal development plan incentives, health status related Wellness/Prevention Early Intervention Disease Management Information Decision Support Incentives & Rewards

100

Task #7 - Discussion on Type(s) and Use of Decision Support Tools

____________________________________________________________

101

Task #8 - Incentives, Rewards,

The Promise of Shared Savings Pay for Compliance & Pay for Performance “Two sides of the same coin”

102

Consumerism Incentives – Participation Based

Incentives must be participation and activity-based rather than outcomes-based. HIPAA laws prevent rewards based on health standards. The law allows incentive designs if the following requirements are met: Limit the reward to a specified amount (not to exceed between 10%-20% of the cost of employee-only coverage). Be reasonably designed to promote health or prevent disease. Be available to all similarly situated individuals. There must be a feasible alternative for those that cannot reach the health standard because of a medical condition. Inform employees that individual accommodations and alternatives are available.

. Be reasonably designed to promote health or prevent disease. Be available to all similarly situated individuals. There must be a feasible alternative for those that cannot reach the health standard because of a medical condition. Inform employees that individual accommodations and alternatives are available.")

103

Wellness Incentives – Outcomes Based

While HIPAA generally prohibits plans from differentiating benefits or premiums based on health status, employers can still design and implement wellness programs with financial incentives. Only a "bona fide wellness program" can provide a reward based on a health standard or health outcome (i.e., a low cholesterol level). To be a "bona fide wellness program," the law specifies that the program must meet four requirements: 1. Limit the reward to a specified amount (not to exceed between 10%-20% of the cost of employee-only coverage). 2. Be reasonably designed to promote health or prevent disease. 3. Be available to all similarly situated individuals. There must be a feasible alternative for those that cannot reach the health standard because of a medical condition. 4. Inform employees that individual accommodations and alternatives are available. - National Business Group on Health

. To be a bona fide wellness program, the law specifies that the program must meet four requirements: 1. Limit the reward to a specified amount (not to exceed between 10%-20% of the cost of employee-only coverage). 2. Be reasonably designed to promote health or prevent disease. 3. Be available to all similarly situated individuals. There must be a feasible alternative for those that cannot reach the health standard because of a medical condition. 4. Inform employees that individual accommodations and alternatives are available. - National Business Group on Health.")

104

Wellness Incentives – Participation Based

All wellness programs that are based on participation rather than outcomes are permitted. For example, financial incentives or premium discounts for participating in a health fair, joining a health club, or attending smoking cessation program, regardless of the health outcomes or results, are allowed. - National Business Group on Health

105

Rewards & Incentives for Smoking Cessation

The NGBH conducted a Quick Survey in December 2003 on "Smoking Cessation Incentives/Disincentives." The results from 26 respondents showed: 69% of the respondents offered discounts on annual health care premiums/contributions for non-smokers, and 15% offered another type of benefit enhancement. Similarly, 45% of the respondents offered premium discounts for employees that participated in smoking cessation/wellness programs. 57% included smoking cessation as part of a broader wellness initiative/incentives at the worksite. - National Business Group on Health

106

Incentive Awards - Three Very Different Personal Care Accounts

Flexible Spending Accounts (FSAs) – Traditional Group Plans with Use-it-or-Lose-it Health Reimbursements Arrangements (HRAs) – Employers’ choice for cash flow flexible incentive based medical plan benefit designs (best suited for self-insured groups) Health Savings Accounts (HSAs) – Employees’ choice for funded portable triple tax advantaged with “High Deductible Health Plans” (best suited for individuals and small groups) Combination Accounts – creative but confusing

– Traditional Group Plans with Use-it-or-Lose-it. Health Reimbursements Arrangements (HRAs) – Employers’ choice for cash flow flexible incentive based medical plan benefit designs (best suited for self-insured groups) Health Savings Accounts (HSAs) – Employees’ choice for funded portable triple tax advantaged with High Deductible Health Plans (best suited for individuals and small groups) Combination Accounts – creative but confusing.")

107

O/P, Low In/P, High Maternity

Using Information & Incentives To Address Wellness & Disease Management Behavioral Changes Low Users Mediu m Users High Users Very High Users No Claims Generally Healthy Acute Episodic Conditions O/P, Low In/P, High Maternity Chronic & ersistent Conditions . O/P, Low In/P,High Catastrophic % Mem 15% 48% 14% 3% 12% 4% 1% % Dollars 0% 5% 21% 20% 63% 32% 17% 56% Prevention Wellness - Lifestyle Wellness - Lifestyle Minimize Minimize Maximize Maximize Wellness - Clinical Early Intervention Wellness - Clinical

108

The Consumerism Grid Incentives & Rewards Personal Accounts

2nd Generation Consumerism Focus on Behavior Changes 1st Generation Consumerism Focus on Discretionary Spending 4th Generation Consumerism Personalized Health & Healthcare The Consumerism Grid 3rd Generation Consumerism Integrated Health & Performance Personal Accounts Initial Account Only Activity & Compliance Rewards Indiv. & Group Corporate Metric Rewards Specialized Accts, Matching HRAs, Expanded QME 100% Basic Preventive Care Web-based behavior change support programs Worksite wellness, safety, stress & error reduction Genomics, predictive modeling push technology Information, health coach Compliance Awards, disease specific allowances Population Mgmt, IHM, Integrated Back-to-Work Wireless cyber –support, cultural DM, Holistic care Passive Info Discretionary Expenses Personal health mgmt, info with incentives to access Health & performance info, integrated health work data Arrive in time info and services, information therapy Cash, tickets, Trinkets Health Incentive Accounts, activity based incentives Non-health corporate metric driven incentives Personal development plan incentives, health status related Wellness/Prevention Early Intervention Disease Management Information Decision Support Incentives & Rewards

109

Task #8 - Discussion on Type(s) and Use of Incentives & Rewards

____________________________________________________________

110

Task #9 – Viewing Healthcare Consumerism by Generations

Review of Plan Design Concepts by Generation

111

1st Generation Healthcare Consumerism

Focus on Plan Design and implementation of HRAs and/or HSAs and basic decision support tools. Impact: Discretionary Expenses Choices: Level and Type of Accounts with Plan Designs, information and Decision Support Services

112

1st Generation HRA Prototype

Employer Funds Only Notional Account Section 105 Plan Balance rolls over year to year Employer controls growth % Employer controls exit rules Vesting COBRA Retiree medical Qualified long-term care Participant responsibility Can fund thru Section 125 plan S.M.M. Insurance Deductible Gap Ensures good health Neutralizes “hoarding” Part of the Insurance Plan Health Reimbursement Arrangement Consumer education Chronic disease management Health Promotion Online tools Telephonic support Preventive Care (Insurance) Education and Decision-Support Tools

Education and Decision-Support Tools.")

113

1st Generation HSA/HDHP Prototype