Download presentation

Presentation is loading. Please wait.

1

AASHTO National Fraud Awareness Conference

Charles Groshens, Labor Compliance Supervisor Minnesota Department of Transportation Chris Smith, Special Agent USDOT, Office of Inspector General Mark Underwood, Supervisory Investigator USDOL, Employee Benefits Security Administration

2

Presentation Purpose To promote working relationships between state, local, and federal agencies to help detect and deter fraud on federally funded highway projects.

3

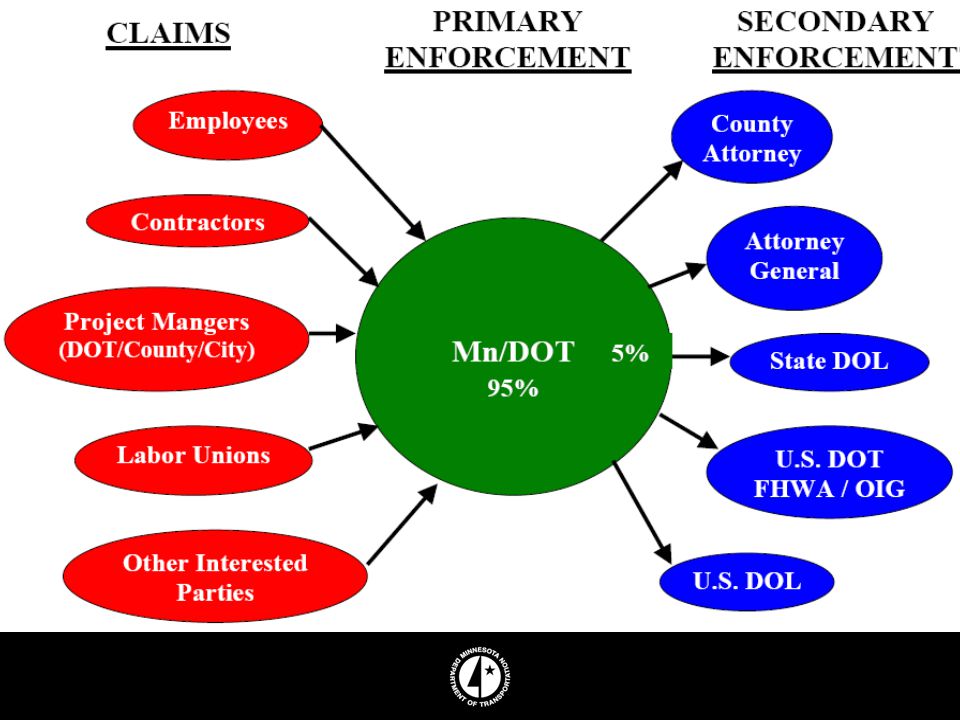

Mn/DOT Labor Compliance Unit (LCU)

")

4

LCU’s Purpose Assist contracting partners and construction contractors in administering their contracts in accordance with the Federal Davis Bacon and Related Acts, Minnesota Prevailing Wage Law and the Contract Labor Provisions.

5

LCU Staff Administration Local (County/City) Construction Projects

Charles Groshens, Supervisor Diane Cornjeo, Administrative Assistant Local (County/City) Construction Projects Clancy Finnegan, Team Leader State Highway Construction Projects Robert Richards, Investigator Ward Wheeler, Investigator Bill Segl, Field Investigator Building Projects Roxanne Farnham, Investigator

Construction Projects. Clancy Finnegan, Team Leader. State Highway Construction Projects. Robert Richards, Investigator. Ward Wheeler, Investigator. Bill Segl, Field Investigator. Building Projects. Roxanne Farnham, Investigator.")

6

Primary Services Provided

Oversight (Ensuring Compliance) Development of Contract Labor Provisions & Specifications Contract Administration Support Dispute Resolution Processes Education and Outreach Investigations and Enforcement

Development of Contract Labor Provisions & Specifications. Contract Administration Support. Dispute Resolution Processes. Education and Outreach. Investigations and Enforcement.")

7

Mn/DOT’s Contracting Partners

Mn/DOT Offices County, City Departments Other State Agencies Consulting Firms Construction Contractors

8

Investigations

9

Compliance Partners Project Engineers/Project Managers Construction Workers Contractors /Associations Unions Other Interested Parties Fringe Fund Administrators Private Sector Attorneys

10

Types of Cases Falsification of Records Fringe Benefit Contribution/Plan Issues Failure to Submit Records Labor Classification Issues Improper Payment of Wages/Overtime Contract Labor Provision Discrepancies Misclassification (Employee vs. IC)

")

12

Strategies to Prevent Fraud

13

Procedures Pre-Construction Conference

Project Reviews / Employee Interviews Daily Construction Diaries Certified Payroll & Fringe Benefit Information Payroll Tracking System Subcontractor Tracking System Educational Outreach Certification Process/Best Value Contracting

14

Mn/DOT Forms and Brochures

Payroll Certification Form (w/fringe benefit information) Request-to-Sublet Forms (w/signatures) Month-end Truck Reports Employee Wage Complaint Forms Employee Right-to-Know Cards

Request-to-Sublet Forms (w/signatures) Month-end Truck Reports. Employee Wage Complaint Forms. Employee Right-to-Know Cards.")

15

Strategies to Uncover Fraud

16

Communicate with Construction Workers

17

Primary Procedures Complaint Forms - employees, others Employee Interviews and Follow-up Employee Right-to-Know Cards Certified Payroll Audit Fringe Benefit Records Audit Review Project Documents Back Pay Check Process

18

New Technology Website: www.dot.state.mn.us/const/labor

Pre-Construction DVD/Video DOT Listserv - 50 states LCU Case Management Database System Electronic Project Data Collection Systems AASHTO Civil Rights and Labor Management System (CRLMS)

")

19

Collaborative Effort of 12 States Production Rollout in 2009

CRLMS Program Collaborative Effort of 12 States Production Rollout in 2009 Labor Fraud Detection Level 2 Payroll Rules Level 3 Payroll Rules DBE Fraud Detection Verification of DBE/Subcontractor Work Prompt Payment Verification DBE Analysis

20

Enforcement

22

Mn/DOT Enforcement Withhold Funds from Primes Reject Future Bids Default and Terminate Contract Suspend or Debar Notify Bonding Companies Refer Investigative Findings to Partners

23

State & Local Partners Labor & Industry – Administrative Procedures, Workers’ Comp, OSHA Department of Administration – Defaults, Debarments Attorney General - Administrative Hearings, Defaults, Prosecutions, Debarments County Attorney – Prosecution of State Statutes Other State Agencies – Statute Enforcement Private Sector Attorneys - Private Right-of-Action, Legislation

24

Federal Partners FHWA – Contract Compliance Actions, Debarments

USDOL Wage & Hour – Civil Davis Bacon & Related Acts Issues, Debarments USDOL Employee Benefits Security Admin. – Employee Benefit Actions IRS – Tax Fraud USDOT Office of Inspector General – Falsification of Records, Collusion, General Fraud Issues

25

Key Things To Remember Identify & develop your partnerships Select appropriate cases to refer Develop preliminary investigations Continue case development with partners Involvement with case until completion Debar after completion Exercise state options if no prosecution

26

Benefits of Partnering

Increased Case Resource Allocation Increased Investigative Staff Broader Knowledge of Regulations Additional Enforcement Remedies Additional Penalties Develop Positive Agency Relationships Positive Publicity & Future Deterrents

27

Collaborative Case Investigations Mark Underwood, Supervisory Investigator U.S. Department of Labor Employee Benefits Security Administration (EBSA)

.")

28

EBSA Field Offices

29

EBSA Responsibilities

Responsible for administering and enforcing the fiduciary, reporting and disclosure provisions of Title I of the Employee Retirement Income Security Act of 1974 (ERISA). ERISA administration is divided among the U.S. Department of Labor, the Internal Revenue Service (IRS), and the Pension Benefit Guaranty Corporation (PBGC).

. ERISA administration is divided among the U.S. Department of Labor, the Internal Revenue Service (IRS), and the Pension Benefit Guaranty Corporation (PBGC).")

30

EBSA Activities Criminal and civil investigations

Public disclosure of ERISA required annual financial reports Assistance to participants or beneficiaries regarding benefits Education, technical and compliance assistance Issuing regulations under Title 1 of ERISA Issuing interpretations under Title 1 of ERISA Granting class or individual exemptions

31

Criminal Statutes Investigated by EBSA

29 U.S.C 18 U.S.C Taft-Hartley - Section 4(a)(2)

(2)")

32

What can EBSA Bring to the Table?

Oversight Authority Expertise in ERISA, Retirement Plans and Health Plans Good Publicity Enforcement Assistance to Governmental Agencies

33

EBSA New Initiative Collaborate with governmental contracting authorities to ensure compliance with the Davis Bacon Act’s Fringe Benefit Regulations under Title 29 CFR Part 5 on federally funded construction projects The Act’s provisions require all contractors to pay workers employed directly upon the site of the work no less than the local prevailing wages and fringe benefits paid either in cash or cash & contributions to “bona fide” fringe benefit programs

34

“Bona Fide” Fringe Benefits

Benefits that are common to the construction industry Irrevocably paid directly into a fund, plan, or program Legally enforceable Communicated in writing to the employee Available to employee upon meeting plan eligibility requirements

35

Timely Deposit Fringe Benefits

Davis-Bacon Act requires that contributions to fringe benefit plans made by a contractor must be made on a regular basis, and not less than quarterly. For Collectively Bargained Plans, Plan Language may dictate sooner

36

Jay Bros., Inc. Investigations

A construction company owned by 2 brothers located in Forrest Lake, Minnesota Contracted with federal, state and local government entities Sponsored a 401k Plan funded by employee contributions and employer fringe contributions. Brothers were Co-trustees

37

Civil Investigation 1# Non-Payment of Fringe Benefits

Dates: Early Early 1998 Issue: January Third Party Administrator sends letter to Contractor about timely contributions to the 401(k) pension fund account on behalf of its employees. The TPA refers the issue to EBSA Employees filed claims with EBSA Outcome: Through voluntary compliance, contractor paid more than $28,521 to the Plan for delinquent employee contributions

pension fund account on behalf of its employees. The TPA refers the issue to EBSA. Employees filed claims with EBSA. Outcome: Through voluntary compliance, contractor paid more than $28,521 to the Plan for delinquent employee contributions.")

38

Civil Investigation 2# Non-Payment of Fringe Benefits

Dates: October Mid 2000 Issue: Employees began issuing complaints to EBSA that the company had returned to their old scheme Outcome: Through voluntary compliance, Jay Bros. paid $291,600 for delinquent contributions to the Plan.

39

EBSA/MnDOT Criminal Investigation Non-Payment of Fringe Benefits

Dates: December 2002 – December 2006 Issue: Contractor’s payroll certification statement indicated contributions were being made to a 401(k) pension fund account on behalf of its employees. Employees filed claims with both EBSA and Mn/DOT stating their online accounts showed no contributions and that the contractor once again had returned to old scheme A cooperative investigation was conducted by EBSA and Mn/DOT

pension fund account on behalf of its employees. Employees filed claims with both EBSA and Mn/DOT stating their online accounts showed no contributions and that the contractor once again had returned to old scheme. A cooperative investigation was conducted by EBSA and Mn/DOT.")

40

Investigation Outcomes

On December 6, 2006 Mark and Mike Jay, along with Jay Bros., Inc. were indicted on charges of 18 U.S.C. §2, §371, §664, §1027, and §1341. Facing 10 years of potential jail time and millions in restitution, each brother pled to 18 U.S.C Each received 5 months incarceration, 5 months work release, 3 years probation.

41

Investigation Outcomes – Jay Bros

With the felony convictions, Jay Bros., Inc., Michael Jay, and Mark Jay are now barred from being a party to any state or federal contracts In addition, the Court ordered Jay Bros. to pay for an independent outside monitor for the employee benefit plans to ensure compliance for 3 years

42

What can you provide to EBSA?

Referrals Manpower Intelligence Expertise Coordinate Prosecution/Debarment

43

Email: Underwood.Mark@dol.gov

Contact Information Mark Underwood Phone: (816)

")

44

Collaborative Case Investigations Chris Smith, Special Agent U. S

Collaborative Case Investigations Chris Smith, Special Agent U.S. Department of Transportation Office of Inspector General

45

Overview OIG Mission and Priorities

Investigation timeline of D&H Construction, Inc. Investigation timeline of U.S. v. Minnesota Valley Landscape, Inc.

46

I. OIG Mission To conduct objective audits and investigations of DOT’s programs and operations To promote economy, effectiveness, and efficiency within DOT To prevent and detect fraud, waste, and abuse in the Department’s programs To review existing and proposed laws or regulations affecting the Department and make recommendations about them To keep the Secretary of Transportation and Congress fully informed about problems in departmental programs and operations

48

OIG Investigative Priorities

Transportation Safety Aviation Motor Carrier Hazardous Material Contract Procurement and Grant Fraud Program and Employee Integrity

49

II. D&H Construction, Inc.

Company Background: Subcontractor on appr. $2M of Federal-aid-highway jobs since 1998 Exhibited a pattern of false certified payrolls Initial estimated losses were approximately $80,000

50

II. D&H Construction, Inc. Investigation Timeline

2004: February – AUSA said case looks good, do search warrant and estimated $80,000 loss ok February – Search warrant conducted on foreclosed D&H property March – Target admitted in interview that he is ultimately responsible for any wrongdoing June – Case agent was told the $90,000 estimated loss does not meet U. S. Attorneys Office (USAO) guidelines of $100K

guidelines of $100K.")

51

II. D&H Construction, Inc. Investigation Timeline

2005: March – New estimated loss calculations of $96,000. still not close to the newer USDOJ threshold which is “significantly into the $100,000” range June – Final loss calculations of $105,000 less then the now $150,000 threshold at the U.S. Attorneys Office October – AUSA stated he is inclined to decline November- SAC sent letter to USAO to reconsider

52

II. D&H Construction, Inc. Investigation Timeline

2006: January – Letter of declination received citing, among other things, that: 1) The company was no longer in business, 2) The defendant did not divert substantial assets to his own personal use, 3) The business records were disorganized which make the dollar loss and intent hard to prove, 4) The defendant could blame misconduct on another employee.

The company was no longer in business, 2) The defendant did not divert substantial assets to his own personal use, 3) The business records were disorganized which make the dollar loss and intent hard to prove, 4) The defendant could blame misconduct on another employee.")

53

Minnesota Valley Landscape, Inc.

III. U.S. v. Minnesota Valley Landscape, Inc. Company Background: Family owned landscaping company in Minnesota, David Lindstrom, Vice-President/owner One of the biggest landscaping contractors and subcontractors on MNDOT projects Prime contractor on $4.7 million in contracts from 1998 – 2003 Subcontractor on many other Federal and State funded contracts

54

III. U.S. v. Minnesota Valley Landscape, Inc. Investigation Timeline

2002: August - Case initiated and accepted at USAO 2003: June – Executed search warrant on premises July – December – Interviews conducted

55

III. U.S. v. Minnesota Valley Landscape, Inc. Investigation Timeline

2004: January – March – AUSA said she was discussing plea agreement with target June – Finalized estimated loss calculations of $400k August – Defense attorney verbally agreed to plead to an information in lieu of indictment September – AUSA became a Hennipin county judge November - USAO does not want AUSA negotiating any plea agreements

56

III. U.S. v. Minnesota Valley Landscape, Inc. Investigation Timeline

2005: January – New AUSA assigned and initiated contact with defense counsel May – Target and company plead to information 2006: June – Target and company sentenced

57

III. U.S. v. Minnesota Valley Landscape, Inc. Prosecution Summary

Plea: June 3, 2005, MVL and David Lindstrom pled to once count of Conspiracy, 18 U.S.C. § 371 for conspiring to defraud the U.S. Government and MNDOT by filing false reports for its over 150 employees over a time period of 7 years ( ) Sentence: June 20, 2006, MVL and Lindstrom ordered to pay restitution of $396, to their employees Lindstrom sentenced to 18 months in jail and a $4,000 fine

Sentence: June 20, 2006, MVL and Lindstrom ordered to pay restitution of $396, to their employees. Lindstrom sentenced to 18 months in jail and a $4,000 fine.")

58

Chris Smith, Special Agent Or visit OIG’s web site:

Questions? Chris Smith, Special Agent (312) Or visit OIG’s web site:

Or visit OIG’s web site:")

Similar presentations

Regulations Pete Gautreau, CPA Partner Danielle Witten, CPA Senior Manager.>")