Download presentation

Presentation is loading. Please wait.

1

Insurance against terrorism risks

OECD-IAIS-ASSAL IV Conference on insurance regulation and supervision in Latin America Session 3: Insurance against terrorism risks Cécile Vignial OECD

2

Ministerial mandate on terrorism insurance

It requests policy analysis and recommendations on: the definition of terrorism risks the coverage of terrorism risks, with an assessment of the respective role of the insurance (and reinsurance) industry, the financial markets and the government the special case of mega-terrorism risks

industry, the financial markets and the government. the special case of mega-terrorism risks.")

3

1. Defining terrorist acts for indemnification purpose

4

1.1. Focus of OECD work on the definition of terrorism

This work does not aim at a general definition of terrorism acts, but at an approach of the concept of terrorism for cover purposes; This work does not aim at enunciating a single and rigid definition for all Member countries, but at identifying key elements of definition on which OECD countries could agree. The adoption of such definition criteria is not meant to be binding.

5

1.2. Defining terrorism: what for?

The events of 11 September 2001 made Member country insurers and reinsurers aware of the need to redefine and assess their commitments with respect to terrorism risk. In many States, the risk of terrorism was generally not cited explicitly in contracts, and cover for it was extended at no additional cost, generally as part of the protection against fire. Since 11 September, exclusion or coverage is made explicit, and their precise scope is specified.

6

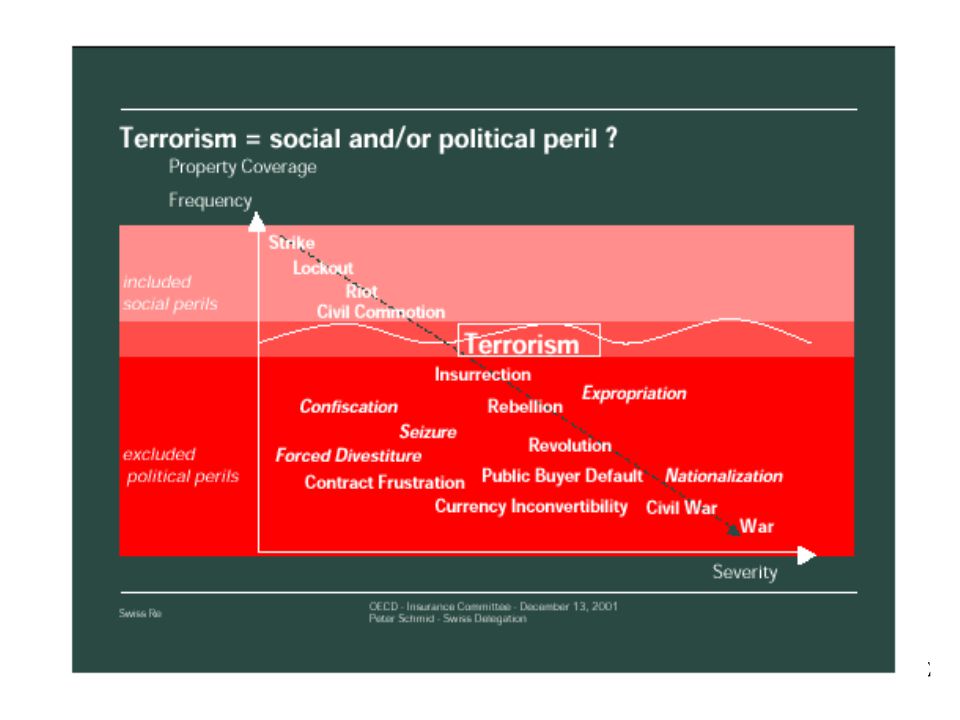

It is important to differentiate between terrorist acts and other manifestations of violence and, in particular, acts of war, the latter being systematically excluded from insurance cover. “Terrorism lies on the borderline between political perils, considered as uninsurable by (re)insurers, and socio-political perils, ordinarily covered by those same (re)insurers” (see SR graph)

insurers, and socio-political perils, ordinarily covered by those same (re)insurers (see SR graph)")

8

1.3. Elements of definition of terrorism acts (see annex 1)

The aim for which terrorism acts are perpetrated A terrorist act is committed: with the intention (or effect) of influencing and provoking fear in all or part of the population The broad psychological repercussions of a terrorist act may transcend the shock inflicted on its immediate victims. in support of a political, religious or ideological goal.

of influencing and provoking fear in all or part of the population. The broad psychological repercussions of a terrorist act may transcend the shock inflicted on its immediate victims. in support of a political, religious or ideological goal.")

9

Terrorism is manifested by:

The means used Terrorism is manifested by: a violent or dangerous act, i.e. causing serious harm to human life, tangible or intangible goods. The qualification of “serious” implies that damages are of a certain magnitude/significance. This notion is important to differentiated acts of terrorism from acts of vandalism for instance. “Dangerous” may apply to acts that are not violent as such, although they could potentially inflict grievous harm on the life, safety or health of persons, or on the environment. Cyber attacks or the pollution of ground water illustrates this point. a threat of such act entailing severe damage

10

Certification In various Member countries (France, the UK, Northern Ireland, the US), another element is added to the definition of a terrorist act: its certification by a governmental representative, which can usually not be subject to appeal to be effective. Such certification is certainly a guarantee of seriousness in the examination of the nature of the act, although the certification may also induce some political bias.

, another element is added to the definition of a terrorist act: its certification by a governmental representative, which can usually not be subject to appeal to be effective. Such certification is certainly a guarantee of seriousness in the examination of the nature of the act, although the certification may also induce some political bias.")

11

1.2. Elements of a definition of terrorist acts that can be indemnified

Among the acts defined as terrorist acts according to the criteria listed above, decision makers in the insurance sector need to identify those for which coverage can be made available, i.e. : acts meeting the criteria for insurability, compensable acts, or acts that will be indemnified even though they do not meet the criteria for insurability.

12

1.2.1. Acts meeting the criteria for insurability

acts that are technically insurable, i.e. that meet the criteria of: assessibility (probability and severity of losses must be quantifiable) randomness (the time at which the insured event occurs must be unpredictable, and the occurrence itself must be independent of the will of the insured) mutuality (numerous persons exposed to a given hazard must join together to form a risk community within which the risk is shared and diversified)

randomness (the time at which the insured event occurs must be unpredictable, and the occurrence itself must be independent of the will of the insured) mutuality (numerous persons exposed to a given hazard must join together to form a risk community within which the risk is shared and diversified)")

13

acts that are economically insurable, i.e. meeting the criteria of :

capacity: their magnitude does not exceed the capacity of the private (re)insurance market, or the capacity of a mix of private/public multi-layer mechanisms when it exists. If a specific terrorism insurance scheme is to be established, the scope of intervention of the various “layers”, reflecting their respective capacity, will need to be defined through quantitative thresholds. The nature of the thresholds, their quantitative level, and the basis on which they should be calculated, should also be defined ex ante.

insurance market, or the capacity of a mix of private/public multi-layer mechanisms when it exists. If a specific terrorism insurance scheme is to be established, the scope of intervention of the various layers , reflecting their respective capacity, will need to be defined through quantitative thresholds. The nature of the thresholds, their quantitative level, and the basis on which they should be calculated, should also be defined ex ante.")

14

Defining quantitative risk thresholds (see annex 2)

nature of threshold: the amount of the financial damage incurred is usually the criterion enforced amount of the threshold: it reflects the amount of losses insurable by a given coverage mechanism and ultimately the limit of global national capacity above which a risks would need to be excluded as currently uninsurable. Risks can be classified according their magnitude, on which depends the type of coverage mechanisms or “layer” to be triggered when claims arise (privately insurable terrorism risks, risks insurable through national private/public partnership (when existing), risks currently uninsurable although they can be compensated through State support, risks that can currently not be indemnified).

, risks currently uninsurable although they can be compensated through State support, risks that can currently not be indemnified).")

15

Minimum amount: terrorism insurance schemes typically cover risks above a certain critical mass

ex: under the US Terrorism Risk Insurance Act for instance, an act must cause at least $5 million in damage to be covered by the programme. In France, GAREAT covers only risks of an insured value above Euro 6 million. In Germany, Extremus AG covers risks of and insured value above Euro 25 million.

16

Maximum amount: at the other end of the risk spectrum, the maximum amount of insurable losses represents the upper limit of insurability at a given moment in time, defined as the available capacity of the private market to cover terrorism risk, or, in case of State guarantee, as the estimated maximum financial involvement that the State is able or willing to supply for the compensation of losses entailed by terrorism, without endangering national economic stability. This upper limit may for instance correspond to the $100 bn per year set in the USA for State involvement, or to the Euro 10bn limit fixed in Germany.

17

Basis on which the threshold is calculated

The various thresholds differentiating the risks according to their magnitude can be established on different basis: event vs time period, single company vs entire market, upon each company performance, as measured by its market share or amount of premiums collected, etc.

18

price: premiums are both actually fair and affordable

Further to recent developments on some OECD insurance markets, the relationship between premium rates and insurability strikes out as an issue more complex and long-lasting than could have been expected. Ex: current difficulties encountered on the US market further to the introduction of compulsory terrorism insurance through the TRIA

19

Acts that are legally/regulatory insurable:

they have been identified by regulatory authorities as insurable/insurance against this risk is made compulsory. In this case only, a risk may be insurable while the other criteria may not be met. According to the criteria above, insurers and national terrorism coverage schemes when existing have defined which types of losses/business lines they are able/willing to insure, establishing a qualitative segmentation of risks

20

Establishing a qualitative classification of risks (see annex 2)

Such classification will define which lines of business the various insurance coverage mechanisms can cover. Individual insurers, but also national terrorism coverage schemes, are still far from covering all types of losses. Interestingly, the various national schemes are not always covering the same lines of business. The exclusion of certain insurance lines, such as third party liability, has been lengthy debated in several countries. Worker compensation (covered even in case of war under the US scheme, but excluded by the UK Pool Re for instance), or bodily injury, are not treated the same way across borders. Lastly, the extend of coverage may also evolve in a given country: ex: Pool Re for nuclear risks coverage

, or bodily injury, are not treated the same way across borders. Lastly, the extend of coverage may also evolve in a given country: ex: Pool Re for nuclear risks coverage.")

21

Acts meeting the criteria for compensation (but failing to meet the criteria for insurability): Compensation by the State: their magnitude does not exceed the maximum financial involvement that the State is able or willing to supply, above insurance coverage, for the compensation of losses entailed by terrorism Other compensation mechanisms: technical characteristics of terrorism acts may allow them to be covered through other instruments (e.g. bonds placed on capital markets).

.")

22

2. Coverage of terrorism risk

23

Three types of actors may be involved in the coverage of terrorism risks:

the private insurance and reinsurance market the States financial markets

24

2.1.Ups and Downs of private sector involvement in terrorism coverage

Evolution of the role of the private sector Terrorism risks potentially comprise events of such magnitude and diversity that, after the heavy losses incurred in the wake of the attacks of 11 September 2001, some insurers and reinsurers have preferred to adopt a prudent stand and exclude them altogether as uninsurable or restrict drastically the cover while substantially raising the level of premium. This trend has been slow down in 2002, to try to stretch the limits of coverage, make terrorism risks, as far as possible, insurable, and, for some private operators, to take advantage of a potentially highly profitable niche.

25

factors underlying changes

technical evolutions ex: encouraging progress in terrorism risk modelling: risk modeller agencies (like Applied Insurance Research (AIR), Eqecat and RMS), among other actors, have developed sophisticated models that they sell to insurers around the globe capacity building it has been achieved through re-capitalisation of terrorism activities, creation of new ventures, or establishment of private pools (e.g. Austria)

, Eqecat and RMS), among other actors, have developed sophisticated models that they sell to insurers around the globe. capacity building. it has been achieved through re-capitalisation of terrorism activities, creation of new ventures, or establishment of private pools (e.g. Austria)")

26

Change in the conditions under which insurers and reinsurers are willing to assume terrorism risks (SR) coverage conditions, wordings and clauses: update the definition of risk, covered perils, excluded perils. Apply sublimits and specify named perils to restrict the scope of cove ex: aviation activities, transport, high-risk property, credit loan, pricing and underwriting: develop more refined pricing methods and procedures, adjusted to risk type, country, region, loss experience and expectancy. risk and capital management. For example: extend scenarios and capacity management procedures to make allowance for possible terrorist attacks, enhance analysis for correlations between lines of business and between underwriting/investment/credit/operational risks, develop alternative risk transfer products and systems addressing terrorism risk.

27

2.2. The crucial role of governments in terrorism coverage

Rationale for government intervention market failure, given the potential magnitude of risks and the uncertainty regarding their technical characteristics political and social consequences of terrorism attacks impact on the economy: the government may have to intervene in case of major disruptions in key economic sectors

28

The wide scope of government tools (see annex 2)

indirect role: promotion of market mechanisms: -- tax incentives for terrorism provisioning, specific forbearance measures, changes in the accounting of assets, imposing special levies on insurance premiums -- making such insurance mandatory under specific criteria guided by economic efficiency. Terrorism risks falls into the risk categories that may require the insurance compulsion (severity could be particularly great, with a large number of innocent persons being harmed because of a single event) Some OECD countries are already applying compulsory coverage of terrorism at least for certain lines of business: e.g. Belgium, France (for casualty & property insurance), Spain, and the US.

Some OECD countries are already applying compulsory coverage of terrorism at least for certain lines of business: e.g. Belgium, France (for casualty & property insurance), Spain, and the US.")

29

Risk Sharing within government support

self-insurance (risk retention) by enterprises and individuals co-reinsurance supplied by members within the pool (or reinsurance supplied by the specialist reinsurance company) insurance high reinsurance supplied by government(s) loss frequency back-stop guarantees provided by government(s) low low high loss severity

by enterprises and individuals. co-reinsurance supplied by members within the pool. (or reinsurance supplied by the specialist reinsurance company) insurance. high. reinsurance supplied by government(s) loss. frequency. back-stop guarantees provided by government(s) low. low. high. loss severity.")

30

Direct role -- subsidiary role ex: in Spain, the State, through the Consorcio de Compensacion de Seguros, plays a subsidiary role if private insurers are not able to cover the risk. -- loan facilities to face immediate liquidity problems -- guarantee: the State intervenes as reinsurer of last resort ex: GAREAT, Pool Re, Extremus AG

31

Country experience (see annex 2)

While many OECD countries (apart from Spain and the United Kingdom) did not set-up in the past specific mechanisms to deal with terrorism insurance, most of them have reassessed their position in the light of the 11th September events. State backing, and the enforcement of private and public/private mechanism specifically devoted to the coverage of terrorism risks, has proven in various countries to be is a key condition for private player’s to re-enter the terrorism market and be involved above certain level of risk exposure.

did not set-up in the past specific mechanisms to deal with terrorism insurance, most of them have reassessed their position in the light of the 11th September events. State backing, and the enforcement of private and public/private mechanism specifically devoted to the coverage of terrorism risks, has proven in various countries to be is a key condition for private player’s to re-enter the terrorism market and be involved above certain level of risk exposure.")

32

2.3. Financial markets: a viable alternative to palliate to capacity shortage?

After September 2001, terrorism risk securitisation onto global debt or equity markets appeared as a promising solution to (re)insurance capacity shortage The launching of cat bonds in the mid 90s provided a model for the expansion of a possible the coverage of natural catastrophes (bond securitisations / Californian Earthquake authority)

insurance capacity shortage. The launching of cat bonds in the mid 90s provided a model for the expansion of a possible the coverage of natural catastrophes (bond securitisations / Californian Earthquake authority)")

33

However, against certain expectations, terrorism risk securitisation has not had the kick-start anticipated from the hardening of the conventional market, and many obstacles still prevent its development. In particular: structuring such securities can prove still more expensive than reinsurance While investors are reluctant to buy a product they are not familiar with, especially when the assessment of the underlying risk is highly complex The continued hardening of reinsurance market may eventually give a chance to the development of ART markets, bearing in mind that it generally takes more than one cycle for new solutions to become successful.

34

2.4. Towards multi-pillar risk-sharing mechanisms

Multi-layer risk-sharing mechanisms are a common solution to extend capacity in insurance markets. Possible State and financial market intervention can to be added to classical models of co- and re- insurance in the case of terrorism risk coverage.

35

MULTI PILLAR RISK SHARING MECHANISM TO COVER TERRORISM RISKS

FIFTH LAYER DOMESTIC GOVERNMENT FOURTH LAYER REINSURANCE FINANCIAL MARKETS THIRD LAYER INSURANCE POOL SECOND LAYER INSURERS SELF-INSURANCE FIRST LAYER INSURED (fair level of premium + deductibles, ensuring better prevention and control of moral hazard )

")

36

Options for Risk-Sharing Networks

risks facing enterprises and individuals self -insure (retain risk) enterprises and individuals risk transfer through securitization risk transfer through insurance national insurance market reinsurance reinsurance reinsurance pool or specialist reinsurance company risk transfer through securitization national and international reinsurance markets can provide debt capital can raise new equity capital or subordinated debt reinsurance and guarantees or can provide debt capital to specialist reinsurance company risk securitization vehicles international agencies, e.g. World Bank can raise new equity capital or subordinated debt government(s) risk securitization onto global debt or equity markets can raise new debt capital can raise new debt capital national and global capital markets

enterprises. and individuals. risk. transfer. through securitization. risk transfer through insurance. national insurance market. reinsurance. reinsurance. reinsurance pool or specialist reinsurance company. risk. transfer. through securitization. national and international. reinsurance. markets. can provide debt capital. can raise new equity capital or subordinated debt. reinsurance. and. guarantees. or can provide debt capital to specialist reinsurance company. risk. securitization. vehicles. international agencies, e.g. World Bank. can raise new equity capital or subordinated debt. government(s) risk securitization. onto global debt or equity markets. can raise new debt capital. can raise new. debt capital. national and global capital markets.")

37

3. Compensation for damage caused by mega-terrorism

38

3.1. Definition of mega terrorism

Mega terrorism refers to risks beyond the current capacity of the insurance industry and the government in a determined country since they involve damages potentially exceeding a country financial capacity - or willingness - to palliate to market failure and to indemnify for losses, without endangering the national economy. Such “mega risks” could only be covered if an international mechanism was to be created, involving States last resort capacity. It would basically aim at adding an international layer to current coverage arrangements and pre-organise financial aspects of international solidarity in case of attack.

39

3.2. Why preparing for mega terrorism

Increasing magnitude of terrorism attacks Over the past few decades, dozens of aggressive movements have emerged espousing varieties of nationalism, religious fundamentalism, fascism and apocalyptic millenarianism. E.g. aircraft hijackings in the 1970s, the 1983 suicide attack on US and French contingents of the multinational peacekeeping force in Beirut, the 1993 attack on the World Trade Center, the 1993 bombing in the City of London, the 1995 sarin gas attack in the Tokyo metro and the 1996 bombing of a US military compound in Saudi Arabia, which put terrorism at the forefront of the subsequent G7 summit. Recent terrorist attacks (Oklahoma City, Khobar Towers, US Embassies in Kenya and Tanzania) have been increasingly more destructive and claimed a growing number of victims. The 11 September attacks exceeded in scale and audacity those of previous events. Yet, intelligence and military experts actively prepare protection against attacks on an even broader scale.

have been increasingly more destructive and claimed a growing number of victims. The 11 September attacks exceeded in scale and audacity those of previous events. Yet, intelligence and military experts actively prepare protection against attacks on an even broader scale.")

40

Assessing the economic impact of such a terrorist attack is nearly impossible – it could in any case exceed the capacity of many individual states Ex: An attack against New York City using a nuclear weapon could leave most of the metropolitan area uninhabitable for years. The direct impact would reduce the country’s production potential by about 3 per cent, that is, the equivalent of a small OECD country’s GDP. New terrorism is international by nature: no country is protected from new forms of terrorism, and new attacks could target or contaminate many countries simultaneously Ex: explosion of nuclear device or release contagious viruses in a populous metropolitan area

41

3.3. Possible models ICAO scheme for the aviation sector:

the ICAO aims at creating a non-profit insurance company which would provide liability coverage for war risks of up to USD 1.5 billion, subject to a franchise of USD 50 million. This approach would require premiums to be paid by each party insured in order to constitute a reserve to pay claims for losses covered by the policies. It also provides for guaranteed reinsurance to be given to the insurance company by the participating States. This scheme has not yet been approved by a sufficient number of countries to be implemented; CEA proposal for a European insurance mechanism: this November 2001 proposal aimed at a coordinated European mechanism combining local public resources at EU or EEA level; Paris Convention and the Brussels Supplementary Convention providing for the compensation of losses resulting from the peaceful use of nuclear energy – probably the most useful model at this stage

42

3.4.Pending issues Many issues have to be solved when considering the implementation of a system of international solidarity definition of terrorism acts to be covered conditions of access definition of losses covered (life/property/environment - geographical coverage) criteria for contribution by parties to the agreement (GDP/population,etc.) procedure for submitting contributions/ competent tribunals dispute settlement procedure duration of the agreement Why to join the agreement if a country has the feeling that there is no major terrorism risk? Is is not too costly for small countries? How to fix the contributions: --intervene above a certain ceiling only --cap their contributions

criteria for contribution by parties to the agreement (GDP/population,etc.) procedure for submitting contributions/ competent tribunals. dispute settlement procedure. duration of the agreement. Why to join the agreement if a country has the feeling that there is no major terrorism risk Is is not too costly for small countries How to fix the contributions: --intervene above a certain ceiling only. --cap their contributions.")

43

Conclusion There is no ideal risk-sharing model to cover terrorism: each cover arrangement should be designed to address the specificity of a national market according to pre-determined public policy goals. However, in defining how terrorism risk should be covered, decision makers -be they private sector or governmental representatives- should take into account several underlying principles in order to provide the most adequate cover and respect all parties involved in this endeavor. Some of these objectives have been inter alia highlighted by the working group on Pool Re's reform

44

Adopt: a long-term perspective to terrorism coverage defining and separating the short-term needs and longer-term challenges relative to the coverage of terrorism; a flexible approach: the form of terrorism events may evolve in time, as well as their insurance market coverage. Coverage should be able to adapt to these new situations or be reevaluated; a balanced approach between the role assigned respectively to the insurance industry, the financial markets and the state as reinsurer of last resort, while avoiding crowding out effects for the private sector that could discourage the adaptation of insurance markets to terrorism risks; avoiding and properly assessing the negative externalities stemming out of insufficient terrorism coverage for the rest of the economy.

Similar presentations

as implemented by the U.S. Department.>")