Download presentation

Presentation is loading. Please wait.

1

Sustainability in Industry: Benchmarks and Road Maps

Darlene Schuster Director, Institute for Sustainability November 2008

2

Acknowledgements Calvin Cobb, Chair Institute for Sustainability Subhas Sikdar, Chair Instiute for Sustainability 2008 Golder and Associates Beth Beloff, Dicksen Tanzil, Abigail Martin Industry Representatives to Center for Sustainable Technology Practices (CSTP) Sustainability Guide Task Group Carol English, Cytec Industries, Inc. Charlene Wall, BASF Dave Taschler, Air Products Lafayette College Professor Javad Tavakoli

Sustainability Guide Task Group. Carol English, Cytec Industries, Inc. Charlene Wall, BASF. Dave Taschler, Air Products. Lafayette College. Professor Javad Tavakoli.")

3

The Institute for Sustainability

A community of sustainability “practitioners” Companies (Center for Sustainable Technology Practices) Professionals—industry and academic (Sustainable Engineering Forum) Youth (Youth Council for Sustainable Technology Practices) Organized under the American Institute of Chemical Engineers (AIChE) Professional membership organization Non-profit 501c(3)

Professionals—industry and academic (Sustainable Engineering Forum) Youth (Youth Council for Sustainable Technology Practices) Organized under the American Institute of Chemical Engineers (AIChE) Professional membership organization. Non-profit 501c(3)")

4

Overview of the Institute

IfS Practitioners, students & companies Sustainability Engineering Forum 745 AIChE members 950 additional non- AIChE members $25 dues Center for Sustainable Technology Practices Industry Group 10 companies, growing Air Products, BASF, Cytec, Dow, FMC, Honeywell Interface Inc. , Middough (WalMart) Youth Council on Sustainable Sciences & Technologies Partnership w/ SustainUS 9750 students, growing Incorporates sustainability into undergrad research, sponsors awards & student chapters Projects of IfS 1.Sustainability Index Purpose of financial guidance, benchmarking & management Differential to other indices Potential for high profitability 2. ICOSSE Aug 09 Mission: to serve the needs of and influence the efforts of professionals, academes, industries, and governmental bodies that contribute to the advancement of sustainability and sustainable development.

Youth Council on. Sustainable Sciences. & Technologies. Partnership w/ SustainUS students, growing. Incorporates sustainability. into undergrad research, sponsors awards & student. chapters. Projects of IfS. 1.Sustainability Index. Purpose of financial guidance, benchmarking & management. Differential to other indices. Potential for high profitability. 2. ICOSSE Aug 09. Mission: to serve the needs of and influence the efforts of professionals, academes, industries, and governmental bodies that contribute to the advancement of sustainability and sustainable development.")

5

Triple Bottom Line: A Business View of Sustainability

6

“Sustainability is a path of continuous improvement, wherein the products and services required by society are delivered with progressively less negative impact upon the Earth” Defined by AIChE Institute for Sustainability November ‘04-July ‘05 Grassroots Project, Earl Beaver, Chair IFS

7

Ecosystems Modeling Industrial Ecology Credit Trading Design Watershed

Protection Industrial Ecology

8

How is your Company’s Sustainability Performance Viewed?

By the community? By your shareholders? By your customers? Versus your peers? The AIChE Sustainability IndexTM

9

How is your Company’s Sustainability Performance Enhanced?

Via the value chain? by corporate decision making? by job function? The CSTP Sustainability Roadmap A Process for Sustainable Decision Making

10

Purpose of a Sustainability Index

Investment guides Ethical investment/SRI Long-term return (“stock picks”) Stock market indices Stakeholder ratings Benchmarks for company management

Stock market indices. Stakeholder ratings. Benchmarks for company management.")

11

Examples of Financial SI’s

Investment Guide? Market Index? Manage-ment Benchmark? Consult to Companies? DJSI FTSE- 4Good GS- Sustain Innovest

12

An Example The Dow Jones Sustainability Index (DJSI)

Investment guide Includes only companies that meet DJSI criteria – governance, transparency, accountability Stock market index Track market performance of DJSI components Subset of corresponding broader indexes DJSI World, subset of Dow Jones World Index Benchmarking Inclusion, being sector leader Consulting services through SAM – analysis and recommendations for companies who want to be included, improve ratings 12

13

Used for Market Tracking

Source: SAM, Dec 2007

![]()

14

Reporting of Financial SI’s

Dow Jones Sustainability Indices Inclusion (in or out), ‘Supersector Leaders’ Individual company scores & analysis – to licensees only FTSE4Good Inclusion (in or out) GS SUSTAIN Ratings: leaders, average, and laggards Analysis for sector leaders energy, mining & steel, food & beverage, pharmaceutical, alternative energy, environmental technologies, biotechnology Innovest Top companies – sector leaders & Global 100 list Ratings (AAA to CCC) and analysis, for investor clients only 14

, ‘Supersector Leaders’ Individual company scores & analysis – to licensees only. FTSE4Good. Inclusion (in or out) GS SUSTAIN. Ratings: leaders, average, and laggards. Analysis for sector leaders. energy, mining & steel, food & beverage, pharmaceutical, alternative energy, environmental technologies, biotechnology. Innovest. Top companies – sector leaders & Global 100 list. Ratings (AAA to CCC) and analysis, for investor clients only. 14.")

15

What a Company Can Get from Financial SI’s

Dow Jones Sustainability Indexes Benchmarking with peers, advisory FTSE4Good “Guidance and support” for companies to work towards inclusion in FTSE4Good – through EIRIS GS SUSTAIN (none specific to sustainability and its ESG analysis) Innovest “Confidential custom benchmarking studies” for companies – operational efficiency and business opportunities per peer analysis 15

Innovest. Confidential custom benchmarking studies for companies – operational efficiency and business opportunities per peer analysis. 15.")

16

Concept of the AIChE Sustainability Indexsm

Based on the Wright Killen Refinery Survival Index (Oil and Gas Journal) Meant to fill a gap: Relies more heavily on quantitative performance indicators Provides a heavier weighting applied to various indicators of safety and environmental performance and to technological innovation towards SD Available to range of sectors, company size The scoring: robust methodology designed to account for subjectivity in a transparent manner. Designed to avoid the ‘black box’ problem of other indices Intended for executives and directors to manage company business lines Global, initially focusing on major chemical companies Publication remains silent on individual company ratings Companies find it useful to benchmark themselves relative to a set of companies Research funded by United Engineering Foundation

Meant to fill a gap: Relies more heavily on quantitative performance indicators. Provides a heavier weighting applied to various indicators of safety and environmental performance and to technological innovation towards SD. Available to range of sectors, company size. The scoring: robust methodology designed to account for subjectivity in a transparent manner. Designed to avoid the ‘black box’ problem of other indices. Intended for executives and directors to manage company business lines. Global, initially focusing on major chemical companies. Publication remains silent on individual company ratings. Companies find it useful to benchmark themselves relative to a set of companies. Research funded by United Engineering Foundation.")

17

Status Needs analysis completed in the Fall of 2005

Pilot study performed in 2006 Launch Methodology Published June ‘07 Index for Fortune 500 CPI November ’07 Additional pilots underway for Engineering Construction and Energy/ Power Sectors Requests to explore development of index from water resources, textile chemical manufacturers Research funded by United Engineering Foundation

18

Advisory Panel Mission Advisors:

to protect and promote the soundness, credibility and utility of the AICHE Sustainability Index™ Advisors: International financial community Industrial sector experts Media Non-governmental Organizations (NGO’s)

")

19

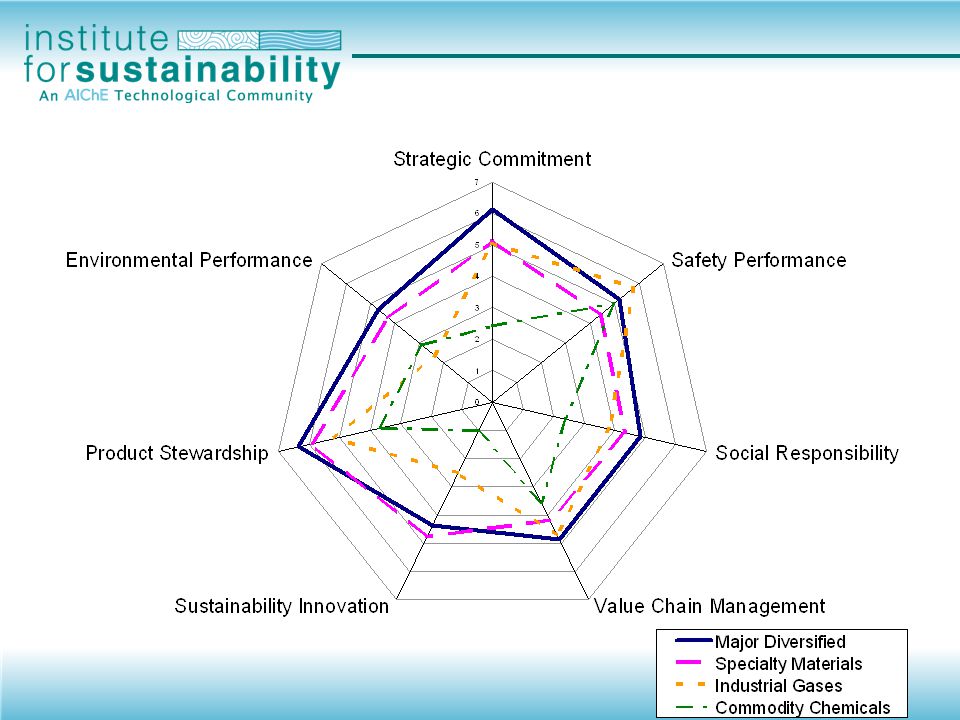

AIChE Sustainability IndexTM for the Chemical Industry November 2007

Gray Shading = Ranges of individual company scores Blue Line = Simple average of 11 representative companies

20

AIChE Sustainability IndexTM for the Chemical Industry November 2007

24

AIChE Sustainability Index for the Chemical Industry (Simple Average) September 2007

Gray Shading = Ranges of individual company scores

25

The AIChE Sustainability IndexTM

Fall 2007 Notes: For Sustainability Index methodology and data sources, see CEP, June 2007, pp Companies included in the assessment are ____, ___, ____, … Strategic Commitment Environmental Performance Product Stewardship Safety Innovation – meeting social needs Value-Chain Management 4.1 4.3 4.3 4.0 3.8 3.9

26

Elements of the Index Strategic Commitment Safety Performance

Environmental Performance Resource Use Waste & Emissions Environmental liabilities Product Stewardship Innovation Product and service innovation – meeting social needs Process innovation Value Chain Management EHS Management Supply Chain Management Stakeholder Engagement These are the new screening criteria Golder proposes based upon available information.

27

Unique Elements Strategic Commitment Safety Performance

Environmental Performance Resource Use Waste & Emissions Environmental liabilities Product Stewardship Innovation Product and service innovation – meeting social needs Process innovation Value Chain Management EHS Management Supply Chain Management Stakeholder Engagement These are the new screening criteria Golder proposes based upon available information.

28

Calculations Use Existing Data Sources

Company reports Annual Corporate Reports SEC 10-K Filings Sustainability/EHS Reports Government Agencies EPA CSB U.S. Patent & Trademark Office Company websites Media reports Independent NGO reports

29

Value Chain Management Details

Environmental Management System Corporate level environmental management system – ISO14001, RC-14001, RCMS or EMAS certified Facility level environmental management system – ISO14001, RC-14001, RCMS or EMAS certified % certified Indication of presence/current effort Supply Chain Management Presence of a supply chain policies and procedures related to sustainability Sustainability evaluation required of suppliers Audits of supplier practices Policies extended to suppliers’ suppliers

30

Value Chain Management Ideal Score of 7

Value-Chain Management—Project Orientation System in place to manage sustainability performance in operations and project delivery System in place to manage sustainability performance of sub-contractors and other suppliers Significant number of projects demonstrate excellence in long-term environmental and social performance Value-Chain Management—Product Orientation Externally recognized environmental management system in-place at the corporate level and at all major facilities Presence of company-wide supplier management policies and procedures related to sustainability, applied and enforced to all supply-chain entities with potentially significant impacts

31

AIChE Sustainability IndexTM

Drills down, but remains broad enough Based on public data Targeted for managers and corporate executives, not investors Focused on Environmental – performance metrics Safety – performance metrics (workplace, process) Product stewardship – mgmt system, history Value chain management – mgmt system Sustainability innovation – initiatives, tools, results Social performance and strategic management also covered Less than other indexes Benchmarked to peers and best practices

Product stewardship – mgmt system, history. Value chain management – mgmt system. Sustainability innovation – initiatives, tools, results. Social performance and strategic management also covered. Less than other indexes. Benchmarked to peers and best practices.")

32

How is your Company’s Sustainability Performance Viewed?

By the community? By your shareholders? By your customers? Versus your peers? The AIChE Sustainability IndexTM

33

How is your Company’s Sustainability Performance Enhanced?

Via the value chain? by corporate decision making? by job function? The CSTP Sustainability Roadmap A Process for Sustainable Decision Making

34

Supported by member companies

CSTP formed in 2004 as part of the AIChE’s Institute for Sustainability Supported by member companies Tailored collaborative projects and pre-competitive research Monthly sustainability education “virtual” sessions Utilize members to conduct project work Project: Development of Case studies and evaluation of Decision Support Tools in industrial Use Project: Focus Groups for Survey of Sustainability in the Chemical Industry (PriceWaterhouse Coopers) Project: R&D Checklist for Sustainability Project: Sustainability Roadmap

Project: R&D Checklist for Sustainability. Project: Sustainability Roadmap.")

35

Background Project: EPA Grant 2005: Case Studies of Industry Decision Support tools for Sustainability Identified gaps & challenges Great tools, not widely used Need for better integration of sustainability into business processes Understand context of management and technology decisions along value chain Understand key decision points, relevant SD considerations, and key functional areas/decision makers involved Need to understand the broader set of tools, approaches, and other resources to help integrate SD into the organization

36

Roadmap Structure & Organization

Composite Checklist – Questions to guide sustainability consideration at each value-chain stage Main Page: Overview Key corporate functions & resources Summary Table – Form to record answers, action plans, responsible parties, status and documentation Scoring Framework Highlight issues and opportunities, updated at each stage

37

Potential for Improvement SD Roadmap Summary Table

192 Key Sustainability Questions Where to ask them during process and product development Who should be included in the “answers?”

38

SD Considerations Resource Use Environmental Impact Health & Safety

Energy use, material intensity, water use, land use Environmental Environmental Impact GHG emissions, air emissions, solid waste, (pollutant effects) Health & Safety Toxic reduction, hazards, process safety Social Societal Impact Workers’ well-being, local community impacts/QOL, global societal impacts/contributions Economic Impact Financials along value-chain (corporate, customers, …) Econ. Management Internal process, value-chain partnership, stakeholder engagement Business Perspective Business Strategy Alignment with business strategy, core values & competencies, market & regulatory drivers

Health & Safety. Toxic reduction, hazards, process safety. Social. Societal Impact. Workers’ well-being, local community impacts/QOL, global societal impacts/contributions. Economic Impact. Financials along value-chain (corporate, customers, …) Econ. Management. Internal process, value-chain partnership, stakeholder engagement. Business Perspective. Business Strategy. Alignment with business strategy, core values & competencies, market & regulatory drivers.")

39

Resource Use Energy Use

How energy intensive is the feedstock? Which feedstock materials are the most energy intensive and are there energy-efficient alternatives? Can the feedstock be produced using renewable energy? Has energy consumption been optimized for the selected process? Can any byproducts be used as energy ? Will energy be saved or conserved in the distribution of this product vs. alternative products/processes? Will the use of this product save or conserve energy for the customer versus alternative products/processes? Would there be opportunities to use renewable energy in the production, distribution or use of the product/process? Are there alternatives for more energy efficient transportation/distribution system? Could the product be reused/recycled to reduce life-cycle energy use? Water Use How water intensive is the feedstock? Which feedstock materials are the most water intensive and are there water-efficient alternatives? Has water use been optimized for the selected process as both a reagent and processing medium? Have water source alternatives been evaluated and considered? Have water quality considerations been aligned with use requirements? Will the product/process be more water efficient in production and use? Has water been reused and recycled appropriately? Have equipment and technology alternatives been evaluated for optimizing water use?

40

Elements of the Roadmap

Value Chain Stages Corporate Functions Corporate functions to involve or consult at each value chain stage. (RACI Chart) Sustainability considerations Tools & Resources

Sustainability considerations. Tools & Resources.")

41

Engaging Key Corporate Functions

Value Chain Stages Corporate Functions Corporate functions to involve or consult at each value chain stage Sustainability considerations Tools & Resources Value Chain Axis Business Strategy Development Upstream Input R&D Idea Generation Concept Scoping Definition Development Scale up Commercialization Production Distribution Industrial Consumer Use Customer Use End of life Facility Molecule

42

Engaging Key Corporate Functions

Value Chain Stages Corporate Functions Corporate functions to involve or consult at each value chain stage Sustainability considerations Tools & Resources Corporate Functions Axis (each box represents a different corporate function that is critical to driving sustainability in the organization) Executive Management Financial Business Management R&D EHS Engineering Manufacturing / Operations Logistics / Supply Chain Sales Customer Technical Service/Support Marketing Communications Public Relations Human Resources Legal Information Technology & Management

Executive Management. Financial. Business Management. R&D. EHS. Engineering. Manufacturing / Operations. Logistics / Supply Chain. Sales. Customer Technical Service/Support. Marketing. Communications. Public Relations. Human Resources. Legal. Information Technology & Management.")

43

Sustainability Considerations

Checklist along the Value Chain Sustainability Considerations Value Chain Axis Sustainability Considerations Specific questions, applied and modified along the value chain whenever appropriate

44

Elements of the Roadmap

Value Chain Stages Corporate Functions Corporate functions to involve or consult at each value chain stage Sustainability considerations Tools & Resources Tools & Resources Publicly available & in-house tools to support sustainability considerations along value chain

45

Scoring Framework Idea Genera-tion Concept Scoping Defini-tion

Develop-ment Scale-Up Com-mercial-ization

46

Using the Roadmap Model developed by CSTP member companies & associated consultants Next step… validation of concept in use

47

Illustration of Roadmap

“Evaluation of Biofuels Processing Plant—Upstate New York”. Reuse of existing brownfields site Possible Feedstocks: Corn; Willow Stages of Roadmap to Illustrate: Upstream Input Stage (show examples) Commercialization Stage (in progress) Provide feedback on criteria, questions Partner with Lafayette College cross functional team

Commercialization Stage (in progress) Provide feedback on criteria, questions. Partner with Lafayette College cross functional team.")

48

Process of Evaluation Our Hypothetical Company

Information Located in upstate New York Purchases corn primarily from mid-western states Has onsite corn ethanol refinery Grows willow biomass onsite Has onsite willow ethanol refinery Focus of study: Not to consider the most sustainable industry possible Developing a plausible vantage point to make comparisons between corn and willow ethanol

49

Test Case: Biofuels Plant

Established process for biofuel from publicly available information Answered Roadmap questions based on internet sources & personal/professional opinion/insights Used publicly available information on willow and corn-derived feedstocks Focused on issues with sustainability and energy efficiency

50

Process of Evaluation Example Industries

Corn Ethanol Well developed industry Studies done by a variety of sources; data readily available Production plants already in operation across the US 2 processes: dry and wet milling

51

Process of Evaluation Corn Ethanol Process Flow Diagram

One of the biggest challenges in evaluating sustainability impact is to adequately consider the system boundaries. Too tight and you can miss a critical interaction. Too broad and you can do an adequate assessment of the problem.

52

Process of Evaluation Corn Ethanol Energy Balance

53

Process of Evaluation Corn Ethanol

Facts about corn ethanol Cost Corn $4.00 per bushel Corn ethanol $ $1.50 per gallon Production US production goals 15 billion gallons by 2017 Current production 4.8 billion gallons of ethanol in general Demand calculated to be 5.4 billion tons Estimated production capacity 6.183 billion gallons of ethanol in general from 113 refineries in 20 states

54

Process of Evaluation Corn Ethanol Production

Millions of gallons

55

Process of Evaluation Example Industries

Willow Ethanol In developmental stages Majority of studies done by SUNY ESF Only one plant in operation More energy/sf than corn

56

Process of Evaluation Willow Ethanol Process Flow Diagram

57

Process of Evaluation Willow Ethanol (Energy Balance)

")

58

Process of Evaluation Willow Ethanol

Facts about willow ethanol Costs Willow biomass $50 per dry ton cellulosic biomass Willow ethanol $ $2.25 per gallon Production US production goals 1 billion gallons per year by 2015 Current production 0.66 million gallons of cellulosic ethanol per year from Iogen in Canada

59

Upstream Input Questions

Can feedstock price, availability and access be maintained over the long-term? Would customer/stakeholder concerns affect the future use of the feedstock Are there current or expected future regulatory drivers that may affect steady supply of feedstock?

60

Long-term viability of corn feedstock not likely to be maintained.

Can feedstock price, availability and access be maintained over the long-term? Corn Feedstock expected to continue to see dramatic increase in demand resulting in increase in price. Increase demand for Corn Feedstock causing an increase in prices. Corn planted in 2007 saw a 113% increase over 2006 Corn is in high demand as a food product as well. used livestock feed various livestock corn syrup as the sweetener for most soft drinks. (Hargreaves, 2007) This competition will further limit access and raise prices. Corn feedstock price and availability can not be maintained if demand continues to increase. The limit for maximum corn production has nearly been reached New technology in feedstocks may cause drop in demand and price. Long-term viability of corn feedstock not likely to be maintained.

This competition will further limit access and raise prices. Corn feedstock price and availability can not be maintained if demand continues to increase. The limit for maximum corn production has nearly been reached. New technology in feedstocks may cause drop in demand and price. Long-term viability of corn feedstock not likely to be maintained.")

61

Can feedstock price, availability and access be maintained over the long-term?

Demand for low-value timber, willow, has dramatically decreased in New York state recently Current growth rate exceeds removal by 317%. (Bower, 2007) Production potential of 188 million dry tons of willow in NYS by 2008 Long term market should be stable (Bower, 2007) Willow feedstock shows very little fluctuation in price or availability.

Production potential of 188 million dry tons of willow in NYS by Long term market should be stable (Bower, 2007) Willow feedstock shows very little fluctuation in price or availability.")

62

How energy intensive is the feedstock

How energy intensive is the feedstock? Which feedstock materials is the most energy intensive and are there energy-efficient alternatives? Corn feedstock production is heavily reliant on fossil fuels for the production of pesticides and fertilizers, operation of the equipment, and transportation. Short Rotation Willow Coppice (SRWC), the hybrid of willow used as biomass for energy, is much less energy intensive than corn. This is because willow has far fewer inputs. Other alternatives for cellulosic ethanol feedstock such as sugar cane, switchgrass and miscanthus have the potential to be developed as very low input crops, if suitable for the region – lower Net Energy Balance. Willow is more energy efficient than corn, but not necessarily the most energy efficient.

, the hybrid of willow used as biomass for energy, is much less energy intensive than corn. This is because willow has far fewer inputs. Other alternatives for cellulosic ethanol feedstock such as sugar cane, switchgrass and miscanthus have the potential to be developed as very low input crops, if suitable for the region – lower Net Energy Balance. Willow is more energy efficient than corn, but not necessarily the most energy efficient.")

63

18. Would customer/stakeholder concerns affect the future use of the feedstock?

Corn feedstock is being impacted by the concerns of outside political/private stakeholders. President Bush - by the end of the decade America will meet 20% of oil needs with renewable sources Demand requires 35 billion gallons of fuel primarily from corn ethanol, already effecting the allocation of fields to corn and the price of dairy In % or 3.4 billion bushels of the corn crop is expected to be needed for ethanol, up 20% from 2006. With expected increase in demand, a shortage is expected in corn stockpiles going in to 2008, despite a billion bushel crop predicted for (Brahic, 2007) A recent surge in corn-based ethanol investment is encouraging growth. (Hasan, 2006) Interest and concern from political/private stakeholders will have a significant effect on how the corn crop is used in the future.

A recent surge in corn-based ethanol investment is encouraging growth. (Hasan, 2006) Interest and concern from political/private stakeholders will have a significant effect on how the corn crop is used in the future.")

64

18. Would customer/stakeholder concerns affect the future use of the feedstock?

Willow feedstock initially would be grown almost exclusively on land being leased to the producers via private land owners and farmers. (Pioneering Energy Crops..., 2000) Cooperation and the future of the feedstock are contingent on the confidence of landowners in the market for willow ethanol. Willow-based ethanol industrial scale is very dependent on interest from investors, customers and potential farmers

Cooperation and the future of the feedstock are contingent on the confidence of landowners in the market for willow ethanol. Willow-based ethanol industrial scale is very dependent on interest from investors, customers and potential farmers.")

65

Would the new product or process reduce GHG emissions over the entire lifecycle?

Plants sequester CO2 – Given the conditions of 0.25 tons ground C increase per hectare per year, “no net CO2” will be emitted Fewer N2O emissions will be released in willow farming than is released in corn farming because of the fewer amounts of fertilizers used Shipment by train and truck is needed and will require more energy usage than shipment by pipelines GHG emissions are increased because of long-distance shipment by diesel burning trucks While willow feedstock has less GHG emissions compared to corn, sequestration depends on farming conditions and GHG emissions in other life-cycle stages especially remain significant

66

Are there any demonstrated or anticipated changes to the marketplace or regulations that could affect environmental, societal or economic attractiveness? Increasing costs of fossil fuels and future regulatory and other constraints on GHG will make ethanol less expensive than gasoline Both cellulosic (willow) and corn ethanol are heavily tied to the government through subsidies If political opinion and support were to be turned away from ethanol, this fledgling industry would have major issues If the US government drops its tariffs against sugar cane import equaling $1.05 per gallon ethanol, it would make the marketplace more challenging Willow ethanol can be very attractive in the long term, however the industry can only develop with the continuation of political support and subsidies

and corn ethanol are heavily tied to the government through subsidies. If political opinion and support were to be turned away from ethanol, this fledgling industry would have major issues. If the US government drops its tariffs against sugar cane import equaling $1.05 per gallon ethanol, it would make the marketplace more challenging. Willow ethanol can be very attractive in the long term, however the industry can only develop with the continuation of political support and subsidies.")

67

23. Are there current or expected future regulatory drivers that may affect steady supply of feedstock? Willow plant feedstock Growth is currently exceeding the rate of harvest Little or no competition for the feedstock among other industries Great abundance near the plant site. (Bower, 2007) Corn feedstock production was the most subsidized crop in America with an allocated $37.5 billion dollars in subsidies between 1995 and 2003 (Bryce, 2005) Huge financial burden will not be sustainable as alternative feedstocks are developed limiting the competitiveness and scope of corn as a feedstock. (Keeney, 2006) Great demand has caused the corn price per bushel to rise over 50% in less than two years. (Hargreaves, 2007) Future supply of corn feedstock is very dependent on how much land can realistically be used to grow corn, what the corn is to be used for, and how long the subsidies last. Variation in Regulatory drivers (outside of subsidies; e.g. water run off, fertilizer use and misuse) must be more fully understood and discussed with policy makers. Impact may have significant impact on supply of corn feedstock.

Corn feedstock production was the most subsidized crop in America with an allocated $37.5 billion dollars in subsidies between 1995 and 2003 (Bryce, 2005) Huge financial burden will not be sustainable as alternative feedstocks are developed limiting the competitiveness and scope of corn as a feedstock. (Keeney, 2006) Great demand has caused the corn price per bushel to rise over 50% in less than two years. (Hargreaves, 2007) Future supply of corn feedstock is very dependent on how much land can realistically be used to grow corn, what the corn is to be used for, and how long the subsidies last. Variation in Regulatory drivers (outside of subsidies; e.g. water run off, fertilizer use and misuse) must be more fully understood and discussed with policy makers. Impact may have significant impact on supply of corn feedstock.")

68

Sources & Documentation

Using the Checklist Summary Table Question Summary of Findings Action Items Responsible Parties Priority/ Status Sources & Documentation … Completed Legend: High priority Medium priority Low priority

69

Scoring Framework Product & Process Development

70

What the Guide Does Provides list of considerations asked as questions by key decision makers at each stage Ability to score responses Track improvement to sustainability concepts through each stage Provides list of resources and tools

71

Summary Sustainability Roadmap identifies key sustainability questions and criteria in a gated process/product development scheme Use of Roadmap in biofuels case illustration appears to be increasing the level of discourse on sustainability issues in a short time period Roadmap offers a holistic framework for consideration of progress down the path towards sustainability Feedback is continually sought for improvement of the model

72

Sustainability: An emerging trend?

All the benefits & blessings flowing from the use of the earth were held to be the rightful heritage of all generations “…treat the earth as though we are tenants, rather than owners”….we must leave behind ‘enough and as good’ for others” The Old Testament- Genesis & Deuteronomy John Locke, Two Treatises of Government, 1689 “Then I say the earth belongs to each…generation during its course…no generation may contract debts greater than may be paid during the course of its own existence” Thomas Jefferson, 1789

73

2008 Projects (2009 continuation)

Sustainability Guide (English—20 min) CSTP SUSTAINABILTY GUIDE (Cytec lead) Release of Version 1 November 18, 2008 Version 2 Tools/scoring additions Raising Awareness (BASF lead) Internal—Newsletter review of 08 and 09 needs Select/approve Exchange topics for 09 3rd Party guidelines (FMC/Colgate/Packaging Institute) Survey plans Supply Chain Certification Issues Table Best Practices (Dow 2008, 2009?) Tools (Air Products) Publication of Tools to CSTP members Incorporation into Sustainability Guide Version 2

CSTP SUSTAINABILTY GUIDE (Cytec lead) Release of Version 1 November 18, Version 2 Tools/scoring additions Raising Awareness (BASF lead) Internal—Newsletter review of 08 and 09 needs. Select/approve Exchange topics for 09. 3rd Party guidelines (FMC/Colgate/Packaging Institute) Survey plans. Supply Chain Certification Issues Table. Best Practices (Dow 2008, 2009 ) Tools (Air Products) Publication of Tools to CSTP members. Incorporation into Sustainability Guide Version 2.")

74

2009 CSTP Proposed Projects

Sustainability Guide (English—20 min) Biofuels Metrics Roundtable (John Carberry, lead; Federal Request) Total Cost Assessment/Full Cost Accounting Users Group (Request by GE, Toyota, Formosa Water Resources Workshop (Request by ASME) Academic Sustainability Roundtable (Request by U Michigan) Certification of Technologies for Carbon Management (request Chevron) Certification of Water Footprinting (10 minutes, overview by xxxx) NIST Metrics Data Sourcing (Request by NIST) Sustainable Supply Chain Forum (Colgate-Palmolive, Packaging World) Interaction with ACC research activities (Honeywell) More??? Eastman????

Biofuels Metrics Roundtable (John Carberry, lead; Federal Request) Total Cost Assessment/Full Cost Accounting Users Group (Request by GE, Toyota, Formosa. Water Resources Workshop (Request by ASME) Academic Sustainability Roundtable (Request by U Michigan) Certification of Technologies for Carbon Management (request Chevron) Certification of Water Footprinting (10 minutes, overview by xxxx) NIST Metrics Data Sourcing (Request by NIST) Sustainable Supply Chain Forum (Colgate-Palmolive, Packaging World) Interaction with ACC research activities (Honeywell) More Eastman")

Similar presentations

>")

Recycling Committee Meeting March 18, 2010 Greenhouse Gas Protocol Product/Supply.>")