Download presentation

Presentation is loading. Please wait.

0

Scientific Research & Experimental Development Tax Credits

1

A – LEARNING OBJECTIVES

To provide an overview of the SR&ED program To provide an understanding of the key elements of the SR&ED program through the use of examples

2

A – SR&ED – A key part of Canada’s Economic Action Plan

Canada supports world class research and innovation to stimulate productivity, create jobs and grow the economy Business Expenditure on R&D (BERD) is a key measure of innovation Global competition for R&D investment is increasing The federal government invests over $7 billion per year in direct and indirect support for R&D

is a key measure of innovation. Global competition for R&D investment is increasing. The federal government invests over $7 billion per year in direct and indirect support for R&D.")

3

A – SR&ED Program The SR&ED program encourages Canadian businesses of all sizes, and in all sectors to conduct R&D in Canada by providing tax based incentives Canada’s SR&ED program is the largest federal program providing over $3.5 billion in tax assistance in 2010 to nearly 24,000 taxpayers Most provinces have complementary SR&ED tax credit incentives that provide further assistance. These programs generally follow the same guidelines as the federal program The SR&ED tax credit generates net positive economic benefits through spill-over effects

4

A – Benefits of Claiming SR&ED

Deductions for SR&ED expenditures Investment tax credits for qualified expenditures Refundable ITCs for Canadian-controlled private corporations with taxable income and taxable capital in Canada below annual limits

5

A – Who can claim? SR&ED benefits are available to taxpayers that:

Carry on business in Canada Perform eligible SR&ED in Canada that is related to that business Make qualifying SR&ED expenditures and File a claim on prescribed forms before the 18 month filing deadline SR&ED is defined for income tax purposes[1], as follows: “scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act 5

basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or. (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act. 5.")

6

A – Recent Trends in the Program

CRA is seeking improved compliance through increased reviews, stringent requirements for supporting evidence and penalties for non-compliant claimants and preparers CRA published policies have been revised Utilization of the SR&ED Program has increased dramatically 2012 budget introduced cut-backs through rate reductions and elimination of capital expenditures SR&ED is defined for income tax purposes[1], as follows: “scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act 6

basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or. (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act. 6.")

7

A – SR&ED Legislative Changes - 2012

Reduce the SR&ED investment tax credit rate from 20% to 15% for taxation years ending after 2013 No change to the enhanced 35% credit for eligible Canadian controlled private corporations Exclude capital expenditures from SR&ED deductions and investment tax credits for property acquired after 2013 Exclude lease payments incurred after 2013 Exclude shared-use equipment for capital expenditure incurred after 2013 Reduce the prescribed proxy amount from 65% to 60% for 2013 and 55% for years after 2013 Reduce contract expenditures and third party payments to 80% effective January 1, 2013 SR&ED is defined for income tax purposes[1], as follows: “scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act 7

basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or. (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act. 7.")

8

A – Exercise# 1 How does the SR&ED program increase Canadian competiveness on the world scale? Provides direct financial incentives to businesses that perform SR&ED Creates jobs and economic benefits for the country (spill-over effect) Business Expenditures on Research and Development (BERD) drives innovation which increases productivity which in turn increases GDP

Business Expenditures on Research and Development (BERD) drives innovation which increases productivity which in turn increases GDP.")

9

A – Exercise# 2 Who can claim SR&ED benefits?

Taxpayers that carry on business in Canada Corporation Individuals Trusts Partnerships (general partners only) Must file claims on prescribed forms within filing deadlines

Must file claims on prescribed forms within filing deadlines.")

10

A – Exercise# 3 Identify 2 major changes in the SR&ED program that come into effect in 2013 and 2014. Reduce the SR&ED investment tax credit rate from 20% to 15% for taxation years ending after 2013 No change to the enhanced 35% credit for eligible Canadian controlled private corporations Exclude capital expenditures from SR&ED deductions and investment tax credits for property acquired after 2013 - Exclude lease payments incurred after 2013 - Exclude shared-use equipment for capital expenditure incurred after 2013 Reduce the prescribed proxy amount from 65% to - 60% for 2013 and - 55% for years after 2013

11

B – LEARNING OBJECTIVES

How to identify eligible SR&ED To introduce the definition of SR&ED in the Income Tax Act (ITA) To consider the interpretation of SR&ED in CRA policies To apply these rules and guidance to the T661 Part 2 SR&ED is defined for income tax purposes[1], as follows: “scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act 1 11

To consider the interpretation of SR&ED in CRA policies. To apply these rules and guidance to the T661 Part 2. SR&ED is defined for income tax purposes[1], as follows: scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is. (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or. (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act")

12

International definition of an R&D project

“For a … project to be classified as R&D, its completion must be dependent on a scientific &/or technological advance, the aim of the project must be the systematic resolution of a scientific and/or technological uncertainty.” Source: Frascati Manual 2002, paragraph 135 Maximum Efficient Use of Knowledge Corporation © 2013

13

International Def’n of Qualified Projects (Scientific Method)

Phase 0: Eligible fields of S&T (OECD) Phase 1: Objectives > “Standard Practice” Phase 2: Variables of Technological Uncertainty Phase 3: “Systematic” Experimentation Putting it all together – the Project template 13

Phase 1: Objectives > Standard Practice Phase 2: Variables of Technological. Uncertainty. Phase 3: Systematic Experimentation. Putting it all together – the Project template. 13.")

14

B – Evaluating SR&ED Eligibility

The following questions can be used to help determine whether a project should be eligible SR&ED: 1. Has the main technological issue(s) for which a technological advancement is required been identified? 2. Is the work in a field of science or technology not excluded by the ITA 3. Has any potentially eligible work been carried out in the taxation year i.e. experimentation, analyses, trials? 4. In which category or categories would you consider the work to be attempting to achieve the advancement i.e. basic research, applied research, experimental development? 5. How is the work organized and tracked? How can it be claimed to satisfy the eligibility criteria and distinguish it as eligible under the ITA? SR&ED is defined for income tax purposes[1], as follows: “scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act 2 14

for which a technological advancement is required been identified 2. Is the work in a field of science or technology not excluded by the ITA. 3. Has any potentially eligible work been carried out in the taxation year i.e. experimentation, analyses, trials 4. In which category or categories would you consider the work to be attempting to achieve the advancement i.e. basic research, applied research, experimental development 5. How is the work organized and tracked How can it be claimed to satisfy the eligibility criteria and distinguish it as eligible under the ITA SR&ED is defined for income tax purposes[1], as follows: scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is. (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or. (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act")

15

B – SR&ED Legislation on Eligibility

The Income Tax Act defines SR&ED in subsection 248(1) as: “systematic investigation or search”, that is carried out in a field of science or technology, by means of experiment or analysis and that is: a) Basic Research, b) Applied Research, or c) Experimental Development*, and Includes d) support work *technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes SR&ED is defined for income tax purposes[1], as follows: “scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act 3 15

as: systematic investigation or search , that is. carried out in a field of science or technology, by means of experiment or analysis and that is: a) Basic Research, b) Applied Research, or. c) Experimental Development*, and. Includes d) support work. *technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes. SR&ED is defined for income tax purposes[1], as follows: scientific research and experimental development means systematic investigation or search that is carried out in a field of science or technology by means of experiment or analysis and that is. (a) basic research, namely, work undertaken for the advancement of scientific knowledge without a specific practical application in view, (b) applied research, namely, work undertaken for the advancement of scientific knowledge with a specific practical application in view, or. (c) experimental development, namely, work undertaken for the purpose of achieving technological advancement for the purpose of creating new, or improving existing, materials, devices, products or processes, including incremental improvements thereto, and, in applying this definition to a taxpayer, [1] in subsection 248(1) of the Act")

16

B – Supporting SR&ED Activities

Para 248(1)(d) support activities: Engineering Design Operations research Mathematical analysis Computer programming Data collection Testing and psychological research The support activities claimed must be commensurate with project needs to overcome obstacles and remove technological uncertainties Analysis of inclusions With respect to amounts included in ITA paragraph 248(1) definition of “SR&ED,” (a-d) Generally speaking, the legislation above provides that all work aimed at incremental technical improvements is eligible for credit to the extent that it was “commensurate with the needs” involved with the resolution of some predetermined technical uncertainty. 4 16

(d) support activities: Engineering. Design. Operations research. Mathematical analysis. Computer programming. Data collection. Testing and psychological research. The support activities claimed must be commensurate with project needs to overcome obstacles and remove technological uncertainties. Analysis of inclusions. With respect to amounts included in ITA paragraph 248(1) definition of SR&ED, (a-d) Generally speaking, the legislation above provides that all work aimed at incremental technical improvements is eligible for credit to the extent that it was commensurate with the needs involved with the resolution of some predetermined technical uncertainty")

17

B – Linked Activities Support activities described in paragraph (d) that are linked to an eligible project can be claimed by: The taxpayer or A related party provided that the work would have been eligible to the taxpayer, had they undertaken the work Use the same project description for support work undertaken by the non-arm’s length company and tick the box for joint R&D – T661 Part 2 Other support activities not described in paragraph (d) can only be claimed by the taxpayer and only if the traditional method is elected 5

can only be claimed by the taxpayer and only if the traditional method is elected. 5.")

18

B – Excluded Work There are certain activities that do not qualify as SR&ED. As set out in subparagraph 248(1), SR&ED does not include work with respect to: Market research or sales promotion Quality control or routine testing of materials, devices, products or processes Research in the social sciences or the humanities Prospecting, exploring or drilling for, or producing, minerals, petroleum or natural gas The commercial production of a new or improved material, device or product or the commercial use of a new or improved process Style changes or Routine data collection Exclusions: (e, h & i) market research, sales promotion and the commercial production are excluded activities to the extent that they extend beyond the resolution of the significant technical uncertainties. Where work which may normally be considered market research involves issues such as the quantification of future project objectives, this work may be eligible SR&ED. (f & k) quality control, routine testing and routine data collection - generally speaking, routine activities are those which can not be considered, “commensurate with the needs, and directly in support of,” the resolution of one or more technical uncertainties. (g) research in the social sciences or the humanities, includes work in any non technical field such as accounting, finance, business studies, economics and psychology to name a few. Some may note that psychological research is mentioned as a potentially supporting activity in paragraph (d) of the legislation. The CRA’s formal position is that this research will be limited to pharmaceutical medical industries where it is tied to other technical or scientific drug studies. (j) style changes include any work aimed at aesthetic improvements rather than objective and verifiable advancements of technical knowledge. 6 18

, SR&ED does not include work with respect to: Market research or sales promotion. Quality control or routine testing of materials, devices, products or processes. Research in the social sciences or the humanities. Prospecting, exploring or drilling for, or producing, minerals, petroleum or natural gas. The commercial production of a new or improved material, device or product or the commercial use of a new or improved process. Style changes or. Routine data collection. Exclusions: (e, h & i) market research, sales promotion and the commercial production are excluded activities to the extent that they extend beyond the resolution of the significant technical uncertainties. Where work which may normally be considered market research involves issues such as the quantification of future project objectives, this work may be eligible SR&ED. (f & k) quality control, routine testing and routine data collection - generally speaking, routine activities are those which can not be considered, commensurate with the needs, and directly in support of, the resolution of one or more technical uncertainties. (g) research in the social sciences or the humanities, includes work in any non technical field such as accounting, finance, business studies, economics and psychology to name a few. Some may note that psychological research is mentioned as a potentially supporting activity in paragraph (d) of the legislation. The CRA’s formal position is that this research will be limited to pharmaceutical medical industries where it is tied to other technical or scientific drug studies. (j) style changes include any work aimed at aesthetic improvements rather than objective and verifiable advancements of technical knowledge")

19

“Defining the SR&ED project” Tax Court vs. CRA Guidance

CRA SR&ED Guidance – the consolidated document Role of the TCC vs. expert witness Tax Court outlines the SR&ED process Defining the “Scientific method” SR&ED project eligibility – TCC vs. CRA requirements Project template (simple view) Step 1a): Ensure proper definition of existing knowledge at the outset Step 1 b): Quantification of objectives vs. standard practice Step 2: Correlate experiments to hypotheses Step 3a): Ensuring work was done “systematically” Step 3b): Clarifying the “technological conclusions / advancements” The CRA recently consolidated its SR&ED rules and procedures into s single document This included a comparison of the - CRA’s 3 eligibility criteria to - The Tax court of Canada’s 5 eligibility questions & - Its recommendations on the “steps required” in the process of recording projects We then examine these directives in the form of a “project documentation template” and examine specific pronouncements by the tax court as to relevant documentation for each of these steps Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge

Step 1a): Ensure proper definition of existing knowledge at the outset. Step 1 b): Quantification of objectives vs. standard practice. Step 2: Correlate experiments to hypotheses. Step 3a): Ensuring work was done systematically Step 3b): Clarifying the technological conclusions / advancements The CRA recently consolidated its SR&ED rules and procedures into s single document. This included a comparison of the. - CRA’s 3 eligibility criteria to. - The Tax court of Canada’s 5 eligibility questions & - Its recommendations on the steps required in the process of recording projects. We then examine these directives in the form of a project documentation template and examine specific pronouncements by the tax court as to relevant documentation for each of these steps. Maximum Efficient Use of Knowledge Corporation © 2013 ME + U = Knowledge.")

20

CRA SR&ED Guidance – the consolidated document

December 19, 2012 the CRA released a consolidated document to replace all prior Interpretation Bulletins (IT’s) Information Circulars (IC’s) & Application Policy Papers (APP’s) related to SR&ED credits. While the CRA claims that it does not represent any new policies they do provide clarification on certain issues & remove ambiguities among former documents. Perhaps the most significant “new” analysis is an attempt to correlate; The CRA’s 3 component eligibility criteria to The 5 criteria used by the Tax Court of Canada / Scientific Method On Dec 19, 2012 the CRA consolidated its SR&ED directives into a single document. The CRA claims it does not represent any new policy but does remove ambiguities and provide additional clarification in certain areas. One of the notable clarifications is the comparison of the CRA’s 3 step eligibility criteria to the 5 steps used by the Tax court of Canada. Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge

Information Circulars (IC’s) & Application Policy Papers (APP’s) related to SR&ED credits. While the CRA claims that it. does not represent any new policies. they do provide clarification on certain issues & remove ambiguities among former documents. Perhaps the most significant new analysis is an attempt to correlate; The CRA’s 3 component eligibility criteria to. The 5 criteria used by the Tax Court of Canada / Scientific Method. On Dec 19, 2012 the CRA consolidated its SR&ED directives into a single document. The CRA claims it does not represent any new policy but does remove ambiguities and provide additional clarification in certain areas. One of the notable clarifications is the comparison of the CRA’s 3 step eligibility criteria to the 5 steps used by the Tax court of Canada. Maximum Efficient Use of Knowledge Corporation © 2013 ME + U = Knowledge.")

21

Notable quote “There is nothing wrong with change, if it is in the right direction” - Sir Winston Churchill Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge

22

B – Five Questions for SR&ED Projects

Was there a scientific or a technological uncertainty—an uncertainty that could not be removed by standard practice? Did the effort involve formulating hypotheses specifically aimed at reducing or eliminating that uncertainty? Was the adopted procedure consistent with the total discipline of the scientific method, including formulating, testing, and modifying the hypotheses? Did the process result in a scientific or a technological advancement? Was a record of the hypotheses tested and the results kept as the work progressed? The answer to all five questions must be yes 7

23

Maximum Efficient Use of Knowledge Corporation © 2013

Finally we provide a detailed comparison of The Tax Courts 5 “main questions” to The CRA’s 3 eligibility criteria And illustrate how each of these requirements is addressed and documented in the proposed RDBASE project template. Some of the major additions we feel could be relevant include: A further focus on defining A) The state of standard practice at the outset of the work B) the variables of experimentation & C) The use of the Scientific method We will illustrate that the courts have addressed each of these issues within their pronouncements but on many of these issues the CRA is still silent. Maximum Efficient Use of Knowledge Corporation © 2013

The state of standard practice at the outset of the work. B) the variables of experimentation & C) The use of the Scientific method. We will illustrate that the courts have addressed each of these issues within their pronouncements but on many of these issues the CRA is still silent. Maximum Efficient Use of Knowledge Corporation ©")

24

B – 1. Was there a scientific or a technological uncertainty—an uncertainty that could not be removed by standard practice? Identify specific technical obstacles encountered in a project to achieve an advance in a product, process or material Identify limitations and constraints of current technology (standard practice) The attempts to overcome these uncertainties should lead to an advance in knowledge. (whether successful or not) 8

The attempts to overcome these uncertainties should lead to an advance in knowledge. (whether successful or not) 8.")

25

Step 1a): Definition of existing knowledge at the outset

Northwest Hydraulics CRA position (all work SP) “work described … refers to standard devices and processes, which are routinely used in similar design situations all over the world.” Tax Court Position “It was the innovative combination and alignment of [these] factors that makes this project unique.” We will now examine specific pronouncements by the tax court judges with respect to each of these 5 steps: In the case of NW Hydraulics the CRA argued the work was routine engineering since the claimant had used all of the devices before. The judge disagreed with the CRA position since the claimant proved that the innovative combination and alignment of these devices carried elements of technology uncertainty which went beyond “standard practice” usage . Maximum Efficient Use of Knowledge Corporation © 2013

work described … refers to standard devices and processes, which are routinely used in similar design situations all over the world. Tax Court Position. It was the innovative combination and alignment of [these] factors that makes this project unique. We will now examine specific pronouncements by the tax court judges with respect to each of these 5 steps: In the case of NW Hydraulics the CRA argued the work was routine engineering since the claimant had used all of the devices before. The judge disagreed with the CRA position since the claimant proved that the innovative combination and alignment of these devices carried elements of technology uncertainty which went beyond standard practice usage . Maximum Efficient Use of Knowledge Corporation ©")

26

Author’s commentary: The Northwest Case illustrates how CRA officials may deny claims on the basis the project appears to be “routine engineering” without providing support for their position but identification of “variables” for experimentation provide adequate evidence for the TCC US / IRS directives – perhaps CRA can adopt? Patent safe harbour Rebuttal presumption IRS must demonstrate within common knowledge if denied This case outlines the importance of benchmarking the steps taken to review the existing (or standard practice) methods which would be typical for such a project and clarify why they are not applicable to the current environment. Once this step is performed, identifying the variables of uncertainty would provide evidence that that the hypotheses go beyond these standard practice models. Notably in the US SR&ED tax credit system IRS auditors are required to provide evidence of such methods if they intend to deny claims on the basis of standard practice. In the author’s opinion this level of accountability would be a excellent measure for the CRA to adopt as well. Maximum Efficient Use of Knowledge Corporation © 2013

methods which would be typical for such a project and clarify why they are not applicable to the current environment. Once this step is performed, identifying the variables of uncertainty would provide evidence that that the hypotheses go beyond these standard practice models. Notably in the US SR&ED tax credit system IRS auditors are required to provide evidence of such methods if they intend to deny claims on the basis of standard practice. In the author’s opinion this level of accountability would be a excellent measure for the CRA to adopt as well. Maximum Efficient Use of Knowledge Corporation ©")

27

Step 1 b): Quantification of objectives vs. standard practice

Sass Manufacturing “Systematic investigation connotes the existence of controlled experiments and of highly accurate measurements and involves the testing of one's theories against empirical evidence. Northwest Hydraulics "Most scientific research involves gradual, indeed infinitesimal, progress.” The cases of Sass Manufacturing and Northwest Hydraulics stress the importance of “extremely accurate measurements” & the expectation of infinitesimally gradual results As such the quantification of objectives becomes the starting point for such work. Maximum Efficient Use of Knowledge Corporation © 2013

28

Initial hypothesis formulation that may provide a solution to problem

B – 2. Did the effort involve formulating hypotheses specifically aimed at reducing or eliminating that uncertainty? Initial hypothesis formulation that may provide a solution to problem Modification of hypotheses through testing and interpretation of results 9

29

Step 2: Correlate experiments to technological uncertainties (hypotheses)

CW Agencies “The word hypothesis in this context is normally considered to mean a provisional concept which is not inconsistent with known facts and serves as a starting point for further investigation by which it may be proved or disproved objectively.” Maritime Ontario Freight Lines “A hypothesis is a tentative assumption or explanation to an unknown problem and, as a rule, this requirement is met by the existence of a logical plan devised to observe and resolve the hypothetical problem.” The pivotal point of the project eligibility concerns the existing of technological uncertainties and related hypotheses to resolve them. The tax courts define “hypotheses” in several tax cases including CW Agencies & Maritime Ontario Freight Lines. These definitions clarify that hypotheses are: Tentative assumptions Based on existing facts For further investigation Maximum Efficient Use of Knowledge Corporation © 2013

30

Identifying “key variables” within “hypotheses”

Northwest Hydraulics “I do not think that conventional engineering would be adequate to deal with the variables and the uncertainties that were inherent in the major disruption and diversion of the flow of the river resulting from the construction” Technological uncertainty is something that exists in the mind of the specialist such as the appellant, who identifies and articulates it and applies its methods to remove that uncertainty.” As illustrated in the case of NW Hydraulics the judge will ultimately examine whether the “variables under experimentation” could have been resolved using the “standard practice’ methodologies. Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge

31

Additional definitions of “scientific hypotheses”

From Wikipedia, the free encyclopedia For a hypothesis to be a scientific hypothesis, the scientific method requires that one can test it. Scientists generally base scientific hypotheses on previous observations that cannot satisfactorily be explained with the available scientific theories. Normally hypotheses have the form of a mathematical model. A working hypothesis is a provisionally accepted hypothesis proposed for further research. Since the tax courts generally look to “generally accepted definitions” to interpret the meaning of words within the legislation we believe the following definitions are relevant to the definition of a “scientific hypothesis.” That “scientific hypotheses” require that one can test them They are based on observations which cannot be explained with existing theories They normally follow mathematical models & Represent a proposed basis for further testing Maximum Efficient Use of Knowledge Corporation © 2013

32

Author’s commentary: Evidence hypotheses via “test matrix.”

This would require the researcher to: Identify the key variables which he/she believes explain the performance Benchmark variables vs. existing models to predict their interaction Rank the variables in order of significance Test the variables to further understand shortfall of the existing models One of the earliest publications on the “science of design” was “Design of Experiments” first published by Sir R.A Fisher in 1935. This books provides guidance on the use of matrices to test the “variables” within theories in what is referred to as DOE model. We have found that strong SR&ED projects are those that can - Identify & rank the variables of uncertainty. Conversely where the research team is unable to identify the “variables” of experimentation it becomes more difficult to prove: The work was done systematically (via controlled experiments) & That it went beyond existing standard practice models. Maximum Efficient Use of Knowledge Corporation © 2013

& That it went beyond existing standard practice models. Maximum Efficient Use of Knowledge Corporation ©")

33

Method of experimentation clearly set out at the onset of the project

B – 3. Was the adopted procedure consistent with the total discipline of the scientific method, including formulating, testing, and modifying the hypotheses? Method of experimentation clearly set out at the onset of the project Demonstrate systematic investigation Work performed by qualified personnel 10

34

Advances understanding of scientific relations or technologies

B – 4. Did the process result in a scientific or a technological advancement? Advances understanding of scientific relations or technologies Search for new knowledge or technical capability Departure from standard practice Resolution of a technical or scientific obstacle 11

35

Step 3b): Clarifying “technological conclusions / advancements”

Rainbow Pipeline “The rejection after testing of an hypothesis is nonetheless an advance in that it eliminates one hitherto untested hypothesis. Much scientific research involves doing just that. The fact that the initial objective is not achieved invalidates neither the hypothesis formed nor the methods used. On the contrary it is possible that the very failure reinforces the measure of the technological uncertainty.” The judge in the Rainbow Pipeline case also commented on evidence of “technological advancement” as required by the income Tax Act. The RDBASE SR&ED Consortium© 2013

36

Documented testing through experimentation or analysis

B – 5. Was a record of the hypotheses tested and the results kept as the work progressed? Documented testing through experimentation or analysis Evidence of results and conclusions 12

37

Step 3a): Ensuring work was done “systematically”

Sass Manufacturing Scientific research must mean the enterprise of explaining and predicting and the gaining knowledge of whatever the subject matter of the hypothesis is. This surely would include repeatable experiments in which the steps, the various changes made and the results are carefully noted.” Step 3 a) To ensure the work was done systematically the judge in Sass manufacturing indicated that the claimant needs to both; Correlate the research to the stated hypotheses & To Keep adequate records of this work. The RDBASE SR&ED Consortium © 2013

To ensure the work was done systematically the judge in Sass manufacturing indicated that the claimant needs to both; Correlate the research to the stated hypotheses & To Keep adequate records of this work. The RDBASE SR&ED Consortium ©")

38

Step 3a): Ensuring work was done “systematically”

Rainbow Pipeline “What may appear routine and obvious after the event may not have been before the work was undertaken. What distinguishes routine activity from the methods required by the definition of SR&ED …. is not solely the adherence to systematic routines, but the adoption of the entire scientific method, with a view to removing a technological uncertainty through the formulation and testing of innovative and untested hypotheses.” In Rainbow Pipeline the judge also clarified that being “methodical or systematic” was a requirement but not in itself proof of SR&ED . To be systematic investigation as contemplated under the Income Tax Act the judge noted that it must also “follow the entire scientific methods including formulation & testing of untested hypotheses. The RDBASE SR&ED Consortium© 2013

39

B – Defining an SR&ED Project

An SR&ED project comprises a set of interrelated activities that collectively are necessary in attempting to achieve the specific scientific or technological advancement defined for the project by overcoming scientific or technological uncertainty The activities are pursued through a systematic investigation or search in a field of science or technology by means of experiment or analysis performed by qualified individuals 13

40

B – Form T661 Part 2 Prescribed form includes description of each eligible project: Structured format with word limits Preparer / employee information for each project No attachments – all information is contained in RSI bar codes Current version of T661 must be used 14

41

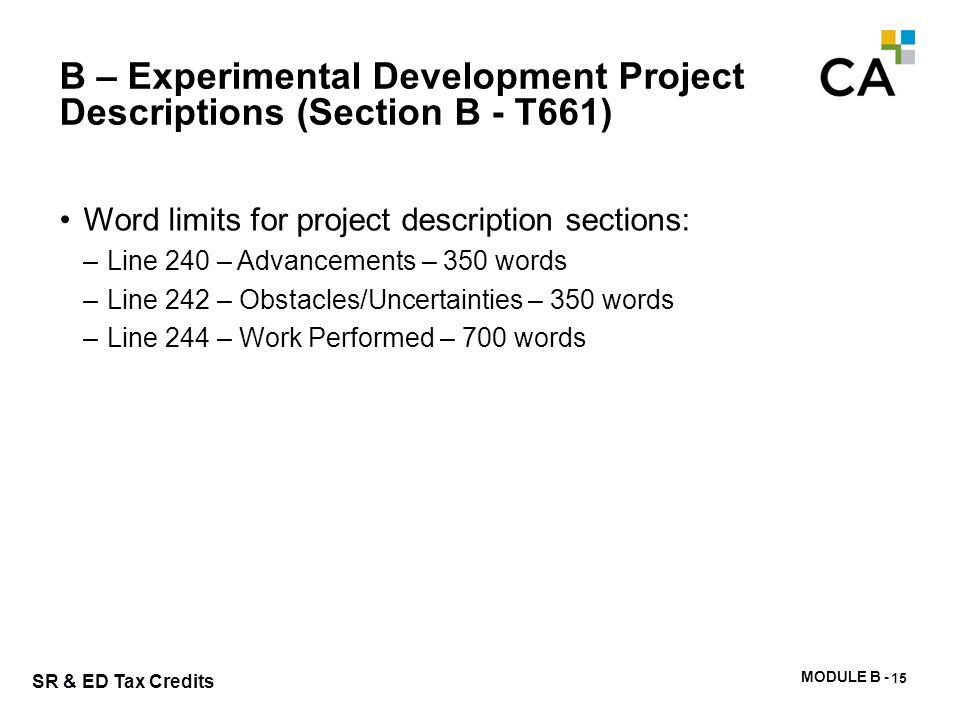

B – Experimental Development Project Descriptions (Section B - T661)

Word limits for project description sections: Line 240 – Advancements – 350 words Line 242 – Obstacles/Uncertainties – 350 words Line 244 – Work Performed – 700 words 15

43

Indicate the technological objective

B – Line 240 – What technological advancement(s) were you trying to achieve? Key content: Indicate the technological objective Describe the existing state of knowledge in the applicable field of technology Describe the new or improved capability Indicate how this new or improved capability advanced the existing state of knowledge in the applicable field of technology Explain what knowledge you gained as a result of the work you did, regardless of success or failure 16 43

were you trying to achieve Key content: Indicate the technological objective. Describe the existing state of knowledge in the applicable field of technology. Describe the new or improved capability. Indicate how this new or improved capability advanced the existing state of knowledge in the applicable field of technology. Explain what knowledge you gained as a result of the work you did, regardless of success or failure")

44

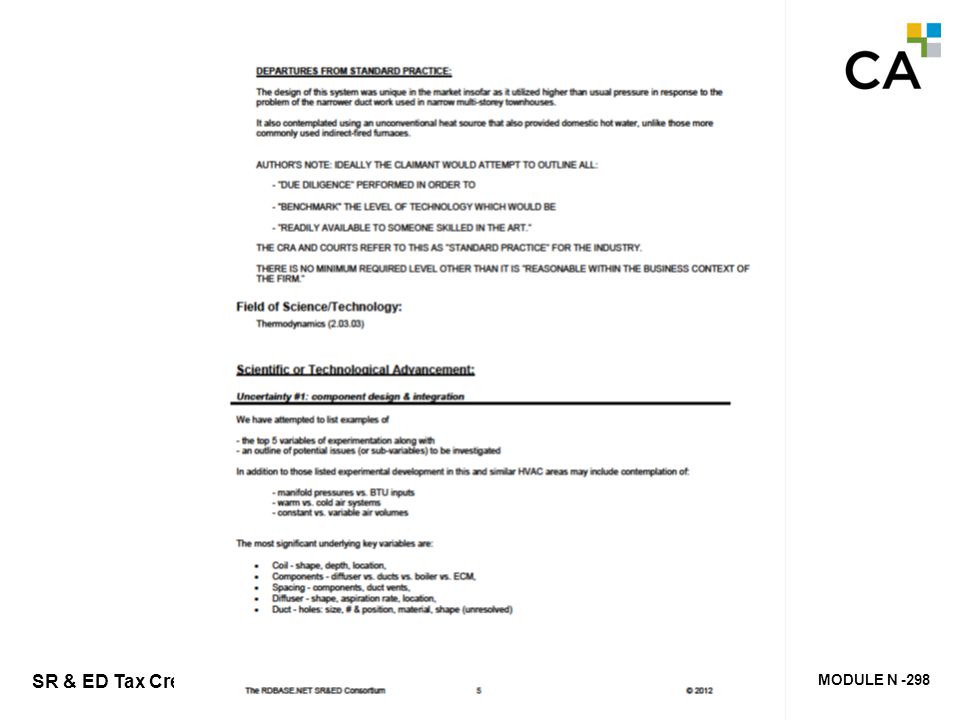

Phase 1: Define “Standard Practice” (The Square )

B Phase 1: Define “Standard Practice” (The Square ) What is known? “Commonly available sources of knowledge or experience are those that can reasonably be assumed to be readily available to those with basic training or experience in the field of concern. These resources enable them to be sufficiently qualified to participate in SR&ED. They also include knowledge that is available in the business context of the firm….An enterprise may not have practical access to information proprietary to a competitor, or known in specialist or academic circles.” [1] “Essentially, the presence of a technological uncertainty puts the project into the realm of experimental development when solutions cannot be based on standard practice alone. A claim for qualifying expenditures should clearly explain all departures from standard practice in the experimental development activity.”[2] “The search for a meaningful advance in the body of scientific or technological knowledge should be present as a guiding element in every eligible project. This requirement is satisfied whether or not the activity is successful. In other words, determining that a hypothesis is incorrect also represents a scientific or technological advance.”[3] [1] CRA IC 86-4R3 – glossary [2] CRA IC 86-4R3 paragraphs 4.3 & 4.4 CRA Guidelines[3] Excerpt from IC 86-4R3 paragraph 2.12 Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge Maximum Efficent Use of Knowledge Corporation ME + U = Knowledge 44

What is known Commonly available sources of knowledge or experience are those that can reasonably be assumed to be readily available to those with basic training or experience in the field of concern. These resources enable them to be sufficiently qualified to participate in SR&ED. They also include knowledge that is available in the business context of the firm….An enterprise may not have practical access to information proprietary to a competitor, or known in specialist or academic circles. [1] Essentially, the presence of a technological uncertainty puts the project into the realm of experimental development when solutions cannot be based on standard practice alone. A claim for qualifying expenditures should clearly explain all departures from standard practice in the experimental development activity. [2] The search for a meaningful advance in the body of scientific or technological knowledge should be present as a guiding element in every eligible project. This requirement is satisfied whether or not the activity is successful. In other words, determining that a hypothesis is incorrect also represents a scientific or technological advance. [3] [1] CRA IC 86-4R3 – glossary. [2] CRA IC 86-4R3 paragraphs 4.3 & 4.4. CRA Guidelines[3] Excerpt from IC 86-4R3 paragraph Maximum Efficient Use of Knowledge Corporation © 2013 ME + U = Knowledge. Maximum Efficent Use of Knowledge Corporation ME + U = Knowledge. 44.")

45

TEMPLATE - THREE COMPONENTS OF AN SR&ED PROJECT – STEP 1:

Maximum Efficient Use of Knowledge Corporation © 2013

46

Maximum Efficient Use of Knowledge Corporation © 2013

Notable quote “He who asks a question is a fool for 5 minutes. He who does not ask a question remains a fool forever.” - Chinese proverb Maximum Efficient Use of Knowledge Corporation © 2013

47

B – Line 242 – What technological obstacles/uncertainties did you have to overcome to achieve those advancements? Describe the shortcomings and/or limitations of the current state of technology that prevented you from developing the new or improved capability Describe the technological problems and unknown elements that had to be removed while you attempted to achieve the technological advancement(s) identified in line 240 17 47

identified in line")

48

Phase 2: Technical Uncertainty (Triangle)

B Phase 2: Technical Uncertainty (Triangle) What is unknown? “Specifically, scientific or technological uncertainty may occur in either of two ways: [scientific uncertainty] it may be uncertain whether the goals can be achieved at all ; or [system uncertainty] the taxpayer may be fairly confident that the goals can be achieved, but may be uncertain which of several alternatives (i.e. paths, routes, approaches, equipment configurations, system architectures, circuit techniques, etc.) will either work at all, or be feasible to meet the desired specifications or cost targets, or both of these…Work on combining standard technologies, devices, and/or processes is eligible if non-trivial combinations of established (well-known) technologies and principles for their integration carry a major element of technological uncertainty; this may be called a "system uncertainty.”[1] “If the technological specifications or objectives to resolve the "system uncertainty" are such that the basic design of the underlying technologies must be changed to achieve the integration, the current costs of the overall project may qualify.”[3] [1] CRA IC 86-4R3 paragraph [2] CRA IC 94-2 – SR&ED Machinery & equipment industry application paper [3] Excerpts from CRA IC 86-4R3 paragraph 4.8 – characteristics of SR&ED Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge Maximum Efficent Use of Knowledge Corporation ME + U = Knowledge 48

What is unknown Specifically, scientific or technological uncertainty may occur in either of two ways: [scientific uncertainty] it may be uncertain whether the goals can be achieved at all ; or. [system uncertainty] the taxpayer may be fairly confident that the goals can be achieved, but may be uncertain which of several alternatives (i.e. paths, routes, approaches, equipment configurations, system architectures, circuit techniques, etc.) will either work at all, or be feasible to meet the desired specifications or cost targets, or both of these…Work on combining standard technologies, devices, and/or processes is eligible if non-trivial combinations of established (well-known) technologies and principles for their integration carry a major element of technological uncertainty; this may be called a system uncertainty. [1] If the technological specifications or objectives to resolve the system uncertainty are such that the basic design of the underlying technologies must be changed to achieve the integration, the current costs of the overall project may qualify. [3] [1] CRA IC 86-4R3 paragraph [2] CRA IC 94-2 – SR&ED Machinery & equipment industry application paper. [3] Excerpts from CRA IC 86-4R3 paragraph 4.8 – characteristics of SR&ED. Maximum Efficient Use of Knowledge Corporation © 2013 ME + U = Knowledge. Maximum Efficent Use of Knowledge Corporation ME + U = Knowledge. 48.")

49

TEMPLATE - THREE COMPONENTS OF AN SR&ED PROJECT – STEP 2:

Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge

50

Maximum Efficient Use of Knowledge Corporation © 2013

Notable quote “They always say time changes things, but you actually have to change them yourself.” - Andy Warhol Maximum Efficient Use of Knowledge Corporation © 2013

51

B – Line 244: What work did you perform in the tax year to overcome the technological obstacles/uncertainties? (Summarize the systematic investigation) Describe only the work that was actually carried out during the tax year and for which you are claiming expenditures in the tax year Describe, in a clear and concise manner, how you attempted to overcome the technological obstacles/ uncertainties that you identified in line 242 Describe, in chronological order, the work done to overcome shortcomings in the underlying technology Clearly demonstrate the systematic nature of the investigation or search and describe the experiments and/or analyses conducted to overcome the obstacles, including the results obtained, their interpretation, and the conclusions made 18 51

52

Phase 3: Systematic Investigation (Circles)

B Phase 3: Systematic Investigation (Circles) What was done? The CRA requires work to be supervised by personnel with appropriate technical backgrounds and clarifies that in describing activities performed. “It must demonstrate the presence of analysis or experiment in the methodology you used to carry out the work. It must also include the results you obtained and the conclusions you made. For example, the types of technical records that are appropriate to support your claim are: · an analysis of the problem, · internal design documents and drawings, · test data and results, & · progress reports.”[1] “The improvement of existing technologies or methodologies using well-established "routine engineering or routine development" would be ineligible if the outcome is predictable. However,…if the .. activity is carried out in support of an eligible experimental development project, then the activity is eligible.”[2] Form T4088 – Guide to form T661 [2] Excerpt from IC 86-4R3 paragraph 2.13 Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge 52

What was done The CRA requires work to be supervised by personnel with appropriate technical backgrounds and clarifies that in describing activities performed. It must demonstrate the presence of analysis or experiment in the methodology you used to carry out the work. It must also include the results you obtained and the conclusions you made. For example, the types of technical records that are appropriate to support your claim are: · an analysis of the problem, · internal design documents and drawings, · test data and results, & · progress reports. [1] The improvement of existing technologies or methodologies using well-established routine engineering or routine development would be ineligible if the outcome is predictable. However,…if the .. activity is carried out in support of an eligible experimental development project, then the activity is eligible. [2] Form T4088 – Guide to form T661. [2] Excerpt from IC 86-4R3 paragraph Maximum Efficient Use of Knowledge Corporation © 2013 ME + U = Knowledge. 52.")

53

TEMPLATE - THREE COMPONENTS OF AN SR&ED PROJECT – STEP 3:

Maximum Efficient Use of Knowledge Corporation © 2013

54

Maximum Efficient Use of Knowledge Corporation © 2013

Notable quote “The more original a discovery, the more obvious it seems afterwards.” - Arthur Koestler Maximum Efficient Use of Knowledge Corporation © 2013

55

Realm of Experimental Development

B Realm of Experimental Development The complete picture “An SR&ED project consists of a set of interrelated activities that meet the three criteria of SR&ED defined in the current version of Information Circular 86‑4, Scientific Research and Experimental Development. This means that the set of activities must be necessary for: 1) the attempt to achieve specific scientific or technological advancement and 2) overcome scientific or technological uncertainty, and 3) must be pursued through a systematic investigation by means of experiment or analysis performed by qualified individuals.” The model above represents the three components of an eligible SR&ED project. “Essentially, the presence of a technological uncertainty puts the project into the realm of experimental development when solutions cannot be based on standard practice alone.” Excerpt from IC 86-4R3 paragraph 4.3 “Achieving a technological advance would require removing the element of technological uncertainty through a process of systematic investigation… For an experimental development activity to be eligible the technological advance achieved has only to be slight.” Excerpt from CRA, IC 86-4R3 paragraph 2.13 “In the context of experimental development, scientific or technological advancement is the knowledge acquired in carrying out the SR&ED project, which advances the understanding of the underlying scientific relations or technology. ..For an experimental development activity to be eligible … it must seek to advance the taxpayer's technological knowledge base. The technological advance achieved has only to be slight.” Excerpt from IC 86-4R3 paragraph 2.13 Maximum Efficient Use of Knowledge Corporation © ME + U = Knowledge Maximum Efficent Use of Knowledge Corporation ME + U = Knowledge 55

the attempt to achieve specific scientific or technological advancement and. 2) overcome scientific or technological uncertainty, and. 3) must be pursued through a systematic investigation by means of experiment or analysis performed by qualified individuals. The model above represents the three components of an eligible SR&ED project. Essentially, the presence of a technological uncertainty puts the project into the realm of experimental development when solutions cannot be based on standard practice alone. Excerpt from IC 86-4R3 paragraph 4.3. Achieving a technological advance would require removing the element of technological uncertainty through a process of systematic investigation… For an experimental development activity to be eligible the technological advance achieved has only to be slight. Excerpt from CRA, IC 86-4R3 paragraph In the context of experimental development, scientific or technological advancement is the knowledge acquired in carrying out the SR&ED project, which advances the understanding of the underlying scientific relations or technology. ..For an experimental development activity to be eligible … it must seek to advance the taxpayer s technological knowledge base. The technological advance achieved has only to be slight. Excerpt from IC 86-4R3 paragraph Maximum Efficient Use of Knowledge Corporation © 2013 ME + U = Knowledge. Maximum Efficent Use of Knowledge Corporation ME + U = Knowledge. 55.")

56

Maximum Efficient Use of Knowledge Corporation © 2013 ME + U = Knowledge

57

B – Basic or Applied Research Project Descriptions (Section C – T661)

Word limits for project description sections: Line 250 – Advancement in scientific knowledge – 350 words Line 252 – Work Performed – 700 words 19 57

58

TCC - Role of the “expert witness”

RIS Christie : role of the scientists in determining SR&ED eligibility “What constitutes scientific research for the purposes of the Act is either a question of law or a question of mixed law and fact to be determined by the Tax Court of Canada, not expert witnesses, as is too frequently assumed by counsel for both taxpayers and the Minister. An expert may assist the court in evaluating technical evidence and seek to persuade it that the research objective did or could not lead to a technological advancement. But, at the end of the day, the expert’s role is limited to providing the court with a set of prescription glasses through which technical information can be viewed before being analyzed and weighed by the trial judge.” Before we look at the specific components of an SR&ED project let’s examine the role the TCC in determining SR&ED eligibility: In the case of RIS Christie the judge stated : “What constitutes scientific research for the purposes of the Act is a question of law to be determined by the Tax Court of Canada, not expert witnesses. the expert’s role is limited to providing the court with a set of prescription glasses through which technical information can be viewed before being analyzed and weighed by the trial judge.” Maximum Efficient Use of Knowledge Corporation © 2013

59

B – Line 250 – What advancements in scientific knowledge were you trying to achieve?

Indicate the objective of the project and describe the scientific knowledge that you gained or were attempting to gain with the work you did Explain why the new knowledge gained as a result of your work is an advance relative to the scientific knowledge that was available at the onset of the project, regardless of success or failure Describe how the results of your experiments and / or analyses advanced the understanding of scientific principles, methodologies, or relations 20 59

60

B – Line 252 – What work did you perform in the tax year and how did that work contribute to the advancements described in line 250? (Summarize the systematic investigation) Describe only the work that was actually carried out during the tax year and for which you are claiming expenditures in the tax year Indicate the knowledge gap that existed at the onset of the project that prevented you from achieving your scientific goals Describe the principles underlying the new concepts that will address the inadequacies of the scientific knowledge that existed at the onset of the project Summarize the experiments and/or analyses conducted, including the results obtained, their interpretation, and the conclusions made 21 60

61

B – Evidence to Support the Claim

22 61

62

B – CRA Publications T4088 – Guide to Form T661

Technical eligibility – Eligibility of Work for SR&ED Investment Tax Credits Policy New guidance documents and policies were released on December 19, 2012 23 62

63

B - Exercise #1 What distinguishes “SR&ED” from “research and development”? R&D is a broad category of activities and related costs which often includes market research and analysis, product development, packaging, consumer testing through to product launch, some of which does not qualify as SR&ED and some which may meet the SR&ED criteria Scientific research is basic or applied research for the purpose of achieving new scientific knowledge. Experimental development is undertaken to expand technological capabilities to produce new or improved materials, products or processes. SR&ED is therefore the eligible project within the business project. 24

64

B - Exercise #2 What is a technological obstacle and why is it important in determining eligibility? A shortcoming or limitation in current technology that prevented you from achieving the technological advancement Technological problems that could not be removed through application of existing knowledge or capabilities A distinguishing feature of an SR&ED project is development of a hypothesis to overcome a known technological obstacle which is a barrier to achieving a technological advance. The systematic investigation to overcome the obstacle must be supported by contemporaneous documentation. 25

65

B – Exercise #3 Relate each of the five questions to one of the three criteria. Was there a scientific or technological uncertainty, an uncertainty that could not be removed by standard practice? Criteria of Technological Uncertainty Did the effort involve formulating hypotheses specifically aimed at reducing or eliminating that uncertainty? Criteria of Technological Uncertainty Was the adopted procedure consistent with the total discipline of the scientific method, including formulating, testing, and modifying the hypotheses? Criteria of Technical Content Did the process result in a scientific or a technological advancement? Criteria of Technological Advancement Was a record of the hypotheses tested and the results kept as the work progressed? Criteria of Technical Content 26

66

B – Exercise #4 Turn to the Project Information on page B-20. This sample was published by the CRA. Review T661 Part 2 Section B Lines 240, 242, 244 and consider the eligibility of the project. Discuss in your group. Are the advancements and obstacles clearly defined? Does the work performed section demonstrate systematic investigation? 27

67

New project format & related example – Nov. 10, 2008 -

New word limits for project descriptions: Standard Practice / objectives – 500 words Advancement (uncertainty) – 500 words Activities – 1000 words Sample form with CRA Project example Data Warehouse development The RDBASE.NET R&D Consortium

– 500 words. Activities – 1000 words. Sample form with CRA Project example. Data Warehouse development. The RDBASE.NET R&D Consortium.")

69

Project: Data warehouse improvement

OBJECTIVE: CPU Utilization 95 % busy to 70 % Response Time 60 to 15 seconds Data Compression 5:1 current - 15:1 goal DEPARTURES FROM STANDARD PRACTICE no relevant methods to characterize non- uniform, dynamic data of this environment. The RDBASE.NET R&D Consortium

70

The RDBASE.NET R&D Consortium

Project #6 II) TECHNOLOGICAL ADVANCEMENTS / UNCERTAINTY: Methods to characterize non-uniform data Compressed data blocks vs entire tables to traverse database III) SYSTEMATIC INVESTIGATION 5 separate development activities The RDBASE.NET R&D Consortium

TECHNOLOGICAL ADVANCEMENTS / UNCERTAINTY: Methods to characterize non-uniform data. Compressed data blocks vs entire tables to traverse database. III) SYSTEMATIC INVESTIGATION. 5 separate development activities. The RDBASE.NET R&D Consortium.")

71

Maximum Efficent Use of Knowledge Corporation ME + U = Knowledge

72

Maximum Efficent Use of Knowledge Corporation ME + U = Knowledge

74

Maximum Efficent Use of Knowledge

75

Maximum Efficent Use of Knowledge

76

Maximum Efficent Use of Knowledge

77

Maximum Efficent Use of Knowledge

78

Maximum Efficent Use of Knowledge

80

The RDBASE.NET R&D Consortium

Technology issues .NET Environment Performance and Scalability: timing issues (deadlocks, races), resource management (memory footprint, garbage collection), exception handling, thread synchronization, responsiveness (startup time, UI load time, response time & refresh rate in web app’s) late binding & reflection (tradeoff - code flexibility vs. safety, runtime performance and scalability) The RDBASE.NET R&D Consortium

, resource management (memory footprint, garbage collection), exception handling, thread synchronization, responsiveness (startup time, UI load time, response time & refresh rate in web app’s) late binding & reflection (tradeoff - code flexibility vs. safety, runtime performance and scalability) The RDBASE.NET R&D Consortium.")

81

Concurrency – Multi-Core Processing The RDBASE.NET R&D Consortium

Hot topical areas Concurrency – Multi-Core Processing bugs like races and deadlocks scheduling mechanisms (required) thread affinity (complexity) scalability (effects exaggerated) The RDBASE.NET R&D Consortium

thread affinity (complexity) scalability (effects exaggerated) The RDBASE.NET R&D Consortium.")

82

A – Software CRA (Canada) focus on “constraints”

· Inter-operability · Conformance to standards · Performance (step response, throughput) · Concurrency · Footprint · Scale-ability · Stability · 3rd party components · legacy requirements The RDBASE.NET R&D Consortium © 2012

· Concurrency. · Footprint. · Scale-ability. · Stability. · 3rd party components. · legacy requirements. The RDBASE.NET R&D Consortium ©")

83

A – Software IRS (USA) – classify types of work

High Probability of Qualifying Activities Emerging fields - AI, speech, image rendering, Hardware integration, New algorithms &/or Techniques, System level work - O/S's or compilers The RDBASE.NET R&D Consortium © 2012

84

A – Software IRS (USA) – classify types of work

Medium Probability of Qualifying Consortium software, Embedded applications (in cell phones, cars, etc), Functional enhancements to existing software, Utility programs (debugger, backup systems, etc.) The RDBASE.NET R&D Consortium © 2012

, Functional enhancements to existing software, Utility programs (debugger, backup systems, etc.) The RDBASE.NET R&D Consortium ©")

85

A – Software IRS (USA) – classify types of work

Low Probability of Qualifying Debugging/QA, GUI or style changes, New certification/validation, Reverse engineering, Vendor products (Cloud services, databases, etc.) The RDBASE.NET R&D Consortium © 2012

The RDBASE.NET R&D Consortium ©")

86

A – Software IRS (USA) – classify types of work (ineligible)

Activities after commercial production: a) Preproduction planning for a finished business component; b) Tooling up for production; c) Trial production runs; d) Trouble shooting involving detecting faults in production equipment or processes; e) Accumulating data relating to production processes; & f) Debugging flaws in a business component. The RDBASE.NET R&D Consortium © 2012

Preproduction planning for a finished business component; b) Tooling up for production; c) Trial production runs; d) Trouble shooting involving detecting faults in production equipment or processes; e) Accumulating data relating to production processes; & f) Debugging flaws in a business component. The RDBASE.NET R&D Consortium ©")

87

C – ELIGIBLE & QUALIFIED EXPENSES LEARNING OBJECTIVES

Introduction to SR&ED expenditures Treatment of the SR&ED expenditure pool Introduction to the traditional and proxy methods Explanation of the significant differences between the two methods 1

88

C - SR&ED Expenditures & Expenditure Pool

SR&ED expenditures include: Salaries & Wages Materials Subcontractors (80% of contract payments for expenditure after 2012) Lease payments (prior to 2014) Overheads Capital equipment (prior to 2014) Third Party Payments SR&ED expenditures are added to a notional pool which is available for deduction or carried forward The pool is the starting point for the calculation of Qualified Expenditures which earn ITCs 2

Lease payments (prior to 2014) Overheads. Capital equipment (prior to 2014) Third Party Payments. SR&ED expenditures are added to a notional pool which is available for deduction or carried forward. The pool is the starting point for the calculation of Qualified Expenditures which earn ITCs. 2.")

89

C - Foreign Expenditures

SR&ED carried on outside of Canada does not create benefits under the program No deduction for capital expenditures No expenditure pool No ITC Limited exception for salaries and wages of Canadian employees working outside Canada 3

90

C - Related To The Business

SR&ED must be related to the business of the taxpayer SR&ED is not a business unless all or substantially all (“ASA”) revenues are derived from SR&ED SR&ED performed by a taxpayer and related to the business of a related corporation is considered to be related to the business of the taxpayer The intention is to provide benefits to performers, not passive investors 4

revenues are derived from SR&ED. SR&ED performed by a taxpayer and related to the business of a related corporation is considered to be related to the business of the taxpayer. The intention is to provide benefits to performers, not passive investors. 4.")

91

C - SR&ED Expenditure Pool

Current Expenditures (taxation years after 1973) Capital Expenditures (taxation years after 1958) Repayments of assistance in the year and all previous years Recapture of ITCs in previous years Other additions such as pools of amalgamated entities LESS Assistance received, receivable or expected Super-allowance benefits amount ITCs claimed to reduce taxable income or refunded in previous years Amounts previously deducted from the pool Other deductions such as insolvency adjustments EQUALS Balance available for deduction in the year or carry forward indefinitely Negative balance = income 5

Capital Expenditures (taxation years after 1958) Repayments of assistance in the year and all previous years. Recapture of ITCs in previous years. Other additions such as pools of amalgamated entities. LESS. Assistance received, receivable or expected. Super-allowance benefits amount. ITCs claimed to reduce taxable income or refunded in previous years. Amounts previously deducted from the pool. Other deductions such as insolvency adjustments. EQUALS. Balance available for deduction in the year or carry forward indefinitely. Negative balance = income. 5.")

92

C – Section B - T661 Sample Calculation of Allowable Expenditures Pool

93

C – Calculation of the pool of deductible expenditures

7

94

C - Method of Claiming Elect each year to use either proxy or traditional method Election is irrevocable, cannot be amended Determines calculation of pool and calculation of Qualified Expenditures Proxy: “directly engaged” salaries and wages, materials, contract payments, lease costs (100% or 50%), no overheads Traditional: “directly attributable” costs including salaries and wages, materials, contract payments, lease costs and other directly attributable and incremental overheads The purpose of section 37 is to permit a taxpayer carrying on business to deduct certain expenditures made in respect of scientific research and experimental development (“SR&ED”). Such expenditures might otherwise not be deductible either because of the possibility that they could be held not to have been incurred for the purpose of gaining or producing income, as provided in paragraph 18(1)(a), or on the basis that they were capital expenditures the deductibility of which is prohibited by paragraph 18(1)(b). Subsection 37(1), which applies where the taxpayer carries on a business in Canada, provides a deduction in respect of both current and capital expenditures on SR&ED in Canada, while subsection 37(2) permits a more limited deduction in respect of any business for SR&ED expenditures of a current nature made outside Canada. Under subsection 37(1) the expenditures made may be deducted in a subsequent taxation year, provided that the taxpayer carries on a business in Canada in the year. 8

, no overheads. Traditional: directly attributable costs including salaries and wages, materials, contract payments, lease costs and other directly attributable and incremental overheads. The purpose of section 37 is to permit a taxpayer carrying on business to deduct certain expenditures made in respect of scientific research and experimental development ( SR&ED ). Such expenditures might otherwise not be deductible either because of the possibility that they could be held not to have been incurred for the purpose of gaining or producing income, as provided in paragraph 18(1)(a), or on the basis that they were capital expenditures the deductibility of which is prohibited by paragraph 18(1)(b). Subsection 37(1), which applies where the taxpayer carries on a business in Canada, provides a deduction in respect of both current and capital expenditures on SR&ED in Canada, while subsection 37(2) permits a more limited deduction in respect of any business for SR&ED expenditures of a current nature made outside Canada. Under subsection 37(1) the expenditures made may be deducted in a subsequent taxation year, provided that the taxpayer carries on a business in Canada in the year. 8.")

95

C - Eligible SR&ED Expenditures Under The Traditional Method

Current Expenditures Expenditures ASA attributable to the prosecution of SR&ED or to the provision of premises, facilities or equipment for the prosecution of SR&ED in Canada Expenditures directly attributable, as determined by regulation, to the prosecution of SR&ED or to the provision of premises, facilities or equipment for SR&ED in Canada No lease payments after 2013 Capital expenditures ASA for the provision of premises, facilities or equipment for SR&ED No capital expenditures after 2013 9

96

C - Eligible SR&ED Current Expenditures Under The Traditional Method

The portion of salaries and wages of employees who directly undertake, supervise or support SR&ED The cost of materials consumed or transformed in the prosecution of SR&ED Payments to contractors for SR&ED performed on behalf of the taxpayer Prior to 2014, the cost of leasing SR&ED equipment used ASA for SR&ED or Pro rata share of cost of leasing equipment used partly for SR&ED, and Overheads (directly related and incremental) 10

10.")

97

C - Eligible SR&ED Current Expenditures Under The Proxy Method

Salaries and wages of employees directly engaged in SR&ED Materials consumed or transformed in the prosecution of SR&ED Payments to contractors for SR&ED performed on behalf of the taxpayer Until 2014, cost of leasing SR&ED equipment (other than general purpose office equipment and furniture (GPOEF) used ASA for SR&ED) 50% of cost of leasing equipment (not GPOEF) used at least 50% for SR&ED (until 2014). No “overhead or other expenditures” in the claim 11

used ASA for SR&ED) 50% of cost of leasing equipment (not GPOEF) used at least 50% for SR&ED (until 2014). No overhead or other expenditures in the claim. 11.")

98

C - Adjustments - Expenditure Pool

The expenditure pool starts with current and capital expenditures and is then adjusted for several amounts Deductions: Government & non-government assistance including provincial ITCs Federal ITC claimed in the prior year Proceeds of the sale of capital assets previously claimed as SR&ED Additions: Recapture of ITC paid in the previous year Repayments of government assistance previously deducted from the pool 12

99

C - Unpaid Amounts Unpaid amounts = expenditures incurred in a year that have not been paid 180 days after year-end For the purposes of calculating SR&ED Expenditures: Unpaid salaries, wages and other remuneration must be reported in year incurred but are not deductible until paid Unpaid amounts other than salaries, wages and other remuneration are deductible in the year incurred (no restrictions) but will not earn ITCs until paid 13

but will not earn ITCs until paid. 13.")

100

C – Prepaid Expenditures

Prepaid amounts considered incurred in the year Third Party Payments to approved research institutes, universities and non-profit R&D corporation are added to the pool when incurred Except non-arm’s length payments which are not added until paid Prepaid amounts not considered incurred in the year In-house expenditures and contract SR&ED payments Third Party Payments to corporations resident in Canada (other than non-profit R&D corporations) Other Third Party Payments to non-arm’s length parties These amounts are not added to the pool until the services are rendered 14

Other Third Party Payments to non-arm’s length parties. These amounts are not added to the pool until the services are rendered. 14.")

101

C – Exercise #1 What are the main differences between the proxy method and the traditional method? Proxy: the proxy method provides a notional amount in lieu of overhead amounts such as indirect salaries and wages, supplies, facilities maintenance, administrative costs and other variable direct costs that are related to the SR&ED The proxy method includes: Directly engaged salaries and wages, 100% or 50% of lease costs, and actual 5 The proxy method does not include overhead amounts including indirect salaries and wages and other amounts that may be related to the SR&ED but are not included in the eligible expenditures for this method Contract payments and materials costs are the same under both methods 15

102

C – Exercise #1 What is the main difference between the proxy method and the traditional method? Traditional: the traditional method includes all incremental and directly attributable expenditures, including: directly engaged salaries and wages, plus other salaries and wages for staff that support the SR&ED, administrative, maintenance, shop floor, supervisory the SR&ED share of allocated overheads and other incremental expenditures Traditional method includes all directly attributable amounts including: Directly engaged salaries and wages, plus other salaries and wages for staff that support the SR&ED, administrative, maintenance, shop floor, supervisory The SR&ED share of allocated overheads and other incremental expenditures 16

103