Download presentation

Presentation is loading. Please wait.

1

Labuan IBFC: Tropical Paradise in the South China Sea

1

2

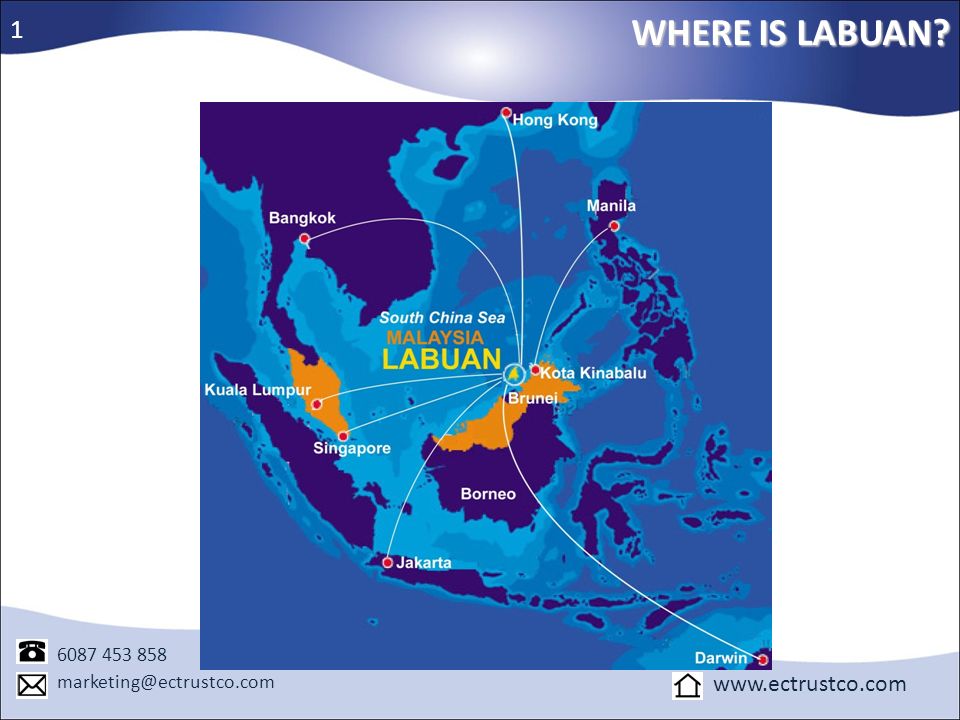

WHERE IS LABUAN? 1 www.ectrustco.com 6087 453 858

2

3

WHO ARE WE? 2 EC Trust (Labuan) Bhd Providing professional services:

Incorporated under Labuan Companies Act, 1990 on 3rd March 2003 Licensed Trust Company under Labuan Financial Services and Securities Act 2010 Providing professional services: Incorporation services and formation of Labuan entities 2. In-house customised support services – Corporate secretarial services Trusts, holding of shares on trust Bank account Legal advice Accounting Custodial services

4

WHO ARE WE? 3 PETER SEARLE B.A. LLB (Hons), LLM Managing Director

Qualifications: Honours degree in Law, including International Law - Australian National University, 1979 Admitted as a Solicitor and Barrister - Supreme Court of Victoria in 1982 completed a Masters of Law in Taxation at Monash University in 1985 Tax and trust law specialist for over 33 years: Australian Taxation Office Canberra Senior Taxation Manager, Coopers and Lybrand Australian barrister Managing Director and Trust Officer, EC Trust (Labuan)

")

5

WHO ARE WE? 4 MARINA MALIM BLS (Hons) Director Qualifications:

Degree of Legal Studies (Hons) - University Teknologi MARA (UiTM) Pursuing her Institute of Chartered Secretaries and Administrator (ICSA) certificate from MAICSA Experience: 2009- present. Director and Trust Officer of EC Trust (Labuan) Bhd Specialising in legal and compliance issues, Labuan company formation and incorporation, licensing, tax planning and secretarial matters under the Labuan laws

- University Teknologi MARA (UiTM) Pursuing her Institute of Chartered Secretaries and Administrator. (ICSA) certificate from MAICSA. Experience: present. Director and Trust Officer of EC Trust (Labuan) Bhd. Specialising in legal and compliance issues, Labuan company formation and. incorporation, licensing, tax planning and secretarial matters under the Labuan laws")

6

WHY CHOOSE LABUAN IBFC? 6 www.ectrustco.com 6087 453 858

7

Stability, certainty, reliability and protection

7 LEGAL FRAMEWORK Issue no par value shares or fractions of shares English common law tradition with modern legislation Make offers or invitations to 50 persons (without Authority’s approval) Restructure or reduce capital (without court approval) Modern company concepts Purchase or finance acquisition of own shares Carry on business with residents Operate private fund (by notification) Dissolve without court approval and appointment of liquidator Company record not open to public inspection Stability, certainty, reliability and protection

Restructure or reduce capital (without court approval) Modern company concepts. Purchase or finance acquisition of own shares. Carry on business with residents. Operate private fund (by notification) Dissolve without court approval and appointment of liquidator. Company record not open to public inspection. Stability, certainty, reliability and protection")

8

LEGAL FRAMEWORK Labuan Entities 8 www.ectrustco.com 6087 453 858

9

9 DOUBLE TAX AGREEMENTS Labuan is part of Malaysia and therefore, qualifies for double taxation relief where Malaysia is contracting party to a specific DTA. Companies that wish to invest in countries where a DTA does not exist between both countries, can establish a Labuan intermediary company with the benefit of Malaysian treaties. Malaysia has 70 DTAs.

10

MALAYSIA : 70 DOUBLE TAX AGREEMENTS

10 MALAYSIA : 70 DOUBLE TAX AGREEMENTS 10

11

11 EXCHANGE CONTROL Labuan company is regarded as non-resident for exchange control purposes. Labuan company is generally not subject to any exchange control requirements.

12

Labuan Business Activity

12 TAX BENEFITS Income Tax Act 1967 Other Activities Labuan Company Labuan Business Activity LBATA 1990 3% or MYR20,000 Trading Non-Trading Not taxable

13

(Section 2 of Labuan Business Activity Tax Act 1990)

13 LABUAN TRADING ACTIVITIES “Labuan trading activity” includes banking, insurance, trading, management, licensing, shipping operations or any other activity which is not a Labuan non-trading activity (Section 2 of Labuan Business Activity Tax Act 1990) ________________________________________________________ Tax charged at the rate of 3% based on the net profits reflected in the audited accounts. or upon election i.e. Labuan Company may choose to pay a fixed sum of MYR 20,000.

________________________________________________________. Tax charged at the rate of 3% based on the net profits reflected in the audited accounts. or. upon election i.e. Labuan Company may choose to pay a fixed sum of MYR 20,")

14

14 LABUAN NON-TRADING ACTIVITIES “Labuan non-trading activity” means an activity relating to the holding of investments in securities, stock, shares, loans, deposits or any other properties by a Labuan entity on its own behalf; ________________________________________________________ Gains from Labuan non-trading activities which include receipt of dividends, sale of investments and interest income from Labuan non-trading activities are not subject to tax in Malaysia.

15

15 TAX REQUIREMENTS The chargeable profits of Labuan entity carrying on Labuan trading activity will be taken from net profits as reflected in the audited accounts. No audited accounts need to be submitted with tax return if elect to pay MYR 20,000.

16

Personal tax exemption

16 TAX BENEFITS No indirect taxes No witholding taxes Tax free dividends Other Tax Benefits Exempt from stamp duty Personal tax exemption

17

service taxes, excise / import duties

17 TAX BENEFITS No Indirect Taxes No indirect taxes such as sales taxes, service taxes, excise / import duties and export duties levied on Labuan companies since Labuan enjoys free port status

18

No Withholding Taxes TAX BENEFITS

18 TAX BENEFITS No Withholding Taxes Royalties, interest and technical or management fees paid by Labuan company to non – resident person or Labuan Company are exempted from income tax and thus not subjected to withholding tax (“WHT”).

")

19

Exempt from Stamp Duty TAX BENEFITS 19

Labuan companies qualify for stamp duty exemption on: Instruments executed by Labuan company in connection with Labuan business activity. Memorandum & Articles of Association of Labuan company. Instruments of transfer of shares in a Labuan company.

20

TAX BENEFITS 100% exemption on director fees

20 TAX BENEFITS Personal Tax Exemption for Expatriates of Labuan Company 100% exemption on director fees received by a non-citizen director 50% tax exemption on gross employment income of a non Malaysian Resident working in a managerial capacity in a Labuan financial institution

21

on Labuan allowances and housing allowances

21 TAX BENEFITS Tax Rebate for Malaysians 50% tax exemption on Labuan allowances and housing allowances of Malaysian citizens working in a Labuan financial institution

22

WHY CHOOSE LABUAN ENTITIES?

22 WHY CHOOSE LABUAN ENTITIES?

23

Tax Planning Opportunities holding Investment Company

23 WHY CHOOSE LABUAN ENTITIES Tax Planning Opportunities outbound investment / international trading international investment leasing activities holding Investment Company A hub for

24

A Hub for Investments and International Trading

24 WHY CHOOSE LABUAN ENTITIES A Hub for Investments and International Trading Singapore Malaysian Co. Labuan Co. (LC) India China Thailand

India. China. Thailand")

25

A Hub for International Trading and Investments

25 WHY CHOOSE LABUAN ENTITIES A Hub for International Trading and Investments Dividend income from the Labuan Company Dividend income received from the Labuan Company is tax exempt in Malaysia and world-wide under the participation exemption. Dividend income received is available for an exempt distribution in Malaysia.

26

Dividend income received is available for exemption as follows:-

26 WHY CHOOSE LABUAN ENTITIES A Hub for Investments and International Trading Dividend income received is available for exemption as follows:- Labuan Co. Exempt dividend Malaysian Co. Exempt dividend Shareholders

27

WHY CHOOSE LABUAN ENTITIES

27 WHY CHOOSE LABUAN ENTITIES A Hub for International Investment Labuan entities may be used to penetrate into Asian market Singapore Thailand Foreign Co. Labuan Co. (LC) Vietnam Cambodia

Vietnam. Cambodia")

28

A Hub for Leasing Activities

28 WHY CHOOSE LABUAN ENTITIES A Hub for Leasing Activities Leasing business means: Business of letting or sub-letting property on hire for the purpose of the use of such property by the hirer regardless whether the letting is with or without an option to purchase the property, including charters of ships, “property” includes any plant, machinery, equipment or other chattel attached or to be attached to the earth “charters of ships” means bareboat charters only and does not include the transportation of passengers or cargo by sea or the charter of ships on a voyage or time charter

29

WHY CHOOSE LABUAN ENTITIES

29 WHY CHOOSE LABUAN ENTITIES Flow Chart

30

An annual license fee of MYR 40,000 is payable

30 WHY CHOOSE LABUAN ENTITIES? An annual license fee of MYR 40,000 is payable plus MYR 20,000 for each subsequent transaction conducted with Malaysian residents. Labuan leasing companies providing lease facilities to non- residents or conducting “out-out” transactions are not required to pay annual fees or the subsequent transaction fees.

31

Patent, Royalty and Copyright Holding

31 WHY CHOOSE LABUAN ENTITIES? Patent, Royalty and Copyright Holding Intellectual property including computer software, technical knowledge, patents, trademarks and copyrights, can be owned by, or assigned to, a Labuan company. The rights can be franchised to companies around the world and the resultant income may be accumulated in Labuan or distributed by the Labuan company free of withholding tax and received tax free under the participation exemption.

32

Labuan IBFC: New Regulatory Updates

32 Labuan IBFC: New Regulatory Updates 32

33

New Legislation 33 Labuan Companies Act 1990

Labuan Financial Services Authority Act 1996 Labuan Financial Services and Securities Act 2010 Labuan Foundations Act 2010 Labuan Business Activity Tax Act 1990 Labuan Trusts Act 1996 Labuan Islamic Financial Services and Securities Act 2010 Labuan Limited Partnerships And Limited Liability Partnership Act 2010

34

Labuan Companies Act 1990 34 www.ectrustco.com 6087 453 858

35

35 Labuan Companies Act 1990 Issue no par value shares or fractions of shares Restructure or reduce capital (without court approval) Modern company concepts Purchase or finance acquisition of own shares Carry on business with residents Dissolve without court approval and appointment of liquidator Company record not open to public inspection

36

Labuan Business Activity Act 1990

36 Labuan Business Activity Act 1990

37

Labuan Business Activity Act 1990

37 Labuan Business Activity Act 1990 Shipping Operations in Malaysia “Labuan trading activity” includes banking, insurance, trading, management, licensing, shipping operations or any other activity which is not a Labuan non-trading activity Allowed “Shipping operations” means the transportation of passengers or cargo by sea or the letting out on a charter of ships on a voyage or time charter basis – Section 2

38

DTA Benefits Labuan Business Activity Act 1990

38 Labuan Business Activity Act 1990 Labuan entities elect under Income Tax Act 1967 to re-engage DTA benefits DTA Benefits Benefits in source country 1. Business profits exempt 2. Lower withholding tax rates

39

Labuan Business Activity Act 1990

39 Labuan Business Activity Act 1990 Information sharing Malaysian Government will not permit fishing expeditions. No automatic information sharing. Prima facie case must be made out by the Government making the request.

40

Labuan Business Activity Act 1990

40 Labuan Business Activity Act 1990 Advance Ruling Advance Ruling enables Labuan entities to seek a ruling of the Director General of IRB on the application of LBATA to Labuan entities. Section 17B

41

Labuan Financial Services

41 Labuan Financial Services And Securities Act 2010

42

Securities laws Labuan Insurance Exchanges (LFX) Labuan Trust Company

42 Labuan Financial Services and Securities Act 2010 Securities laws Labuan Insurance Exchanges (LFX) Labuan Trust Company Labuan Banking

Labuan Trust Company. Labuan Banking")

43

Key Features Labuan Financial Services and Securities Act 2010 43

1. Make invitations to 50 persons without the Authority’s approval 2. Operate private funds without prior approval from any Authority 3. Operate in a strictly confidential and private business environment which is entrenched by Malaysian Statutes supported by fiercely independent government in Malaysia’s post-colonial era

44

Key Features Labuan Financial Services and Securities Act 2010 44

4. Licensed insurance brokers being financial planners - The new definition of insurance broker has been extended to expressly include a person who is licensed to “analyse the financial circumstances of another person and provides a plan to meet that other person’s financial needs and objectives…”

45

Labuan Foundations Act 2010

45 Labuan Foundations Act 2010

46

Labuan Foundations Act 2010 46 Labuan Foundations (LF) Capacity of LF

Beneficiaries Management Founder of LF Purpose and Objective S.50 LF is a body corporate and may sue and be sued in its corporate name Founder act as an officer of LF S.6(1) A resident or a non - resident S.7(1) The main purpose of LF shall be the management of its property. S.5(1) A resident or a non - resident Provide for the appointment of a council to manage LF. Income derived from Malaysian property falls under ITA 1967 Property of LF cannot include Malaysian property except with prior approval from authority or LF is charitable S.7(2) LF may also include other lawful objects Income derived from non -Malaysian property falls under LBATA

A resident or a non - resident. S.7(1) The main purpose of LF shall be the management of its property. S.5(1) A resident or a non - resident. Provide for the appointment of a council to manage LF. Income derived from Malaysian property falls under ITA Property of LF cannot include Malaysian property except with prior approval from authority or LF is charitable. S.7(2) LF may also include other lawful objects. Income derived from non -Malaysian property falls under LBATA.")

47

Labuan Foundations Act 2010 47 Labuan Foundations (LF)

Benefits Rights to information :- Rights of beneficiaries to request for information concerning the property of LF Confidentiality:- No information or documents concerning LF may be divulged to a third party unless with court order Asset protection:- LF grants asset protection unless the assets are fraudulently disposed to LF. Distribution of assets :- Permissible to beneficiary unless the distribution is to defeat the creditor claim. Unenforceability of a foreign claim

48

Labuan Foundations Act 2010 48

Foundation is a legal entity. Liability of foundation is limited to the value of its net assets. Allows redomicilation of foundation into or out of Labuan. Where LF is dissolved and there remains some property after its dissolution, those properties shall be the property of the beneficiary(ies). A foundation can be deemed Islamic if it subscribes to Shariah principles and appoints a Shariah advisor.

. A foundation can be deemed Islamic if it subscribes to Shariah principles and appoints a Shariah advisor")

49

Labuan Trust Act 1996 49 www.ectrustco.com 6087 453 858

50

50 Labuan Trust Act 1996 Default provision : exist perpetuity Purpose trust, charitable trust, promotion of religion, advancement of human rights and fundamental freedom Flexibility for a fixed-term trust to be converted to perpetual or vise versa Labuan Special Trust Allow trust to hold shares in Labuan Holding Company, which in turn may hold assets such as cash, real estate, art, securities, businesses, insurance policies etc Retention of day-to-day control over the direction and management of investments and businesses can be held by a settlor or protector and the trustee is not liable for losses.

51

WHAT ARE YOU WAITING FOR?

51 WHAT ARE YOU WAITING FOR? What are you waiting for? Come to Labuan or visit our website at and join the ranks of successful companies and individuals gaining the benefits of Labuan, Malaysia.

52

Thank you 52 Tel : +60 87 453 858 EC Trust (Labuan) Bhd.

Wisma EC Trust U0195 Jalan Merdeka 87007 Labuan F.T Malaysia Tel : Fax: Web: Thank you

Similar presentations

>")

Procurement Technical Assistance Center (PTAC) FAR.>")