Download presentation

Presentation is loading. Please wait.

1

PRIMER COMMUNITY FOUNDATIONS OF CANADA PILOT PROJECT JULY 2008

2

Table of Contents I Introduction to Responsible Investment (p. 3)

- Jantzi Research II Shareholder Action and Proxy Voting (p. 34) - The Ethical Funds Company III Community Investment (p. 45) - Tides Canada Foundation and Vancity Community Foundation IV Developing a Responsible Investment Policy (p. 79) - SHARE V Bibliography (p. 95) Note: The RIPP Primer is compiled from different source presentations. Originals are credited in detail in the Bibliography.

- The Ethical Funds Company. III Community Investment (p. 45) - Tides Canada Foundation and Vancity Community Foundation. IV Developing a Responsible Investment Policy (p. 79) - SHARE. V Bibliography (p. 95) Note: The RIPP Primer is compiled from different source presentations. Originals are credited in detail in the Bibliography.")

3

I Introduction to Responsible Investment

4

What’s in a name? the integration of environmental, social and governance parameters into the investment decision making process SRI MBI

5

Responsible Investment

the incorporation of an institution’s central purpose or calling into its investment decision making process. Responsible Investment

6

Definition of RI There are many different names given to responsible investment, but one common definition: “The integration of environmental, social and governance factors in the selection and management of investments.” From Social Investment Organization

7

Four Approaches to RI ESG Integration – the integration of social, environmental and governance factors in stock selection Screening – selecting investments on the basis of pre-identified social, environmental and governance factors Shareholder action – exercising ownership rights such as proxy voting, management negotiations, shareholder resolutions Community investment – assets invested in local community development

8

Responsible investing is becoming mainstream…

9

Europe retail SRI in Europe totals more than €48.7 billion in assets – increase of 102% from year before institutional SRI in Europe totals about €2 trillion in assets under management

10

Government mandated disclosure: a catalyst for change

July 2000 – UK Pensions Disclosure Regulation: “the extent (if at all) to which social, environmental or ethical considerations are taken into account in the selection, retention and realisation of investments” Belgium, France, Germany, Italy Pension funds acting on SRI France - Fonds de Réserve Pour Les Retraites Netherlands – ABP, PGGM Scandinavia – Sweden, Denmark, Norway Australia 2001 – Financial Services Reform Act

to which social, environmental or ethical considerations are taken into account in the selection, retention and realisation of investments Belgium, France, Germany, Italy. Pension funds acting on SRI. France - Fonds de Réserve Pour Les Retraites. Netherlands – ABP, PGGM. Scandinavia – Sweden, Denmark, Norway. Australia – Financial Services Reform Act.")

11

United Kingdom February Trustee Act requires charity trustees to make sure investments are suitable, not only financially but also with regard to the charity’s stated aims increasing number of charities and foundations embracing SRI Barnardo’s

12

Barnardo’s UK charity focused on children - founded 1866

“…not to hold investments in companies whose activities are considered to be to the detriment of children and where we believe donor support might be adversely affected.” companies considered to exploit children (usually in the Third World) in the manufacture of their products companies who derive significant income from the production or distribution of pornography or adult entertainment television companies which derive more than 10% of their turnover from the production or sale of tobacco products

in the manufacture of their products. companies who derive significant income from the production or distribution of pornography or adult entertainment television. companies which derive more than 10% of their turnover from the production or sale of tobacco products.")

13

SRI Assets in the U.S.

14

U.S. Foundations interviewed 92 foundations – 64 private, 24 community and 4 corporate during the past ten years the number of U.S. foundations involved in SRI has doubled fastest growth in foundations with less than $200 million in assets under management F.B. Heron Foundation, David and Lucile Packard Foundation, Vermont Community Foundation

15

U.S. Foundations focuses on development and implementation – “from idea to execution’ 12 case studies highlighting a variety of experiences – Kalamazoo Community Foundation risk, return, and impact

16

SRI Assets Under Management in Canada

$503 billion in SRI assets in 2006 increase from $65.5 billion over two years Jantzi Research Inc. Jantzi Research Inc.

17

The Legality of RI…

18

Harries vs. Church Commissioners

Trustees may avoid investing in a company if it clearly conflicts with the aim or purpose of the organization, even though it may be the most prudent investment financially. In those circumstances where trustees are satisfied that investing in a company engaged in a particular type of business would conflict with the very objects their trust is seeking to achieve, then they’re duty bound not to invest.

19

Legal Perspective October 2005 – Freshfields Bruckhaus Deringer

A legal framework for the integration of environmental, social and governance issues into institutional investment leading international law firm, with over 2,400 lawyers in 28 offices in 18 countries across Europe, Asia and the U.S. “…integrating ESG considerations into an investment analysis so as to more reliably predict financial performance is clearly permissible and is arguably required in all jurisdictions.”

20

Evidence that it is possible to implement RI and generate a competitive rate of return…

21

Mainstream Investment Initiatives and Investors

Multilateral mainstream SRI initiatives Carbon Disclosure Project CICA - MD&A Disclosure About the Financial Impact of Climate Change and other Environmental Issues UN Principles of Responsible Investment Pension Funds who have endorsed UNPRI - Canada Pension Plan Investment Board - British Columbia Investment Management Corp. - Caisse de dépot

22

What’s the Opportunity?

generation of alpha growing body of research highlighting link between superior sustainability performance and enhanced share value

23

Materiality studies demonstrate value of ESG

10 sell-side brokerage houses invited to undertake reports across sectors/ themes to evaluate the materiality of environmental, social and governance (ESG) issues ESG issues are material – there is robust evidence that ESG issues affect shareholder value in both the short- and long-term the impact of ESG issues on share price can be valued and quantified materiality varies across sector and themes

issues. ESG issues are material – there is robust evidence that ESG issues affect shareholder value in both the short- and long-term. the impact of ESG issues on share price can be valued and quantified. materiality varies across sector and themes.")

24

Materiality Studies 10 academic/20 sell-side brokerage studies

evidence suggests that there appears to be no performance penalty from taking ESG factors into account in the investment management process 10 studies are positive, 7 neutral, and 3 negative SRI leading to underperformance is a misconception

25

Positive Performance of Sustainability Indexes

e.g. Jantzi Social Index®

26

Jantzi Social Index® - Backtest

27

Jantzi Social Index® - Backtest

28

JSI® - Comparative Values (through April, 2008)

RETURNS Apr 2008 3 mths 6 mths 1 yr 3 yr* 5 yr* Inception* Inception** JSI 5.90% 7.60% -3.90% 5.45% 16.21% 17.80% 8.32% 94.71% S&P/TSX COMPOSITE 4.60% 6.66% -3.42% 6.58% 16.837% 18.65% 8.19% 92.71% S&P/TSX 60 5.42% 7.36% -1.73% 10.15% 18.80% 19.47% 8.16% 92.23% Source: State Street Global Advisors (SSgA) * Annualized ** Cumulative (since 01/01/2000)

* Annualized ** Cumulative. (since 01/01/2000)")

29

JSI® - Comparative Returns (through April 30, 2008)

")

30

Why Mission-Based Organizations Invest in RI

Advance organizational mission Align investments with values Enhance shareholder value Reduce reputational risk Provide marketplace differentiation Provide universal investors with investment options May be legally required

31

Different Screening Approaches

Negative screens – also referred to as exclusionary screens Best-of-sector approach – allows investment in, e.g., the top 20% to 35% of companies in every sector, ranked on sustainability performance grounds. This can allow funds to invest in companies from every industry, as long as they rank the companies chosen comparatively well for environmental, social and governance (ESG) criteria Positive screens - usually used to described thematic focus such as cleantech/renewable energy

criteria. Positive screens - usually used to described thematic focus such as cleantech/renewable energy.")

32

Companies are Rated for their ESG Performance

33

Standards for determining social/environmental performance

Strengthening Communities community consultation aboriginal relationships charitable giving Environment UNEP: The Hazardous Chemicals and Wastes Conventions (e.g. Stockholm Convention on Persistent Organic Pollutants) Human Rights UN Declaration of Human Rights United Nations Global Compact

Human Rights. UN Declaration of Human Rights. United Nations Global Compact.")

34

Shareholder Action and Proxy Voting

II Shareholder Action and Proxy Voting

35

The Name Game Shareholder Action Corporate Engagement

Shareholder Engagement Shareholder Action DON’T CLICK Shareholder Activism Corporate Dialogue

36

Shifting perceptions Screening

Source: Fearless Forecast, ©2005 Mercer Human Resource Consulting LLC and Mercer Investment Consulting, Inc.

37

Shifting perceptions ESG evaluations

Source: Fearless Forecast, ©2005 Mercer Human Resource Consulting LLC and Mercer Investment Consulting, Inc.

38

Shifting perceptions Active ownership

Source: Fearless Forecast, ©2005 Mercer Human Resource Consulting LLC and Mercer Investment Consulting, Inc.

39

Shareholder Action Definitions

Monitoring corporate performance Seeking changes in corporate practice through dialogue May involve the use of shareholder proposals Shareholder proposal Request that a company undertake specific action Companies are legally obliged to include proposals in management proxy circular Voted on at annual general meeting

40

Why Conduct Shareholder Action?

Value Engage to acquire an informational advantage Engage to encourage long term value creation Engagement to control risk and boost performance Values Engage to make companies more sustainable Engage to better fulfill your mission Need examples at each level

41

Shareholder Action Approach

Identify Candidates and Establish Goals Establish Stakeholder Coalition Communicate Concerns to Company and Offer Dialogue Company Acknowledges Concerns and Agrees to Dialogue Company Fails to Acknowledge Concerns Company Agrees to Dialogue File Shareholder Proposal Meet with Company We have 3 core values which guide our Sustainable Investment program > reflect broad Canadian values 1. Encourage companies to reduce their negative impacts on the environment, adopt a precautionary approach, and work towards business practices that help restore the environment 2. We expect companies to accept their responsibility to protect and promote human rights within their sphere of influence. This means they should avoid being complicit in human rights violations and should also protect international labor rights 3. A company’s stakeholders include shareholders, employees, customers, suppliers. We encourage companies to be responsive to their stakeholders, listening to their concerns and developing business practices that seek to address these concerns. Company Opposes Proposal in Proxy Circular Establish Course of Action Solicit Support and Move Proposal at AGM Follow-up and Monitor Company Progress Assess Results and Establish Next Steps

42

Proxy Voting Definitions

Owners of common stock have the right to vote on a variety of company policies and practices Opportunity to vote comes in advance of annual meeting Voting items from management and shareholders Published in Management Information Circular Proxy voting guidelines Establish proxy voting positions and decision rules on corporate governance and social issues Proxy voting services Assist investors with the proxy management, analysis, voting, and disclosure process

43

Proxy Voting Disclosure

44

Proxy Voting Current Web Disclosure

45

III Community Investing

46

Social Purpose Business

Different Names for Community Investing… Social Finance Triple Bottom Line (TBL) Community Economic Development (CED) Mission Related Investing (MRI) Mission Based Investing (MBI) Social Enterprise Social Economy Socially Responsible Investing (SRI) Environment Social Governance (ESG) Program Related Investment (PRI) Social Investing Social Purpose Business Social Venture Fund

Community Economic Development (CED) Mission Related Investing (MRI) Mission Based Investing (MBI) Social Enterprise. Social Economy. Socially Responsible Investing (SRI) Environment Social Governance (ESG) Program Related Investment (PRI) Social Investing. Social Purpose Business. Social Venture Fund.")

47

Context Driving Financial Innovation

New perspectives on “theory of change” beyond “grantsmanship” Leveraging more assets: convening capability, networks, long term capital, leadership, etc Recognizing urgency and scale of enviro-social challenges; new rules of the game (e.g. carbon’s impact) Rise of social entrepreneurship Search for social innovation’s scaled impact Moving beyond sectoral silos (government, voluntary, business): role of hybrid space & relationship to social innovation Recognizing value of community asset building and social enterprise Benefiting from international lessons & best practices (UK, US, etc.)

Rise of social entrepreneurship. Search for social innovation’s scaled impact. Moving beyond sectoral silos (government, voluntary, business): role of hybrid space & relationship to social innovation. Recognizing value of community asset building and social enterprise. Benefiting from international lessons & best practices (UK, US, etc.)")

48

Foundations Involved Already

Active foundations in MRI/MBI/CI field (partial list): JW McConnell Family Foundation (Qwest U loan); Ivey, Metcalfe: NCC Revolving Fund with RBC (in formation) with foundation loan guarantees Edmonton Community Foundation (Social Enterprise) Vancity Community Foundation (Groans: grant/loans) Vancouver Foundation (SRI, SVF) Endswell Foundation (non profit building) Tides Canada Foundation (social enterprise) Ilahie Foundation (non profit building) Bealight Fdn/Social Capital Partners (social enterprise) Muttart Foundation (non profit building) CAIC (Canadian Alternative Investment Co-op) handling CI investments for religious charities; [Jubilee Fund]

: JW McConnell Family Foundation (Qwest U loan); Ivey, Metcalfe: NCC Revolving Fund with RBC (in formation) with foundation loan guarantees. Edmonton Community Foundation (Social Enterprise) Vancity Community Foundation (Groans: grant/loans) Vancouver Foundation (SRI, SVF) Endswell Foundation (non profit building) Tides Canada Foundation (social enterprise) Ilahie Foundation (non profit building) Bealight Fdn/Social Capital Partners (social enterprise) Muttart Foundation (non profit building) CAIC (Canadian Alternative Investment Co-op) handling CI investments for religious charities; [Jubilee Fund]")

49

How Do Social Entrepreneurs Finance Their Great Ideas?

Social entrepreneurs are seeking: Scale, Durability, Impact That requires resilient, sustainable financing Traditional nonprofit external funding sources – charitable donations and Gs+Cs – face challenges More likely option is “business model”: social enterprise or hybrid (part nonprofit, part enterprise) NEXT What is social finance???

NEXT What is social finance")

50

Challenge becomes: How to finance social entrepreneurs’ enterprises?

Moving from grants to other forms of finance…

51

NONPROFITS DEPEND ON FEW SOURCES OF INCOME

40% provincial, 9% federal Government Earned Income Donations and Grants Other

52

Growing Donations But Declining Donors: 1984 to 2005

Donors as a % of Taxfilers Average Donation ($) Source: CRA compiled by Imagine Canada

Source: CRA compiled by Imagine Canada.")

53

finance with a social or environmental mission

Social finance is… finance with a social or environmental mission Or Social finance is a sustainable approach to managing money that delivers social, environmental dividends and economic return through social enterprises operating in the non-profit or public benefit universe.

54

Social Finance Exists Across A Broad Continuum…

HIGH INVOLVEMENT Venture philanthropy Venture capital CHARITABLE COMMERCIAL Traditional grant making Bank lending LOW INVOLVEMENT Adapted from Margaret Bolton, 2003

55

Social finance’s most visible example is MICROFINANCE…

56

Social enterprise is… A business with primarily social (and/or environmental) objectives whose surpluses are principally reinvested for that purpose in the business or in the community, rather than being driven by the need to maximise profit for shareholders and owners...

objectives whose surpluses are principally reinvested for that purpose in the business or in the community, rather than being driven by the need to maximise profit for shareholders and owners...")

57

Social finance for public benefit

Sources Intermediaries Mechanisms Recipients Uses The flow of financial capital to human need uses: Affordable Housing Social Enterprise Support for working families Health & Home Care Community Development Social Economy Clean Technology Microfinance Fair Trade Green Building Education Bottom of the Pyramid (source: market sector listing adapted from

58

Social Finance Examples

Local community development The Columbus Foundation used $2 million PRI to seed an $18 million low-cost housing fund to build 1,600 new units of affordable housing. The Social Enterprise Fund (SEF) is designed to fuel the social economy by providing alternative financing, leveraging mainstream funding, and providing technical assistance to social entrepreneurs. The SEF will be capitalized in the amount of $10.5M over five years. Key financial partners are likely to include the City of Edmonton, the Edmonton Community Foundation, other levels of government and private donations. Startup or expansion capital in underserved communities Deutsche Bank created an innovative $20 million investment fund to finance the expansion of eye care hospitals in developing countries. The Eye Fund I will provide loans and guarantees to support the development of affordable, sustainable and accessible eye care for the world's poor while providing a near-market return Debt mechanisms Millions in loans to community finance institutions and social enterprises by Vancity, Citizens Bank and Calvert Foundation’s Community Investment Note, Using public policy & tax system PLAN (Planned Lifetime Advocacy Network) promoted Registered Disability Savings Plan (RDSP), families are incentivized to save for disabled children who will survive them

is designed to fuel the social economy by providing alternative financing, leveraging mainstream funding, and providing technical assistance to social entrepreneurs. The SEF will be capitalized in the amount of $10.5M over five years. Key financial partners are likely to include the City of Edmonton, the Edmonton Community Foundation, other levels of government and private donations. Startup or expansion capital in underserved communities. Deutsche Bank created an innovative $20 million investment fund to finance the expansion of eye care hospitals in developing countries. The Eye Fund I will provide loans and guarantees to support the development of affordable, sustainable and accessible eye care for the world s poor while providing a near-market return. Debt mechanisms. Millions in loans to community finance institutions and social enterprises by Vancity, Citizens Bank and Calvert Foundation’s Community Investment Note, Using public policy & tax system. PLAN (Planned Lifetime Advocacy Network) promoted Registered Disability Savings Plan (RDSP), families are incentivized to save for disabled children who will survive them.")

59

Collaborative approaches and blended returns

Growing social and environmental pressures + government and market failure = the conditions for social innovation Projected Income New Social Finance Expanding Earned Income Existing Earned Income Gvrnt Gs & Cs Charitable Donations

60

Social Finance Supports Businesses in the Public Benefit Universe

Low Profit Limited Liability Companies (L3C)

")

61

- managing other’s money

TAX Individuals INVEST How does capital flow? Government Organizations Financial Entities - managing other’s money From the source Into an organization For use in either DIRECT Operations Programs Assets

62

Foundation MBI, MRI, PRI PRIs are a new tool for philanthropy

Employ an investment approach What’s the rationale? New arena for impact Leverage potential: partnerships (business, non-profit, government) and hybrids Supports new trend of SE organizational profile Embraces the financial sustainability & financial resiliency agenda Diversifies asset management

and hybrids. Supports new trend of SE organizational profile. Embraces the financial sustainability & financial resiliency agenda. Diversifies asset management.")

63

Canada Revenue Agency Rules

CRA includes CI in its 1999 Community Economic Development (CED) policy, referring to PRIs Two frameworks applicable: PRIs (Program Related Investments) with charities Regular Investing CRA Off-the Record Policy Consultation (2008)

policy, referring to PRIs. Two frameworks applicable: PRIs (Program Related Investments) with charities. Regular Investing. CRA Off-the Record Policy Consultation (2008)")

64

Envisioning Canada’s Social Finance Marketplace

NONPROFITS: Accessing social finance for financially self-sustaining & asset building enterprises tackling social & environmental needs (e.g. economic opportunity for disadvantaged populations, homecare infrastructure, disability agenda/RDSP, market shifting, community-based renewal energy, etc.) MAINSTREAM CAPITAL: Offering range of RDSPs, “Community Venture Funds”, “Green Venture Funds”, “Local Employment Venture Funds”, “Conservation Economy Investment Funds”, “Social Housing”, etc. GOVERNMENT: Providing enabling policy (Municipal, Provincial & Federal) Special tax credits for social enterprise investing, enabling private capital. Income at lowered tax rate, or receive refundable tax credit. Regulatory changes to simplify how charities and non-profits can directly operate or control social enterprises in the new hybrid space. Capacity building support for the evolving non-profit sector through dedicated funding mechanisms targeting key constituencies and social policy goals (e.g. for business plan development of social sector social enterprises, for technical training for financial and business managers in the emerging social-business hybrid sector, etc.) INVESTING PUBLIC: Expanding ownership of “social finance” asset class products in addition to equities and fixed income securities USER PUBLIC: Benefiting from emergence of innovative new systems of delivery and support for public benefit services and sustainability services.

MAINSTREAM CAPITAL: Offering range of RDSPs, Community Venture Funds , Green Venture Funds , Local Employment Venture Funds , Conservation Economy Investment Funds , Social Housing , etc. GOVERNMENT: Providing enabling policy (Municipal, Provincial & Federal) Special tax credits for social enterprise investing, enabling private capital. Income at lowered tax rate, or receive refundable tax credit. Regulatory changes to simplify how charities and non-profits can directly operate or control social enterprises in the new hybrid space. Capacity building support for the evolving non-profit sector through dedicated funding mechanisms targeting key constituencies and social policy goals (e.g. for business plan development of social sector social enterprises, for technical training for financial and business managers in the emerging social-business hybrid sector, etc.) INVESTING PUBLIC: Expanding ownership of social finance asset class products in addition to equities and fixed income securities. USER PUBLIC: Benefiting from emergence of innovative new systems of delivery and support for public benefit services and sustainability services.")

65

Social Finance Poised To Grow Quickly Since…

Canada can borrow proven models from US and UK We can make the transition to a robust social finance marketplace with: - New conversation among finance, government, foundations and nonprofits about the potential to scale up innovative social enterprise and social finance - New capital market instruments involving the range of financial institutions: banks, credit unions, pension funds, mutual funds, etc. - Public policy that a) creates incentives for capital to expand into social finance, b) borrows international best practices in charity regulations that enable foundations and nonprofits to operate successfully in the growing hybrid space - Strengthening the capacity of nonprofits, their social enterprises, and intermediary institutions

creates incentives for capital to expand into social finance, b) borrows international best practices in charity regulations that enable foundations and nonprofits to operate successfully in the growing hybrid space. - Strengthening the capacity of nonprofits, their social enterprises, and intermediary institutions.")

66

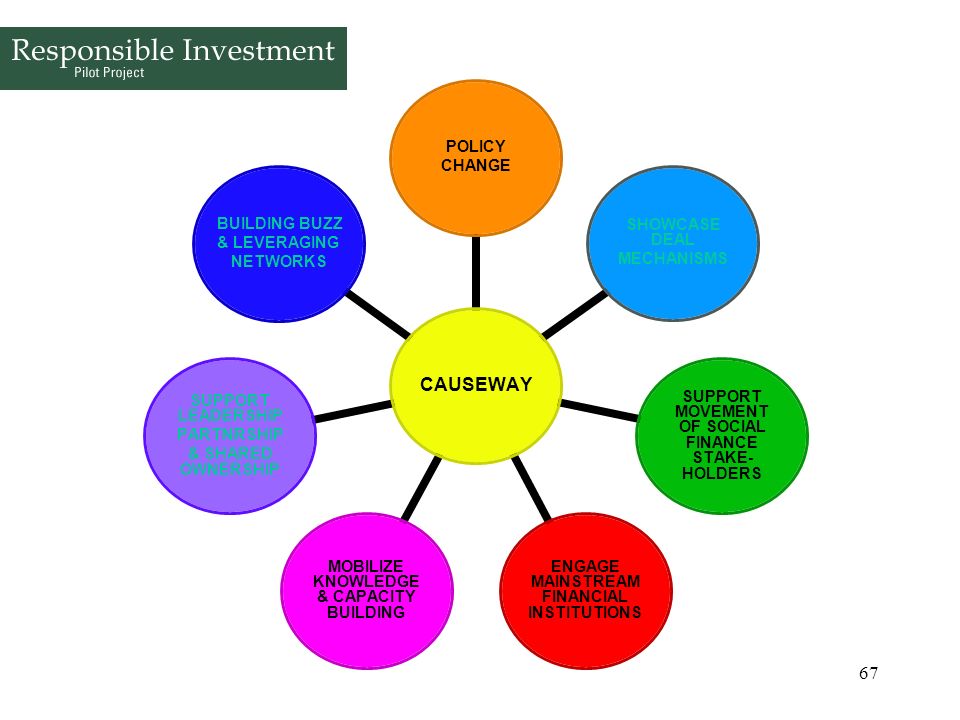

Causeway New national collaboration accelerating a social finance market place for financing social innovation serving public benefit

68

For more information about CAUSEWAY http://causeway-sff. wikispaces

For more information about CAUSEWAY and Social Finance visit: For more information on the charity sector visit:

69

Community Investing in Practice:

A Vancity Case Study

70

Role of Community Investing at Vancity Community Foundation

Community investing as part of our objectives since inception Our bylaws refer to “investments which are prudent” rather than those “in which trustees are authorized by law to invest” Part of strategy for using all our assets toward mission Fit with Vancity Credit Union as a key partner and with existing capacity CI increasingly a fit with donors and other partners (and growing demand from community organizations)

")

71

CI at Vancity Community Foundation

A range of different transactions, including individual micro-credit loans, social enterprise, arts, social housing, asset building for non-profits, bridge loans, etc. Fits within CRA guidelines as Program Related Investment (especially with respect charities), or as part of overall investment strategy Most often done as part of a much larger financial package, leveraged as high as 10:1

, or as part of overall investment strategy. Most often done as part of a much larger financial package, leveraged as high as 10:1.")

72

CI at Vancity Community Foundation

During some down market cycles, the community investment holdings have been the strongest part of our portfolio Still working on articulating an effective framework for measuring non-financial returns

73

CI at Vancity Capital Corporation

Significant amount of community investing experience through Vancity Capital Corporation (venture capital subsidiary of Vancity Credit Union) More than $15MM, 50 transactions and sizes, $25K to $1.5MM, areas including education, arts, employment training, housing, transportation, natural resource management, social services, health, sports, food, alternative energy, aboriginal communities, etc.

More than $15MM, 50 transactions and sizes, $25K to $1.5MM, areas including education, arts, employment training, housing, transportation, natural resource management, social services, health, sports, food, alternative energy, aboriginal communities, etc.")

74

CI at Vancity Capital Corporation

Losses less than 2%, including some additional risk mitigation in place from Federal Government, average returns of 10% (before operating cost allocations) – return on assets somewhere between 6% - 12% depending on leverage and allocation assumptions in model Non-profit organization represent 15% of the overall portfolio at Vancity Capital, as high as 25% when including sustainability businesses

– return on assets somewhere between 6% - 12% depending on leverage and allocation assumptions in model. Non-profit organization represent 15% of the overall portfolio at Vancity Capital, as high as 25% when including sustainability businesses.")

75

Lessons learned in CI It starts with a willingness to engage in this activity (some tolerance for risk taking and a view to how this fits the mandate of the organization) – often learning by doing and seeing value in lessons Need to set boundaries and objectives for this (often in policy, or a shared understanding Balance the need for structure and boundaries with flexibility (often through processes – using committees or individuals with delegated authority or using the entire Board within tolerances for risk and based on investment size

– often learning by doing and seeing value in lessons. Need to set boundaries and objectives for this (often in policy, or a shared understanding. Balance the need for structure and boundaries with flexibility (often through processes – using committees or individuals with delegated authority or using the entire Board within tolerances for risk and based on investment size.")

76

Lessons Learned in CI Capacity is a key challenge (both the capacity of your organization to structure transactions and lend, and the capacity of investees to effectively use repayable capital) Relationships are key. It often comes down to trust, and community investments often emerge from existing relationships within organizations Investment partners help to spread risk and can complement the due diligence process Additional risk mitigation tools or “credit enhancements” can be useful (additional loss reserves, risk sharing agreements, rate buy downs, insurance, priority agreements, etc…)

Relationships are key. It often comes down to trust, and community investments often emerge from existing relationships within organizations. Investment partners help to spread risk and can complement the due diligence process. Additional risk mitigation tools or credit enhancements can be useful (additional loss reserves, risk sharing agreements, rate buy downs, insurance, priority agreements, etc…)")

77

Lessons Learned in CI A portfolio approach helps ensure broader blended returns and helps avoid concentration risk with too few transactions in too few sectors A long time frame is important, together with a set of financial and non-financial objectives (including appropriate milestones for development) To achieve scale, it will likely be necessary to seek intermediaries with specific expertise and to package transactions for multiple investors

To achieve scale, it will likely be necessary to seek intermediaries with specific expertise and to package transactions for multiple investors.")

78

Developing A Responsible Investment Policy

IV Developing A Responsible Investment Policy

79

The Policy Development Roadmap

“Should a foundation be more than a private investment company that uses some of its excess cash flow for charitable purposes?” F.B Heron Foundation Board of Directors Yes – but how 79

80

The Policy Development Roadmap

“We want to implement responsible investment…now what?” initiate discussion at board level set policy objectives develop policy and integrate identify implementation strategy 80

81

The Policy Development Roadmap

Initiate Discussion at Board Level Identify the informational needs for your board. (i.e. How does RI affect returns? Are other foundations implementing RI strategies) Identify and participate in educational opportunities Identify mentors and/or other external experts Build your RI team to include staff, board and investment committee members The role of the investment committee is critical – need to understand their perspectives and constraints and they need to be involved throughout the process 81

Identify and participate in educational opportunities. Identify mentors and/or other external experts. Build your RI team to include staff, board and investment committee members. The role of the investment committee is critical – need to understand their perspectives and constraints and they need to be involved throughout the process. 81.")

82

The Policy Development Roadmap

Set Policy Objectives What does responsible investment mean for your foundation? What are the key triggers that led your organization to consider responsible investment? How can a responsible investment policy be grounded within the values and mission of the foundation? Survey stakeholders to better understand priorities in order to reflect these in the responsible investment policy How does responsible investment fit within your existing program priorities and activities? 82

83

The Policy Development Roadmap

Develop Policy and Integrate Start with an overarching policy statement or philosophy Look at sample and model policies to act as a guide How does responsible investment fit within your existing investment strategies? (i.e. asset allocation strategy, performance guidelines, investment manager review criteria) Talk to your investment managers and ask them questions about responsible investment Integrate responsible investment principals into your investment policies or guidelines 83

Talk to your investment managers and ask them questions about responsible investment. Integrate responsible investment principals into your investment policies or guidelines. 83.")

84

The Policy Development Roadmap

Identify Implementation Strategy Choosing your pathway Identify the strategies that make the most sense and meet the priorities and objectives you have laid out Incremental approaches allow decision-makers to educate themselves about each strategy, consider their value and monitor the results over time Pathways could include entering the market opportunistically or allocating a certain portion of the endowment for RI strategies Some organizations start with proxy voting because it works with their existing portfolio EVERY STEP COUNTS! 84

85

Why Responsible Investment

The Atkinson Foundation: A Case Study Why Responsible Investment MISSION …to promote social and economic justice in the tradition of Joseph E. Atkinson. INVESTMENT PHILOSOPHY The Foundation believes that it should implement its mission not only through the ideas people, organizations and projects it supports, but also by how it invests and otherwise uses its assets. Ensuring that its deeds match its words, the Foundation seeks to ensure that its grant making and investment practices all align with its mission. Foundation founded in 1942 by Joseph Atkinson Funding themes: Early childhood education and economic justice. Asset size – approximately $60 million 85

86

The Atkinson Foundation

Overcoming Hesitancy KEY CATALYSTS Champions at the staff, board and investment committee level Broad ‘theoretical’ support for the need to align grant-making and investing with mission KEY STEPS Building the collective knowledge of the Board Asking questions…over and over again Identifying and working with mentors Utilizing grant capital to foster a greater understanding of RI and MBI And finally…developing the policy 86

87

The Atkinson Foundation

Mission Based Investment Policy The Foundation is committed to its fiduciary responsibilities and recognizes that this responsibility does not end with maximizing return and minimizing risks. The Foundation believes its fiduciary responsibility includes the consideration of its investment decisions on corporate conduct, and broader social concerns. The Foundation will pursue MBI with the following assumptions in mind: Evidence demonstrates that MBI does not have to have a negative effect on financial returns; There are no perfect companies; and MBI can positively influence corporate conduct, improve stakeholder relations and ultimately maximize profits. 87

88

The Atkinson Foundation

Mission Based Investment Policy cont’d The Foundation will work with its fund managers to develop positive and negative screens, and to be an active shareholder. The Foundation will further its mission through investments that: Promote high quality, fair and just employment opportunities; Support young children and their caregivers; Reduce poverty and improve quality of life for the poor; Support such other granting themes as the Foundation may determine from time to time. The Foundation favours companies that support and advocate for a strong and effective public sector. 88

89

The Atkinson Foundation

Implementation…With Some Help from Friends Portfolio audit conducted by Jantzi Research Associates ACF holdings moved to a segregated fund to allow the Foundation to direct proxy voting and shareholder engagement activities A set of customized proxy voting guidelines were developed with support of SHARE Moira Hutchinson joined the investment committee in 2006 The Foundation hired SHARE to facilitate a shareholder engagement program focusing on precarious employment practices 89

90

The Atkinson Foundation

Identifying a Focus Decided to focus their efforts initially on shareholder engagement for two main reasons: FIRST, the investment committee was comfortable with shareholder engagement as an initial strategy SECOND, they felt that shareholder engagement could be a complimentary strategy to the efforts of grassroots organizations that they were providing grants to Developed a shareholder engagement program focused on precarious employment practices in the commercial real estate sector 90

91

The Atkinson Foundation

Time for Action – Shareholder Engagement Strategy Engagement dialogues underway with two publicly traded companies Management meetings with companies to get more information on contracting practices Multi-stakeholder roundtable to consider the merit of devising a labour code of conduct or policy Working Group drafting a model labour code of conduct for the commercial property sector in Canada Research commissioned that will examine the business case for good labour practices in commercial property management 91

92

The Atkinson Foundation

A Small Fund Leveraging Big Change Connecting RI strategy to the work of grantees Successfully brought together some of Canada’s largest asset owners and commercial real estate investors to look at the issue of precarious employment practices in commercial properties Initiating research that will draw on North American case studies that investors internationally will have access to Principal catalyst in the creation of a model labour code of conduct outlining employment and contracting standards for the commercial real estate sector in Canada 92

93

The Atkinson Foundation

Key Lessons…so far This takes time – moving from the theoretical to the practical proved to take several years in the realm of RI Working with the investment committee from the beginning is crucial and empathizing with their apprehensions There are many paths – need to find strategies that meet your foundations needs and work at a pace that decision-makers are comfortable with Small funds can make a difference Change is slow but every step counts “We are not done yet” 93

94

V Bibliography

95

Bibliography Michael Jantzi, Responsible Investing for Foundations – An Introduction, June 5/08 Bob Walker, Shareholder Action, June 5/08 Tim Draimin, Foundations’ Financial Innovation and Community Investing, June 5/08 Derek Gent, Community Investing: A Practitioners Perspective, June 5/08 Peter Chapman and Shannon Rohan, Responsible Investment Policy Development, June 5/08 GEM, Sustainable Investing Handbook for Mission-Based Organizations, June 2008.

Similar presentations

![[Imagine School at North Port] Oral Exit Report Quality Assurance Review Team School Accreditation.](/1/271987/big_thumb.jpg "[Imagine School at North Port] Oral Exit Report Quality Assurance Review Team School Accreditation.>")

Survey commissioned by the European Parliament and co-ordinated by Directorate-General for Communication.>")

Grants Chapter 6.>")