Download presentation

Presentation is loading. Please wait.

1

INLAND REVENUE AUTHORITY OF SINGAPORE

3

COURSE MATERIAL Q&A question slip GST General Guide for Traders

How do I keep Records and Accounts How do I prepare my GST Return? Lecture Notes on GST Class GST Class Feedback Form Slip on IRAS Homepage

4

CONTENTS Overview Of GST System How GST works Concepts Of GST

Scope Of Tax Exports Tax Invoice Purchases Obligations GST F5 & F7 Slide 2 - How GST works - GST concepts - Responsibilities of a GST registered trader - Exports - Purchases and Imports - Record keeping - Obligations - How to complete the GST return

5

CONTENTS Common Misconceptions Application Exercise

Penalties & Recovery Actions Q & A session Feedback Slide 3 - Change of business circumstances - Common misconceptions - Common errors - Application exercise - Q & A session - Feedback

6

OVERVIEW OF GST SYSTEM What is GST? - tax on domestic consumption

- paid whenever customers buy goods or services from GST registered businesses - charged and accounted for at a rate of 7% (with effect from 1 July 2007)

")

7

OVERVIEW OF GST SYSTEM Are All Goods And Services Taxable?

- All Goods and Services within the GST System are taxable except those which have been specifically exempted by the Act - Main exempt items are financial services and the sale or lease of residential properties

8

OVERVIEW OF GST SYSTEM Who Collects GST?

- For supply of goods or services in Singapore, GST is collected by traders like you who have registered with the Comptroller of GST - For importation of goods, GST is collected by the Singapore Customs at the point of importation

9

HOW GST WORKS Basic GST Process (Output Tax) GST collected

from customers Slide 6 When you take the GST that you collected (that is the Output Tax) minus the GST you have paid (the Input Tax), you arrived at the Net GST amount.

minus the GST you have paid (the Input Tax), you arrived at the Net GST amount.")

10

HOW GST WORKS Basic GST Process (Output Tax) (Input Tax)

GST collected less GST paid on from customers business purchases Slide 6 When you take the GST that you collected (that is the Output Tax) minus the GST you have paid (the Input Tax), you arrived at the Net GST amount.

minus the GST you have paid (the Input Tax), you arrived at the Net GST amount.")

11

HOW GST WORKS Basic GST Process (Output Tax) (Input Tax)

GST collected less GST paid on from customers business purchases equals Net GST Slide 6 When you take the GST that you collected (that is the Output Tax) minus the GST you have paid (the Input Tax), you arrived at the Net GST amount.

minus the GST you have paid (the Input Tax), you arrived at the Net GST amount.")

12

HOW GST WORKS + - Basic GST Process Net GST Payable to Refundable from

+ - Payable to Refundable from Comptroller Comptroller Slide 7 If this Net GST amount is a positive figure (meaning that the GST you collected is greater than the GST you have paid out), then the amount is payable to the Comptroller of GST. On the other hand, if the Net GST amount is a negative figure (meaning that the GST you have paid is greater than the GST you have collected, then the Net GST amount is refundable to you from the Comptroller.

, then the amount is payable to the Comptroller of GST. On the other hand, if the Net GST amount is a negative figure (meaning that the GST you have paid is greater than the GST you have collected, then the Net GST amount is refundable to you from the Comptroller.")

13

HOW GST WORKS SELLING PRICE GST Payable

Import Value = $ 5,000 GST paid on import = $350 Manufacturer’s Price = $10, Manufacturer GST Collected = $700 GST Amount = $ Less: GST Paid = $350 Selling Price = $10,700 GST Payable = $350 Retailer’s Price = $20,000 GST Collected = $1,400 GST Amount = $ 1, Retailer Less: GST Paid = $ 700 Selling Price = $21, GST Payable = $ 700 Consumer pays = $21,400 Total GST Paid = $1,400 Consumer Slide 8

14

CONCEPTS OF GST Scope of Tax Types of Supply

When Should You Account for GST? What Is the Value of Supply That Is Subject to GST? Slide 9 - the scope of tax - what transactions attract GST - when to account for GST - what is the amount that is subjected to GST

15

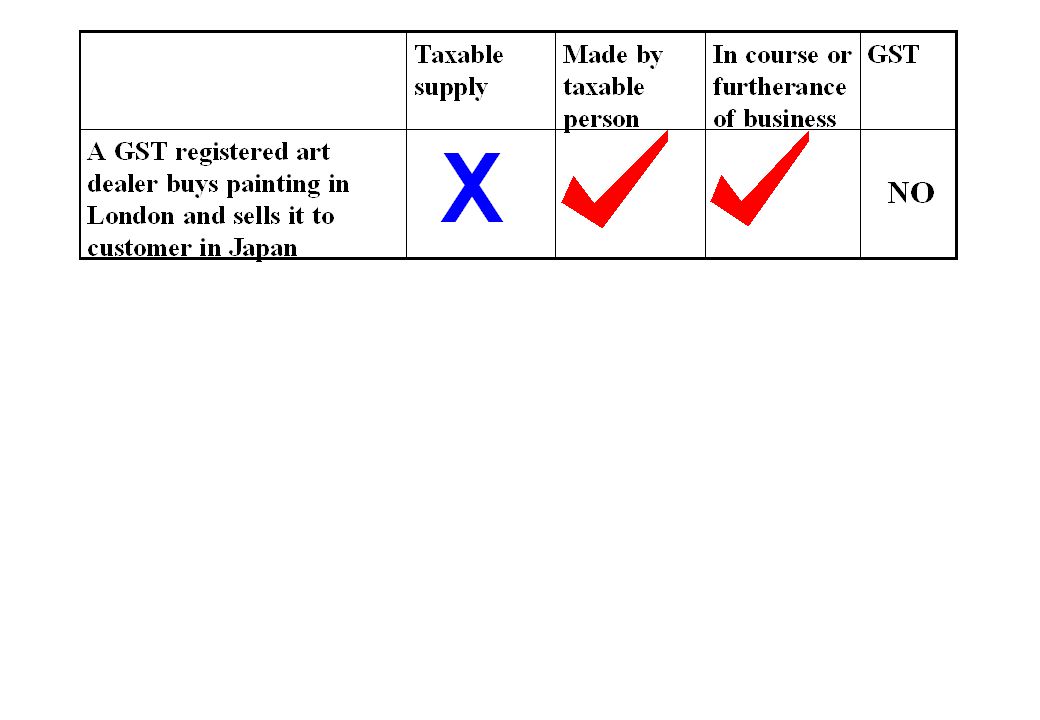

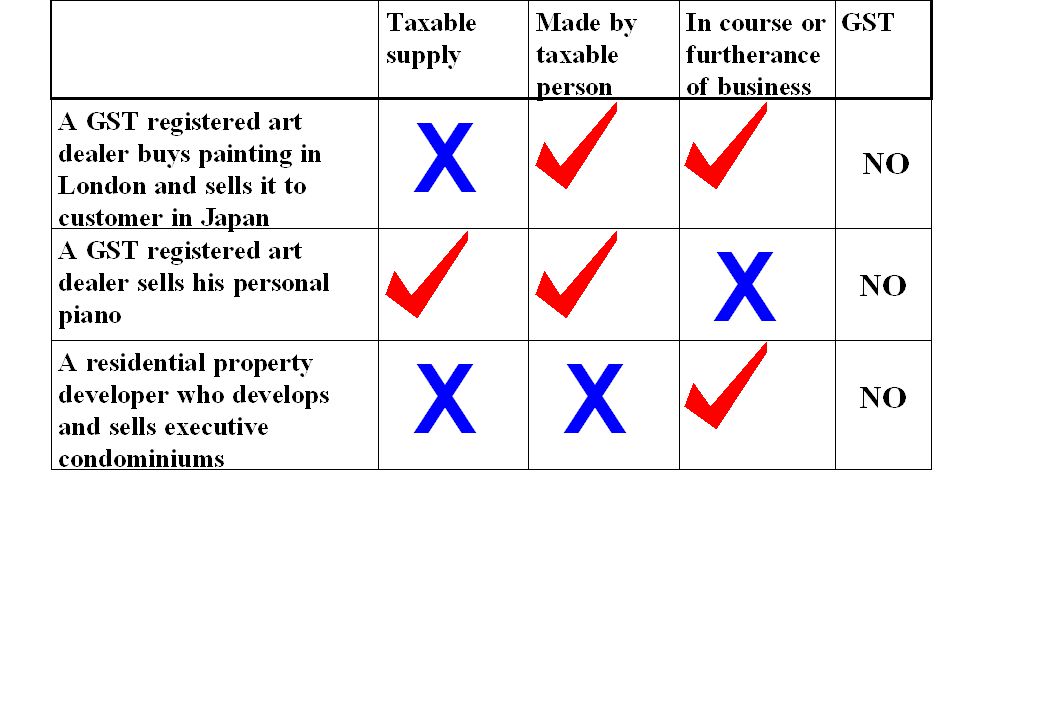

SCOPE OF TAX Section 8 of GST Act

GST will be charged on any supply of goods or services if it is : i) made in Singapore ii) a taxable supply iii) made by taxable person iv) in the course or furtherance of business

made in Singapore. ii) a taxable supply. iii) made by taxable person. iv) in the course or furtherance of business.")

16

SCOPE OF TAX Supply includes all forms of supply done for a consideration. Slide 11 What is supply? Supply includes all forms of supply done for a consideration. Forms of supply can be either goods or services

17

SCOPE OF TAX MADE IN SINGAPORE? PLACE OF SUPPLY

Goods are supplied in Singapore if goods are in Singapore or from Singapore Services are supplied in Singapore if supplier belongs in Singapore

18

SCOPE OF TAX TAXABLE SUPPLY - A supply of goods or services made in

Singapore other than an exempt supply - Consist of standard-rated and zero- rated supplies

19

SCOPE OF TAX Taxable Person - A person that is GST-registered or

is required to be registered for GST under the Act

20

TYPES OF SUPPLY Non-Taxable Taxable Out-of-Scope Exempt Slide 12

What transactions attract GST? To answer this, we need to look at the various types of supplies. We can categorise the supplies into 2 groups, that is the non-taxable and the taxable supply. As the name suggests, non-taxable supplies are supplies which do not attract GST. This category can be sub-divided into out-of-scope and exempt supplies.

21

TYPES OF SUPPLY Non-Taxable Taxable Out-of-Scope Exempt

Zero-rated (0%) Slide 13 Taxable supply refers to supplies which attract GST. This would include standard rated supply and zero-rated supply. Standard-rated (7%)

Slide 13. Taxable supply refers to supplies which attract GST. This would include standard rated supply and zero-rated supply. Standard-rated (7%)")

22

NON-TAXABLE SUPPLY Out -of-scope Supply Private Transactions

Third Country Sales (Sales outside Singapore) Exempt Supply Sale and Lease of Residential Properties Financial Services

Exempt Supply. Sale and Lease of Residential Properties. Financial Services.")

23

without coming into S’pore

Goods are shipped from China to U.S.A. without coming into S’pore Supply is out-of-scope

24

TAXABLE SUPPLY Zero-rated Supply (0% GST) Export of Goods

International Services Standard-rated Supply (7% GST) All Others Eg: Sale of Fixed Assets

All Others. Eg: Sale of Fixed Assets.")

25

TAXABLE SUPPLY SALE OF FIXED ASSETS

GST must be charged on the sale of Fixed Assets Eg : Non residential properties, furniture, computers, etc GST to be accounted on Selling Price of Asset

26

TAXABLE SUPPLY GST is a transaction based tax

Need to review all transactions including those not in the normal course of business I would like to stress here that GST is a transaction based tax. Thus, you will need to review your transactions to see if it amounts to a taxable supply. And whether GST needs to be charged accordingly. If you notice here, there is a special treatment on gifts. Let us now take a look at when to account for output tax on gifts.

31

WHEN SHOULD YOU ACCOUNT FOR GST?

GOODS Time of Supply for Goods Goods are removed or made available; Tax invoice issued; or Payment received whichever is the earliest Subject to 14-day rule

32

WHEN SHOULD YOU ACCOUNT FOR GST?

14-day Rule Tax invoice issued within 14 days when the goods are removed Time of supply is the tax invoice date, provided payment is not made yet

33

WHEN SHOULD YOU ACCOUNT FOR GST?

14-day Rule Total value of supply - $11,000 Invoice for payment Goods Invoice for Balance received $5, Removed Amount $11, ($11,000 - $5,000) 01/03/ /03/ /04/07 Time of supply : ?

01/03/07 31/03/07 14/04/07. Time of supply :")

34

WHEN SHOULD YOU ACCOUNT FOR GST?

14-day Rule Total value of supply - $11,000 Invoice for payment Goods Invoice for Balance received $5, Removed Amount $11, ($11,000 - $5,000) 01/03/ /03/ /04/07 Time of supply : 01/03/07 ($5,000) 14/04/07 ($6,000)

01/03/07 31/03/07 14/04/07. Time of supply : 01/03/07 ($5,000) 14/04/07 ($6,000)")

35

WHEN SHOULD YOU ACCOUNT FOR GST?

SERVICES Time of Supply for Services Services are completed; Tax invoice issued; or Payment received whichever is the earliest Subject to 14-day rule

36

WHEN SHOULD YOU ACCOUNT FOR GST?

14-day Rule Tax invoice issued within 14 days when the services are completed Time of supply is tax invoice date, provided payment is not made yet

37

WHAT IS THE VALUE OF SUPPLY THAT IS SUBJECT TO GST?

Consideration in money Value + GST = Consideration Eg: $100 (Value) + $7 (GST) = $107

+ $7 (GST) = $107.")

38

WHAT IS THE VALUE OF SUPPLY THAT IS SUBJECT TO GST?

Consideration not in money Value of supply = open market value Trade/cash discount given Value of supply = discounted price

39

WHAT IS THE VALUE OF SUPPLY THAT IS SUBJECT TO GST?

Transactions with related parties Value of supply = open market value Eg: Co. X, a GST-registered business, sold the company’s furniture (market value $5,000) to one of its directors at $800. Value of supply should be $5,000.

to one of its directors at $800. Value of supply should be $5,000.")

40

WHAT IS THE VALUE OF SUPPLY THAT IS SUBJECT TO GST?

Goods for private use Eg: Mr Y, a renovation contractor who is GST registered, uses business goods such as marble tiles for his own home If the cost of materials is $10,000, GST = $10,000 x 7% = $700

41

EXPORTS Supporting export documents : Zero-rated

Evidence of exports required Supporting export documents : Bill of Lading , Airway Bill IESGP permit (previously known as TDB permit). Please note that permit must be taken before the export of goods, otherwise, the Comptroller may not accept it as evidence EXPORTS are zero-rated ss. You nd to maintain export documents as evidence of exports. Examples of such documents include the following: READ SLIDE…

. Please note that permit. must be taken before the export of goods, otherwise, the Comptroller may not. accept it as evidence. EXPORTS are zero-rated ss. You nd to maintain export documents as evidence of exports. Examples of such documents include the following: READ SLIDE…")

42

EXPORTS Supporting export documents : invoice to overseas customer

purchase order insurance documents packing list or delivery note addressed to overseas customer evidence of payment received READ SLIDE IMPT: In the event if you are unable to satisfy the Comptroller, by way of documentary evidence that you’ve exported the goods you’ve to std-rate the ss and charge GST accordingly.

43

TAX INVOICE Importance of Tax Invoice When to issue a Tax Invoice?

When not to issue a Tax Invoice? Contents of a Tax Invoice Simplified Tax Invoice READ SLIDE

44

IMPORTANCE OF TAX INVOICE

primary document for input tax claim documentary evidence that GST has been charged on the standard-rated supply For purchases, the tax invoice is a primary document for GST purpose to support input tax claims. Tax Invoice is an impt documentary evidence that GST has been charged on the std-rated ss.

45

WHEN TO ISSUE A TAX INVOICE?

must be issued if making a standard-rated supply to a taxable person within 30 days after time of supply So, When do you issue a tax invoice? Tax Invoice must be issued when you make a std-rated ss. It applies to all std-rated supplies including sale of fixed assets and not just for your normal sales. Tax invoice has to be issued within 30 days from the time of ss.

46

WHEN NOT TO ISSUE A TAX INVOICE?

No need to issue tax invoices for: zero-rated supplies exempt supplies deemed supplies READ SLIDE Deemed Supplies An example of deem ss is free gift where the cost of gift is more than $200 or 3 gifts or more are given to the same person within a period of 3 mths. Note: Although tax invoices need not be issued, you are still required to issue normal commercial invoices, where appropriate.

47

CONTENTS OF A TAX INVOICE

Tax invoice must show : an identifying number invoice date your customer’s name (or trading name) and address description of the goods and services your name, address and GST registration number READ SLIDE

and address. description of the goods and services. your name, address and GST registration number. READ SLIDE.")

48

CONTENTS OF A TAX INVOICE

the words “tax invoice” total amount payable excluding tax, the rate of GST and the total tax chargeable shown separately total amount payable, including tax breakdown of exempt, zero-rated or other supply, stating separately the gross amount payable in respect of each READ SLIDE Where tax invoice is issued in foreign currency, it must be converted to Sing dollars using the prevailing exchange rate when the supply takes place.

49

SIMPLIFIED TAX INVOICE

When to Issue? amount payable including tax <$1,000 only for standard-rated supplies Particulars name, address and registration number date of issue description of the goods or services total amount payable including GST the words “Price Payable inclusive of GST” READ SLIDE For non-GST registered customers, you can just issue receipts instead of tax invoices.

50

PURCHASES Claiming of input tax Imports Disallowed Input Tax Claims

Conditions for Pre-registration Input Tax Claims READ SLIDE

51

CLAIMING OF INPUT TAX Tax Invoice

Evidence for claiming GST incurred on business purchases Tax invoice addressed to business name ABC Co. Con’t As mentioned earlier, tax invoices acts as the evidence for making I/p tax claims You’re only allowed to claim GST based on tax invoices that are addressed to your biz name. LET ME SHOW YOU SOME CASES WHERE TRADERS HAVE MADE WRONGFUL CLAIMS

52

CLAIMING OF INPUT TAX Case 1 : Lack of Evidence

Tax invoice issued to another person Co. claimed input tax based on tax invoices issued to their related company The input tax was for purchases made by the related co. Input tax claims were disallowed Here, we’ve a case of “Lack of Evidence” Tax invoice is issued to another person (for eg, a related co.) The GST-registered trader claimed i/p tax based on the tax invoice issued to their related co. The i/p tax was for purchases made by the related co. Thus, this i/p tax is disallowed.

The GST-registered trader claimed i/p tax based on the tax invoice issued to their related co. The i/p tax was for purchases made by the related co. Thus, this i/p tax is disallowed.")

53

CLAIMING OF INPUT TAX Case 2 : Private Expenditure

holds valid tax invoices GST trader made claims on redevelopment of residential property expenditure is of a private nature input tax claims were disallowed and trader was compounded Next, we’ve a case where the trader claims GST on private expenditure Trader holds a valid tax invoice But GST is incurred on expenses on the redevelopment of his own residential property Expenditure is of a private nature. Therefore, i/p tax is disallowed and trader was compounded.

54

IMPORTS Importer - Person who is entitled to claim GST paid on imports

GST payment permit - Evidence to support input tax claims We’ll now look at “IMPORTS” The importer will be the one who is able to claim for GST paid upon the importation of gds The GST payment permit or the Cargo Clearance Permit must be maintained as evidence of claims. Further, you will also need to keep other doc like invoice from the overseas suppliers and shipping doc. In order to claim i/p tax, the permit must bear your name as the importer and the gds are imported for your biz purpose.

55

DISALLOWED INPUT TAX CLAIMS (REG 26 & 27)

a) Club Subscription Fee b) Medical and Accident Insurance Premium c) Medical Expenses d) Family Benefits e) Cost and Running Expenses of Motor Cars

Club Subscription Fee. b) Medical and Accident Insurance Premium. c) Medical Expenses. d) Family Benefits. e) Cost and Running Expenses of Motor Cars.")

56

CONDITIONS FOR PRE-REGISTRATION INPUT TAX CLAIMS

GOODS : Goods supplied to or imported by taxable person NOT supplied or consumed before date of registration Proper stock account is maintained If you incur i/p tax claims prior to your effective date of registration, you must write in to the Comptroller of GST for approval before making the claims. The Conditions for pre-registration claims on Goods are: READ SLIDE

57

PRE-REGISTRATION CLAIMS

GST registration date : 01/06/07 Expenses Incurred : Invoice Date Description Amount Claimable? i) 01/04/ Purchase of stocks $1, Yes ii) 30/04/07 Utilities charges $ No iii)15/05/07 Office rental $2, No iv)01/05/07 Imports which $ No are sold on 31/05/07

01/04/07 Purchase of stocks $1,000 Yes. ii) 30/04/07 Utilities charges $300 No. iii)15/05/07 Office rental $2,500 No. iv)01/05/07 Imports which $900 No. are sold on 31/05/07.")

58

CONDITIONS FOR PRE-REGISTRATION INPUT TAX CLAIMS

SERVICES : Services provided to taxable person NOT related to goods supplied or consumed before date of registration NOT supplied to taxable person more than 6 months before date of registration NOT provided by taxable person before date of registration Conditions for pre-registration claim on SERVICES received prior to the effective date of registration are:

59

PRE-REGISTRATION CLAIMS

GST registration date : 01/06/07 Expenses Incurred : Invoice Date Description Amount Claimable? i) 01/11/06 Management fee $1, No ii) 30/04/07 Consultancy fee $2, Yes iii) 01/04/07 Commission fee $ No for goods sold on 01/05/07

01/11/06 Management fee $1,000 No. ii) 30/04/07 Consultancy fee $2,000 Yes. iii) 01/04/07 Commission fee $ 500 No for goods sold on. 01/05/07.")

60

BAD DEBT RELIEF Entitled to claim Bad Debt Relief if you satisfy conditions under Reg. 83 A “Self-Review of Eligibility to claim Bad Debt Relief” Form available from website If you satisfy conditions, claim in Box 7 of current GST return No need to write in for approval

61

GST Integrated Phone Service

Want to check whether we have received your GST return? Request for Statement of account? JUST CALL (24-hour automated voice response system) for all these and more ...

for all these and more ...")

62

BREAK I’ve now come to the end of the first part of the presentation.

You may go for a 15 mins break & pls be seated by __________. If you’ve any query, pls write them down on the paper provided and drop them into the box outside the audi when you go for your break. If you wish to go to the restrooms, you may turn right after leaving the door. If you want a drink, you may take the lift to the Café at 2nd level. Thank you.

63

Download GST forms and handbooks Find guides on GST form filling!

Do you know you can access GST information at IRAS homepage? Come visit us (click ‘Information on Goods & Services Tax’) You can ... Download GST forms and handbooks Find guides on GST form filling! Slide 2 - How GST works - GST concepts - Responsibilities of a GST registered trader - Exports - Purchases and Imports - Record keeping - Obligations - How to complete the GST return

You can ... Download GST forms and handbooks. Find guides on GST form filling! Slide 2. - How GST works. - GST concepts. - Responsibilities of a GST registered trader. - Exports. - Purchases and Imports. - Record keeping. - Obligations. - How to complete the GST return.")

64

CONTENTS Obligations GST F5 & F7 Common Misconceptions

Application Exercise Slide 3 - Change of business circumstances - Common misconceptions - Common errors - Application exercise - Q & A session - Feedback

65

OBLIGATIONS Record Keeping Filing Of GST F5 Payment Of Tax

Registration Change Of Business Circumstances GST - Inclusive Price

66

RECORD KEEPING What Records To Keep? Business and accounting records

Tax invoices and receipts issued/received Credit notes and debit notes Business contract and agreement

67

RECORD KEEPING What Records To Keep? Tourist refund claim forms

Import and export documents (e.g. permit, bill of lading, airway bill) Other documents supporting change in consideration

Other documents supporting. change in consideration.")

68

RECORD KEEPING Examples of Business and Accounting Records:

General Ledgers Debtors and Creditors Ledgers Purchase Orders and Delivery Notes Purchase and Sales Books Cash Books and other account books Records of daily takings

69

RECORD KEEPING Stock records Bank Statements and Pay-in Slips

Relevant Business Correspondences GST Accounts Annual Account (e.g. balance sheet, profit & loss statement) Any other documents and records GST guide on ‘How do I keep records and accounts’

Any other documents and records. GST guide on ‘How do I keep records and accounts’")

70

RECORD KEEPING Business goods put to non-business use

Other Records Business goods put to non-business use Disposal of business assets Supplies of goods and services received Removal of goods from Customs-licensed warehouse

71

RECORD KEEPING How do you keep records and accounts?

no specific guidelines complete and up-to-date figures in GST Returns can be easily verified

72

RECORD KEEPING From 1 January 2007 Keep records for 7 years

Can start to keep only 5 years of records Records relating to accounting periods in 2007 and after Keep records for 7 years - Records relating to accounting periods ending before 2007

73

RECORD KEEPING Comptroller’s written approval not required to keep records in non-paper form IRAS circular on ‘Wavier of requirement to seek IRAS’ approval for keeping of records in Machine Sensible Form / Imaging System and Electronic Invoicing’. GST guides on ‘Keeping Machine Sensible Records & Electronic Invoicing’ and ‘Keeping of Records in Imaging Systems’

74

RECORD KEEPING Failure to keep records Guilty of an offence

fine < $5,000 and/or imprisonment <6 months 2nd or subsequent conviction fine < $10,000 and/or imprisonment < 3 years

75

FILING OF GST F5 FILING One GST F5 for One Prescribed Accounting Period YOU MUST NOT USE: Forms issued for Other Periods

76

FILING OF GST F5 DUE DATE within 1 month after the end of each accounting period Eg : Due date for period 01/10/06 to 31/12/06 is 31/01/2007

77

FILING OF GST F5 All Tax Returns Must Be Filed By Due Date

If No Trading Is Done, a ‘Nil’ Return Is Still Required.

78

FILING OF GST F5 FAILURE TO FILE RETURN OR MAKE INCOMPLETE RETURN:

An Offence Comptroller Can Assess Amount of Tax Due Notice of Assessment (Estimated) Will Be Sent to Trader

Will Be Sent to Trader.")

79

PAYMENT OF TAX DUE DATE MODES OF PAYMENT

within 1 month after end of each accounting period MODES OF PAYMENT Giro or Cheque Cross all cheques and make them payable to “Comptroller of Goods and Services Tax”

80

PAYMENT OF TAX If Net Amount Payable <$5, No Payment Is Required

If Net Amount Repayable <$5, No Refund Will Be Made The Amount Will Not Be Carried Forward

81

REGISTRATION Just A Reminder ... Compulsory Registration

Voluntary Registration - must remain registered for at least 2 years

82

Registration GST Certificate

With effect from 15 Sep 1999, we no longer issue GST registration certificate and you are not required to display at your business premises

83

Registration As a GST registered trader, you must print your GST registration number on your tax invoices, simplified tax invoices and serially printed receipts

84

If You Are Registered As A Sole-Proprietor

Registered for GST in your individual name Value of taxable supplies is the aggregate taxable turnover of all your sole-proprietorship businesses Charge GST on supplies made by all your sole-proprietorship businesses

85

If You Are Registered As A Sole-Proprietor

Qn: What if you set up another sole- proprietorship business in future, do you need to register this new business? Ans: No, because you, as the sole-proprietor, are already registered.

86

If You Are Registered As A Sole-Proprietor

You should use the same GST registration number to charge GST with effect from the date of commencement of new business What you must do: Send in ACRA instant information extract of the new business

87

If You Are Registered As A Partnership

Registration is in the name of the respective firms Value of taxable supplies is the aggregate taxable turnover of all partnerships having the same composition of partners

88

If You Are Registered As A Partnership

Charge GST on supplies made by all other partnerships with the same composition of partners Qn: What should you do if you set up another partnership business with the same composition of partners?

89

If You Are Registered As A Partnership

Ans: Send in ACRA instant information extract of the new business and GST F3 immediately. A separate GST registration number will be given for the new business. You are required to charge and account for GST from date of commencement of new business.

90

CHANGE OF BUSINESS CIRCUMSTANCES

Changes involve Business name and address Giro bank account number De-registration Transfer of business as a going concern So what does change of business circumstances mean? Over here, we have listed some of the changes and they include change of your business address and account numbers.

91

CHANGE OF BUSINESS CIRCUMSTANCES

Write in to inform Comptroller within 30 days Do not delay - Refund could be delayed - Transfer of Business, penalties may apply for late notification Please note that you will need to inform IRAS whenever there is a change of business circumstance. As advised here, you have to inform us promptly as your refund may be affected.

92

CEASE TO MAKE TAXABLE SUPPLIES

Notify Comptroller by submitting GST F9 (Application for Cancellation of GST) Within 30 days

Within 30 days.")

93

CEASE TO MAKE TAXABLE SUPPLIES

Once your application is approved, GST F8 (Final Goods and Services Tax Return) will be issued Need to account for deemed output tax - if value of your assets on hand including stock, fixed assets and non-residential properties (for which input tax has been allowed previously) exceeds $10,000

will be issued. Need to account for deemed output tax. - if value of your assets on hand including stock, fixed assets and non-residential properties (for which input tax has been allowed previously) exceeds $10,000.")

94

TRANSFER OF BUSINESS AS A GOING CONCERN

Eg: Business was converted from a partnership to a private limited Notify the Comptroller 30 days before the date of transfer

95

GST-INCLUSIVE PRICE Any price displays, advertisements, or quotations in respect of goods or services made to the public should be inclusive of GST Failure to comply with the GST-inclusive price display requirement is an offence -GST legislation requires that a GST-registered business to display, advertise, publish or quote price inclusive of GST. - It is an offence for failure to comply with the above - If your price displays have not been in compliance with the above, you should take immediate steps to rectify your price displays and ensure that they show GST-inclusive prices. - The diagram below is an eg. of GST-inclusive price tag. ABC Co. Pte Ltd $107.00

96

GST RETURNS How To Complete : 1. GST F5 2. GST F7

97

HOW TO COMPLETE GST F5 Include:

Box 1: Total value of standard-rated supplies (excluding GST Amount) Include: Sale of goods & services (generally local supplies) Sale of business assets Deposits received as part payment Supplies to staff

Include: Sale of goods & services (generally local supplies) Sale of business assets. Deposits received as part payment. Supplies to staff.")

98

HOW TO COMPLETE GST F5 (excluding GST Amount) Include:

Box 1: Total value of standard-rated supplies (excluding GST Amount) Include: Hire of goods to someone else Gift of goods costing > $200 Deduct: Credit note issued to customers Debit note received from customers

Include: Hire of goods to someone else. Gift of goods costing > $200. Deduct: Credit note issued to customers. Debit note received from customers.")

99

HOW TO COMPLETE GST F5 Box 2: Total value of zero-rated supplies

Include: Supplies of goods which are exported Supplies of international services

100

HOW TO COMPLETE GST F5 Box 3: Total value of exempt supplies Include:

Supplies of financial services (4th Schedule) Sale and lease of residential properties

Sale and lease of residential properties.")

101

HOW TO COMPLETE GST F5 Box 5: Total value of taxable purchases

(excluding GST Amount) Include: Standard-rated purchases Imports Zero-rated purchases (Egs: IDD calls, International Freight Charges, Air Tickets)

Include: Standard-rated purchases. Imports. Zero-rated purchases. (Egs: IDD calls, International Freight Charges, Air Tickets)")

102

HOW TO COMPLETE GST F5 ...cont’d (taxable purchases) Deduct:

Debit note issued to suppliers Credit note received from suppliers

103

HOW TO COMPLETE GST F5 * Not to enter for taxable purchases*

Wages & salaries Purchases for private use Purchases from non GST-registered suppliers

104

HOW TO COMPLETE GST F5 * Not to enter for taxable purchases *

Purchases and maintenance of motor cars Family benefits Employee medical & insurance expenses Club subscription & entrance fees

105

HOW TO COMPLETE GST F5 Box 7 (input tax) Includes:

allowable input tax incurred on your taxable purchases refund of GST to tourists bad-debt relief

106

HOW TO COMPLETE GST F5 Input tax errors Eg: Computational Errors

Double claiming of input tax A company used a spreadsheet program to prepare input tax claims The formula in the spreadsheet was wrong resulting in double claiming of input tax Another common error made by traders is double claiming of input tax. This may be made in the same accounting period or in another accounting period. In this instance, the trader had used a spreadsheet with a wrong formula, resulting in double claims of input tax. The error was rectified by the filing of an F7 to correct the errors.

107

HOW TO COMPLETE GST F5 Please note:

To drop off cents for Boxes 1 to 5 & 9 Declare figures in S$, not in foreign currencies All boxes must be completed

108

HOW TO COMPLETE GST F5 Example: ABC company has the following business transactions for one accounting period: 1) Imports - $20,000 2) Local sale - $10,000 3) Sale of fixed asset - $5,000 4) Local purchase - $8,000 5) Export sales - $50,000

Imports - $20,000. 2) Local sale - $10,000. 3) Sale of fixed asset - $5,000. 4) Local purchase - $8,000. 5) Export sales - $50,000.")

109

HOW TO COMPLETE GST F5 To which boxes do they belong ?

1) Imports - $20,000 (Box 5) 2) Local sale - $10,000 (Box 1) 3) Sale of fixed asset - $5,000 (Box 1) 4) Local purchase - $8,000 (Box 5) 5) Export sales - $50,000 (Box 2)

Imports - $20,000 (Box 5) 2) Local sale - $10,000 (Box 1) 3) Sale of fixed asset - $5,000 (Box 1) 4) Local purchase - $8,000 (Box 5) 5) Export sales - $50,000 (Box 2)")

110

HOW TO COMPLETE GST F5 What about Box 6 (output tax) and Box 7

(input tax) ? 1) Imports - $20,000 GST - $1,400 (Box 7) 2) Local sale - $10,000 GST - $700 (Box 6) 3) Fixed asset - $5,000 GST - $350 (Box 6) 4) Local purchases - $8,000 GST - $560 (Box 7) 5) Export sales - $50, GST charged at 0%

1) Imports - $20,000 GST - $1,400 (Box 7) 2) Local sale - $10,000 GST - $700 (Box 6) 3) Fixed asset - $5,000 GST - $350 (Box 6) 4) Local purchases - $8,000 GST - $560 (Box 7) 5) Export sales - $50,000 GST charged at 0%")

111

HOW TO COMPLETE GST F5 Box 1 Standard-rated supplies $15,000

Box 2 Zero-rated supplies $50,000 Box 3 Exempt supplies $0 Box 4 Total of Box $65,000 Box 5 Taxable purchases $28,000 Box 6 Output tax $1,050.00 Box 7 Input tax $1,960.00 Box 8 Net GST to be claimed $910.00 Box 9 Total imports under MES $0

112

GST F7 (Disclosure of Errors in GST Return)

Purpose: To disclose errors made in the GST F5 But you do not use it for all errors! The following chart will help you determine if you need to file F7(s) for your errors

for your errors.")

113

ERRORS Is the total of all errors > 5% of total supplies?

Do the errors involve GST? NO NO Include the errors in the next return NO YES Is the amount of net GST errors > $500? YES YES File in F7

114

GST F7 (Disclosure of Errors in GST Return)

Example 1 Errors involve GST (values of supplies and purchases are correct) Qtr 1: Overdeclared by $300 Qtr 2: Underdeclared by $200 Qtr 3: Overdeclared by $250

Qtr 1: Overdeclared by $300. Qtr 2: Underdeclared by $200. Qtr 3: Overdeclared by $250.")

115

GST F7 (Disclosure of Errors in GST Return)

Net GST error = = $350 As the net error is $350 (<$500), no need to file GST F7. Just adjust in Box 7 of current GST F5.

, no need to file GST F7. Just adjust in Box 7 of current GST F5.")

116

GST F7 (Disclosure of Errors in GST Return)

Example 2 Errors do not involve GST Standard-rated supplies error = $200 (output tax is correct) Zero-rated supplies error = $10,000 Taxable purchases error = $500 (input tax is correct)

Zero-rated supplies error = $10,000. Taxable purchases error = $500 (input tax is correct)")

117

GST F7 (Disclosure of Errors in GST Return)

Total errors = $ , = $10,700 Total supplies = $150,000 Percentage of error to total supplies = $10,700/$150,000 X 100 = 7% (>5%) => File GST F7 for the quarter the error was made

=> File GST F7 for the quarter the error was made.")

118

GST F7 (Disclosure of Errors in GST Return)

How can I obtain the GST F7? You can: call GST Integrated Phone Service at (Option 4) request through your TaxPortal write in visit us personally at our Taxpayer Services Centre (1st floor, Revenue House) – Letter of Authority required

request through your TaxPortal. write in. visit us personally at our Taxpayer Services Centre (1st floor, Revenue House) – Letter of Authority required.")

119

VOLUNTARY DISCLOSURE Take steps to ensure compliance with GST Legislation File true and complete returns Remember: Always do it right the first time

120

VOLUNTARY DISCLOSURE Good practice: To review past returns and disclose errors by filing the GST F7 and make the necessary adjustments. Otherwise, heavier penalty will be imposed if the errors are discovered by us.

121

Submission of incorrect return

Omission/understatement of output tax or overstatement of input tax; or Gives any incorrect information Penalty = Amount of tax undercharged

122

Submission of incorrect return

Without reasonable excuse or negligence Penalty = 2 X Amt of tax undercharged; and Fine < $5,000; or Imprisonment < 3 years; or both

123

COMMON MISCONCEPTIONS

124

COMMON MISCONCEPTIONS

Gifts : need not account GST Trade-in : charge GST on net amount Non-reporting of supplies On-charging of supplies Absorption of GST

125

COMMON MISCONCEPTIONS

Tourist Refund Scheme: Tourist can claim GST based on tax invoices only

126

Misconception No. 1 Gifts : Need not account GST

Conditions for accounting GST on gifts : Incurred GST on purchase of goods Cost of gift > $ 200 or Cost of gift < $ 200, but 3 or more gifts given to the same person within 3 months A lot of traders make the mistake of not charging output tax on gifts. FYI, You will need to charge output tax on gifts if it satisfies the following conditions. Firstly, you must have incurred input tax on the gift, i.e. you have made a purchase from another registered trader. The cost of the gift is > $200. However, if the cost < or = to $200 but 3 or more gifts are given to the same person within 3 months to form a series of gift, then you will be required to account output tax on these gifts.

127

GIFTS >$200 / SERIES OF GIFTS.

GST must be accounted on goods given out as Lucky Draw prizes eg. Dinner & Dance lucky draw prizes Hampers/Gifts to clients Also, please remember that you will need to account output tax for the following items listed here as well.

128

Misconception No. 2 Trade-in : Charge GST on net amount

GST must be accounted on the value of the 2 separate supplies Incorrect to account GST on the net difference only GST is a transaction based tax. Thus, for a trade-in, there are actually 2 supplies here. It is wrong to account GST on the net difference only. Let me illustrate this with an example.

129

A Year End Sale Not to Be Missed!!!

Fridges are going at an unbeatable price of $650 only!! Even more incredible news!! Trade in your old fridge for a Brand New Fridge for only $450!! Unbelievable but true!! So come on down to our stores now !!!

130

Misconception No. 3 Non-reporting of supplies

On-Charging of Supplies Absorption of GST Now we come to the area where traders fail to report their supplies thinking that they need not report them in the first place.

131

ON-CHARGING OF SUPPLIES

Reimbursements vs Disbursements Reimbursements - supply attracts GST Disbursements - do not attract GST We will look at the difference between reimbursement and disbursement. To start off, just bear in mind as we go through the illustrations that reimbursements attract GST, while disbursements do not. The place of supply rule holds. For reimbursements to another local company and a related company, you will need to std-rate as usual; but if the reimbursement is to an overseas company, you may be able to standard-rate it depending on the circumstances.

132

DISBURSEMENTS OR REIMBURSEMENTS

Both involve payments to third parties “on behalf” of another party. GST treatment depends on whether the payment is treated as a disbursement or a reimbursement (rebilling). Disbursement: No GST chargeable Reimbursement: GST chargeable Confusion arises when determining whether a series of transactions results in a reimbursement (within the scope of GST) or a disbursement (outside the scope of GST) is the fact that both words are often used interchangeably, as though they have the same meaning.

. Disbursement: No GST chargeable. Reimbursement: GST chargeable. Confusion arises when determining whether a series of transactions results in a reimbursement (within the scope of GST) or a disbursement (outside the scope of GST) is the fact that both words are often used interchangeably, as though they have the same meaning.")

133

GST CONCEPT Section 8(1)of GST Act:

“Tax shall be charged on any supply of goods or services made in Singapore where it is a taxable supply in the course or furtherance of any business carried on by him.”

134

WHAT IS A SUPPLY? Section 10(2)(a) of the GST Act:

“…includes all forms of supply, but not anything done otherwise than for a consideration” What is important from a GST perspective is to determine whether any money received amounts to consideration for a supply of goods or services. Where a taxpayer purchases goods and then passes them on to someone else, there has likely been a supply made to him and by him, both of which should be subject to GST if made by registered businesses in Singapore.

135

DISBURSEMENTS OR REIMBURSEMENTS

Contract for gds and svcs is between Co A & 3rd party. Tax Invoice is issued to Co A. Co A is legally responsible to pay 3rd party for the gds & svcs. Onward supply 3rd party (Supplier) Co A Co B (Main Contractor) Contract for goods and services is directly between Co B and 3rd party. Tax invoice is issued to Co B. Co B is legally responsible to pay 3rd party for the goods and services. Reimbursement is in essence 2 supplies. One from supplier to Co A and another from Co A to, say, the main contractor (MC). If Co A seeks reimbursement from the main contractor (MC), GST is chargeable because it is treated as an onward supply from A to the MC. Disbursement: No Supply, no GST chargeable Reimbursement: A supply exists and GST chargeable

Co A. Co B. (Main Contractor) Contract for goods and services is directly between Co B and 3rd party. Tax invoice is issued to Co B. Co B is legally responsible to pay 3rd party for the goods and services. Reimbursement is in essence 2 supplies. One from supplier to Co A and another from Co A to, say, the main contractor (MC). If Co A seeks reimbursement from the main contractor (MC), GST is chargeable because it is treated as an onward supply from A to the MC. Disbursement: No Supply, no GST chargeable. Reimbursement: A supply exists and GST chargeable.")

136

ABSORPTION OF GST I wish to absorb the GST on my sales. Do I have to pay any GST to IRAS? GST must be accounted to IRAS on supplies even if you absorb GST. The GST is calculated as follows: GST = 7/107 x selling price Eg : selling price=$100 GST = 7/107 x $100 = $6.54 Another commonly asked question is this:.... Please note that even though you claim that you are absorbing GST, in actual fact, there is still GST accountable to IRAS. The amount is worked out as follows:

137

Misconception No. 4 Tourist Refund Scheme : Tourist can claim GST based on tax invoices only

For tourist who buys goods from you to qualify for refund: - You must participate under Tourist Refund Scheme - You must issue tax-free shopping cheque(s) or refund claim form(s) to tourists so as to enable them to claim GST

or refund claim form(s) to tourists so as to enable them to claim GST.")

138

TOURIST REFUND SCHEME Global Refund Singapore Pte Ltd : 6225 6238

Premier Tax Free (Singapore) Pte Ltd : Singapore Retailer Association :

Pte Ltd. : Singapore Retailer Association :")

139

Application Exercise

140

APPLICATION EXERCISE Answers to Exercise Supplies :

1) Export sales : zero-rated supply <0%> 2) Local sales : standard-rated supply <7%> 3) Disposal of business asset <7%> 4) Interest income : <exempt supply> 5) Value of gift >$200 : Deemed supply <7%> 6) Payment of wages and salaries <Out-of-scope supply>

Export sales : zero-rated supply <0%> 2) Local sales : standard-rated supply <7%> 3) Disposal of business asset <7%> 4) Interest income : <exempt supply> 5) Value of gift >$200 : Deemed supply <7%> 6) Payment of wages and salaries <Out-of-scope supply>")

141

APPLICATION EXERCISE Answers to Exercise Purchases/ Payment :

7) Taxable purchase <claimable> 8) Taxable purchase <claimable> 9) Non-taxable purchase <not applicable> 10) Not allowable under Regulation 26 <not claimable>

Taxable purchase <claimable> 8) Taxable purchase <claimable> 9) Non-taxable purchase <not applicable> 10) Not allowable under Regulation 26 <not claimable>")

142

CONTENTS Penalties & Recovery Actions Slide 3

- Change of business circumstances - Common misconceptions - Common errors - Application exercise - Q & A session - Feedback

143

PENALTIES ON NON / LATE SUBMISSION OF GST F5

$ PER COMPLETED MONTH ( MAXIMUM $10,000 FOR EACH RETURN ) Eg: GST F5 for the quarter ended 31 Dec 2006 due on 31 Jan 2007. GST F5 filed on 14 May 2007 No. of months late = 3 (Feb to Apr) Amount of penalties = $ (3 x $200)

Eg: GST F5 for the quarter ended 31 Dec due on 31 Jan GST F5 filed on 14 May No. of months late = 3 (Feb to Apr) Amount of penalties = $ (3 x $200)")

144

PENALTIES ON NON / LATE SUBMISSION OF GST F5

FINE NOT EXCEEDING $5,000 AND IN DEFAULT OF PAYMENT TO IMPRISONMENT NOT EXCEEDING 6 MONTHS DIRECTOR’S LIABILITY (S74(1) OF THE GST ACT)

OF THE GST ACT)")

145

USEFUL INFORMATION RE: GST F5

ISSUANCE OF GST F5 NOTIFICATION OF CHANGE OF ADDRESS CONFIRMATION OF RETURN RECEIVED GST HELPLINE:

146

PENALTIES ON NON / LATE PAYMENT OF GST

5 % ON OUTSTANDING TAX ADDITIONAL PENALTY OF 2% OF TAX OUTSTANDING ADDED FOR EACH COMPLETED MONTH UP TO MAXIMUM 50% OF TAX OUTSTANDING

147

RECOVERY ACTIONS NON-FILING OF GST RETURN

ISSUE OF DEFAULT ASSESSMENT IMPOSE PENALTIES ON NON / LATE SUBMISSION OF GST F5 ISSUE SUMMONS TO ATTEND COURT

148

RECOVERY ACTIONS NON PAYMENT OF TAX

IMPOSE PENALTIES ON TAX OUTSTANDING APPOINT OTHER PARTY AS AGENT eg. BANK, TENANT STOP INDIVIDUAL FROM LEAVING THE COUNTRY TAKE LEGAL ACTIONS

149

Q & A Session

150

Last update on 17 April 2007

Similar presentations

is a tax on value added by any economic activity(like manufacturing, retailing etc.) VAT is collected in stages on transactions involving.>")

: Presentation on GST Legislation.>")

>")

>")

Applies to the sale.>")

>")