Download presentation

Presentation is loading. Please wait.

1

Pricing Strategies and Tactics

Luiz Afonso dos Santos Senna, PhD

2

Fatores na fixação de Preço

Q: When you set the price for your products or service, what factors influenced you? Pricing decisions are influenced by various factors: Cost of the product Economic conditions Competition Customer needs and characteristics (age, taste, geography) Company objectives NEXT SLIDE

Company objectives. NEXT SLIDE.")

3

Fatores Externos afetando as decisões de preços

Fatores Externos incluem a natureza do mercado e da demanda, competição e outros elementos ambientais Mercado e demanda Custos definem o limite inferior e a demanda define o limite de preço. As relações preço-demanda são fuindamentais par aos teomadres de decisão em transportes

4

Preço em diferentes tipos de mercados

Mercados de Competição Pura Bens/serviços uniformes Não existe um único vendedor ou comprador com efeito significativo sobre o preço de mercado Marketing mix possui pouco impacto

5

Preço em diferentes tipos de mercados

Competição Monopolística Compradores e vendedores trocam sobre uma gama de preços Ênfase em diferenças por meio de diferenciação através de marketing mix Competição Oligopolística Poucos vendedores altamente sensíveis aos preços de cada um e de estratégias de marketing

6

Objetivos de Pricing Considerações primárias na fixação de preços

7

Preço baseado em custos X baseado em valor

Cost-based versus value-based pricing Source: The Strategy and Tactics of Pricing, by Thomas T. Nagle and Reed K. Holden (2011)

")

8

Pricing, Competição e Estrutura de Mercado

9

Porter’s Five Forces Model (old)

How does our pricing strategy fit into this framework? What economic principles apply?

10

Market Structure – Internal rivalry

Market structure and pricing decisions are closely related. But how to define the market? The degree to which the firm gets to choose price is determined in large part by market structure There are two extreme cases: perfect competition and monopoly

11

Assessing and responding to a competitor’s price cut (depending on the market structure)

")

12

Perfect Competition Large numbers of buyers and sellers

Conditions necessary: Large numbers of buyers and sellers Homogeneous product Free entry and exit Perfect information

13

Perfect Competition Demand curve for any given firm is horizontal. Price is set by market at Pe Firm can sell as much or as little as desired at market price, but nothing if they raise P.

14

Monopoly Conditions necessary

Single seller of product No close substitutes Significant barriers to entry There are few examples of perfect competition and pure monopoly. Most firms have a differentiated product, and there are substitutes.

15

Pricing in Perfect Competition

Do not choose price. Choose output quantity. TC includes opportunity cost of capital invested. What will be our profit (loss) from our output decision? Should we produce now? (SR) Should we stay in the industry? (LR)

from our output decision Should we produce now (SR) Should we stay in the industry (LR)")

16

Costs at different levels of production

Cost per unit at different levels of production

17

Pricing in a Monopoly Profit maximization will be achieved by setting price so that MC=MR. It is not reached by setting price as “high as possible.” Like any firm, the monopolist is constrained by their demand curve. One cannot choose both P and Q.

18

The Shut-Down Rule At what point should the firm cease production of a certain item? When might it pay to produce at a loss? In SR, many costs are fixed. Just because a firm is making losses, it does not necessarily mean it should shut down (short run), or even go out of business (long-run).

, or even go out of business (long-run).")

19

The Shut-Down Rule cont.

Profit = TR – TC; TR=P*Q, TC = VC + FC (TR - VC) - FC = [(P - AVC)Q] – FC Separate out fixed costs, focus on variable elements As long as P>AVC, there is a positive contribution to fixed costs. If firm shuts down (Q = 0), then Profit = - FC If shut down: Firm has a loss of fixed costs.

- FC = [(P - AVC)Q] – FC. Separate out fixed costs, focus on variable elements. As long as P>AVC, there is a positive contribution to fixed costs. If firm shuts down (Q = 0), then Profit = - FC. If shut down: Firm has a loss of fixed costs.")

20

The Shut-Down Rule cont.

In SR, firm may minimize losses by continuing to produce. If losses are expected permanently, get out. Case of multiple products: C = FC + VC1 + VC2

21

The Shut-Down Rule P = (TR1 - TVC1) + (TR2 - TVC2) - FC

P = (P1*Q1 - AVC1*Q1) + (P2*Q2 - AVC2*Q2) - FC P = [(P1 - AVC1)*Q1]+ [(P2 - AVC2)*Q2] - FC Results: SR - each product should be produced if Pi>AVCi In LR, the firm should continue operating only if expected P>=0 (Profits are non-negative)

+ (P2*Q2 - AVC2*Q2) - FC. P = [(P1 - AVC1)*Q1]+ [(P2 - AVC2)*Q2] - FC. Results: SR - each product should be produced if Pi>AVCi. In LR, the firm should continue operating only if expected P>=0 (Profits are non-negative)")

22

Price Discrimination Selling the same good to different people at different prices Conditions necessary: Identifiable customer groups with differing price elasticities Maintain separation of groups--prevent resale.

23

Types of Price Discrimination

First degree Identify and charge each customer what they are willing to pay Limit: D = MR, no consumer surplus. Second degree Quantity discounts. Volume purchases are given lower prices. Need to measure goods and services bought by consumers.

24

Types of Price Discrimination

Third degree Segment markets in some way. Charge all in the segment the same prices. Treat each segment as a separate market– then do MR=MC in each Are coupons as a price discrimination mechanism?

25

Oligopoly Strategies Must have credibility.

Common theme - Rivalrous behavior Pricing - limit pricing - set prices low as signal to possible entrants or other competitors your willingness and ability to defend your market share. Must have credibility. Trading SR profit for more profits later

26

Oligopoly Strategies Use the legal / regulatory systems

File patent application Challenge business charter application File regulatory challenge Pre-emptive entry - Wal-Mart

27

Oligopoly Strategies Announce capacity expansion

Capacity and production Announce capacity expansion Revise/modify products - more difficult to copy Advertising Raise cost of entry for others

28

Oligopoly and Monopolistic Competition

Few sellers - usually large ones Recognized interdependence in pricing and output decisions Need to consider response of rivals in pricing decisions Typically significant barriers to entry

29

Oligopoly and Monopolistic Competition

Large number of interdependent sellers Differentiated product Good substitutes Easy entry and exit

30

Oligopoly and Monopolistic Competition

Most industries are one or the other Oligopoly: many heavy manufacturing Autos, steel, chemicals, pharmaceuticals Monopolistic Competition Service companies, retail stores, large corporations (McDonald’s, Wendy’s) The important point is that demand is downward sloping

The important point is that demand is downward sloping.")

31

Cartels Small number of firms Homogeneous product Entry barriers

Illegal in most countries – but encouraged in others Conditions helpful: Small number of firms Homogeneous product Entry barriers Similarity of members

32

Cartels Cheating on agreement Price cutting behaviour

Problems with cartels: Cheating on agreement Price cutting behaviour Tend to fall apart Note: When might firms in an industry ask for (demand) regulation?

regulation")

33

Pricing Strategies Profit maximizing rule:

Set production at level where MR = MC Non - Maximizing pricing rules there are a variety of these

34

Pricing for Multi-Product Firm

Two products, x and y. TRfirm = TRx + TRy If there are any spillovers from x to y, then you may get complications.

35

Multi-Product Firm cont.

The two terms on the right side of the equation represent interactions. They can be either positive or negative. If x and y are complementary goods, the effect is positive. If x and y are substitutes, the effect is negative. One unit’s gain is the other’s loss.

36

Two part pricing Charge P = MC

charge a fixed fee to extract some of the “consumer surplus” Examples: country clubs health clubs electricity providers

37

Declining block pricing

Charging different prices according to how much is purchased Attempt to extract consumer surplus and transfer value to company

38

Auction pricing models

Standard auction model multiple bidders compete with each other start at some low price, then successive bids raise price until someone “wins” Dutch auction model start at a high price, lower it until someone bids ex: dutch flower auctions How to extract consumer surplus?

39

Porter’s Five Forces Model

How does the development of online business affect this analytic tool? How does the Internet change the economic principles that apply?

40

Market structure and the Internet

Traditional industry structure paradigm? Structure, time and place? Firm size, customer access and service? Pricing, and reputation online Who is competing with whom?

42

Internet and demand issues

Role of customer service and customer loyalty online: e-loyalty? Consumer demand issues - which goods to buy online, which in person? How to price online? Does this signal the end of the Brand?

43

Pricing and the Internet

Traditional pricing paradigm? Access to demand data…... Measurement of demand elasticities? Ability to conduct pricing “experiments” Ability to spot market changes - and move quickly (perhaps) Access to bigger customer base Will prices be lower online?

Access to bigger customer base. Will prices be lower online")

44

Firm structure and the Internet

Are traditional firm structure concepts now irrelevant? Economies of scale? Scope? How does this affect firm incentives to vertically integrate (or de-integrate)? Central role of transaction costs…...

Central role of transaction costs…...")

45

The Determinants of Demand

Demand The relationship between the quantity of a good desired by people in a market and the factors that affect that the quantity desired is referred to as the demand for the product. We can express the demand for a product in the form We have some precise definitions related to how income and prices of other goods affect the demand for a good/service

46

Price of other goods (pj) Income (y) Expectations of future prices

Factors that we expect to affect the demand for the good include: Population (n) Price of the good (pi) Price of other goods (pj) Income (y) Expectations of future prices Tastes (T)

Price of the good (pi) Price of other goods (pj) Income (y) Expectations of future prices. Tastes (T)")

47

Substitutes and Complements

Two goods, x and y, are said to be substitutes if an increase in the price of x (y) increases the demand for good y (x) and a decrease in the price of x (y) decreases the demand for y (x) – (Butter and margarine) Two goods, x and y, are said to be complements if an increase in the price of x (y) decreases the demand for good y (x) and a decrease in the price of x (y) decreases the demand for y (x) (Sugar and coffee)

increases the demand for good y (x) and a decrease in the price of x (y) decreases the demand for y (x) – (Butter and margarine) Two goods, x and y, are said to be complements if an increase in the price of x (y) decreases the demand for good y (x) and a decrease in the price of x (y) decreases the demand for y (x) (Sugar and coffee)")

48

Income and Demand A good is said to be normal if an increase (decrease) in income increases (decreases) the demand for the good. A good is said to be inferior if an increase (decrease) in income decreases (increases) the demand for a good

in income increases (decreases) the demand for the good. A good is said to be inferior if an increase (decrease) in income decreases (increases) the demand for a good.")

49

The Demand Curve The relationship between the quantity demanded of a good and the price of that good is referred to as the demand curve.

51

The demand curve gives the relationship between price and the quantity consumers will desire to purchase at that price Note the demand curve is drawn given that no other factors affecting the demand for the product, such as income, population, or tastes, change Demand for the product is based on specific, unchanging values for the other factors that affect demand

52

The Law of Demand As the price of a good decreases (increases), more (less) of it will be purchased That is, the demand curve is downward sloping There are two factors that explain this relationship: As the price of a good increases, consumers will substitute into other goods (substitution effect); .As the price of a good increases, consumers will have less real income to purchase all goods (income effect).

; .As the price of a good increases, consumers will have less real income to purchase all goods (income effect).")

53

Changes in Demand versus Changes in Quantity Demanded

A movement along a demand curve is referred to as a change in quantity demanded. The quantity demanded changes because of a price change. A shift in the demand curve is referred to as a change in demand. Demand changes (the demand curve shifts) because of a change in one of the factors affecting demand other than price (income, price of other goods, tastes, population) changes.

because of a change in one of the factors affecting demand other than price (income, price of other goods, tastes, population) changes.")

54

Demand for steaks D1 represents the demand for steaks (lbs/day) given the price of chicken is $3.50; the number of customers is 1,500 a day; and the average annual household income is $40 thousand. Then we might expect the following: A decrease in demand for steak if the price of chicken, a substitute for steak, fell from $3.50 to $2.00. This is shown by a shift in of the demand curve from D1 to D2 An increase in demand for steak if the annual income increases from $40 to $60 thousand, since steak is a normal good. This is shown by a shift out of the demand curve from D1 to D3

given the price of chicken is $3.50; the number of customers is 1,500 a day; and the average annual household income is $40 thousand. Then we might expect the following: A decrease in demand for steak if the price of chicken, a substitute for steak, fell from $3.50 to $2.00. This is shown by a shift in of the demand curve from D1 to D2. An increase in demand for steak if the annual income increases from $40 to $60 thousand, since steak is a normal good. This is shown by a shift out of the demand curve from D1 to D3.")

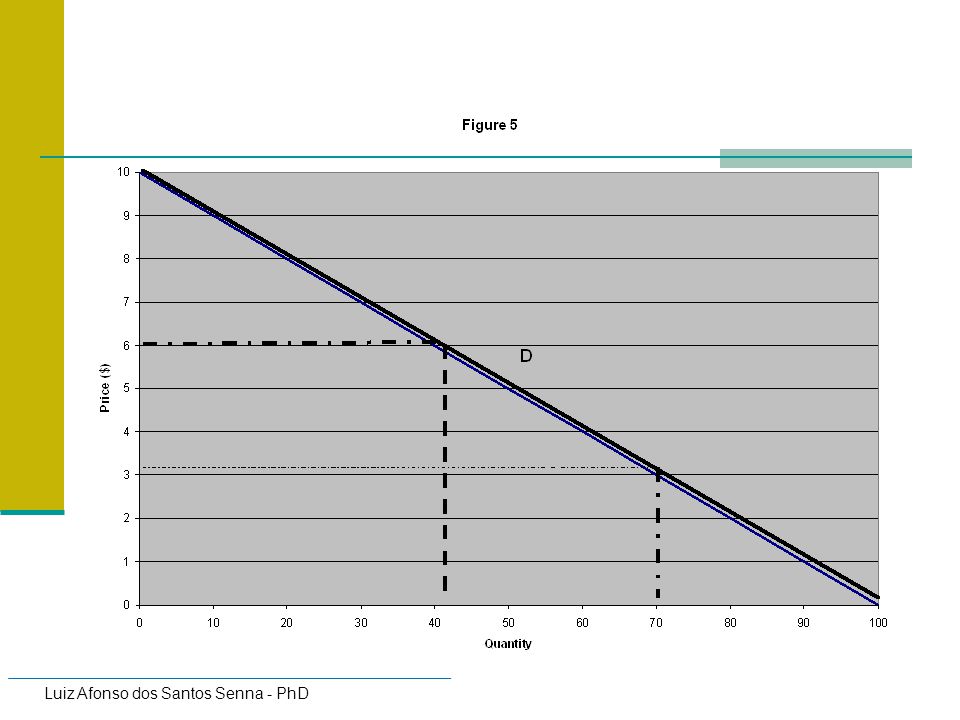

57

Algebraic Representation

The preceding figure that follows is given by QD = P Linear relationship we can graph by choosing two points. Easiest points: Q = 0 0 = P or P = 10, Q = 0 P = 0 implying Q = (0) = 100 and therefore P = 0, Q = 100 Slope, dQ/dP = -10

= 100 and therefore P = 0, Q = 100. Slope, dQ/dP = -10.")

58

The Determinants of Supply

Number of Firms Price of Product Cost of inputs Wages Capital Materials Price of other goods Expectations of Future Prices Technology

59

The Supply Curve The relationship between the quantity supplied of a good and the price of that good is referred to as the supply curve The supply curve gives the relationship between price and the quantity produces will wish to sell at that price Note the supply curve is drawn given that no other factors affecting the supply for the product Supply of the product is based on specific, unchanging values for the other factors that affect supply

61

The Law of Supply As the price of a good increases (decreases), more (less) of it will be produced and offered for sale. The supply curve is upward sloping. This is explained by the assumption that marginal (incremental) cost increases as output increases.

cost increases as output increases.")

62

Changes in Supply versus Changes in Quantity Supplied

A movement along a supply curve is referred to as a change in quantity supplied. The quantity supplied changes because of a price change. A shift in the supply curve is referred to as a change in supply. Supply changes (the supply curve shifts) because of a change in one of the factors affecting supply other than price changes.

because of a change in one of the factors affecting supply other than price changes.")

63

Comparisons What happens to Price & Quantity when: Incomes increase

Wages fall Prices of other goods change Making predictions of the impact on the market of these types of changes is referred to as Comparative Statics

64

Comparisons These changes are all changes in demand or changes in supply Shifts in demand or supply curve 4 possibilities: Increase in demand (shift out demand curve) Decrease in demand (shift in demand curve) Increase in supply (shift out supply curve) Decrease in supply (shift in supply curve)

Decrease in demand (shift in demand curve) Increase in supply (shift out supply curve) Decrease in supply (shift in supply curve)")

66

Pricing Strategy How does a company decide what price to charge for its products and services? What is “the price” anyway? doesn’t price vary across situations and over time? Some firms have to decide what to charge different customers and in different situations They must decide whether discounts are to be offered, to whom, when, and for what reason

67

Why is Pricing Important?

In a company with average economics*, 1% increase in volume = 3.3% increase in profit 1% increase in price = 11.1% increase in profit Improvements in price typically have 3-4 times the effect on profit as proportionate increases in volume. *Based on average of 2,463 companies

68

Price vs. Nonprice Competition

In price competition, a seller regularly offers products priced as low as possible and accompanied by a minimum of services In non price competition, a seller has stable prices and stresses other aspects of marketing With value pricing, firms strive for more benefits at lower costs to consumer With relationship pricing, customers have incentives to be loyal-- get price incentive if you do more business with one firm

69

Nonprice Competition Some firms feel price is the main competitive tool, that customers always want low prices Other firms are looking for ways to add value, thereby being able to avoid low prices Sometimes prices have to be changed in response to competitive actions Many firms would prefer to engage in non price competition by building brand equity and relationships with customers

70

SELECT PRICING OBJECTIVE

The Process: An Illustration SELECT PRICING OBJECTIVE SELECT METHOD OF DETERMINING THE BASE PRICE: Cost-plus pricing Price based on both demand and costs Price set in relation to market alone DESIGN APPROPRIATE STRATEGIES: Price vs. nonprice competition Skimming vs. penetration Discounts and allowances Freight payments One price vs. flexible price Psychological pricing Leader pricing Everyday low vs. high-low pricing Resale price maintenance

71

Steps for Determining Prices

Establish Pricing Objectives Increase sales volume? Prestigious image? Increase market share?

72

Steps for Determining Prices

Study Costs Can you make a profit? Can you reduce costs without affecting quality or image?

73

Steps for Determining Prices

Estimate Demand What do customers expect to pay? Prices usually are directly related to demand.

74

Steps for Determining Prices

Study Competition

75

Steps for Determining Prices

Decide on a Pricing Strategy Price higher than the competition because your product is superior Price lower, then raise it once your product is accepted

76

Steps for Determining Prices

Set Price Monitor and evaluate its effectiveness as conditions in the market change

77

Pricing Technology Smart Pricing – decisions are based on an enormous amount of data that Web-based pricing technology crunches into timely, usable information. Communicating Prices to Customers – electronic gadgets that provide real-time pricing information such as electronic shelves, digital price labels

78

Pricing Technology RFID Technology – wireless technology that involves tiny chips imbedded in products. The chip has an antenna, a battery, and a memory chip filled with a description of the item Toll technology

79

Geographic Considerations

FOB (free on board) plant or FOB origin: Price quotation that does not include shipping charges. Buyer pays all freight charges to transport the product from the manufacturer Freight absorption: system for handling transportation costs under which the buyer may deduct shipping expenses from the costs of goods

plant or FOB origin: Price quotation that does not include shipping charges. Buyer pays all freight charges to transport the product from the manufacturer. Freight absorption: system for handling transportation costs under which the buyer may deduct shipping expenses from the costs of goods.")

80

Uniform-delivered price: system for handling transportation costs under which all buyers are quoted with the same price, including transportation expenses Zone pricing: system for handling transportation costs under which the market is divided into geographic regions and a different price is set in each region Basing-point system: system for handling transportation costs in which the buyer’s costs included the factory price plus freight charges from the basing-point city nearest the buyer. Seeks to equalize competition between distant marketers

81

Product and Pricing Strategies

This chapter, the second of four on the marketing function, gives you a close look at two elements of the marketing mix: product and price. The exploration of price starts with a rundown of the major types of products, the life cycle that most products progress through from introduction to the point at which they’re removed from the market, and the process companies use to create new products. Following that, you’ll learn about the techniques used to identify products: branding, packaging, and labeling. The final product discussion involves the decisions companies make when managing multiple families of products. The chapter wraps up with a look at pricing strategies. Product and Pricing Strategies

82

Product Characteristics

Types of Products Stages As the central element in every company’s exchanges with its customers, products naturally command considerable attention when managers plan new offerings and manage the marketing mixes for their existing offerings. To understand the nature of these decisions, it’s important to recognize the various types of products and the stages that products go through during their “lifetime” in the marketplace.

83

Marketing Strategy Over the Product Life Cycle

INTRODUCTION GROWTH MATURITY DECLINE Marketing strategy Market development Increase market Defend market Maintain efficiency in emphasis share share exploiting product Pricing High price, unique Lower price Price at or below Set price to remain strategy product / cover over time competition profitable or reduce production costs to liquidate Promotion Mount sales Appeal to Emphasize Reinforce loyal Strategy promotion for mass market brand differences, customers; reduce product awareness benefits & loyalty promotion costs Place strategy Distribute through Build intensive Enlarge Be selective in selective outlets network of distribution distribution, trim outlets network unprofitable outlets FOCUS: pricing strategies SHOW TITLE ONLY! ELICIT the appropriate PRICING STRATEGIES at each stage of the Product Life Cycle! Ask Ss for an example of one of their products or services. Q: At what stage is it? How are you pricing it? (How much does it cost?) Have you changed the price? Are you planning to change the price? When and why? Q: As a producer, what pricing strategy would you use when you introduce a product? high volume/low price or high price/lower volume must recover R&D investment; penetration or skimming Q: What would you do regarding the price as the product enters the growth and maturity stage? Lower price Competitive pricing Q: At what stages do you think it is really important to promote the product to ensure its survival? (introduction & maturity) Please remember this for your own product. During which of the 6 weeks would that be? (Weeks 4,5,6) Q: What would you do in terms of amount of promotion to introduce a product? Special sales promotions; displays; flyers to raise awareness Emphasize uniqueness of product! Q: What would you do in the maturity stage – increase or decrease advertising? Advertising = heaviest; highest cost outlay for the product

Have you changed the price Are you planning to change the price When and why Q: As a producer, what pricing strategy would you use when you introduce a product high volume/low price or high price/lower volume must recover R&D investment; penetration or skimming. Q: What would you do regarding the price as the product enters the growth and maturity stage Lower price Competitive pricing. Q: At what stages do you think it is really important to promote the product to ensure its survival (introduction & maturity) Please remember this for your own product. During which of the 6 weeks would that be (Weeks 4,5,6) Q: What would you do in terms of amount of promotion to introduce a product Special sales promotions; displays; flyers to raise awareness. Emphasize uniqueness of product! Q: What would you do in the maturity stage – increase or decrease advertising Advertising = heaviest; highest cost outlay for the product.")

84

Other Pricing Strategies

Price-Based Optimization Skimming Penetration Most manufacturers design a product, then try to figure out how to make it for a price. But recent thinking holds that cost should be the last item analyzed in the pricing formula, not the first. Companies that use priced-based pricing can maximize their profit by first establishing an optimal price for a product or service. The product's price is based on an analysis of a product's competitive advantages, the users' perception of the item, and the market being targeted. Once the desired price has been established, the firm focuses its energies on keeping costs at a level that will allow a healthy profit. Optimal pricing uses computer software to generate the ideal price for every item, at each individual store, at any given time. Research shows that many retailers routinely underprice or overprice the merchandise of their shelves. They generally set a price by marking up from cost, or by benchmarking against the competition’s prices, or simply by hunch. A product's price seldom remains constant and will vary depending on the product's stage in its life cycle. During the introductory phase, for example, the objective might be to recover product development costs as quickly as possible. To achieve this goal, the manufacturer might charge a high initial price—a practice known as skimming—and then drop the price later, when the product is no longer a novelty and competition heats up. Rather than setting a high initial price to skim off a small but profitable market segment, a company might try to build sales volume by charging a low initial price, a practice known as penetration pricing. This approach has the added advantage of discouraging competition, because the low price (which competitors would be pressured to match) limits the profit potential for everyone.

limits the profit potential for everyone.")

85

Price Adjustment Strategies

Discount Pricing Bundling Dynamic Pricing Once a company has set a products’ price, it may choose to adjust that price from time to time to account for changing market situations or changing customer preferences. Three common price adjustment strategies are price discounts, bundling, and dynamic pricing. When you use discount pricing, you offer various types of temporary price reductions, depending on the type of customer being targeted and the type of item being offered. Sometimes sellers combine several of their products and sell them at one reduced price. This practice, called bundling, can promote sales of products consumers might not otherwise buy—especially when the combined price is low enough to entice them to purchase the bundle. Dynamic pricing is the opposite of fixed pricing. Using Internet technology, companies continually reprice their products and services to meet supply and demand. Dynamic pricing not only enables companies to move slow selling merchandise instantly but also allows companies to experiment with different pricing levels. Because price changes are immediately posted to electronic catalogs or websites, customers always have the most current price information.

86

Pricing Strategies

87

Penetration Pricing

88

Penetration Pricing Price set to ‘penetrate the market’

‘Low’ price to secure high volumes Typical in mass market products – chocolate bars, food stuffs, household goods, etc. Suitable for products with long anticipated life cycles May be useful if launching into a new market

89

Market Skimming

90

Market Skimming High price, Low volumes

Skim the profit from the market Suitable for products that have short life cycles or which will face competition at some point in the future (e.g. after a patent runs out) Examples include: Playstation, jewellery, digital technology, new DVDs, etc.

Examples include: Playstation, jewellery, digital technology, new DVDs, etc.")

91

Market Skimming Many are predicting a firesale in laptops as supply exceeds demand Plasma screens: Currently at high prices but for how long? Title: Thin-shaped television. Copyright: Getty Images, available from Education Image Gallery

92

Value Pricing

93

Value Pricing Price set in accordance with customer perceptions about the value of the product / service Examples include status products/exclusive products Companies may be able to set prices according to perceived value. Title: BMW At The Frankfurt Auto Show. Copyright: Getty Images, available from Education Image Gallery

94

Loss Leader

95

Loss Leader Goods/services deliberately sold below cost to encourage sales elsewhere Typical in supermarkets, e.g. at Christmas, selling bottles of gin at £3 in the hope that people will be attracted to the store and buy other things Purchases of other items more than covers ‘loss’ on item sold e.g. ‘Free’ mobile phone when taking on contract package

96

Psychological Pricing

97

Psychological Pricing

Used to play on consumer perceptions Classic example - $9.99 instead of $10.00! Odd-even: $5.95, $.79, $699 OR $12, $50 Multiple Unit-3 for !1.00 better than $.34 each

98

Psychological Pricing

Odd-Even Pricing Odd numbers convey a bargain image -- $.79, $9.99, $699 Even numbers convey a quality image -- $10, $50, $100

99

Psychological Pricing

Prestige Pricing – sets a higher than average price to suggest status

100

Psychological Pricing

Multiple-Unit Pricing – 3 for $.99 Suggests a bargain and helps increase sales volume. Better than selling the same items at $.33 each.

101

Psychological Pricing

Everyday Low Prices (EDLP) – set on a consistent basis

– set on a consistent basis.")

102

Going Rate (Price Leadership)

")

103

Going Rate (Price Leadership)

In case of price leader, rivals have difficulty in competing on price – too high and they lose market share, too low and the price leader would match price and force smaller rival out of market May follow pricing leads of rivals especially where those rivals have a clear dominance of market shar Where competition is limited, ‘going rate’ pricing may be applicable – banks, petrol, supermarkets, electrical goods – find very similar prices in all outlets

104

Tender Pricing

105

Tender Pricing Many contracts awarded on a tender basis

Firm (or firms) submit their price for carrying out the work Purchaser then chooses which represents best value Most government contracts A European consortium led by Airbus recently won a contract to supply refuelling services to the RAF – priced at £13 billion!

submit their price for carrying out the work. Purchaser then chooses which represents best value. Most government contracts. A European consortium led by Airbus recently won a contract to supply refuelling services to the RAF – priced at £13 billion!")

106

Price Discrimination

107

Price Discrimination Charging a different price for the same good/service in different markets Requires each market to be impenetrable Requires different price elasticity of demand in each market Air/rail First class Business class Economy class Prices for rail travel differ for the same journey at different times of the day

108

Discounts and Allowances

Cash Discounts – offered to buyers to encourage them to pay their bills quickly. 2/10, net 30 Quantity Discounts – offered for placing large orders Trade Discounts – the way manufacturers quote prices to wholesalers and retailers.

109

Promotional Pricing -- Used with sales promotion

Loss Leader Pricing – offering very popular items for sale at below-cost prices Special-Event Back-to-school specials Dollar days Anniversary sales Rebates and Coupons

110

Discounts and Allowances

Seasonal Discount – offered outside the customary buying season

111

Discounts and Allowances

Allowances – go directly to the buyer. Customers are offered a price reduction if they sell back an old model of the product they are purchasing

112

Destroyer Pricing/Predatory Pricing

113

Destroyer/Predatory Pricing

Deliberate price cutting or offer of ‘free gifts/products’ to force rivals (normally smaller and weaker) out of business or prevent new entrants Anti-competitive and illegal if it can be proved Typical of oligopoly with collusion Microsoft – have been accused of predatory pricing strategies in offering ‘free’ software as part of their operating system – Internet Explorer and Windows Media Player - forcing competitors like Netscape and Real Player out of the market

out of business or prevent new entrants. Anti-competitive and illegal if it can be proved. Typical of oligopoly with collusion. Microsoft – have been accused of predatory pricing strategies in offering ‘free’ software as part of their operating system – Internet Explorer and Windows Media Player - forcing competitors like Netscape and Real Player out of the market.")

114

The Legality and Ethics of Price Strategy

Issues That Limit Pricing Decisions Unfair Trade Practices Price Fixing Price Discrimination Predatory Pricing

115

Unfair Trade Practice Acts

Laws that prohibit wholesalers and retailers from selling below cost

116

Price Fixing An agreement between two or more firms on the price they will charge for a product (usually in oligopolistic markets)

")

117

Price Discrimination The Robinson-Patman Act of 1936 (USA):

Prohibits any firm from selling to two or more different buyers at different prices if the result would lessen competition

118

Robinson-Patman Act Defenses

Seller Defenses Robinson-Patman Act Defenses Cost Market Conditions Competition

119

Predatory Pricing The practice of charging a very low price for a product with the intent of driving competitors out of business or out of a market.

120

Discussion: Impact of Ethics on Pricing

How should you price if your product is a life-saving drug? What are the ethical considerations? Customers have no choice Need to pay for the research When cheaper options doesn’t work Competition decides

121

Some other pricing strategies

These all involve the use of some numerical understanding….

122

Absorption/Full Cost Pricing

123

Absorption/Full Cost Pricing

Full Cost Pricing – attempting to set price to cover both fixed and variable costs Absorption Cost Pricing – Price set to ‘absorb’ some of the fixed costs of production

124

Marginal Cost Pricing

125

Marginal Cost Pricing Marginal cost – the cost of producing ONE extra or ONE fewer item of production MC pricing – allows flexibility Particularly relevant in transport where fixed costs may be relatively high Allows variable pricing structure – e.g. on a flight from London to New York – providing the cost of the extra passenger is covered, the price could be varied a good deal to attract customers and fill the aircraft

126

Marginal Cost Pricing Example:

Aircraft flying from Bristol to Edinburgh – Total Cost (including normal profit) = £15,000 of which £13,000 is fixed cost* Number of seats = 160, average price = £93.75 MC of each passenger = 2000/160 = £12.50 If flight not full, better to offer passengers chance of flying at £12.50 and fill the seat than not fill it at all! *All figures are estimates only

= £15,000 of which £13,000 is fixed cost* Number of seats = 160, average price = £ MC of each passenger = 2000/160 = £ If flight not full, better to offer passengers chance of flying at £12.50 and fill the seat than not fill it at all! *All figures are estimates only.")

127

Contribution Pricing

128

Contribution Pricing Contribution = Selling Price – Variable (direct costs) Prices set to ensure coverage of variable costs and a ‘contribution’ to the fixed costs Similar in principle to marginal cost pricing Break-even analysis might be useful in such circumstances

129

Target Pricing

130

Target Pricing Setting price to ‘target’ a specified profit level

Estimates of the cost and potential revenue at different prices, and thus the break-even have to be made, to determine the mark-up Mark-up = Profit/Cost x 100 This strategy is used by many clothes retailers where they can add upto 60% mark-up on the basic cost of the clothes. So even with a 50% sales offer they still make a profit!

131

Cost-Plus Pricing

132

Cost-Plus Pricing Calculation of the average cost (AC) plus a mark up

AC = Total Cost/Output

133

Influence of Elasticity

134

Influence of Elasticity

Price Inelastic: % change in Q < % change in P e.g. a 5% increase in price would be met by a fall in sales of something less than 5% Revenue would rise A 7% reduction in price would lead to a rise in sales of something less than 7% Revenue would fall

135

Influence of Elasticity

Any pricing decision must be mindful of the impact of price elasticity The degree of price elasticity impacts on the level of sales and hence revenue Elasticity focuses on proportionate (percentage) changes PED = % Change in Quantity demanded % Change in Price

changes. PED = % Change in Quantity demanded. % Change in Price.")

136

Influence of Elasticity

Price Elastic: % change in quantity demanded > % change in price e.g. A 4% rise in price would lead to sales falling by something more than 4% Revenue would fall A 9% fall in price would lead to a rise in sales of something more than 9% Revenue would rise

137

Select a Pricing Method

Mark-up Pricing - “Cost Plus” Target Return Pricing Perceived Value Pricing

138

Device Pricing vs. Whole Product Pricing

Value of any product to its market is strongly influenced by prices of competitive products Competitive “devices” are analyzed, but “products” are priced Product “features” have different values: Customer service Warranties Distribution channels (e.g., convenience) The “sum” of the features makes up the “product”

The sum of the features makes up the product")

139

Determining Perceived Value

What value is placed on the end result? The cost of alternative solutions to the customer. A function of: Prices of comparable (though not identical) products The “value” (+/-) of the product’s differences vs. the competitive offering The value of the “Whole Product”

products. The value (+/-) of the product’s differences vs. the competitive offering. The value of the Whole Product")

140

Economic Value Analysis

Identify the cost of the competitive product or process (i.e., the reference value) Identify all the factors that differentiate the product. Determine the value to the customer of these differentiating factors (i.e., the differentiation value) Sum the reference value and the differentiation value to determine the total economic value.

Identify all the factors that differentiate the product. Determine the value to the customer of these differentiating factors (i.e., the differentiation value) Sum the reference value and the differentiation value to determine the total economic value.")

141

Customer’s Perceived Value

Economic Value vs. Perceived Value Economic Value Product Performance Customer’s Perceived Value Marketing Effort* *A key task of marketing is to translate the economic value into high customer perceived value Pricing Decision

142

Select a Pricing Method

Mark-up Pricing - “Cost Plus” Target Return Pricing Perceived Value Pricing Value Pricing Going Rate Pricing (market price) Reference Pricing (comparison w/substitutes) Sealed-Bid Pricing

Reference Pricing (comparison w/substitutes) Sealed-Bid Pricing.")

143

Select the Final Price $ 10,000 $ 375.00 $2,000,000

Desired/Required Distributor Margins Psychological pricing Influence of other marketing mix elements Company pricing policies Impact of price on others $ 10,000 $ $2,000,000

144

Conjoint Analysis Stated Preference Methods Trade-off Analysis and Behavioural models

145

Behavioural Models -Logit Model-

e= basis of the logarithm neperiano i- alternative being considered J= set of alternatives where i is one of them Ui= utility function of altarnative i Uj= utility function of alternative j

146

Ui = utility function α= parameters to be estimated Xi= attributes

147

Data Collection Revealed Preference Stated preference

Data gained from experience Good to know about previous experience and existing products/services Stated preference Data gainded from hipothetical questions in selected scenarios Good to gain information about new services/products

Similar presentations

Entrepreneurship I.>")