Download presentation

Presentation is loading. Please wait.

1

Foundation for Accounting Education – FAE

2009 Business Valuation Conference New York, New York – May 21, 2007 Forensic Valuation: Faster, Better, Higher Return© The “Combat CPA©” Series… Darrell D. Dorrell, CPA/ABV, MBA, ASA, CVA, CMA, DABFA financialforensics®

2

Today – Session Description…

3 categories: Accelerate the valuation process Applied forensic techniques, e.g. guidelines Court cases re forensic accounting Will preview in reverse order Accelerate (throughout) 2

2.")

3

Our offices…

4

Who worked on this material?

5

The art & science of investigating

financialforensics® Our mission statement: To spearhead forensic accounting innovation in civil, criminal and combat matters.© (financialforensics® October 2002) The definition of forensic accounting is: The art & science of investigating people & money.© (financialforensics® Newsletter, September 1993)

The definition of forensic accounting is: The art & science of investigating. people & money.© (financialforensics® Newsletter, September 1993)")

6

Some of our recent work using these techniques…

US Department of Justice (USDOJ) – USA Bulletin: Forensic accounting - counter-terrorism Federal Bureau of Investigation (FBI) Forensic accounting - money laundering/white-collar crime Oregon Department of Justice (ORDOJ) HMC/Znetix, Inc. for SEC/Receiver - $106 million 2nd largest Washington securities fraud More than 12 executives; serving 910 months in aggregate Forensic Accountants’ Report: $400 mm for-profit: alter-ego/fraudulent conveyance - $20 million $100 mm for-profit: purchasing agent embezzlement $14 mm for-profit: controller embezzlement - $5.5 million $10 mm city: Finance Director embezzlement - $1.4 million $7 mm for-profit: CFO embezzlement $2 mm non-profit: controller embezzlement - $140,000 $1 mm for-profit: office manager embezzlement Dental practice: wife embezzlement - $70,000 Auto repair shop: owner embezzlement - $1,500 Law & Order TV series – technical advice Large Police Bureau – Financial Crimes

– USA Bulletin: Forensic accounting - counter-terrorism. Federal Bureau of Investigation (FBI) Forensic accounting - money laundering/white-collar crime. Oregon Department of Justice (ORDOJ) HMC/Znetix, Inc. for SEC/Receiver - $106 million. 2nd largest Washington securities fraud. More than 12 executives; serving 910 months in aggregate. Forensic Accountants’ Report: $400 mm for-profit: alter-ego/fraudulent conveyance - $20 million. $100 mm for-profit: purchasing agent embezzlement. $14 mm for-profit: controller embezzlement - $5.5 million. $10 mm city: Finance Director embezzlement - $1.4 million. $7 mm for-profit: CFO embezzlement. $2 mm non-profit: controller embezzlement - $140,000. $1 mm for-profit: office manager embezzlement. Dental practice: wife embezzlement - $70,000. Auto repair shop: owner embezzlement - $1,500. Law & Order TV series – technical advice. Large Police Bureau – Financial Crimes.")

7

CAN YOU GIVE US AN EXAMPLE OF HOW FORENSIC ACCOUNTING IS USED IN COUNTERTERRORISM?

USDOJ… HAVE YOU TRAINED FEDERAL AGENCIES? FBI… WHERE WAS FA/IM© “FORENSIC ACCOUNTING/INVESTIGATION METHODOLOGY©” FIRST PUBLISHED? We wrote “Bulletin” for USDOJ

8

Selected Valuation/Forensic Accounting Cases:

alter ego: Forest products, services businesses, merger & acquisition Anti-trust: Forest products Bankruptcy dismissal (Chapter 13): Health care Beach of contract: Manufacturing, distribution, health care, banking, transportation Copyright: Art work, publications ESOPs, 401(k) share redemption: Dealerships, manufacturing Estate 706: manufacturing, distribution, construction, raw land, electronics, apartments Forensic accounting: Civil and criminal; private sector, public sector Fraud: Civil and criminal; private sector, public sector Fraudulent conveyance/transfer: Health clubs, finish carpentry Gifting 709: Securities, real property (residential/commercial) Information technology: Software, hardware Internet companies: B2B, B2C ISOs/ESOs: Black-Scholes, lattice/binomial Lending/Financing: Banks, borrowers Lost profits: Construction, manufacturing, distribution Marital Dissolution: Equitable distribution, community property Merger/Acquisition: Pre-transaction and post-transaction analysis Patent: Reasonable royalty, et al Public Sector: Jail Costing/Pricing Study, Public Funds Mismanagement Solvency/Insolvency: Wholesale distribution, agricultural Trademark; Trade Dress: Specialized tools Trade Secrets: Cell phone software

: Health care. Beach of contract: Manufacturing, distribution, health care, banking, transportation. Copyright: Art work, publications. ESOPs, 401(k) share redemption: Dealerships, manufacturing. Estate 706: manufacturing, distribution, construction, raw land, electronics, apartments. Forensic accounting: Civil and criminal; private sector, public sector. Fraud: Civil and criminal; private sector, public sector. Fraudulent conveyance/transfer: Health clubs, finish carpentry. Gifting 709: Securities, real property (residential/commercial) Information technology: Software, hardware. Internet companies: B2B, B2C. ISOs/ESOs: Black-Scholes, lattice/binomial. Lending/Financing: Banks, borrowers. Lost profits: Construction, manufacturing, distribution. Marital Dissolution: Equitable distribution, community property. Merger/Acquisition: Pre-transaction and post-transaction analysis. Patent: Reasonable royalty, et al. Public Sector: Jail Costing/Pricing Study, Public Funds Mismanagement. Solvency/Insolvency: Wholesale distribution, agricultural. Trademark; Trade Dress: Specialized tools. Trade Secrets: Cell phone software.")

9

Forensic accounting defined…

The art & science of investigating people & money.© Forensic Accounting Academy© - April 2007 (financialforensics® Newsletter, September 1993)

")

10

AICPA Latest “Definition”

“generally involving the application of specialized knowledge and investigative skills possessed by CPAs to collect, analyze, and evaluate evidential matter and to interpret and communicate findings in the courtroom, boardroom, or other legal or administrative venues.” CPA Expert, Winter 2009, page 2

11

Forensic Accounting – Foundational Discipline

Economic Damages Tax PI, WD Performance Auditing Forensic Accounting Audit/Review/Comp Valuation Internal Audit Fraud

12

Everything that you see/hear today is:

Public record And/or Disguised

13

How does forensic accounting affect valuation?

14

How does forensic accounting affect valuation, attest, litigation, tax, fraud, et al? i.e. virtually ALL of your practice areas

15

Forensic Accounting & Valuation, et al…

Your clients’ expectations reach beyond your core expertise whether auditing, tax, valuation or litigation. Such expectations are no surprise since forensic accounting is now a household term. Thanks to extensive media coverage of several high profile corporate collapses and showcasing of forensic accounting specialists the public “thinks” that all CPAs have such expertise. Consequently, the public, i.e. your clients “think” that you deliver professional services from a foundation of forensic accounting. The accounting profession has reinforced such perceptions despite failing to provide guidance. Specifically, virtually every accounting periodical devotes space to forensic accounting and related subjects. Further, all CPE providers offer various courses on the subject or some derivative. Finally, accounting graduates are increasingly attracted to firms offering such services. Paradoxically, the accounting profession has yet to embrace (or even offer) a cogent, comprehensive, forensic accounting methodology comprising the forensic tools by which accountants can guide and refine their forensic accounting craft. Likewise, defending one’s core expertise continues to be more challenging without independently codified benchmarks.

a cogent, comprehensive, forensic accounting methodology comprising the forensic tools by which accountants can guide and refine their forensic accounting craft. Likewise, defending one’s core expertise continues to be more challenging without independently codified benchmarks.")

16

How does forensic accounting affect valuation?

Does valuation require: Veracity or reliability of the financial statements Financial analysis, e.g. ratios, trending? Designed by lenders; lack cash & forensic tests; unfamiliar to valuators Benchmarking against subject, peers? Normalizations; (do you analyze before & after?) Do you normalize with journal entries? Earnings projections/estimations - feasible? Tested against cash generated? Economic benefit stream reliability? Discount/capitalization rate development? Management assessment/performance? Facilities and operations walkthrough? Guideline company comparison/selection? Market transactions statistical “fit” Secondary adjustments, e.g. DLOM, DLOC, Key Customer? Etc.?

Do you normalize with journal entries Earnings projections/estimations - feasible Tested against cash generated Economic benefit stream reliability Discount/capitalization rate development Management assessment/performance Facilities and operations walkthrough Guideline company comparison/selection Market transactions statistical fit Secondary adjustments, e.g. DLOM, DLOC, Key Customer Etc.")

17

Today – Session Description…

Will preview in reverse order Court cases re forensic accounting Applied forensic techniques, e.g. guidelines Accelerate (throughout) 17

17.")

18

Today – Session Description…

Will preview in reverse order Court cases re forensic accounting Applied forensic techniques, e.g. guidelines Accelerate (throughout) 18

18.")

19

Example Court Cases – Forensic Accounting

In re Coram Healthcare Corp., 2004 Bankr. LEXIS 1516 (Oct. 3, 2004) Valuation issue was Debtors’ value which would determine whether Trustee’s plan was “fair and equitable.” Both parties experts’ used same methodologies, guideline public company analysis, guideline transaction analysis, and DCF – but conclusions disparate Court noted: “Big 4 firm [for equity committee] and investment banker team [for trustee] included different assets in reaching their valuation conclusions, attached different weights to the three valuation methodologies, and took different positions regarding management’s projections.” Equity Committee argued: investment banking team deflated Debtors’ value by relying on conservative projections because of flawed assumption and errors investment banking team did not conduct independent review of projections consistency or actual performance Big 4 valuation used “upside projections” including EBITDA adjustments deemed to be irregular, including growth, cash flow and management’s established reserves; total adjustments increased EBITDA by 40% Court: “Although valuations are subjective, (sic) there are proper and improper methods of performing a valuation.” “[Big 4 firm] took aggressive and optimistic views regarding the valuation and strength of the Debtors. Therefore, we do not find that the [Big 4 firm] valuation is an accurate reflection of the Debtors’ value.”

Valuation issue was Debtors’ value which would determine whether Trustee’s plan was fair and equitable. Both parties experts’ used same methodologies, guideline public company analysis, guideline transaction analysis, and DCF – but conclusions disparate. Court noted: Big 4 firm [for equity committee] and investment banker team [for trustee] included different assets in reaching their valuation conclusions, attached different weights to the three valuation methodologies, and took different positions regarding management’s projections. Equity Committee argued: investment banking team deflated Debtors’ value by relying on conservative projections because of flawed assumption and errors. investment banking team did not conduct independent review of projections consistency or actual performance. Big 4 valuation used upside projections including EBITDA adjustments deemed to be irregular, including growth, cash flow and management’s established reserves; total adjustments increased EBITDA by 40% Court: Although valuations are subjective, (sic) there are proper and improper methods of performing a valuation. [Big 4 firm] took aggressive and optimistic views regarding the valuation and strength of the Debtors. Therefore, we do not find that the [Big 4 firm] valuation is an accurate reflection of the Debtors’ value.")

20

Example Court Cases – Forensic Accounting

Susan Fixel, Inc. v. Rosenthal & Rosenthal, Inc., 2005 Fla. App. LEXIS 1101 (Feb. 1, 2006) Claims for breach of fiduciary duty and negligent misrepresentation – total loss Expert calculated damages with client-prepared revenue and cash flow projections Court: “[expert] never verified those projections nor prepared his own.” Court: “…too speculative…” Court: expert made critical error in date of valuation; 1 year prior to damages date Court: excluded his testimony at trial Company argued while lost profits may require more evidence, a market valuation could rely on forecasts Court: disagreed – “It is as inappropriate to use purely speculative forecasts of future revenue to determine the market value of a business as it is to use such speculative forecasts in determining future lost profits.” Appeals Court: Affirmed expert exclusion as unreliable when expert used improper date and relied on speculative income projections

Claims for breach of fiduciary duty and negligent misrepresentation – total loss. Expert calculated damages with client-prepared revenue and cash flow projections. Court: [expert] never verified those projections nor prepared his own. Court: …too speculative… Court: expert made critical error in date of valuation; 1 year prior to damages date. Court: excluded his testimony at trial. Company argued while lost profits may require more evidence, a market valuation could rely on forecasts. Court: disagreed – It is as inappropriate to use purely speculative forecasts of future revenue to determine the market value of a business as it is to use such speculative forecasts in determining future lost profits. Appeals Court: Affirmed expert exclusion as unreliable when expert used improper date and relied on speculative income projections.")

21

Example Court Cases – Forensic Accounting

In re Nellson Nutraceutical, 2007 Bankr. LEXIS 99 (January 18, 2007) Chapter 11 case; private manufacturer of nutrition bars and supplements Expert learned after-the-fact that management’s long-range financial plans did not represent their “best and most honest thinking.” Principal equity holders “ needed” a “value” exceeding $365,000,000 Principal equity holders screened valuation analysts to pre-determine their methodologies Investors & attorneys sent selected expert values to be attributed to growth plans Privately and via discussed how to “figure out a way” expert could assist investors Investors pushed through a “puffed up” business plan for debtors Plan inflated revenues/EBITDA projections, ignored price compressions… … ignored increased market competition, eliminated “millions” of CapEx Court: “In sum, [the investors] utilized [their] control over [the debtors] to manipulate both the business planning and valuation process to come up with an artificially inflated enterprise value… to claim some residual value for their existing equity position. There is no other credible interpretation of the evidence before the Court.” Court specifically exonerated three experts All three testified that there results would require reduction to reflect flawed projections One unable to recite the Gordon Growth model on cross examination Debtors’ expert: Expert sent draft DCF analysis that did not reach desired equity During telecon Board convinced appraiser to use CapEx methodology One week later, appraiser sent Board “new” report using CapEx methodology Court reached its own conclusion after “adjusting” experts’ results per manipulation

Chapter 11 case; private manufacturer of nutrition bars and supplements. Expert learned after-the-fact that management’s long-range financial plans did not represent their best and most honest thinking. Principal equity holders needed a value exceeding $365,000,000. Principal equity holders screened valuation analysts to pre-determine their methodologies. Investors & attorneys sent selected expert values to be attributed to growth plans. Privately and via discussed how to figure out a way expert could assist investors. Investors pushed through a puffed up business plan for debtors. Plan inflated revenues/EBITDA projections, ignored price compressions… … ignored increased market competition, eliminated millions of CapEx. Court: In sum, [the investors] utilized [their] control over [the debtors] to manipulate both the business planning and valuation process to come up with an artificially inflated enterprise value… to claim some residual value for their existing equity position. There is no other credible interpretation of the evidence before the Court. Court specifically exonerated three experts. All three testified that there results would require reduction to reflect flawed projections. One unable to recite the Gordon Growth model on cross examination. Debtors’ expert: Expert sent draft DCF analysis that did not reach desired equity. During telecon Board convinced appraiser to use CapEx methodology. One week later, appraiser sent Board new report using CapEx methodology. Court reached its own conclusion after adjusting experts’ results per manipulation.")

22

Example Court Cases – Forensic Accounting

Aukeman v. Aukeman, 2007 Mich. App. LEXIS 1524 (June 12, 2007) Husband/owner testified weekly business sales averaged $58,000 with slight growth His expert used the numbers to value the three grocery stores at $1.53 million Wife’s expert used sales projections husband/owner used to obtain financing Her expert used weekly sales of $122,000 to value stores at $3 million+ Court: arrived at $2,225,000

Husband/owner testified weekly business sales averaged $58,000 with slight growth. His expert used the numbers to value the three grocery stores at $1.53 million. Wife’s expert used sales projections husband/owner used to obtain financing. Her expert used weekly sales of $122,000 to value stores at $3 million+ Court: arrived at $2,225,000.")

23

Example Court Cases – Forensic Accounting

Imaging International v. Hell Graphic Systems, Inc., 2007 N.Y. Misc. LEXIS 7368 (October 29, 2007) Business owner supplied most/all of financial information – previously convicted of tax fraud Expert initially calculates damages at $11 million, but revises to $4 million Printer purchased printing equipment that never worked properly, but kept using it 3 years later filed bankruptcy Jury awarded liability to printer who had sued for fraud Printer used expert for damages: Prepared two reports, i.e and 2005 – widely disparate results First used “ex post” approach, projecting revenue for 15 years from 1990, 6% annual growth: $11 million Second used “ex ante” with DCF and 12% growth rate + 4% premium: $4 million Expert assumed Hell Graphic’s fraud was sole cause of business’ failure For both reports, expert relied on information provided by the owner, without any independent review or access to underlying financial documentation Rebuttal expert found: Printer lost two major customers for reasons unrelated to allegation Owner refused to make staffing changes recommended by turnaround firm Owner found guilty of tax fraud two months before bankruptcy Industry shifted from analog to digital technology during relevant period Printer’s expert relied entirely on unverified data provided by owner who destroyed documents prior to trial Court found: Owner lacked credibility, therefore expert’s damage analysis lacked credibility Expert failed to explain variance in growth rates and failed to account for other possible causes of decline Failed to provide a preponderance of evidence

Business owner supplied most/all of financial information – previously convicted of tax fraud. Expert initially calculates damages at $11 million, but revises to $4 million. Printer purchased printing equipment that never worked properly, but kept using it. 3 years later filed bankruptcy. Jury awarded liability to printer who had sued for fraud. Printer used expert for damages: Prepared two reports, i.e and 2005 – widely disparate results. First used ex post approach, projecting revenue for 15 years from 1990, 6% annual growth: $11 million. Second used ex ante with DCF and 12% growth rate + 4% premium: $4 million. Expert assumed Hell Graphic’s fraud was sole cause of business’ failure. For both reports, expert relied on information provided by the owner, without any independent review or access to underlying financial documentation. Rebuttal expert found: Printer lost two major customers for reasons unrelated to allegation. Owner refused to make staffing changes recommended by turnaround firm. Owner found guilty of tax fraud two months before bankruptcy. Industry shifted from analog to digital technology during relevant period. Printer’s expert relied entirely on unverified data provided by owner who destroyed documents prior to trial. Court found: Owner lacked credibility, therefore expert’s damage analysis lacked credibility. Expert failed to explain variance in growth rates and failed to account for other possible causes of decline. Failed to provide a preponderance of evidence.")

24

Example Court Cases – Forensic Accounting

Mood v. Kronos Products, Inc., 2007 Tex. App. LEXIS 9243 (November 27, 2007) After 11 years exclusive agreement, both parties breached Kronos terminated without adhering to 60-day notice Mood counterclaimed for unauthorized sales to a Mood customer & breach damages At trial Mood presented no direct expert testimony on first claim, using instead: Kronos invoices for about 2 years Mood’s average gross annual sales to customer Kronos began selling to A general assertion that Mood’s “usual” profit margin was 20% Expert witness assertion that about 80% of Mood’s sales were from Kronos products Mood presented expert to calculate breach damages Attempted to predict lost profits over 10 years, i.e “Discrete revenue forecast” per recent year’s net income and applied 17% discount rate Jury awarded $1.1 million; judge vacated for a “take nothing” verdict Mood appealed; Kronos defended and Appeals Court agreed: Kronos’ gross sales to one customer insufficient evidence of lost profits; did not show same product/volume/price Gross sales “estimate” was based on “hypothetical statement by counsel at trial, i.e. “no evidence” of actual sales Mood’s claim of 20% gross margin (and 80% of overall sales from one product) lacked sufficient factual basis Mood’s expert relied on history for 10 year projection & did not differentiate between direct and consequential Expert failed to address loss of goodwill and/or going concern value resulting from the breach Court commented: “Put another way, [the expert’s] analysis did not specifically address the economic impact of the summary termination of the distributorship agreement.”

After 11 years exclusive agreement, both parties breached. Kronos terminated without adhering to 60-day notice. Mood counterclaimed for unauthorized sales to a Mood customer & breach damages. At trial Mood presented no direct expert testimony on first claim, using instead: Kronos invoices for about 2 years. Mood’s average gross annual sales to customer Kronos began selling to. A general assertion that Mood’s usual profit margin was 20% Expert witness assertion that about 80% of Mood’s sales were from Kronos products. Mood presented expert to calculate breach damages. Attempted to predict lost profits over 10 years, i.e Discrete revenue forecast per recent year’s net income and applied 17% discount rate. Jury awarded $1.1 million; judge vacated for a take nothing verdict. Mood appealed; Kronos defended and Appeals Court agreed: Kronos’ gross sales to one customer insufficient evidence of lost profits; did not show same product/volume/price. Gross sales estimate was based on hypothetical statement by counsel at trial, i.e. no evidence of actual sales. Mood’s claim of 20% gross margin (and 80% of overall sales from one product) lacked sufficient factual basis. Mood’s expert relied on history for 10 year projection & did not differentiate between direct and consequential. Expert failed to address loss of goodwill and/or going concern value resulting from the breach. Court commented: Put another way, [the expert’s] analysis did not specifically address the economic impact of the summary termination of the distributorship agreement.")

25

Example Court Cases – Forensic Accounting

Derby v. Comm’r, 2008 WL (U.S. Tax Ct.) (Feb. 28, 2008) Northern California physicians sold their practice to a non-profit medical foundation in 1994 To maintain professional autonomy physicians refused to sign non-compete Foundation did not want to pay for goodwill, and wanted to avoid kick-back laws Attorney suggested donating intangible value to foundation as charitable donation National valuation firm derived intangible result and “certification of appraisal” to each Allocation formula derived by one physician used for each personal tax return After IRS audit 3rd appraiser enlisted who used physician’s allocation formula Appraiser adopted physician’s allocation formula Tax Court cited various appraiser deficiencies: Failed to distinguish between personal and professional goodwill Failed to account for non-compete Adopted physician formula without any independent analysis Ignored physician access bonus

(Feb. 28, 2008) Northern California physicians sold their practice to a non-profit medical foundation in To maintain professional autonomy physicians refused to sign non-compete. Foundation did not want to pay for goodwill, and wanted to avoid kick-back laws. Attorney suggested donating intangible value to foundation as charitable donation. National valuation firm derived intangible result and certification of appraisal to each. Allocation formula derived by one physician used for each personal tax return. After IRS audit 3rd appraiser enlisted who used physician’s allocation formula. Appraiser adopted physician’s allocation formula. Tax Court cited various appraiser deficiencies: Failed to distinguish between personal and professional goodwill. Failed to account for non-compete. Adopted physician formula without any independent analysis. Ignored physician access bonus.")

26

Example Court Cases – Forensic Accounting

Structural Polymer Group, Ltd. V. Zoltek Corp., 2008 WL (8th Cir.) (Oct. 8, 2008) Plaintiff contracted with defendant for all their carbon fiber needs for 10 years, subject to certain limitations Alleged breach in years 5 & 6 Plaintiff sought damages years 5 & 6 and remaining 4 years Plaintiff’s expert relied “only” on Discussions with management Management summaries Internal budgets Projected sales compared to actual purchases Defendant’s annual report Defendant’s depositions & CEO statement “But for” case subtracting variable costs & then-market price Applied to plaintiff’s 18-month gross profit margin Jury’s findings for plaintiff upheld in appeal

(Oct. 8, 2008) Plaintiff contracted with defendant for all their carbon fiber needs for 10 years, subject to certain limitations. Alleged breach in years 5 & 6. Plaintiff sought damages years 5 & 6 and remaining 4 years. Plaintiff’s expert relied only on. Discussions with management. Management summaries. Internal budgets. Projected sales compared to actual purchases. Defendant’s annual report. Defendant’s depositions & CEO statement. But for case subtracting variable costs & then-market price. Applied to plaintiff’s 18-month gross profit margin. Jury’s findings for plaintiff upheld in appeal.")

27

Example Court Cases – Forensic Accounting

Fluor Enterprises, Inc. v. Conex International Corp WL (Tex. App.) (Dec. 18, 2008) Petrochemical company hired mechanical contractor & Fluor Enterprises, Inc. At completion company failed to pay about $2 million to contractor Contractor sued Fluor for “business disparagement” and “interference” Jury awarded contractor $98 million; Fluor appealed Contractor used economics professor for damages Focused only on lost profits, not causation Professor apparently did not consider actual contracts company awarded contractor 5-year post assignment period Professor’s other problems included: Downturn in refinery business for the relevant period Not familiar with “normal” profit margin for the industry Did not analyze job cost analysis Did not include overhead Incorporated a contract that expired 3 years prior to initial project Failed to apply his methodology consistently and with objectivity Averaged profit margins but not expenses and costs Court commented: “…based his opinion of lost future profits on past performance only when it benefitted [the contractor.” “In other words, [the expert] provides no evidence of specific lost sales..,” “Thus, he did not supply one complete calculation, but provided computations based on different methods of calculation.”

(Dec. 18, 2008) Petrochemical company hired mechanical contractor & Fluor Enterprises, Inc. At completion company failed to pay about $2 million to contractor. Contractor sued Fluor for business disparagement and interference Jury awarded contractor $98 million; Fluor appealed. Contractor used economics professor for damages. Focused only on lost profits, not causation. Professor apparently did not consider actual contracts company awarded contractor. 5-year post assignment period. Professor’s other problems included: Downturn in refinery business for the relevant period. Not familiar with normal profit margin for the industry. Did not analyze job cost analysis. Did not include overhead. Incorporated a contract that expired 3 years prior to initial project. Failed to apply his methodology consistently and with objectivity. Averaged profit margins but not expenses and costs. Court commented: …based his opinion of lost future profits on past performance only when it benefitted [the contractor. In other words, [the expert] provides no evidence of specific lost sales.., Thus, he did not supply one complete calculation, but provided computations based on different methods of calculation.")

28

Today – Session Description…

Will preview in reverse order Court cases re forensic accounting Applied forensic techniques, e.g. guidelines Accelerate (throughout) 28

28.")

29

Cookies on the bottom shelf…

30

“Covert” Forensic Tools

Deposition Matrix© Valuation Report Card©

36

Statistics “hacks”

38

Deposition Matrix©

39

“Valuation Report Card©”

40

Gap Detection (con’t)

")

41

How/Where do you start/stay?

42

Pictures…

44

Pictures…

45

Pictures…

46

Is this cash “lockbox” secure?

47

Finding the bodies…

48

Today – Session Description…

Will preview in reverse order Court cases re forensic accounting Applied forensic techniques, e.g. guidelines Accelerate (throughout) 48

48.")

49

You May Want To Receive…

Sarbanes-Oxley (SOX) Compliance Journal “Financial Hieroglyphics – The Numbers “Speak” to Me” American Journal of Family Law “Is The Moneyed Spouse Lying About The Money?©” Value Examiner 2008 Update: Marketability Discounts - A Comprehensive Analysis National Litigation Consultants’ Review “Valuation Forensics”

Compliance Journal. Financial Hieroglyphics – The Numbers Speak to Me American Journal of Family Law. Is The Moneyed Spouse Lying About The Money © Value Examiner Update: Marketability Discounts - A Comprehensive Analysis. National Litigation Consultants’ Review. Valuation Forensics")

50

25+ “New” forensic accounting/valuation techniques…

Full-and-False Inclusion Genogram TATA/TARTA/TITA/TDTA/TAPTA AQI Behavior Detection FACS Styleometry ICE©/SCORE© Link Analysis Articulated Cash Flow Dechow-Dichev Techniques Timeline Analysis IRS Formal Indirect Methods A(5) “Cash-T” (Modified) Net Worth Bank Deposits & Cash Expenditures Markup Unit & Volume Expectations Attributes Gap Detection Proof-of-Cash Deposition Matrix Entity(s) Chart Lev-Thiagarajan Techniques Damages Report Card Digital Analysis CATA/CRO MSSP

Cash-T (Modified) Net Worth. Bank Deposits & Cash Expenditures. Markup. Unit & Volume. Expectations Attributes. Gap Detection. Proof-of-Cash. Deposition Matrix. Entity(s) Chart. Lev-Thiagarajan Techniques. Damages Report Card. Digital Analysis. CATA/CRO. MSSP.")

51

The 250-300 techniques require a methodology

52

What Is A Methodology? Basic Example – for the Cops

A way of doing things, a process… Criminal Investigation 7-Step Method Others Forensic Accounting Investigation Combined Criminal/Forensic Accounting

53

“ICE©” C - Control E - External I - Internal

54

“ICE©” Closely-Held Business Example

C – Control Bank Statements E – External Tax Returns Attest Reports I – Internal PBC Financials Operating Reports

55

“ICE©” C – Control E – External I – Internal Bank Statements

Proof-of-Cash Timing Non-Cash E – External Tax Returns Attest Reports I – Internal PBC Financials Operating Reports

56

Why Isn’t ICE©” Sufficient?

You must be: “Thinking Outside the… Triangle©” That is where SCORE© comes in

57

“SCORE©” Flow of $ and/or Units Stakeholder In Out S – Suppliers U $

C – Customers O – “Owners” Investors/Lenders R – Regulators n/a E – Employees

58

What Is A Methodology? Forensic Accounting Example

A way of doing things, a process… Criminal Investigation 7-Step Method Others Forensic Accounting Investigation Combined Criminal/Forensic Accounting

59

What Can You Expect This Week (Today)?

Uncertainty… Vocabulary – a common language… VERY hard work… possible growth… Leave your ego at the door…

60

DATA COLLECTION AND ANALYSIS

Forensic Accounting/Investigation Methodology (FA/IM)© FOUNDATIONAL INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL Interviews & Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Identify parties to the case Correlate the matters of law Confirm technical capabilities Clear conflict Insure matching of expectations between counsel and facts and circumstances of matter Determine whether engaged as consultant or expert Prepare and secure engagement letter Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery Identification of all parties Specification of key timelines Privilege determination Agreement on standards References Deliverables AICPA/BVFLS Practice Aids Litigation Services Handbook, 4th & Cumulative Supplements NACVA Resources “Entity / Party Chart” Signed engagement letter Retainer

© FOUNDATIONAL. INTERPERSONAL. DATA COLLECTION AND ANALYSIS. TRIAL. Interviews. & Interrogation. Surveillance. -Electronic, Physical. Trial. Preparation. Assignment. Development. Scoping. Data. Collection. Confidential. Informants. Laboratory. Analysis. Analysis of. Transactions. Post- Assignment. Background. Research. Undercover. Testimony. & Exhibits. Purpose of Stage. Tasks to be Performed. Potential Issues. Identify parties to the case. Correlate the matters of law. Confirm technical capabilities. Clear conflict. Insure matching of expectations between counsel and facts and circumstances of matter. Determine whether engaged as consultant or expert. Prepare and secure engagement letter. Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery. Identification of all parties. Specification of key timelines. Privilege determination. Agreement on standards. References. Deliverables. AICPA/BVFLS Practice Aids. Litigation Services Handbook, 4th & Cumulative Supplements. NACVA Resources. Entity / Party Chart Signed engagement letter. Retainer.")

61

Contributing Authors and/or Instructors

Thomas F. Burrage CPA/ABV, CVA, DABFA Burrage & Johnson, CPA’s, LLC – Albuquerque, NM Darrell D. Dorrell, CPA/ABV, MBA, CVA, ASA, CMA, DABFA financialforensics® – Lake Oswego, OR Gregory A. Gadawski, CPA/ABV, CVA, CFE Katherine Heekin – JD, CFE The Heekin Law Firm – Portland, OR Dr. Diane A. Matthews, CPA, CFE Carlow University – Pittsburgh, PA Patricia A. Perzel, CPA, CVA, CFFA, CFD Perzel & Lara Forensic CPA’s, P.A. – Clearwater, FL Gabriel H. Shurek, Manager Gettry Marcus Stern & Lehrer, CPA, P.C. – Woodbury, NY Mark S. Warshavsky, CPA/ABV, MBA, CVA, CBA, CFE, DABFA, CFFA Paul E. Zikmund – MBA, MA, CFE, CFD Solomon Edwards Group, LLC – Philadelphia, PA

62

DATA COLLECTION AND ANALYSIS

Forensic Accounting/Investigation Methodology (FA/IM)© FOUNDATIONAL INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL Interviews& Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Identify parties to the case Correlate the matters of law Confirm technical capabilities Clear conflict - firm-wide database Insure matching of expectations between counsel and facts and circumstances of matter Determine whether engaged as consultant or expert Prepare and secure engagement letter & retainer Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery Identification of all parties Specification of key timelines Privilege determination Agreement on standards References Deliverables AICPA/BVFLS Practice Aids Litigation Services Handbook, 4th & Cumulative Supplements NACVA Resources Conflict Resolution Form “Entity / Party Chart” Signed engagement letter & retainer Retainer

© FOUNDATIONAL. INTERPERSONAL. DATA COLLECTION AND ANALYSIS. TRIAL. Interviews& Interrogation. Surveillance. -Electronic, Physical. Trial. Preparation. Assignment. Development. Scoping. Data. Collection. Confidential. Informants. Laboratory. Analysis. Analysis of. Transactions. Post- Assignment. Background. Research. Undercover. Testimony. & Exhibits. Purpose of Stage. Tasks to be Performed. Potential Issues. Identify parties to the case. Correlate the matters of law. Confirm technical capabilities. Clear conflict - firm-wide database. Insure matching of expectations between counsel and facts and circumstances of matter. Determine whether engaged as consultant or expert. Prepare and secure engagement letter & retainer. Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery. Identification of all parties. Specification of key timelines. Privilege determination. Agreement on standards. References. Deliverables. AICPA/BVFLS Practice Aids. Litigation Services Handbook, 4th & Cumulative Supplements. NACVA Resources. Conflict Resolution Form. Entity / Party Chart Signed engagement letter & retainer. Retainer.")

63

DATA COLLECTION AND ANALYSIS

Forensic Accounting/Investigation Methodology (FA/IM)© FOUNDATIONAL INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL Interviews & Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Identify parties to the case Correlate the matters of law Confirm technical capabilities Clear conflict - firm-wide database Insure matching of expectations between counsel and facts and circumstances of matter Determine whether engaged as consultant or expert Prepare and secure engagement letter & retainer Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery Identification of all parties Specification of key timelines Privilege determination Agreement on standards References Deliverables AICPA/BVFLS Practice Aids Litigation Services Handbook, 4th & Cumulative Supplements NACVA Resources Conflict Resolution Form “Entity / Party Chart” Signed engagement letter & retainer Retainer

© FOUNDATIONAL. INTERPERSONAL. DATA COLLECTION AND ANALYSIS. TRIAL. Interviews. & Interrogation. Surveillance. -Electronic, Physical. Trial. Preparation. Assignment. Development. Scoping. Data. Collection. Confidential. Informants. Laboratory. Analysis. Analysis of. Transactions. Post- Assignment. Background. Research. Undercover. Testimony. & Exhibits. Purpose of Stage. Tasks to be Performed. Potential Issues. Identify parties to the case. Correlate the matters of law. Confirm technical capabilities. Clear conflict - firm-wide database. Insure matching of expectations between counsel and facts and circumstances of matter. Determine whether engaged as consultant or expert. Prepare and secure engagement letter & retainer. Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery. Identification of all parties. Specification of key timelines. Privilege determination. Agreement on standards. References. Deliverables. AICPA/BVFLS Practice Aids. Litigation Services Handbook, 4th & Cumulative Supplements. NACVA Resources. Conflict Resolution Form. Entity / Party Chart Signed engagement letter & retainer. Retainer.")

64

DATA COLLECTION AND ANALYSIS

Forensic Accounting/Investigation Methodology (FA/IM)© FOUNDATIONAL INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL Interviews & Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Identify parties to the case Correlate the matters of law Confirm technical capabilities Clear conflict - firm-wide database Insure matching of expectations between counsel and facts and circumstances of matter Determine whether engaged as consultant or expert Prepare and secure engagement letter & retainer Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery Identification of all parties Specification of key timelines Privilege determination Agreement on standards References Deliverables AICPA/BVFLS Practice Aids Litigation Services Handbook, 4th & Cumulative Supplements NACVA Resources Conflict Resolution Form “Entity / Party Chart” Signed engagement letter & retainer Retainer

© FOUNDATIONAL. INTERPERSONAL. DATA COLLECTION AND ANALYSIS. TRIAL. Interviews. & Interrogation. Surveillance. -Electronic, Physical. Trial. Preparation. Assignment. Development. Scoping. Data. Collection. Confidential. Informants. Laboratory. Analysis. Analysis of. Transactions. Post- Assignment. Background. Research. Undercover. Testimony. & Exhibits. Purpose of Stage. Tasks to be Performed. Potential Issues. Identify parties to the case. Correlate the matters of law. Confirm technical capabilities. Clear conflict - firm-wide database. Insure matching of expectations between counsel and facts and circumstances of matter. Determine whether engaged as consultant or expert. Prepare and secure engagement letter & retainer. Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery. Identification of all parties. Specification of key timelines. Privilege determination. Agreement on standards. References. Deliverables. AICPA/BVFLS Practice Aids. Litigation Services Handbook, 4th & Cumulative Supplements. NACVA Resources. Conflict Resolution Form. Entity / Party Chart Signed engagement letter & retainer. Retainer.")

65

DATA COLLECTION AND ANALYSIS

Forensic Accounting/Investigation Methodology (FA/IM)© FOUNDATIONAL INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL Interviews & Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Identify parties to the case Correlate the matters of law Confirm technical capabilities Clear conflict - firm-wide database Insure matching of expectations between counsel and facts and circumstances of matter Determine whether engaged as consultant or expert Prepare and secure engagement letter & retainer Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery Identification of all parties Specification of key timelines Privilege determination Agreement on standards References Deliverables AICPA/BVFLS Practice Aids Litigation Services Handbook, 4th & Cumulative Supplements NACVA Resources Conflict Resolution Form “Entity / Party Chart” Signed engagement letter & retainer Retainer

© FOUNDATIONAL. INTERPERSONAL. DATA COLLECTION AND ANALYSIS. TRIAL. Interviews. & Interrogation. Surveillance. -Electronic, Physical. Trial. Preparation. Assignment. Development. Scoping. Data. Collection. Confidential. Informants. Laboratory. Analysis. Analysis of. Transactions. Post- Assignment. Background. Research. Undercover. Testimony. & Exhibits. Purpose of Stage. Tasks to be Performed. Potential Issues. Identify parties to the case. Correlate the matters of law. Confirm technical capabilities. Clear conflict - firm-wide database. Insure matching of expectations between counsel and facts and circumstances of matter. Determine whether engaged as consultant or expert. Prepare and secure engagement letter & retainer. Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery. Identification of all parties. Specification of key timelines. Privilege determination. Agreement on standards. References. Deliverables. AICPA/BVFLS Practice Aids. Litigation Services Handbook, 4th & Cumulative Supplements. NACVA Resources. Conflict Resolution Form. Entity / Party Chart Signed engagement letter & retainer. Retainer.")

66

DATA COLLECTION AND ANALYSIS

Forensic Accounting/Investigation Methodology (FA/IM)© FOUNDATIONAL INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL Interviews & Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Identify parties to the case Correlate the matters of law Confirm technical capabilities Clear conflict - firm-wide database Insure matching of expectations between counsel and facts and circumstances of matter Determine whether engaged as consultant or expert Prepare and secure engagement letter & retainer Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery Identification of all parties Specification of key timelines Privilege determination Agreement on standards References Deliverables AICPA/BVFLS Practice Aids Litigation Services Handbook, 4th & Cumulative Supplements NACVA Resources Conflict Resolution Form “Entity / Party Chart” Signed engagement letter & retainer Retainer

© FOUNDATIONAL. INTERPERSONAL. DATA COLLECTION AND ANALYSIS. TRIAL. Interviews. & Interrogation. Surveillance. -Electronic, Physical. Trial. Preparation. Assignment. Development. Scoping. Data. Collection. Confidential. Informants. Laboratory. Analysis. Analysis of. Transactions. Post- Assignment. Background. Research. Undercover. Testimony. & Exhibits. Purpose of Stage. Tasks to be Performed. Potential Issues. Identify parties to the case. Correlate the matters of law. Confirm technical capabilities. Clear conflict - firm-wide database. Insure matching of expectations between counsel and facts and circumstances of matter. Determine whether engaged as consultant or expert. Prepare and secure engagement letter & retainer. Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery. Identification of all parties. Specification of key timelines. Privilege determination. Agreement on standards. References. Deliverables. AICPA/BVFLS Practice Aids. Litigation Services Handbook, 4th & Cumulative Supplements. NACVA Resources. Conflict Resolution Form. Entity / Party Chart Signed engagement letter & retainer. Retainer.")

67

DATA COLLECTION AND ANALYSIS

Forensic Accounting/Investigation Methodology (FA/IM)© FOUNDATIONAL INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL Interviews & Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Identify parties to the case Correlate the matters of law Confirm technical capabilities Clear conflict - firm-wide database Insure matching of expectations between counsel and facts and circumstances of matter Determine whether engaged as consultant or expert Prepare and secure engagement letter & retainer Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery Identification of all parties Specification of key timelines Privilege determination Agreement on standards References Deliverables AICPA/BVFLS Practice Aids Litigation Services Handbook, 4th & Cumulative Supplements NACVA Resources Conflict Resolution Form “Entity / Party Chart” Signed engagement letter & retainer Retainer

© FOUNDATIONAL. INTERPERSONAL. DATA COLLECTION AND ANALYSIS. TRIAL. Interviews. & Interrogation. Surveillance. -Electronic, Physical. Trial. Preparation. Assignment. Development. Scoping. Data. Collection. Confidential. Informants. Laboratory. Analysis. Analysis of. Transactions. Post- Assignment. Background. Research. Undercover. Testimony. & Exhibits. Purpose of Stage. Tasks to be Performed. Potential Issues. Identify parties to the case. Correlate the matters of law. Confirm technical capabilities. Clear conflict - firm-wide database. Insure matching of expectations between counsel and facts and circumstances of matter. Determine whether engaged as consultant or expert. Prepare and secure engagement letter & retainer. Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery. Identification of all parties. Specification of key timelines. Privilege determination. Agreement on standards. References. Deliverables. AICPA/BVFLS Practice Aids. Litigation Services Handbook, 4th & Cumulative Supplements. NACVA Resources. Conflict Resolution Form. Entity / Party Chart Signed engagement letter & retainer. Retainer.")

68

DATA COLLECTION AND ANALYSIS

Forensic Accounting/Investigation Methodology (FA/IM)© FOUNDATIONAL INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL Interviews & Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Identify parties to the case Correlate the matters of law Confirm technical capabilities Clear conflict - firm-wide database Insure matching of expectations between counsel and facts and circumstances of matter Determine whether engaged as consultant or expert Prepare and secure engagement letter & retainer Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery Identification of all parties Specification of key timelines Privilege determination Agreement on standards References Deliverables AICPA/BVFLS Practice Aids Litigation Services Handbook, 4th & Cumulative Supplements NACVA Resources “Entity / Party Chart” Signed engagement letter & retainer Retainer

© FOUNDATIONAL. INTERPERSONAL. DATA COLLECTION AND ANALYSIS. TRIAL. Interviews. & Interrogation. Surveillance. -Electronic, Physical. Trial. Preparation. Assignment. Development. Scoping. Data. Collection. Confidential. Informants. Laboratory. Analysis. Analysis of. Transactions. Post- Assignment. Background. Research. Undercover. Testimony. & Exhibits. Purpose of Stage. Tasks to be Performed. Potential Issues. Identify parties to the case. Correlate the matters of law. Confirm technical capabilities. Clear conflict - firm-wide database. Insure matching of expectations between counsel and facts and circumstances of matter. Determine whether engaged as consultant or expert. Prepare and secure engagement letter & retainer. Establish concrete timelines, e.g. discovery cutoff, report submittal, etc. Establish counsel communications protocol, e.g. whether/how subject to discovery. Identification of all parties. Specification of key timelines. Privilege determination. Agreement on standards. References. Deliverables. AICPA/BVFLS Practice Aids. Litigation Services Handbook, 4th & Cumulative Supplements. NACVA Resources. Entity / Party Chart Signed engagement letter & retainer. Retainer.")

69

Forensic Accounting/Investigation Methodology (FA/IM)©

INTERPERSONAL DATA COLLECTION AND ANALYSIS TRIAL/REPORTS FOUNDATIONAL Interviews & Interrogation Surveillance -Electronic, Physical Trial Preparation Assignment Development Scoping Data Collection Confidential Informants Laboratory Analysis Analysis of Transactions Post- Assignment Background Research Undercover Testimony & Exhibits Purpose of Stage Tasks to be Performed Potential Issues Obtain sufficient relevant data to provide credible evidence Summarize and analyze the findings of all deliverables and observations Identify any missing information or “gaps” DRAFT the Forensic Accountant’s Report TASKS Common-sizing Horizontal analysis Vertical analysis Statement analysis (written) Accept-reject testing Stratified mean-per-unit (MPU) Attributes sampling Link Analysis/Root Tracing Item Listing Forensic Accountant’s Report does not support the indictment Additional techniques do not substantiate missing gaps References Deliverables Bragg, Steven M., Business Ratios and Formulas (Wiley) Benford’s – IDEA software “Gap” Analysis Indictment Matrix WPN (words/pictures/numbers)

Accept-reject testing. Stratified mean-per-unit (MPU) Attributes sampling. Link Analysis/Root Tracing. Item Listing. Forensic Accountant’s Report does not support the indictment. Additional techniques do not substantiate missing gaps. References. Deliverables. Bragg, Steven M., Business Ratios and Formulas (Wiley) Benford’s – IDEA software. Gap Analysis. Indictment Matrix. WPN (words/pictures/numbers)")

70

Forensic Accounting – Foundational Discipline

Economic Damages Tax PI, WD Performance Auditing Forensic Accounting Audit/Review/Comp Valuation Internal Audit Fraud

71

Full-and-False-Inclusion

…the yellow crime scene tape of forensic accounting…

72

Chain of Custody Gaps in the chain or mishandling of evidence can damage a case Evidence may still be admissible if it can be authenticated by an identifying feature, but a mistake in custody affects the weight of the evidence In fraud cases, maintaining custody is particularly significant for electronic evidence (concern regarding alteration) – hand-to-hand chain of custody detailing how it was stored and protected from alteration

– hand-to-hand chain of custody detailing how it was stored and protected from alteration.")

73

Genogram

74

Consolidated Operations

W W P W P W Fr W W P P P Fr W P Fr Red font – Family Fr – Friends since high school P – “Pajama party” participant W – Worked together many years

75

Entity Chart(s)

")

76

Timeline Analysis

77

Today – Session Description…

Will preview in reverse order Court cases re forensic accounting Applied forensic techniques, e.g. guidelines Accelerate (throughout) 77

77.")

78

Preliminary Analysis – “Surprises”

Shareholders’ Equity section Reconciliation yielded discrepancies Quarter-to Prior Year Quarter Changes Year-to-Year Changes

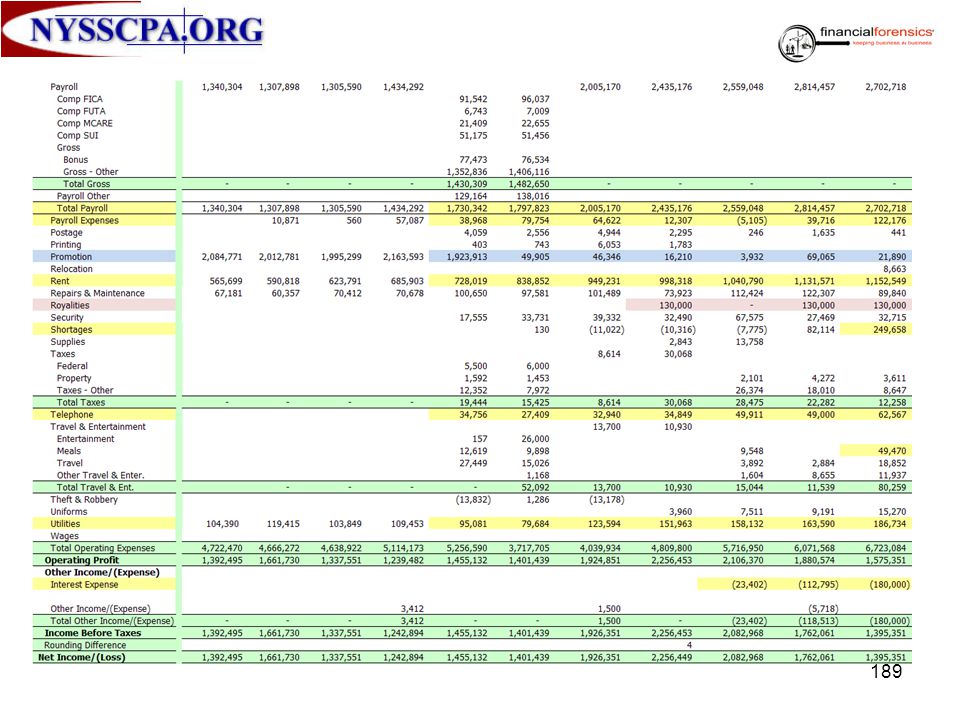

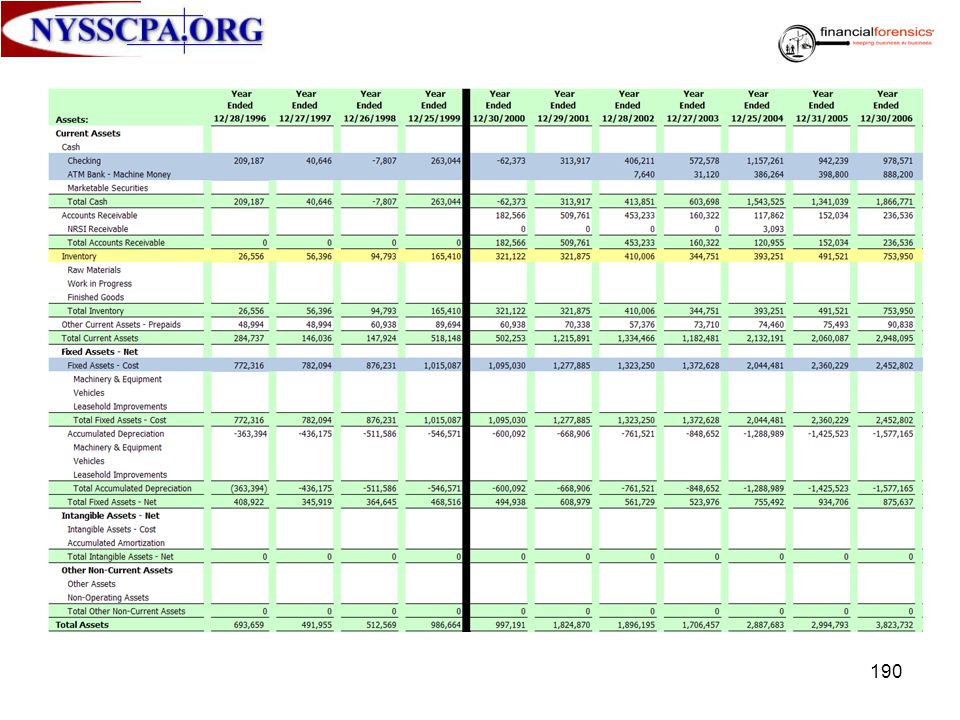

79

XYZ Historical Balance Sheets Source: Audited Financial Statements

Balance Sheet Conclusions: Large sums into “soft” assets “Hard” assets declined

80

XYZ Historical Income Statements Source: Audited Financial Statements

Income Statement Conclusions: Solid gross profit Very heavy debt load Heavy losses in entity investments Heavy debt restructuring Heavy losses in store open/close

81

XYZ Historical Cash Flow Statements Source: Audited Financial Statements

Cash Flow Statement Conclusions: Operating cash impacted 2003 Few fixed assets 2002 & 2003 Only financing outflow in 2002

82

Annual Financial Statement Indicators

83

Financial Ratios – Overall Assessment

84

Overall Financial Condition C-

Overall Scoring – Grade Balance Sheet C- Intangible assets not productive Inefficient use of long-term debt Income Statement B- Strong gross profit Heavy interest expense Expenses not managed Cash Flow Statement D Inefficient capital structure Overall Financial Condition C- Long-term to “fix”

85

Baseline Financials

86

“Traditional Ratios” Financials Reliable?

87

Forensic Tests - Simple

88

Earnings Manipulation Tests - Annual

Asset Quality Index Total Accruals to Total Assets Index Days’ Sales in Receivables Index – n/a Inventory Index Sales Growth Index Gross Margin Index

89

Earnings Manipulation Tests - Quarter

Comparison of Revenue & Gross Margin Asset Quality Index Total Accruals to Total Assets Index Days’ Sales in Receivables Index – n/a Inventory Index Sales Growth Index Gross Margin Index

90

Surprises in Shareholders’ Equity

91

Year-to-Year Discrepancies

92

Equity Declined in 2002

93

Long-Term Debt Increases

94

Other Non-Current Assets Increased

95

Net Intangible Assets Increased

96

“Soft” Assets Grew Dramatically

97

Large Sums into “Soft” Assets

98

Revenue-Producing Assets Declined

99

Large Swings in Net Income

100

Impact of Heavy Debt Load

101

Solid Gross Profit

102

Operating Expenses Increased

103

Revenues Increased

104

Cash Earned from Operations

105

Largest Operating Cash Impact

106

Cash Used for Investing

107

Cash In/Out for Financing

108

Only Cash Out in 2002

109

Significant Increase in 2003

110

Significant Increase in 2002

111

Pattern Contrary to Reported

112

2005 Contrary to Reported

113

Contrary to Common-Size

114

2005 Gross Profit “Spikes” Then Declines

115

“Normal” Is 1.0

116

Dramatic Variations in 2005

117

Cash Realization Ratio (CRO)

Operating Cash / Net Income.

118

Asset Quality Index (AQI)

(1-Current Assets t + PPE t / Total Assets t divided by: (1-Current Assets t -1 + PPE t -1 / Total Assets-1)

")

119

Depreciation Index (DI)

(Depreciation t-1+Net PPE t-1) / (Depreciation t +Net PPE t)

/ (Depreciation t +Net PPE t)")

120

SGA Expenses Index (SGAEI)

SGAEI t / Sales t SGAEI t-1 / Sales t-1

121

Good Co. or Bad Co.? - CRO

122

XYZ Quarterly

123

Good Co. or Bad Co.? - GMI

124

XYZ Quarterly

125

Good Co. or Bad Co.? - AQI

126

XYZ Quarterly

127

Good Co. or Bad Co.? - SGI

128

XYZ Quarterly

129

Good Co. or Bad Co.? - LI

130

XYZ Quarterly

131

Forensic Accounting – Foundational Discipline

Economic Damages Tax PI, WD Performance Auditing Forensic Accounting Audit/Review/Comp Valuation Internal Audit Fraud

132

Decompose the Cash Flows

133

Is Correlated Cash Flow Improving?

134

Cash Flow Correlation IBE - Income before extraordinary items and discontinued operations. CFO - Cash flow from operations. CI - Comprehensive income defined as the change in owners' equity plus dividends net of capital contributions. FCF - Free cash flow is measured by cash flow from operations (CFO) minus net capital expenditures plus net interest payments.

minus net capital. expenditures plus net interest payments.")

135

Today – Session Description…

Will preview in reverse order Court cases re forensic accounting Applied forensic techniques, e.g. guidelines Accelerate (throughout) 135

135.")

136

Where are the holes? What do you see?

Reconcile Equity Where are the holes? What do you see? 2004 2003 2002 2001 2000 1999 Beginning Shareholders' Equity 641,000 534,900 412,897 350,570 317,049 287,574 Net Income/(Loss) 768,398 508,400 467,138 267,377 27,797 29,475 Dividends Paid Common Stock (500,500) Dividends Paid Common Non-Voting Stock Dividends Paid Preferred Stock Common Stock Issued Common Non Voting Stock Issued 500,500 Treasury Stock Purchased (402,300) (367,050) (205,050) (27,797) Distributions to Shareholder (100,000) Foreign currency translation adj 5,500 Min. pension liability adj. Unreal gains on marketable sec Prior Period Adjustments Other Restatements, Net (298,632) Ending Shareholders' Equity 1,016,666 512,985

768, , , , , ,475. Dividends Paid Common Stock. (500,500) Dividends Paid Common Non-Voting Stock. Dividends Paid Preferred Stock. Common Stock Issued. Common Non Voting Stock Issued. 500,500. Treasury Stock Purchased. (402,300) (367,050) (205,050) (27,797) Distributions to Shareholder. (100,000) Foreign currency translation adj. 5,500 Min. pension liability adj. Unreal gains on marketable sec Prior Period Adjustments. Other Restatements, Net. (298,632) Ending Shareholders Equity. 1,016, ,985.")

137

Journal Entries to Normalize

The resultant impact of the normalizations is summarized by year below.

138

“Show Your Work”

139

“ICE©” C – Control E – External I – Internal Bank Statements

Proof-of-Cash Timing Non-Cash E – External Tax Returns Attest Reports I – Internal PBC Financials Operating Reports

140

Internal Revenue Service, Part 4 Chapter 10

FSAT – Financial Status Audit Techniques Financial Status Analysis Formal Indirect Methods Not precluded by books and records. See Lipsitz v. Commissioner, 21 T.C. 917 (1954)

")

141

When to Use Formal Indirect Methods

Financial Status Analysis – unbalanced Irregularities – books & records; weak internal controls Gross margin – significant changes; by period or peer group Unexplained deposits in bank accounts Cash deposits See “Inflation and Consumer Spending” Net worth increase – not supported

142

Financial Status Analysis

143

Formal Indirect Methods

Source & application of funds (IRM ) a.k.a. “Cash T” Analysis Bank Deposits & Cash Expenditures (IRM ) Markup Method (IRM ) Unit & Volume (IRM ) Net Worth (IRM )

a.k.a. Cash T Analysis. Bank Deposits & Cash Expenditures (IRM ) Markup Method (IRM ) Unit & Volume (IRM ) Net Worth (IRM )")

144

Formal Indirect Methods

Source & application of funds a.k.a. “Cash T” Analysis Bank Deposits & Cash Expenditures Markup Method Unit & Volume Net Worth

145

Source & Applications of Funds United States v. Johnson, 319 U. S

Uses subject’s cash flows to compare: All known expenditures Estimates personal living expenses All known receipts Takes into account: Net changes in assets & liabilities Non-deductible expenditures (for tax matters) Non-taxable receipts (for tax matters) If expenditures > receipts: unreported

Non-taxable receipts (for tax matters) If expenditures > receipts: unreported.")

146

Source & Applications of Funds

Typical uses Deductions/expenditures out of proportion Cash does not flow from a bank account Common use of cash – in or out

147

Source & Applications of Funds

Accrual impacts Beginning A/R shown on “debit” side i.e., collected during period Ending A/R shown on “credit” side i.e., effects a noncash income increase Beginning A/P shown on “credit” side i.e., current period cash out Ending A/P shown on “debit” side i.e., current period income reduction

148

Source & Application of Funds

149

“Cash T” Example

150

Formal Indirect Methods

Source & application of funds a.k.a. “Cash T” Analysis Bank Deposits & Cash Expenditures Markup Method Unit & Volume Net Worth

151

Bank Deposits & Cash Expenditures Gleckman v. United States, 80 F

Bank Deposits & Cash Expenditures Gleckman v. United States, 80 F.2d 394 (8th Cir. 1935) Differs from Bank Account Analysis: Depth of analysis of ALL bank account transactions Accounts for cash expenditures Estimates actual personal living expenditures Theory: only 2 things can occur with $$$: deposit or spent (including hoard)

Differs from Bank Account Analysis: Depth of analysis of ALL bank account transactions. Accounts for cash expenditures. Estimates actual personal living expenditures. Theory: only 2 things can occur with $$$: deposit or spent (including hoard)")

152

Bank Deposits & Cash Expenditures

Assumptions: Bank deposits, adjustment for non-applicable items reflect taxable receipts (for tax matters) Outlays on tax return were real: Could only occur from check, cash or credit card If cash, presumes taxable source Taxpayer’s burden to demonstrate nontaxable

Outlays on tax return were real: Could only occur from check, cash or credit card. If cash, presumes taxable source. Taxpayer’s burden to demonstrate nontaxable.")

153

Bank Deposits & Cash Expenditures

Used for business & nonbusiness May lead to additional sources If method indicates understatement of income: Underreported income AND/OR Overstated expenses

154

Bank Deposits & Cash Expenditures

Typical uses: Books & records unreliable Deposits suggest income sources Most expenses paid by check Account previously used as reporting base Comments: Significant cash reliance may preclude Cannot take shortcut Method incomplete unless cash accounted for

155

Gross Receipts Defined

Deposits into accounts Funds expended, but not deposited Funds accumulated, but not deposited

156

Bank Deposits & Cash Expenditures

157

Formal Indirect Methods

Source & application of funds a.k.a. “Cash T” Analysis Bank Deposits & Cash Expenditures Markup Method Unit & Volume Net Worth

158

Markup Method United States v. Fior D’Italia, Inc. , l536 U. S

Reconstructs income: Uses subject-specific percentages or ratios Obtained from Bureau of Labor statistics or industry sources May use subject’s actual markups May overcome weaknesses of other Formal Indirect Methods when cash is unknown Cost of Goods Sold verified and used to derive Revenues

159

Markup Method Typical uses:

Inventories are principal income-producing asset and subject records unreliable Cost of Goods Sold readily ascertained and reasonable certainty re sales prices Cash-based business, e.g. gasoline retailers, liquor stores, taverns, restaurants, jewelry stores, et al

160

Markup Method Gross Profit Margin to Sales:

(Sales-Cost of Goods Sold)/Sales

/Sales.")

161

Markup Method - Example

162

Formal Indirect Methods

Source & application of funds a.k.a. “Cash T” Analysis Bank Deposits & Cash Expenditures Markup Method Unit & Volume Net Worth

163

Unit & Volume Irby v. Commissioner TC Memo 1997-347

Apply sales price to volume of subject business Carryout pizza, coin operated laundry, mortuaries

164

Unit & Volume Typical uses:

Units readily ascertained and pricing apparent Few types of products/services with little variation and price

165

Unit & Volume – Example

166

Item Listing Method Logical starting point Very easy to modify

Provides a trail of investigation Leads to other evidence Simple for the “court,” jury, judge, etc.

167

Item Listing - Beginning

168

Net Worth Method Very old method:

United States v. Frost 25 F. Cas (N.D. III. 1869) First criminal case involving method: United States v. Beard, 222 F.2d 84 (4th Cir. 1955) Approved by U.S. Supreme Court: Holland v. United States, 348 U.S. 121 (1954)

First criminal case involving method: United States v. Beard, 222 F.2d 84 (4th Cir. 1955) Approved by U.S. Supreme Court: Holland v. United States, 348 U.S. 121 (1954)")

169

Holland Requirements:

Establish opening net worth, i.e. “base year” with reasonable certainty Negate reasonable taxpayer explanations inconsistent with guilt; e.g. non-taxable funds Establish net worth increases attributable to taxable income If no books and records willfulness may be inferred from that fact couple with income understatement If books & records ok on face willfulness might not be inferred from net worth increase alone Government must prove beyond reasonable doubt, but not mathematical certainty

170

(Modified) Net Worth Method

Long-recognized by the courts Implied income based upon changes in cost-based net worth (equity) Intuitively understood “Relatively” simple to prepare Straightforward to explain in court aka “Indirect Method”

Intuitively understood. Relatively simple to prepare. Straightforward to explain in court. aka Indirect Method")

171

Net Worth Method

172

Example Net Worth Method

173

Cash Inflows/Outflows Analysis

174

(Modified) Net Worth - Applied

Dual Integration of (Pat Perzel): Lifestyle Cash Flow Net Worth

: Lifestyle Cash Flow. Net Worth.")

175

Non-Business Expenditures

Forensic Analysis: Unreported Income Non-Business Expenditures

177

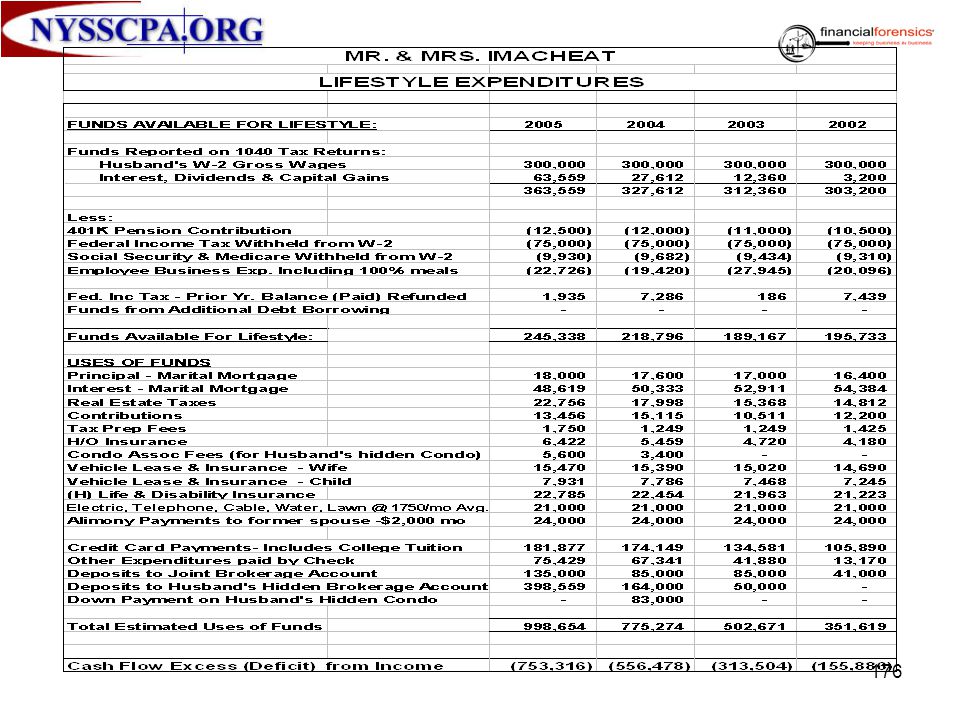

LIFESTYLE EXPENDITURES, CON’T

MR. & MRS. IMACHEAT LIFESTYLE EXPENDITURES, CON’T

182

Proof-of-Cash Traces “reported” receipts and disbursements to bank statement(s) Relatively simple to prepare Excellent validation tool Intuitively understood Start with annual, “drill-down” to monthly

183

Example Proof-of-Cash (Annual)

")

184

Actual Proof-of-Cash (Monthly)

")

185

Today – Session Description…

Will preview in reverse order Court cases re forensic accounting Applied forensic techniques, e.g. guidelines Accelerate (throughout) 185

185.")

192

Essential Concept of Statistics

Attributes Necessary to Prepare a Business Valuation Judgment Analytical skills Financial expertise Judgment is Key Element During the valuation process, certain information will be readily available and unquestionable. Other information will require the valuator to use judgment. The elements of common sense, informed judgment, and reasonableness all work together in formulating the opinion of value, regardless of the nature or purpose of the valuation.

193

1. Descriptive Statistics

1.1 A meaningful way to summarize a collection of data: May be presented in tabular, graphic or numerical format Used to provide summaries of the information in a data set Makes the data easier to interpret Attributes Necessary to Prepare a Business Valuation Judgment Analytical skills Financial expertise Judgment is Key Element During the valuation process, certain information will be readily available and unquestionable. Other information will require the valuator to use judgment. The elements of common sense, informed judgment, and reasonableness all work together in formulating the opinion of value, regardless of the nature or purpose of the valuation.

194

2. Inferential Statistics

2.1 Inferential statistics relate to: The process of using data from a sample To make estimates and test hypotheses concerning the characteristics of a population 2.2 Inferential statistics uses the following groups: Population – is a set of all elements in a particular study Sample – is a subset of the population Important IRS Guidelines Revenue Ruling – Valuation of closely held companies Revenue Ruling – Excess Earnings Method Revenue Ruling – Minority stockholder of family – controlled company is not subject to family attribution rules

195

3. The Objective of Statistics

3.1 Statistical inference is a logical method by which relative truth can be extracted from numerical data: Describes sets of numbers or objects Make reasonable inferences about groups based on incomplete and/or limited information Inferences about the characteristics of a parent group by studying a limited amount of data from a smaller group Reasons for Business Valuations Business Selling all or partial interest of a business Buying all or a partial interest of a business Mergers/Acquisitions Corporate or partnership dissolutions Obtaining financing Buy-sell agreements Purchase price allocations Gift and Estate Area Estate planning Estate and gift tax returns Family limited partnerships Litigation Marital dissolutions Dissenting stockholder suits Insurance claims Determining damages in litigation Other Charitable contributions Preparing personal financial statements

196

3. The Objective of Statistics (con’t)

3.2 An inference is an educated statistical guess used to solve a particular problem: Relates to the degree of probability of a thing being true or that a particular event will occur Statistics are only mathematical estimates Case Examples Estate Tax Valuation A father and two sons each owned a one-third interest in a wholesale jewelry manufacturing company. When the father died, we valued the father’s one-third interest in the Company for estate tax purposes and were able to reduce the value and the estate tax by applying minority discounts. Acquisition of a Business We were retained to value a dental practice for the purpose of a purchase. The scope of our review included normalizing the earning stream and the preparation of a cash flow analysis to determine disposable income to meet the buyer’s debt requirements. We were able to reduce the purchase price due to various risk factors inherent in the practice. Gifting to Family Members The owner of a wholesale hardware distribution company wished to gift shares of his Company’s stock to his son who worked for the Company for many years. We valued the Company’s shares of common stock for the father’s gifting program. A client who owned the general and limited partnership interests of a Family Limited partnership (FLP) that had real estate and marketable securities wished to gift limited partnership interests to his children and grandchildren. We valued their limited partnership interests in the FLP and were able to transfer any future appreciation of the assets out of our clients estate. Matrimonial A business owner had a valuation done on his business to determine its value for equitable distribution purposes. We were retained by the spouse to have the business independently valued. We valued the business significantly higher due to significant personal expenses in the business.

that had real estate and marketable securities wished to gift limited partnership interests to his children and grandchildren. We valued their limited partnership interests in the FLP and were able to transfer any future appreciation of the assets out of our clients estate. Matrimonial. A business owner had a valuation done on his business to determine its value for equitable distribution purposes. We were retained by the spouse to have the business independently valued. We valued the business significantly higher due to significant personal expenses in the business.")

197

3. The Objective of Statistics (con’t)

3.3 Statistics are rarely presented, absent a statement of precision (confidence). These are related issues: Precision relates to the probability associated with the estimate and the degree upon which the user can rely on the inference Any statistical study that omits a statement of precision should be scrutinized for bias or prejudice Precision is dependent on: Properly selected sample or samples Correctly applied statistical methods Standard of Value · Fair market value – willing buyer and willing seller · Fair value – varies in each state; most common in minority shareholder cases · Investment value (intrinsic value) – incorporates synergies and other factors

. These are related issues: Precision relates to the probability associated with the estimate and the degree upon which the user can rely on the inference. Any statistical study that omits a statement of precision should be scrutinized for bias or prejudice. Precision is dependent on: Properly selected sample or samples. Correctly applied statistical methods. Standard of Value. · Fair market value – willing buyer and willing seller. · Fair value – varies in each state; most common in minority shareholder cases. · Investment value (intrinsic value) – incorporates synergies and other factors.")

198

3. The Objective of Statistics (con’t)