Download presentation

Presentation is loading. Please wait.

1

VA Guaranteed Home Loans

Roanoke VA Regional Loan Center Compliments of Roanoke and Cleveland RLC

2

Contact Information National VA website: Roanoke VA website: Toll Free: (800) This is a little play on words; Contact & Information – information on how to contact us, but also, you can obtain information through these sites and at this phone number The Lender’s Handbook – Definitive source for information on VA loans

This is a little play on words; Contact & Information – information on how to contact us, but also, you can obtain information through these sites and at this phone number. The Lender’s Handbook – Definitive source for information on VA loans.")

3

Types Of VA Loans Purchase or construct a home

Purchase a VA/HUD approved condo or townhouse Purchase farm property Purchase a home and improve at the same time Manufactured home on permanent foundation Interest Rate Reduction Refinance Loans (IRRRL) Cashout Refinances Energy Efficient Improvement Give details of each of the above EEM details in Chapter 7, section 3 up to $3,000 based on documented costs up to $6,000, analysis determines increased PITI offset by likely reduction in utility costs more than $6,000 to the extent that cost is supported by equal increase in value. Up to 4 units Farm property appraised for residential value Others – Includes purchase MH and land and affix to permanent foundation; simultaneously purchase and improve…, others…..

Cashout Refinances. Energy Efficient Improvement. Give details of each of the above. EEM details in Chapter 7, section 3. up to $3,000 based on documented costs. up to $6,000, analysis determines increased PITI offset by likely reduction in utility costs. more than $6,000 to the extent that cost is supported by equal increase in value. Up to 4 units. Farm property appraised for residential value. Others – Includes purchase MH and land and affix to permanent foundation; simultaneously purchase and improve…, others…..")

4

WHAT A VA LOAN CAN DO Ensures Equal Opportunity to Veterans

No Down Payment Program Negotiable Fixed Interest Rate Streamlined Processing for Lenders Right to Prepay without Penalty Assumable Mortgage Limitations on Closing Costs Forbearance Extended to VA Homeowners Experiencing Temporary Financial Difficulty

5

Dispelling The Myths Appraisals take forever! Too much red tape!

Too much paperwork! VA takes too long!

6

Do You Remember The Past ?

Find a Home Apply to Lender For Loan Apply for COE Lender Orders Appraisal by Phone VA Mails Guaranty To Lender Processing Time Six to Eight Weeks! Appraisal Received by VA, Reviewed and CRV Issued VA Reviews Each Package (30 to 40 Documents!!) Lender Packages Loan and Sends to VA for Approval SAY A FEW WORDS ABOUT EACH PICTURE AS YOU CLICK AND IT MOVES ACROSS THE SCREEN VA Approves or Disapproves Loan and Notifies Lender Lender Sends Loan Package to VA Lender Closes Loan

Lender Packages Loan and. Sends to VA for Approval. SAY A FEW WORDS ABOUT EACH PICTURE AS YOU CLICK AND IT MOVES ACROSS THE SCREEN. VA Approves or Disapproves. Loan and Notifies Lender. Lender Sends. Loan Package to VA. Lender Closes Loan.")

7

Where We Are Today… Find Home Go to Lender

Determines eligibility electronically using ACE Go to Lender Uses AUS to get decision in minutes Orders Appraisal thru TAS Self Explanatory Lender Closes Loan Obtains Loan Guaranty Electronically 14-21 Days

8

What Changed? How we got from there.. …..To Here Consolidation

45 Regional Offices administered VA’s Home Loan Program; now 9 Regional Loan Centers & the Eligibility Center The Portal, TAS, FFPS, WBLS, webELI, others Lenders have the Power We review a minimum of 10% of closed loans to ensure compliance with VA’s Guidelines & Standards Consolidation Automation Delegation Oversight

9

How Long Does The Average VA Loan Sit On a Government Employee’s Desk?

0 days 15 days 30 days 45 days Forever The reason for this, in addition to the consolidation and automation that I previously talked about, is that most VA loans are processed by what we call the “Automatic” procedure.

10

Automatic Procedure Lender.. Originates Processes

Underwrites Income & Credit packages and the Appraisal Closes loan without sending anything to VA Lender guarantees loan online through a system called WebLGY

11

Loans That Must Be Submitted As Prior Approval

Joint Loans Vets in receipt of non-service connected pension Vets rated incompetent by VA Interest Rate Reduction Loans when refinancing a delinquent loan ************************************ Of course, Prior approval lenders must submit loans for Prior approval. Automatic lender’s underwriter may submit loan for Prior approval when the believe it warrants merit and should be approved.

12

Prior Approval Lender.. Originates Processes

Submits loan to VA for underwriting Closes after VA issues commitment, usually in 3-5 days

13

99% of VA Loans are Automatics

1% are Priors

14

Who Is Eligible For A VA Home Loan?

Honorably discharged veterans who served: 2 years on active duty 6 years in the Reserve/National guard POW’s held in captivity for 90 days of more 90 days of wartime duty when called up or ordered under U.S.C. Title 10 (this US code must appear on DD214). 181 days of peacetime duty called up under U.S.C. Title 10 Some unmarried surviving spouses Reserves/Guard member eligible with 6 years of service, or, if activated under title 10 Unmarried surviving spouse; spouse’s death must have occurred while in military on active duty or related to something that happened to them while they were on active duty Other – Public health service, certain merchant seaman, etc. 14

. 181 days of peacetime duty called up under U.S.C. Title 10. Some unmarried surviving spouses. Reserves/Guard member eligible with 6 years of service, or, if activated under title 10. Unmarried surviving spouse; spouse’s death must have occurred while in military on active duty or related to something that happened to them while they were on active duty. Other – Public health service, certain merchant seaman, etc. 14.")

15

90 Days Wartime World War II – (9/16/40 - 07/25/47)

Korean Conflict – (06/27/50 - 1/31/55) Vietnam – (08/05/ /07/75) Persian Gulf - 08/02/90 …

Vietnam – (08/05/ /07/75) Persian Gulf - 08/02/90 …")

16

181 Days Peacetime Post WWII - 7/26/47 - 6/26/50

Post Korean - 2/1/55 - 8/4/64 Post Vietnam - 5/8/75 - 8/1/90

17

2 Year Requirement Enlisted person - After September 7, 1980

Officer – After October 16, 1981 (90 days applies to Persian Gulf wartime service called up under U.S.C. Title 10)

")

18

Reserve & National Guard

6 Years Total Service unless activated under Title 10

19

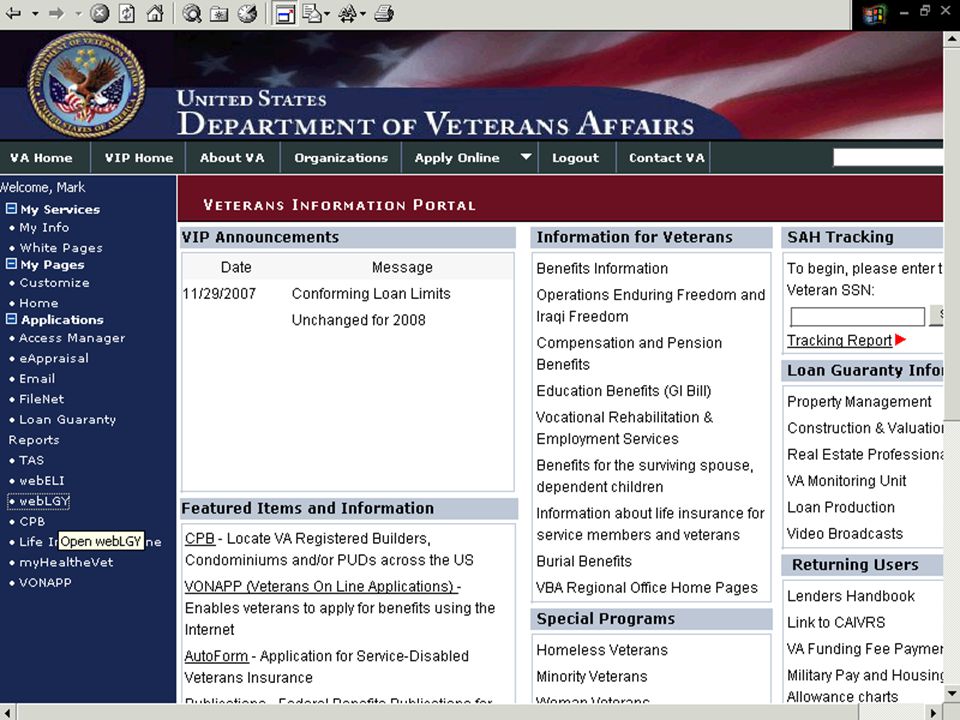

VETERANS INFORMATION PORTAL (VIP)

Veterans Information Portal – Where Lenders Access: ACE TAS WBLS Other…(TAS, e-appraisal.etc.)

")

20

Obtaining A COE VA Form 26-1880

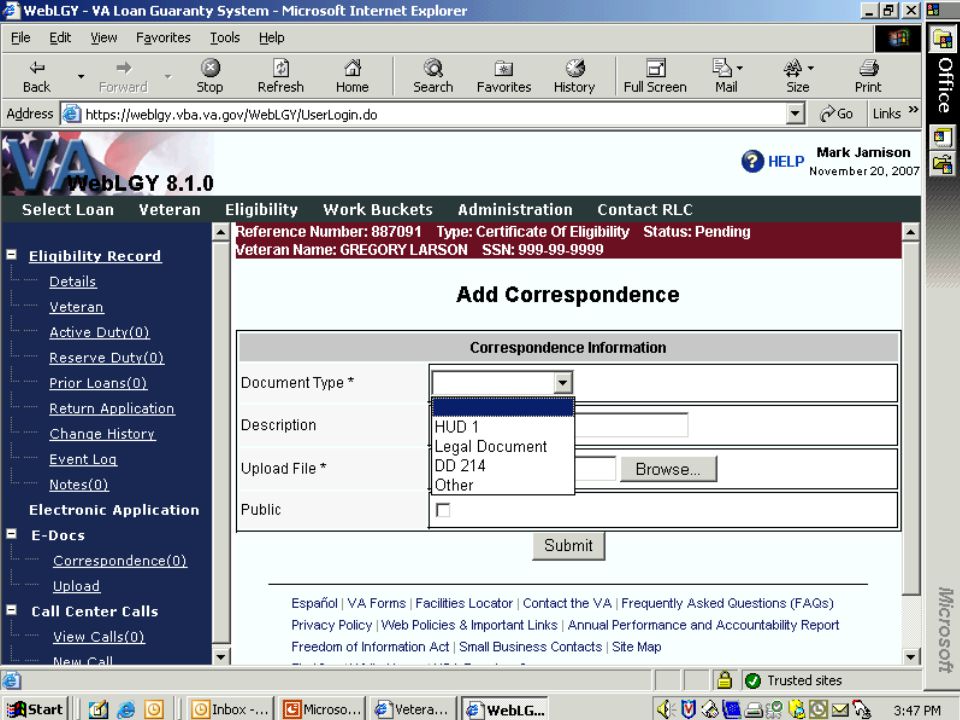

Proof of service documentation (DD214, active duty statement of service or Reserve/National Guard points statement) If veteran had previous VA home that was sold, a copy of the HUD-1 Settlement Statement , Request for a Certificate of Eligibility available on website: Proof of service: DD 214 Statement of Service NGB 22 or NGB 23 Restoration Documents (1880, HUD 1, proof of service) “One Time Restoration” without disposal of property. To get proof of service docs: 20

If veteran had previous VA home that was sold, a copy of the HUD-1 Settlement Statement , Request for a Certificate of Eligibility available on website: Proof of service: DD 214. Statement of Service. NGB 22 or NGB 23. Restoration Documents (1880, HUD 1, proof of service) One Time Restoration without disposal of property. To get proof of service docs:")

21

Automated Certificates Of Eligibility (ACE)

An automated system used by lenders to obtain an online certificate of eligibility Accessed through the VIP

22

Those who use a favorite, shortcut, or an old link may have trouble accessing the Portal or its applications (TAS, ACE). You need to type the website “vip.vba.va.gov” into the address bar to access the portal.

28

ACE Facts For use by lenders and mortgage brokers

No application for certificate of eligibility needed Vet’s SSN & Name all that’s required to use ACE system Typical successful ACE candidate is a first time user of VA program, discharged after 1980 and served on active duty for 2 years

29

ACE Facts (cont.) ACE certificates of eligibility no longer printed on green or gold safety paper. ACE certificates printed from computer on white paper. Authorization number distinguishes authenticity

30

ACE Can’t Make All Determinations

Reserves/National Guard Prior VA loan foreclosure Insufficient time/discharge type Unmarried surviving spouse

31

If ACE Is Not Successful: How To Obtain A COE

32

VA Eligibility Center Winston Salem Eligibility Center P.O. Box Winston Salem, NC VA Form “Request for a Certificate of Eligibility” Status of LA Refer to EC handout 32

33

What Does A Certificate Of Eligibility (COE) Mean To You?

GNMA, FNMA and FHLMC require government loans to have a minimum of 25% guaranty coverage Basic entitlement – under old law, allows for up to $36,000 for loans not to exceed $144,000 Certificate of eligibility tells the lender, broker or real estate agent how much entitlement a veteran has

34

What Does A Certificate Of Eligibility Mean To You (cont.)?

A veteran who previously used the VA home loan program would need to sell the home and transfer title to obtain the full basic and bonus entitlement back (restoration of entitlement) A veteran can obtain a certificate of eligibility over and over, provided they have adequate entitlement

A veteran can obtain a certificate of eligibility over and over, provided they have adequate entitlement.")

35

Appraised Value or Purchase Price

Maximum VA Loan Amount Limited to the lesser of: Appraised Value or Purchase Price + VA Funding Fee Energy Efficient Improvements

36

Maximum VA Loan Amounts

Maximum VA loan is the lesser of the appraised value or the purchase price VA loan is based on available entitlement Secondary market requirements for GNMA, FNMA and FHLMC require at least a 25% guaranty Of course, Prior approval lenders must submit loans for Prior approval. Automatic lender’s underwriter may submit loan for Prior approval when the believe it warrants merit and should be approved.

37

Maximum VA Loan Amounts

VA’s maximum guaranty on a $417,000 loan is $104,250, or $417,000 x 25% = $104,250 ****WE’VE RAISED THE ROOF**** Example: The COE issued to you shows $36,000 basic entitlement. This amount can be increased to an amount equal to 25% of the Freddie Mac conforming loan limit which is $417,000 across the country – exception for those counties with a temporary increase. Alexandria, VA, for example, is one county with a temporary increase of $768,750 for a home over $144,000. Entitlement = $192,187.5 ($36,000 basic + $156,187.5 bonus)….$192,187.5 x 4 = $768,750. If you qualify for a home costing $768,750, the lender that you are approved through would receive a 25% guaranty. Of course, Prior approval lenders must submit loans for Prior approval. Automatic lender’s underwriter may submit loan for Prior approval when the believe it warrants merit and should be approved.

….$192,187.5 x 4 = $768,750. If you qualify for a home costing $768,750, the lender that you are approved through would receive a 25% guaranty. Of course, Prior approval lenders must submit loans for Prior approval. Automatic lender’s underwriter may submit loan for Prior approval when the believe it warrants merit and should be approved.")

38

Partial Entitlement Remaining Entitlement Scenario

Veteran purchases a home in 1995 for $100,000 VA guarantees 25% of loan or $25,000 Loan is still open and being paid on Assuming the conforming loan limit is $417,000. If the conforming loan limit is higher – ex. bonus as shown on previous screen would be more. Remaining Entitlement: $36,000 basic entitlement - 25,000 used $11,000 remaining basic +68,250 bonus entitlement $79,250 total entitlement left x $317,000 maximum loan to obtain 25% guaranty

39

VA Appraisals What’s changed at VA regarding appraisals?!!!

40% increase in number of appraisers in all states All appraisers must be e-commerce compliant Appraisers are expected to communicate with all parties Lender Appraisal Processing Program (92%) Timeliness issues aggressively monitored Funding Fee is only cost that can be added to the loan Current rates (see handout): Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS Debt Checks Referred to earlier.

Timeliness issues aggressively monitored. Funding Fee is only cost that can be added to the loan. Current rates (see handout): Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans. 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS. Debt Checks Referred to earlier.")

40

Minimum Property Standards Bottom Line: NO “FIXER UPPERS!”

VA Appraisals Minimum Property Standards Safe – meets local/county safety codes (electrical, structural and location) Sanitary – well, septic and sanitary sewer pass local/county inspection Sound – meets local/county structural building codes Bottom Line: NO “FIXER UPPERS!” Funding Fee is only cost that can be added to the loan Current rates (see handout): Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS Debt Checks Referred to earlier.

Sanitary – well, septic and sanitary sewer pass local/county inspection. Sound – meets local/county structural building codes. Bottom Line: NO FIXER UPPERS! Funding Fee is only cost that can be added to the loan. Current rates (see handout): Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans. 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS. Debt Checks Referred to earlier.")

41

Basic Rule Of VA Loans Regarding Owner Occupancy

Generally, must occupy within 60 days Exceptions – IRRRLs – do not have to occupy Spouse of veteran can satisfy occupancy If veteran is on active duty, must occupy within 12 months IRRRL must certify previously occupied If by virtue of active duty military service, unable to occupy the property, the occupancy requirement is met if the house is occupied by the service person’s legal spouse Occupany generally required within 60 days Exceptions and other details, Lender’s Handbook, Chapter 3, Section 5

42

VA FUNDING FEE Funding fee can be added to the based loan amount

Funding fee amount varies depending on loan type, down payment, and whether or not veteran had VA loan previously Funding fee is paid online at Some borrowers are exempt Funding Fee is only cost that can be added to the loan Current rates (see handout): Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS Debt Checks Referred to earlier.

: Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans. 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS. Debt Checks Referred to earlier.")

43

Veterans Exempt From Funding Fee

Veteran receiving 10% disability compensation from VA Veteran receiving military pension from VA, in lieu of compensation Surviving spouse of a veteran who died as a result of active duty injuries *******************************

44

VA Funding Fees Basics Please refer to your handbook.

Loan Type Active Duty Funding Fee % Reservist/National Guard Funding Fee % Purchase 2.15% 2.40% Subsequent Use 3.30% Cashout Subsequent 3.3% 2.4% Misnamed (CAIVRS checks for federal debt), we use it: Verifies VA income Confirms when loan must come in for Prior approval such as incompetent vet or vet in receipt of non-service connected pension Confirms if vet exempt from FF because of disability (usually 10% min. rating) VB Act of 2004 in 12/04 made possible exemption for pre-discharge ratings

, we use it: Verifies VA income. Confirms when loan must come in for Prior approval such as incompetent vet or vet in receipt of non-service connected pension. Confirms if vet exempt from FF because of disability (usually 10% min. rating) VB Act of 2004 in 12/04 made possible exemption for pre-discharge ratings.")

45

UNDERWRITING Underwriter’s Objective: Determine that the veteran is a

satisfactory credit risk, and has the income to qualify for the loan

46

INCOME Stable and Reliable Anticipated to continue

Sufficient in amount Reportable/Verifiable Identify and verify income to meet: - mortgage payment - other shelter expenses - debts and obligations - family living expenses

47

Income Income must be “verifiable”

Prefer a 2 year history, but consideration given for at least 12 months on the job Veteran can obtain VA loan immediately out of the military if employment is related to military technical experience Explain significant gaps in employment Consider income of spouse who is contractually obligated on loan or in a community property state.

48

Verification Standard: Alternative:

VA Form , Verification of Employment, or Pay stubs Alternative: Telephone verification Pay stubs (30 days) W 2s for 2 years Verbal VOE = need date of verification, the name title and telephone number of the person with whom employment was verified. Alternative documentation can only be used if the lender concludes that income is stable, reliable, and anticipated to continue. Feedback certification on AUS loans state what’s needed.

W 2s for 2 years. Verbal VOE = need date of verification, the name title and telephone number of the person with whom employment was verified. Alternative documentation can only be used if the lender concludes that income is stable, reliable, and anticipated to continue. Feedback certification on AUS loans state what’s needed.")

49

Other Types of Verifications

Faxed & Internet Verifications Employment Verification Services Leave & Earning Statement (LES) for Active Duty Service (available at “my pay” Income tax returns (self employment) & YTD P&L and balance sheet Other…… Faxed & Internet (must be able to determine “authenticity”); fax must contain “banner” information; internet must contain “URL” Employment verification services – “The work number for everyone” (TALX); these must be approved by VA LES online at will bring it up. Self employed, generally less than 2 years, not stable/reliable (can’t use) unless previous related employment and seller’s (of business) financial records. Consider economic outlook. Is there a steady or significant decline in earnings over the period analyzed? Other = leases

for Active Duty Service (available at my pay Income tax returns (self employment) & YTD P&L and balance sheet. Other…… Faxed & Internet (must be able to determine authenticity ); fax must contain banner information; internet must contain URL Employment verification services – The work number for everyone (TALX); these must be approved by VA. LES online at will bring it up. Self employed, generally less than 2 years, not stable/reliable (can’t use) unless previous related employment and seller’s (of business) financial records. Consider economic outlook. Is there a steady or significant decline in earnings over the period analyzed Other = leases.")

50

Income less than 12 months…

Generally not considered stable and reliable Carefully consider: ~ Employer’s evaluation of probability of continued employment ~ Special training/education/skills required If using this income… … you must explain why!!! Consider skilled positions: nurse, medical technician, lawyer, computer systems, analyst, etc. Income may be considered to offset debts of months duration. Determine amounts to be used based on factors such as: - employers probability of continued employment - length of employment (ex. 10 months vs. 6 months) Include explanation with loan submission. Consider recent history of frequent changes in employment Analyze the reasons for the changes Favorable: Career advancement in same line of work Unfavorable: No apparent betterment to applicant One line of work to another Income from Overtime, Part-time, Second jobs and bonuses: Must be stable, reliable, and has continued (and is verified) for at least two years. Also must be regular, predictable, and likely to continue For example, 2nd job: Is it compatible with hours of duty and work conditions of primary job? How long has the applicant been employed under such arrangement? This income, if verified at least 12 months, may be used to offset debts. Include explanation.

Include explanation with loan submission. Consider recent history of frequent changes in employment. - Analyze the reasons for the changes. Favorable: Career advancement in same line of work Unfavorable: No apparent betterment to applicant One line of work to another. Income from Overtime, Part-time, Second jobs and bonuses: Must be stable, reliable, and has continued (and is verified) for at least two years. Also must be regular, predictable, and likely to continue. - For example, 2nd job: Is it compatible with hours of duty and work conditions of primary job How long has the applicant been employed under such arrangement This income, if verified at least 12 months, may be used to offset debts. Include explanation.")

51

Overtime, Part Time and Bonus Income

Generally not considered stable and reliable unless 2 year history Verification for at least 12 months – income may be used to offset debts of 10 to 24 months Income from Overtime, Part-time, Second jobs and bonuses: Must be stable, reliable, and has continued (and is verified) for at least two years. Also must be regular, predictable, and likely to continue For example, 2nd job: Is it compatible with hours of duty and work conditions of primary job? How long has the applicant been employed under such arrangement? This income, if verified at least 12 months, may be used to offset debts of 10 to 24 months.

for at least two years. Also must be regular, predictable, and likely to continue. - For example, 2nd job: Is it compatible with hours of duty and work conditions of primary job How long has the applicant been employed under such arrangement This income, if verified at least 12 months, may be used to offset debts of 10 to 24 months.")

52

Credit History 3-File Merged (MCR)

Residential Mortgage Credit Report (RMCR) Verify Rent/Mortgage history Include a written explanation for any debt that is not rated: For example, childcare expenses. VOR/VOM history often best indicator of whether applicant will make timely mortgage payments in the future.

Verify Rent/Mortgage history. Include a written explanation for any debt that is not rated: For example, childcare expenses. VOR/VOM history often best indicator of whether applicant will make timely mortgage payments in the future.")

53

Does VA Consider Credit Scores?

YES NO

54

Automated Underwriting Systems (AUS)

Most major lenders approved to use AUS systems Typical VA “Accept” is in the 640 credit score range

55

Automated Underwriting Systems Approved By VA

Desktop Underwriter Loan Prospector Countrywide’s CLUES Chase’s ZIPPY PMI/AURA For VA Loans

56

AUS “Accept” For VA Loans

In the 640 mid-credit score range “Accept” gives credit clearance with waiver of certain derogatory issues AUS “Accept” does not mean loan is clear to close Veteran must still meet debt ratio and residual income factors

57

AUS Refer or Manual Underwrite: What We Consider For Approval

Review individual trade lines – derogatories in last 12 months? Collection accounts – minor or major? Charge offs – how much and how long ago? Federal debt – cannot close with open, unpaid Federal debt Judgments – cannot close with open, unpaid judgments Absence of credit history Should be no lates in most recent 12 months Collection accounts do not necessarily have to be paid as a condition of loan approval. Recent payment of collections does not alter unsatisfactory payment history Judgments must be paid in full or subject to a repayment plan with a history or timely payments. Federal debts should be paid or in repayment plan 12 + months An absence of credit history is not a reason for disapproval. For non-traditional credit, develop evidence of timely payment of non-installment obligations. This should not be used to offset derogatory credit. (Usually 12 months history required) If the applicant(s) are determined satisfactory credit risks in spite of derogatory credit, include an explanation for the basis of this determination.

If the applicant(s) are determined satisfactory credit risks in spite of derogatory credit, include an explanation for the basis of this determination.")

58

Bankruptcy ~ Chapter 7 Discharged 2 + years ago if bankruptcy was caused by borrower’s financial mismanagement Discharged 12 months ago - must be due to circumstances beyond borrower’s control Must have documentation Must have re-established credit in most recent 12 months For months: May be possible if due to reasons beyond the control of the applicant(s) and if good credit has been re-established. (example: medical reasons, not divorce) Divorce is not viewed to be beyond the control of the borrower. For business failure, ensure that it was not due to applicant’s misconduct. Bankruptcy in most recent 12 months, it’s not going to be possible to determine good credit risk.

and if good credit has been re-established. (example: medical reasons, not divorce) Divorce is not viewed to be beyond the control of the borrower. For business failure, ensure that it was not due to applicant’s misconduct. Bankruptcy in most recent 12 months, it’s not going to be possible to determine good credit risk.")

59

Bankruptcy ~ Chapter 13 & Consumer Credit Counseling

This indicates an effort to pay and may be viewed as evidence of acceptable credit if: 12 month payment history, no lates Acknowledgment of trustee or agency For Consumer Credit Counseling: If the applicant(s) have good prior credit and are participating in CCC, then such participation is considered to be a neutral factor, or even a positive factor, in determining credit worthiness. Do not treat this as a negative item if the veteran entered into a CCC plan before reaching the point of having bad credit.

have good prior credit and are participating in CCC, then such participation is considered to be a neutral factor, or even a positive factor, in determining credit worthiness. Do not treat this as a negative item if the veteran entered into a CCC plan before reaching the point of having bad credit.")

60

Foreclosures Develop facts and circumstances

Same waiting periods as Chapter 7 Bankruptcy Prior VA Loan: Ensure no debt to Government and entitlement restored Apply bankruptcy guidelines.

61

Debts & Obligations May remove debts with 10 monthly payments remaining (if not significant) Only monthly revolving and installment accounts considered Child care is a monthly obligation Investigate all allotments on LES or pay stubs Verify and consider Alimony and Child Support Obtain verification directly from creditor for: - Debts not on credit report - Accounts listed “will rate by mail” or “need written authorization” Resolve any discrepancies. Childcare falls under the guidelines as debt that has not been rated on the credit report. (sec. 4.05, page 4-31)

")

62

Debts & Obligations You May Disregard

Co-obligor on another’s loan: evidence payments made by someone else No reason to believe applicant will need to make payments in the future Student Loan payments deferred 12 months or more. 401K loans (or other loans secured against deposited funds). 401K Loan example: A veteran has $10,000 in his TSP (or other retirement account). He takes out a loan (borrows against it) for $7,000. The lender does not have to include this monthly payment as debt AND may only include the remaining $3,000 as available assets.

. 401K Loan example: A veteran has $10,000 in his TSP (or other retirement account). He takes out a loan (borrows against it) for $7,000. The lender does not have to include this monthly payment as debt AND may only include the remaining $3,000 as available assets.")

63

Assets Sufficient in amount VA Form 26-8497a, Verification of Deposit

Alt Docs: Last two bank statements Internet and faxed verifications ********************** Gift Letters: Statement from the gift giver stating that the gift does not have to be repaid. (Evidence of available funds not a VA requirement) Note: down payment can be borrowed (not when price exceeds value)

Note: down payment can be borrowed (not when price exceeds value)")

64

VA’s Standards Debt-to-income Ratio – 41%

Residual Income - should meet VA’s residual income tables Lender must complete Loan Analysis, VA Form

65

Debt Ratio 46% - $50 Residual Shortfall

Approve Loan Reject Loan Could go either way VA standards are “guidelines” Consider all of the facts in the individual case Consider COMPENSATING FACTORS Was it an AUS approve (with data integrity)?

")

66

Contract Issues Contingent on VA financing VA

“Escape Clause” is mandatory Seller must pay termite inspection ************************ . See Option Clause in handout

67

Allowable Fees & Charges

Appraisal Report & Compliance Inspections Credit Report Prepaid Taxes and Hazard Insurance Title Exam and Title Insurance Fees Flood Zone Determination Environmental Endorsements (3.0, 8.1,103.5) Recording Fees and Taxes EPA Endorsement Origination Fee (1%) Reasonable Discount Points (May roll up to 2 points into an IRRRL) See Handout Whenever the charge relates to services performed by a third party, the amount paid by the borrower is limited to the actual charge of that third party. For example: The lender obtains a credit report at a cost of $30. Then the lender may only charge the borrower $30. The borrower may not pay a duplicate fee for services that have already been paid for by another party. Alta Endorsement fees for Hybrid ARMS is allowable as long as the charge is reasonable. ($50).

Recording Fees and Taxes. EPA Endorsement. Origination Fee (1%) Reasonable Discount Points (May roll up to 2 points into an IRRRL) See Handout. Whenever the charge relates to services performed by a third party, the amount paid by the borrower is limited to the actual charge of that third party. For example: The lender obtains a credit report at a cost of $30. Then the lender may only charge the borrower $30. The borrower may not pay a duplicate fee for services that have already been paid for by another party. Alta Endorsement fees for Hybrid ARMS is allowable as long as the charge is reasonable. ($50).")

68

Fees That Can Never Be Charged To A Veteran

Termite/Pest Inspection Septic Inspection (as mandated by county) Well Inspection (as mandated by county) Mortgage Broker Fee See Handout (if asked) HUD/FHA inspection Fees for builders Others…..

Well Inspection (as mandated by county) Mortgage Broker Fee. See Handout. (if asked) HUD/FHA inspection Fees for builders. Others…..")

69

WHAT’S NEW IMPACT OF RESPA FOR VA

New HUD1 and Good Faith Estimate VA will continue to have a cap on the origination fee and limit the type of charges that may be paid by the veteran. In order to monitor these fees, VA is requiring lenders to itemize these charges in the empty 800 lines of the HUD-1 (effective 5/1/2010). Lenders will be required to maintain a copy of the GFE and invoices for third party charges as part of their origination package.

. Lenders will be required to maintain a copy of the GFE and invoices for third party charges as part of their origination package.")

70

One Percent Origination Fee

The lender may charge the veteran a flat fee up to one percent of the loan amount. The flat fee is intended to cover the lender’s costs and services which are not reimbursable as itemized fees. For Interest Rate Reduction Refinance Loans – this fee may not exceed 1% of the existing loan balance of the loan being refinanced plus the cost of energy efficient items less any cash payments from the veteran. Circular – Lists Reasonable and Customary Items along with Unallowable Itemized Fees – Also refer to Chapter 8, section 2d of the Lenders Handbook.

71

2009 VA Loan Statistics 325,675 VA loans nationwide

$68.2 billion in VA loan volume Average VA loan $209,395.

72

Foreclosure Avoidance Options

Repayment Plans Deed In Lieu of Foreclosure Loan Modification VA Refunding Compromise Sale THE HOMEOWNER NEEDS TO CONTACT THEIR LENDER

73

VA Compromise Sales (Short Sales)

If the value of the veteran’s property has dropped and you, as a realtor, cannot get a contract to pay the loan in full, you may want to consider the VA compromise sale program. If you get a contract equal to the value and the closing costs are reasonable and customary, this program may work for you. With this program, the lender (on behalf of VA) can step in and pay the difference to pay the loan off plus closing costs that are reasonable so that the homeowner can avoid foreclosure. When the lender reviews a case for VA compromise, they look at the case as if it were going to foreclosure versus allowing the VA compromise to go through. There must be a savings in order for the compromise sale to go through. ******************************************************************* If, for example, you submit a contract that equals the value but the value has dropped drastically or the closing costs are too high for whatever reason (or a combination of both factors), the contract will fall through. Funding Fee is only cost that can be added to the loan Current rates (see handout): Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS Debt Checks Referred to earlier.

can step in and pay the difference to pay the loan off plus closing costs that are reasonable so that the homeowner can avoid foreclosure. When the lender reviews a case for VA compromise, they look at the case as if it were going to foreclosure versus allowing the VA compromise to go through. There must be a savings in order for the compromise sale to go through. ******************************************************************* If, for example, you submit a contract that equals the value but the value has dropped drastically or the closing costs are too high for whatever reason (or a combination of both factors), the contract will fall through. Funding Fee is only cost that can be added to the loan. Current rates (see handout): Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans. 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS. Debt Checks Referred to earlier.")

74

VA Compromise Sales (Short Sales)

Contract Sales Price: $ 95,000 Closing Costs: $ 7,800 Total $102,800 Total Debt of $113,619 less Net After Sale of $102,800 = Comp Claim Payment of $10,819 Foreclosure Principal: $110,000 Interest $ 2,019 Foreclosure Costs $ 1,000 Advances $ TOTAL Debt $113,619 *Net Value ,943 Foreclosure Claim $ 16,676 Funding Fee is only cost that can be added to the loan Current rates (see handout): Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS Debt Checks Referred to earlier. Potential Foreclosure Claim of$16,676 – Comp Claim $10,819=$5,857. Savings to VA: $5,857 and VA does not have to take back a property to re-sell. *Note: net value = appraisal of $105,000 less 11.87% = net value of 96,943. The 11.87% is the average cost to acquire and market a foreclosed property.

: Purchase – 2.15% (2.4%-for reservists) Subsequent Use – 3.3% for all veterans. 5% down payment – 1.5% (1.75% for reservists) 10% down payment – 1.25% (1.5% for reservists) IRRRLs - .5% FFPS. Debt Checks Referred to earlier. Potential Foreclosure Claim of$16,676 – Comp Claim $10,819=$5,857. Savings to VA: $5,857 and VA does not have to take back a property to re-sell. *Note: net value = appraisal of $105,000 less 11.87% = net value of 96,943. The 11.87% is the average cost to acquire and market a foreclosed property.")

Similar presentations

>")

Lender must determine and document the borrower’s.>")

249-1800,>")

(adapted from AARP information)>")