Download presentation

Presentation is loading. Please wait.

1

Monopoly

4

Introduction Interpretation of monopoly definition

Monopoly or market power Downward sloping demand curve Price setting and quantity Welfare consequences Sources of monopoly power Profitable pricing strategies

5

Competition recap

6

Introduction Brotherhood for the Respect, Elevation, and Advancement of Dishwashers Impact of achieving goal SR life better for dishwashers LR wages of dishwashers decrease by full amount of tips

7

Introduction Why wages bid down by full amount of tips

Who benefits from tipping Tools for analyzing competitive industry

8

Section 7.1 The competitive firm

9

Competitive Firm Firm sells any quantity wants at going market price

Classic example farm Small part of market served by each firm Horizontal demand curve Products are interchangeable Buyers can easily buy from another producer

11

Revenue TR = P X Q MR ≡ P MR curve is flat Coincides with demand curve

13

Firm’s Supply Decision

Produce good until MR = MC Competitive firm produces a quantity where P = MC Note: P ≡ MR Supply curve MC and supply are inverse functions Supply curve looks like upward sloping portion of MC curve as long as MC curve upward sloping SR and LR supply curves exist for the firm

16

Shutdowns and Exits Does the producer want to produce the good?

Two distinctions Shutdown: firm stops producing the good but still pays fixed costs Exit: firm leaves the industry entirely and no longer faces any costs Firms, in SR, can shutdown but not exit Remains operational if P > AVC In LR, can exit

18

Short-Run Supply Curve

Firms SR supply curve identical to part of SRMC curve that lies above AVC curve Shutdown otherwise Upward sloping due to AC and MC U-shape Diminishing marginal returns to variable factors of production Elasticity of supply Percent change in quantity supplied resulting from a 1% change in price

20

The competitive industry in the short run

Section 7.2 The competitive industry in the short run

21

Competitive Industry in the SR

All firms in industry competitive SR is period of time in which no firm can enter or exit the industry Number of firms cannot change LR is period of time in which any firm can enter or leave the industry Industry’s SR supply curve Sum of SR individual firm supply curves More elastic than individual supply curves

23

Supply, Demand, and Equilibrium

Each firm operates where supply meets demand Industry equilibrium consequence of optimizing behavior on part of individuals and firms Intersecting industry wide supply and industry wide demand

24

Competitive Equilibrium

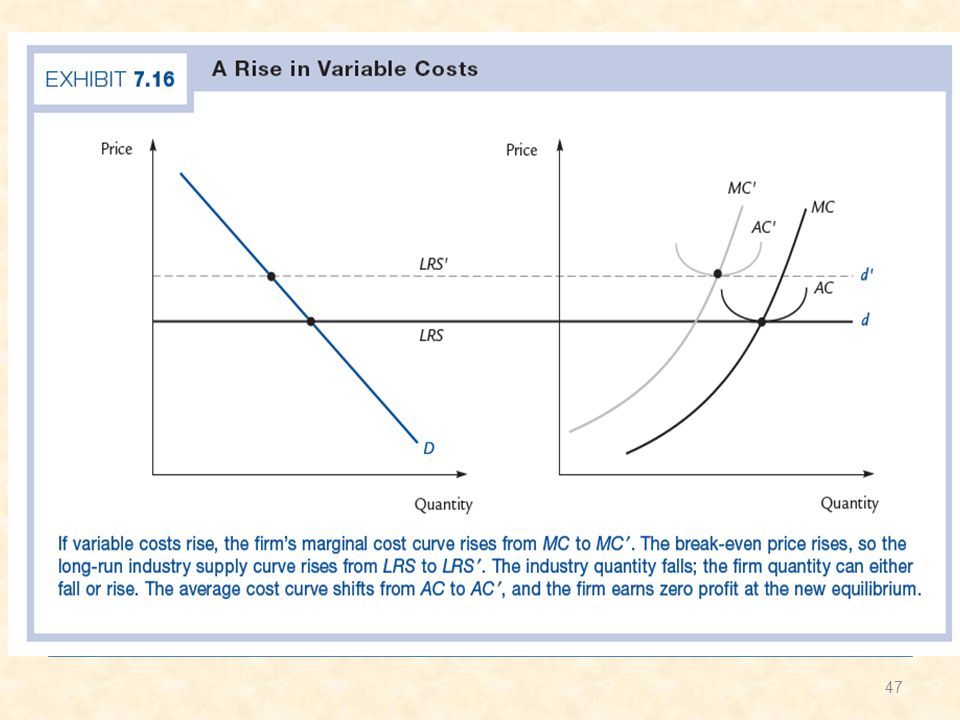

Firms produces where supply (or MC) curve crosses horizontal line at market going price Increase in FC Price and quantity remain unchanged Increase in VC Raises firms MC curve Causes some firms to shutdown Higher market equilibrium price Firm’s output could go up or down Increase in industry demand Increase in firm’s output

curve crosses horizontal line at market going price. Increase in FC. Price and quantity remain unchanged. Increase in VC. Raises firms MC curve. Causes some firms to shutdown. Higher market equilibrium price. Firm’s output could go up or down. Increase in industry demand. Increase in firm’s output.")

26

Change in Fixed Cost Increase in FC

Price and quantity remain unchanged

27

Change in Variable Cost

Increase in VC Raises firms MC curve Causes some firms to shutdown Higher market equilibrium price Firm’s output could go up or down

29

Change in Industry Demand

Increase in industry demand Higher market equilibrium price Increase in firm’s output

31

Industry’s Costs Sum of total cost of all individual firms

To minimize cost of all firms, use equimarginal principle Insure that MC same for all producers in industry Automatic because all firms have same price

32

The competitive firm in the long run

Section 7.3 The competitive firm in the long run

33

Competitive Firm in the LR

Some fixed cost in SR become variable cost in the LR Firms can enter and exit in the LR

34

Profit and the Exit Decision

Profit = TR – TC Costs includes all foregone opportunities SR versus LR supply response Firm LR supply curve more elastic than SR supply curve Shuts down if price of output falls below average variable cost Exits if price of output falls below average cost

36

LRMC and Supply Firms operate where P = LRMC

Remain in industry, LR supply curve identical to LRMC curve Exit decision is made at the point P=AC (note that there is no more fixed cost in the LR)

")

38

The competitive industry in the long run

Section 7.4 The competitive industry in the long run

39

Competitive Industry in the LR

Firms wishing to enter or exit the market do so in the LR, flatting out the LR supply curve So unlike the case in the SR, the LR supply curve is a horizontal line. Important assumption: all firms are identical in costs Break-even price plays an important role here (1) all firms produce at the break-even price; (2) it determines the level of LR supply curve

all firms produce at the break-even price; (2) it determines the level of LR supply curve.")

41

Zero Profit Condition Economic versus accounting profit

Accounting profit refers to total revenue minus total financial cost Economic profit refers to accounting profit minus the value of the best foregone opportunity

43

Industry’s LR Supply Curve

All firms identical Industry supply curve flat at the break-even price Break-even price and the LR supply Break-even price (P = AC) at which a seller earns zero profit LR supply curve identical with part of firm’s LRMC curve lying above LRAC curve

at which a seller earns zero profit. LR supply curve identical with part of firm’s LRMC curve lying above LRAC curve.")

44

Flat LR Supply Curve Flatness based on entry and exit

P < AC, all firms exit P > AC, unlimited number of firms enter LR zero profit equilibrium almost never reached Demand and cost curves shift so often that entry and exit never settles down Approximation to the truth

45

Equilibrium LR same as SR between firm and industry

Market price determined by intersection of industrywide demand and supply Firms face flat demand curves at market price Analysis of changes to equilibrium Changes in FC Changes in VC Changes in demand

49

Application: Government as a Supplier

In SR, government policy to build and operate apartment complex increasing housing In LR, supply curve does not shift Determined by break-even price Number of privately owned apartments withdrawn from the market equals number of apartments built by government

51

Relaxing the Assumptions

Assumption 1: All firms are identical, have identical cost curves True in industries that do not require unusual skills Assumption 2: Cost curves do not change as industry expands or contracts True in industries not large enough to affect input prices Without these assumptions, all firms do not have the same break-even price

52

Constant Cost Constant cost industry Satisfies the 2 assumptions

53

Increasing Cost Increasing cost industry

Break-even price for new entrants increases as industry expands Assumption 1 violated: Less-efficient firms Assumption 2 violated: Factor-price effect LR industry supply curve slopes upward

56

Decreasing Cost Decreasing cost industry

Break-even price for new entrants decreases as industry expands LR industry supply curve slopes downward

58

Applications A tax on motel rooms Tipping the busboy

61

Using the Competitive Model

Fundamentals of competitive analysis Industry versus firm demand and supply SR versus LR Entry and exit decisions

62

Price and output under monopoly

63

Price Pricing operates where MR = MC

MR curves lies everywhere below demand curve

65

Output Lower price to increase output

Monopolist operates on elastic portion of demand curve Ex. Prices of gasoline, oranges, and music CDs No supply curve No going market price

66

Measuring Monopoly Power

67

Welfare Assumption about same industry wide MC curve for competitive and monopolistic industries Social welfare loss under monopoly Marginal value exceeds marginal cost Monopolist could produce additional good

69

Subsidies and Public Policy

Subsidies for monopolist Induce monopolist to provide competitive quantity Arises from “ideal” subsidy Could encourage inefficient production Creates price ceilings Follows rate-of-return regulation

73

Sources of Monopoly Power

Natural monopoly Industry where AC curve decreasing at point where crosses market demand Industry survive only if monopolized

75

Sources, cont. Welfare economics Imperfect competition

Monopoly outcome best for some Imperfect competition Downward pressure on prices Innovation

76

Other Sources of Monopoly Power

Patents Ex. photography Resource monopolies Single firm controls productive input Legal barriers to entry

77

Monopoly, market, and government

This video explains why the concept of monopolies are incompatible with the free market, and actually the result of non-market (government) forces.

forces.")

78

Price Discrimination Charging different prices for identical items

Ability to prevent resell of low-price units

79

First Degree First-degree Charging each customer most willing to pay

Welfare gains

81

Third-Degree Charging different prices in different markets

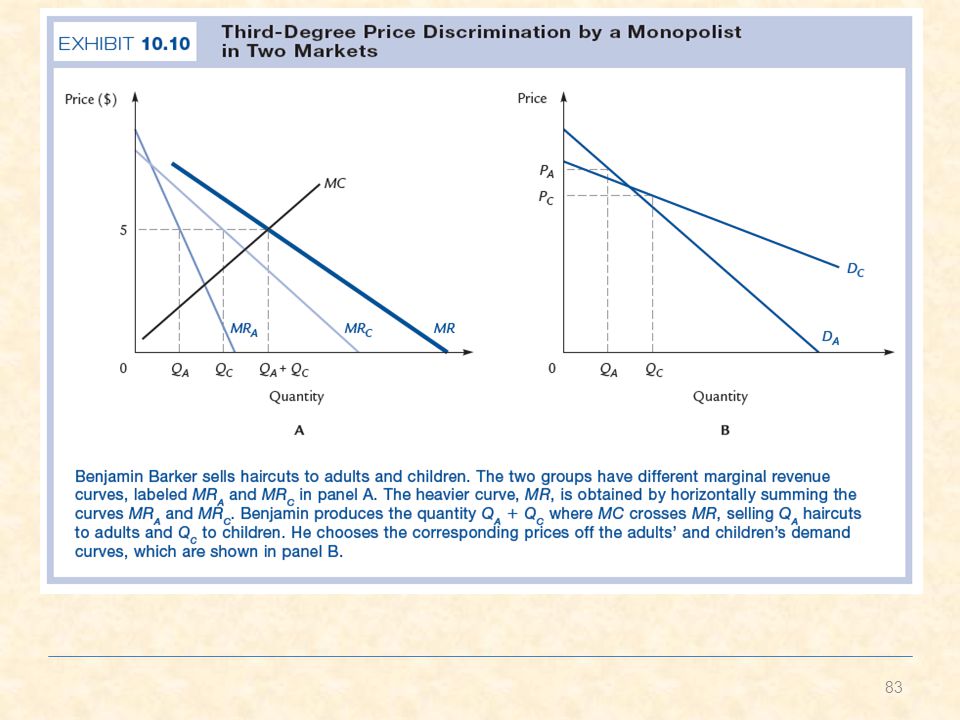

Groups of consumers identifiable Different downward sloping demand curve Producer profit Production of goods where MR same in both markets and equal to MC More elastic demand group receives lower price

84

maxy1, y2 (=p1(y1)y1+ p2(y2)y2-c(y1+y2)).

Third-degree: the most common form of price discrimination (student discounts, senior citizens’ discounts). Suppose there are two groups of people and there is no resale. Then the monopolist’s profit maximization problem becomes maxy1, y2 (=p1(y1)y1+ p2(y2)y2-c(y1+y2)). Hence FOC becomes MR1(y1)=MC(y1+y2)=MR2(y2).

. Suppose there are two groups of people and there is no resale. Then the monopolist’s profit maximization problem becomes. maxy1, y2 (=p1(y1)y1+ p2(y2)y2-c(y1+y2)). Hence FOC becomes. MR1(y1)=MC(y1+y2)=MR2(y2).")

85

Since MR1(y1)=p1(y1)[1-1/|1|] and MR2(y2)=p2(y2)[1-1/|2|], hence p1>p2 if and only if |1|<|2|. The market with lower absolute value of elasticity has a higher price. Quite sensible since elasticity measures how sensitive the group is to price changes. There are some other often-observed practices used by firms with monopoly power.

![Since MR1(y1)=p1(y1)[1-1/|1|] and MR2(y2)=p2(y2)[1-1/|2|], hence p1>p2 if and only if |1|<|2|. The market with lower absolute value of elasticity has a higher price. Quite sensible since elasticity measures how sensitive the group is to price changes.](http://slideplayer.com/slide/1495402/5/images/85/Since+MR1%28y1%29%3Dp1%28y1%29%5B1-1%2F%7C%EF%81%A51%7C%5D+and+MR2%28y2%29%3Dp2%28y2%29%5B1-1%2F%7C%EF%81%A52%7C%5D%2C+hence+p1%3Ep2+if+and+only+if+%7C%EF%81%A51%7C%3C%7C%EF%81%A52%7C.+The+market+with+lower+absolute+value+of+elasticity+has+a+higher+price.+Quite+sensible+since+elasticity+measures+how+sensitive+the+group+is+to+price+changes..jpg "There are some other often-observed practices used by firms with monopoly power.")

86

Second-degree: also known as non-linear pricing since the price per unit of output is not constant, but depends on how much you buy. The monopolist can offer different price-quantity packages so that the consumers can self select. Note that the low-end consumer’s package is distorted so that the high-end consumer will not choose the low-end package.

87

Fig. 25.3

88

Compared to perfect price discrimination, without high-end, low-end is offered higher quantity but still ends up with zero surplus. Without low-end, high end gets zero surplus, now gets positive surplus and the quantity offered is the same. Applying this to air travels, by offering a downgraded product, the airlines can charge the consumers who need flexible travel arrangements more for their tickets.

89

Many many examples of PD

Coupons, rebates, free delivery, coffee lids…… The spirit of PD – to offer lower prices to customers who are more sensitive to price. There is no point to offer coupons if everyone redeemed them, and there is no point to coupons if only a random set of customers redeemed them. Note: almost everything that appears to be price discrimination admits at least one alternative explanation. For example, coupon clippers temp to go shopping when the shop is not crowded.

90

Pricing strategies by monopolist: versioning

Versioning is a practice of offering an inferior product to charge differently for different customers. For example, hardcopy and paperback of the same book. Another example is the same printers designed to print slower deliberately. Strictly speaking, versioning should not be considered as a form of PD in some cases as products involved are different.

91

Pricing strategies by monopolist: Two-Part Tariff

First part Entry fee allows purchase of goods or services Meaning of tariff

92

Pricing strategies by monopolist: Two-Part Tariff

Second part Customers are charged maximum willing to pay Charge competitive price as long as no difference in consumers Charge low initial fee and high usage fee

94

Pricing strategies by monopolist: Two-Part Tariff

By implementing the two-part tariff, a monopoly firm can produces at the competitive market level, enhancing the efficiency. Examples Clubs that charge a member fee and an usage fee Health insurance – copayment increases efficiency.

95

Pricing strategies by monopolist: Bundling

packages of related goods are often offered for sale together: software suite (word processor, spreadsheet, presentation tool), cosmetic products, etc. Bundling may be cost saving or it may be due to complementarities among the goods involved. But there can be reasons involving consumer behavior. Consider the following example. Assume the marginal cost of producing is zero.

, cosmetic products, etc. Bundling may be cost saving or it may be due to complementarities among the goods involved. But there can be reasons involving consumer behavior. Consider the following example. Assume the marginal cost of producing is zero.")

96

Type of consumers word pro spreadsheet A B Suppose the willingness to pay for the bundle is the sum. If each item is sold separately, then revenue will be 400. If instead bundling two goods together, can get the revenue of 440. In other words, the dispersion of willingness to pay may be reduced.

Similar presentations

Grants Chapter 6.>")

Motion Controller Design for A Class of Second-order Systems Center for Self-Organizing Intelligent.>")

>")